You might also like

- Work DescriptionDocument2 pagesWork Descriptionasifabdullah khanNo ratings yet

- Rec Letter MailDocument1 pageRec Letter Mailasifabdullah khanNo ratings yet

- A Case Study On Intel Corporation, 1992: Group-62 (B Section)Document33 pagesA Case Study On Intel Corporation, 1992: Group-62 (B Section)asifabdullah khanNo ratings yet

- A Case Study On Fast Ion Battery: Group-62-BDocument22 pagesA Case Study On Fast Ion Battery: Group-62-Basifabdullah khanNo ratings yet

- Interview PrepDocument1 pageInterview Prepasifabdullah khanNo ratings yet

- 1976 $MM 1981 $MM 1987 $MM 1991 $MM Exhibit 1 Top Integrated Circuit Manufacturers, Worldwide Revenues ($ Millions)Document69 pages1976 $MM 1981 $MM 1987 $MM 1991 $MM Exhibit 1 Top Integrated Circuit Manufacturers, Worldwide Revenues ($ Millions)asifabdullah khanNo ratings yet

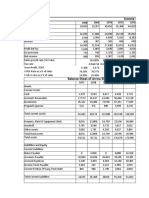

- Income Statement of Arrow Electronics: ItemsDocument78 pagesIncome Statement of Arrow Electronics: Itemsasifabdullah khanNo ratings yet

- Case 01-Group 62Document32 pagesCase 01-Group 62asifabdullah khanNo ratings yet

- "Anti-Dumping Case Study" Course Name: International Finance and Trade Course Code: F-306Document1 page"Anti-Dumping Case Study" Course Name: International Finance and Trade Course Code: F-306asifabdullah khanNo ratings yet

- Icon - College Feedback - Must Follow Feedback For All ICON College WorkDocument3 pagesIcon - College Feedback - Must Follow Feedback For All ICON College Workasifabdullah khanNo ratings yet

- ICON College of Technology and Management Faculty of Business and Management StudiesDocument26 pagesICON College of Technology and Management Faculty of Business and Management Studiesasifabdullah khanNo ratings yet

- ICON-Unit 17 Understanding and Leading Change Feb 2019Document14 pagesICON-Unit 17 Understanding and Leading Change Feb 2019asifabdullah khanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Collection ProceduresDocument8 pagesCollection Proceduresfilfam4545No ratings yet

- Railway Hand Book On Internal ChecksDocument308 pagesRailway Hand Book On Internal ChecksHiraBallabh82% (34)

- Collection LetterDocument4 pagesCollection LetterKiran KumarNo ratings yet

- CAUNCA vs. SALAZAR PDFDocument35 pagesCAUNCA vs. SALAZAR PDFKristela AdraincemNo ratings yet

- MIS in Manufacturing SectorDocument15 pagesMIS in Manufacturing Sectorsagar2go80% (5)

- Modulo de Ignicion S4965A3025E20 - ADocument22 pagesModulo de Ignicion S4965A3025E20 - ADario Amaris MarquezNo ratings yet

- Withholding Taxes Learning ObjectivesDocument8 pagesWithholding Taxes Learning ObjectivesAce AlquinNo ratings yet

- Software Architecture in PracticeDocument717 pagesSoftware Architecture in PracticeDominick100% (6)

- Financial Markets and Institutions: Instructor Teferi Deyuu (PH.D.)Document27 pagesFinancial Markets and Institutions: Instructor Teferi Deyuu (PH.D.)Asfawosen DingamaNo ratings yet

- Aida Hadzibegovic 31499348 Proof of Payment - ThirdPartyDocument1 pageAida Hadzibegovic 31499348 Proof of Payment - ThirdPartyaida.skamo.rezervniNo ratings yet

- Biopharmaceutics 6th Sem Important Questions 2003Document67 pagesBiopharmaceutics 6th Sem Important Questions 2003Asmita TiwariNo ratings yet

- Victoria V Inciong DigestDocument3 pagesVictoria V Inciong DigestXryn MortelNo ratings yet

- Community Relations CHAPTER ONEDocument20 pagesCommunity Relations CHAPTER ONEAdewuyi Alani RidwanNo ratings yet

- Basic Saving Account With Complete KYCDocument2 pagesBasic Saving Account With Complete KYCVarsha100% (1)

- Cheema & Brothers LimitedDocument5 pagesCheema & Brothers LimitedMuhammad AamirNo ratings yet

- Coffee CabanaDocument10 pagesCoffee CabanaAbhay Kumar SinghNo ratings yet

- Prescription Based Selling Skills (PBSS)Document66 pagesPrescription Based Selling Skills (PBSS)Anjum MushtaqNo ratings yet

- CRA01 Confirmation of Residential or Business Address For Online Completion External FormDocument2 pagesCRA01 Confirmation of Residential or Business Address For Online Completion External FormBrandon BothaNo ratings yet

- Iqhbal Delsal: Personal Information Professional SummaryDocument2 pagesIqhbal Delsal: Personal Information Professional SummaryDressa AlexanderNo ratings yet

- I. Programming. Draw A Complete FlowchartDocument4 pagesI. Programming. Draw A Complete FlowchartRey AdrianNo ratings yet

- Ypvpgwl15ypvpgwl15-Study Material-202005110828pm028364-Science 1-1Document5 pagesYpvpgwl15ypvpgwl15-Study Material-202005110828pm028364-Science 1-1AnantNo ratings yet

- Instapdf - in Accounting Ratios Class 12 All Formulas 176Document18 pagesInstapdf - in Accounting Ratios Class 12 All Formulas 176Subhavi DikshitNo ratings yet

- Channel Distribution IMC Tool.Document25 pagesChannel Distribution IMC Tool.Utsav SoniNo ratings yet

- SP-1157 - V 2 5 HSE Specification - HSE TrainingDocument135 pagesSP-1157 - V 2 5 HSE Specification - HSE TrainingSiva NandhamNo ratings yet

- Improve Your Hiring Topgrading EGuide 8 2021Document45 pagesImprove Your Hiring Topgrading EGuide 8 2021Laura SaenzNo ratings yet

- Rights and Duties of AdvocatesDocument11 pagesRights and Duties of AdvocatesSunayana GuptaNo ratings yet

- Corporate Bylaws ofDocument10 pagesCorporate Bylaws ofJoebell VillanuevaNo ratings yet

- Engr. Sheila Marie B. Fronda: Government LicensesDocument7 pagesEngr. Sheila Marie B. Fronda: Government LicenseschellyNo ratings yet

- Purchase Intention in Social Commerce: An Empirical Examination of Perceived Value and Social AwarenessDocument22 pagesPurchase Intention in Social Commerce: An Empirical Examination of Perceived Value and Social Awarenesssatrio pitoyoNo ratings yet

- Marketing Plan of Costa PDFDocument27 pagesMarketing Plan of Costa PDFDaniel C. SeceanuNo ratings yet