You might also like

- 1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapDocument11 pages1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapShesha Nimna GamageNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementShesha Nimna GamageNo ratings yet

- What Is Working Capital Management (WCM)Document26 pagesWhat Is Working Capital Management (WCM)Sudip BaruaNo ratings yet

- Concepts of Working CapitalDocument14 pagesConcepts of Working Capitalkhuranacommunication57No ratings yet

- FM Pointers For ReviewDocument12 pagesFM Pointers For ReviewAngelyne GumabayNo ratings yet

- New Research 2017Document19 pagesNew Research 2017SAKSHI GUPTANo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Unit5 A (A2)Document3 pagesUnit5 A (A2)punte77No ratings yet

- Tutorials ITSMDocument7 pagesTutorials ITSMVINCENT CHUANo ratings yet

- Net Working CapitalDocument10 pagesNet Working CapitalGambit BruNo ratings yet

- Unit 5 Woking CapitalDocument10 pagesUnit 5 Woking CapitalRich ManNo ratings yet

- What Are The Disadvantages of The Perpetual and Period Inventory System?Document4 pagesWhat Are The Disadvantages of The Perpetual and Period Inventory System?Siwei TangNo ratings yet

- Receivable ManagementDocument2 pagesReceivable ManagementR100% (1)

- Working Capital Management: Week 6Document45 pagesWorking Capital Management: Week 6Danica DimaculanganNo ratings yet

- Working CapDocument19 pagesWorking CapJuhi SharmaNo ratings yet

- Working CapitalDocument7 pagesWorking CapitalSreenath SreeNo ratings yet

- Importance of Working Capital ManagementDocument2 pagesImportance of Working Capital Managementxxtha999No ratings yet

- Working Capital ManagementDocument4 pagesWorking Capital ManagementFabia ArshadNo ratings yet

- 1.1. Importance of Working Capital ManagementDocument7 pages1.1. Importance of Working Capital ManagementShesha Nimna GamageNo ratings yet

- New Microsoft Word DocumentDocument4 pagesNew Microsoft Word DocumentMasudRanaNo ratings yet

- Unearned Revenue Liability Balance Sheet Income StatementDocument3 pagesUnearned Revenue Liability Balance Sheet Income Statementrohan rathoreNo ratings yet

- Certain Period, or That They Are Not Getting Payments For Invoices in Fast Enough. A SharpDocument6 pagesCertain Period, or That They Are Not Getting Payments For Invoices in Fast Enough. A Sharpmalik waseemNo ratings yet

- Chapter Two Literature Review: I. Gross Concept II. Net ConceptDocument26 pagesChapter Two Literature Review: I. Gross Concept II. Net ConceptSachchithananthan ArikaranNo ratings yet

- Importance of Working CapitalDocument4 pagesImportance of Working CapitalChaitanya DachepallyNo ratings yet

- Components of Working Capital CashDocument3 pagesComponents of Working Capital Cashkavitachordiya86No ratings yet

- WMDocument31 pagesWMNiña Rhocel YangcoNo ratings yet

- Sources of Short Term FinanceDocument4 pagesSources of Short Term FinancerupeshbwNo ratings yet

- Corporate FininanceDocument10 pagesCorporate FininanceMohan KottuNo ratings yet

- Financial Management Lecture NoteDocument50 pagesFinancial Management Lecture NoteTuryamureeba JuliusNo ratings yet

- Corporate FinanceDocument31 pagesCorporate FinanceAbhi RainaNo ratings yet

- Sources of Working Capital 201 0Document9 pagesSources of Working Capital 201 0rabadiyaNo ratings yet

- Management of Working Capital: Ajeet Kumar ThakurDocument125 pagesManagement of Working Capital: Ajeet Kumar ThakurDilip Kumar YadavNo ratings yet

- Current Liabilities in Financial AccountingDocument2 pagesCurrent Liabilities in Financial AccountingdmugalloyNo ratings yet

- Ms 41Document12 pagesMs 41kvrajan6No ratings yet

- Financial Management Lecture NoteDocument48 pagesFinancial Management Lecture NotesumuNo ratings yet

- BF CH 5Document12 pagesBF CH 5IzHar YousafzaiNo ratings yet

- Financial Management Lecture NoteDocument51 pagesFinancial Management Lecture NoteJade MalaqueNo ratings yet

- Assessment 2 Part ADocument11 pagesAssessment 2 Part AChriseth CruzNo ratings yet

- Teamwork Presentation: Credit ManagementDocument26 pagesTeamwork Presentation: Credit ManagementSashi RajNo ratings yet

- 1cm8numoo 989138Document52 pages1cm8numoo 989138javed1204khanNo ratings yet

- Working Capital Management by Birla GroupDocument39 pagesWorking Capital Management by Birla GroupHajra ShahNo ratings yet

- Business Finance - DocxnotesDocument70 pagesBusiness Finance - DocxnotesKimberly ReignsNo ratings yet

- WCM Unit-LDocument6 pagesWCM Unit-Laanishkashyap61No ratings yet

- Diego Alejandro Muñoz Codigo: 2260388 Preguntas en InglesDocument3 pagesDiego Alejandro Muñoz Codigo: 2260388 Preguntas en InglesDiego Alejandro Muñoz CuevasNo ratings yet

- Accounts Receivable ManagementDocument4 pagesAccounts Receivable Managementsubbu2raj3372No ratings yet

- Unit 5 Topic 1Document9 pagesUnit 5 Topic 1Ibrahim AbidNo ratings yet

- 003251-3.1 Sources of FinanceDocument53 pages003251-3.1 Sources of FinanceMirellaNo ratings yet

- Working Capital Management: Roshankumar S PimpalkarDocument6 pagesWorking Capital Management: Roshankumar S PimpalkarVin BankaNo ratings yet

- 2014 3a. Explain Why Operating Leverage Decreases As A Company Increases Sales and Shifts Away From The Break-Even PointDocument10 pages2014 3a. Explain Why Operating Leverage Decreases As A Company Increases Sales and Shifts Away From The Break-Even PointHiew fuxiangNo ratings yet

- Week 11: Working Capital ManagementDocument4 pagesWeek 11: Working Capital ManagementTeresa Del Campo RodríguezNo ratings yet

- Working Capital ManagementDocument16 pagesWorking Capital Managementsidhantha100% (12)

- Account ReceivablesDocument5 pagesAccount Receivablessubbu2raj3372No ratings yet

- Working Capital On Telecommunication IndustryDocument54 pagesWorking Capital On Telecommunication IndustrySAGARNo ratings yet

- What Is Working Capital ManagementDocument17 pagesWhat Is Working Capital ManagementKhushboo NagpalNo ratings yet

- Working Capital Management: ConceptDocument22 pagesWorking Capital Management: ConceptshimonmakNo ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

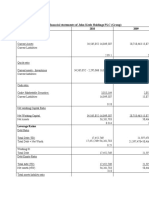

- Ratio Analysis On Financial Statements of John Keels Holdings PLC (Group)Document11 pagesRatio Analysis On Financial Statements of John Keels Holdings PLC (Group)Shesha Nimna GamageNo ratings yet

- Year - Capacity Utilization (%)Document1 pageYear - Capacity Utilization (%)Shesha Nimna GamageNo ratings yet

- Correct AnswersDocument2 pagesCorrect AnswersShesha Nimna GamageNo ratings yet

- AssetsDocument2 pagesAssetsShesha Nimna GamageNo ratings yet

- Question OneDocument16 pagesQuestion OneShesha Nimna GamageNo ratings yet

- 1.1. Importance of Working Capital ManagementDocument7 pages1.1. Importance of Working Capital ManagementShesha Nimna GamageNo ratings yet

- Financial Audit Process: Terms of EngagementDocument1 pageFinancial Audit Process: Terms of EngagementShesha Nimna GamageNo ratings yet

- Annual Statistics 2018Document21 pagesAnnual Statistics 2018Shesha Nimna GamageNo ratings yet

- Blended Learning Desing For ACF 201Document2 pagesBlended Learning Desing For ACF 201Shesha Nimna GamageNo ratings yet

- Student Health Services - 305 Estill Street Berea, KY 40403 - Phone: (859) 985-1415Document4 pagesStudent Health Services - 305 Estill Street Berea, KY 40403 - Phone: (859) 985-1415JohnNo ratings yet

- Presentation (AJ)Document28 pagesPresentation (AJ)ronaldNo ratings yet

- Ghosh, D. P., 1971, Inverse Filter Coefficients For The Computation of Apparent Resistivity Standard Curves For A Horizontally Stratified EarthDocument7 pagesGhosh, D. P., 1971, Inverse Filter Coefficients For The Computation of Apparent Resistivity Standard Curves For A Horizontally Stratified EarthCinthia MtzNo ratings yet

- Elementary Linear Algebra Applications Version 11th Edition Anton Solutions ManualDocument36 pagesElementary Linear Algebra Applications Version 11th Edition Anton Solutions Manualpearltucker71uej95% (22)

- 1654557191.969365 - Signed Contract Application 212143Document11 pages1654557191.969365 - Signed Contract Application 212143ella may sapilanNo ratings yet

- CB Insights Venture Report 2021Document273 pagesCB Insights Venture Report 2021vulture212No ratings yet

- PctcostepoDocument4 pagesPctcostepoRyan Frikkin MurgaNo ratings yet

- Mehta 2021Document4 pagesMehta 2021VatokicNo ratings yet

- Consumer Trend Canvas (CTC) Template 2022Document1 pageConsumer Trend Canvas (CTC) Template 2022Patricia DominguezNo ratings yet

- Caisley, Robert - KissingDocument53 pagesCaisley, Robert - KissingColleen BrutonNo ratings yet

- Womack - Labor History, Industrial Work, Economics, Sociology and Strategic Position PDFDocument237 pagesWomack - Labor History, Industrial Work, Economics, Sociology and Strategic Position PDFhmaravilloNo ratings yet

- IPA Digital Media Owners Survey Autumn 2010Document33 pagesIPA Digital Media Owners Survey Autumn 2010PaidContentUKNo ratings yet

- FORTRESS EUROPE by Ryan BartekDocument358 pagesFORTRESS EUROPE by Ryan BartekRyan Bartek100% (1)

- Girl: Dad, I Need A Few Supplies For School, and I Was Wondering If - . .Document3 pagesGirl: Dad, I Need A Few Supplies For School, and I Was Wondering If - . .AKSHATNo ratings yet

- Hardy-WeinbergEquilibriumSept2012 002 PDFDocument6 pagesHardy-WeinbergEquilibriumSept2012 002 PDFGuntur FaturachmanNo ratings yet

- Fault Detection of Gear Using Spectrum and CepstruDocument6 pagesFault Detection of Gear Using Spectrum and Cepstruराकेश झाNo ratings yet

- Types of CostsDocument9 pagesTypes of CostsPrathna AminNo ratings yet

- Eapp Module 1Document6 pagesEapp Module 1Benson CornejaNo ratings yet

- Sabena Belgian World Airlines vs. CADocument3 pagesSabena Belgian World Airlines vs. CARhea CalabinesNo ratings yet

- MK Slide PDFDocument26 pagesMK Slide PDFPrabakaran NrdNo ratings yet

- Sample File: A of TheDocument6 pagesSample File: A of TheMegan KennedyNo ratings yet

- Calcutta Bill - Abhimanyug@Document2 pagesCalcutta Bill - Abhimanyug@abhimanyugirotraNo ratings yet

- Occupant Response To Vehicular VibrationDocument16 pagesOccupant Response To Vehicular VibrationAishhwarya Priya100% (1)

- Darshan Institute of Engineering & Technology Unit: 7Document9 pagesDarshan Institute of Engineering & Technology Unit: 7AarshenaNo ratings yet

- Supply Chain Analytics For DummiesDocument69 pagesSupply Chain Analytics For DummiesUday Kiran100% (7)

- Endogenic Processes (Erosion and Deposition) : Group 3Document12 pagesEndogenic Processes (Erosion and Deposition) : Group 3Ralph Lawrence C. PagaranNo ratings yet

- Thailand Day 2Document51 pagesThailand Day 2Edsel BuletinNo ratings yet

- Counter-Example NLPDocument8 pagesCounter-Example NLPRafaelBluskyNo ratings yet

- Outbreaks Epidemics and Pandemics ReadingDocument2 pagesOutbreaks Epidemics and Pandemics Readingapi-290100812No ratings yet

- Mohit Maru 4th Semester Internship ReportDocument11 pagesMohit Maru 4th Semester Internship ReportAdhish ChakrabortyNo ratings yet