You might also like

- Cost SheetDocument20 pagesCost SheetKeshviNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Wealth Management & Asset ManagementDocument32 pagesWealth Management & Asset ManagementVineetChandakNo ratings yet

- Economic Order QuantityDocument33 pagesEconomic Order QuantityAhl Medina DunaNo ratings yet

- Throughput AccountingDocument27 pagesThroughput AccountingImran Umar100% (1)

- Tivo Case SolutionDocument15 pagesTivo Case SolutionMONIKA MANDAL (IPM 2016-21 Batch)No ratings yet

- Inventory ManagementDocument23 pagesInventory ManagementAiron Keith Along67% (3)

- 01 CA Inter Costing Book - 2022Document385 pages01 CA Inter Costing Book - 2022Khushi GuptaNo ratings yet

- QMR-Q-M-PR-24 Procedure For Management of Documented InformationDocument7 pagesQMR-Q-M-PR-24 Procedure For Management of Documented InformationMohammedNo ratings yet

- E-GOVERNANCE in BangladeshDocument23 pagesE-GOVERNANCE in BangladeshZafour100% (1)

- pp06 Final PDFDocument16 pagespp06 Final PDFSaleh Al-shaikhNo ratings yet

- Brochure - City Gas DistributionDocument3 pagesBrochure - City Gas DistributionIE_kumarNo ratings yet

- Moa ImmersionDocument7 pagesMoa ImmersionJeriel Gener ApurilloNo ratings yet

- SAP MM Unit Test CasesDocument8 pagesSAP MM Unit Test Caseshemantkinoni100% (1)

- 1 Eoq PDFDocument12 pages1 Eoq PDFLyber PereiraNo ratings yet

- Accounting Fo MaterialDocument15 pagesAccounting Fo Materialzahid khanNo ratings yet

- Material Assignment PDFDocument21 pagesMaterial Assignment PDFjoeyNo ratings yet

- Inventory Management (2021)Document8 pagesInventory Management (2021)JustyNo ratings yet

- Inventory Management - IIMJDocument27 pagesInventory Management - IIMJAnkush PatraNo ratings yet

- Inventory Systems For Independent DemandDocument4 pagesInventory Systems For Independent DemandCharice Anne VillamarinNo ratings yet

- Vishnu VardhanDocument36 pagesVishnu VardhanYogeshwarNo ratings yet

- Corporate Accounting & Costing: Dr. Deepak SharmaDocument13 pagesCorporate Accounting & Costing: Dr. Deepak SharmaDr. Deepak SharmaNo ratings yet

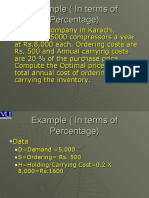

- Example (In Terms of Percentage)Document30 pagesExample (In Terms of Percentage)Anaya MalikNo ratings yet

- Inventories ATs Garcia CristineJoy G BSA-1BDocument4 pagesInventories ATs Garcia CristineJoy G BSA-1BCj GarciaNo ratings yet

- Chapter 8 MowenDocument25 pagesChapter 8 MowenRosamae PialaneNo ratings yet

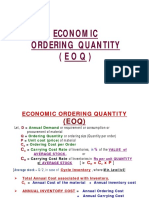

- NB: When The Holding Cost Per Unit Is Not Given, We Usually Take It To Be A Percentage of Purchase Price (C) Per UnitDocument3 pagesNB: When The Holding Cost Per Unit Is Not Given, We Usually Take It To Be A Percentage of Purchase Price (C) Per UnitVans Tee100% (1)

- Manacc 2 Course OutlineDocument10 pagesManacc 2 Course OutlineBenard ChimhondoNo ratings yet

- COST FORMULA - UnlockedDocument28 pagesCOST FORMULA - Unlockedmahinos696No ratings yet

- Presented by Bhavishya Gupta Section "A" ROLL No.-M08032Document12 pagesPresented by Bhavishya Gupta Section "A" ROLL No.-M08032Deepakgupta0001No ratings yet

- FFM1-Ch 2.1. Inventory ManagementDocument37 pagesFFM1-Ch 2.1. Inventory ManagementQuỳnhNo ratings yet

- Module 4Document42 pagesModule 4Gagan Deep SinghNo ratings yet

- Costing Booster Batch: FOR MAY 2023Document244 pagesCosting Booster Batch: FOR MAY 2023Vishal VermaNo ratings yet

- QAD Average CostingDocument12 pagesQAD Average Costingdemisca_alina4179No ratings yet

- Managing Economies of Scale Cycle InventoryDocument33 pagesManaging Economies of Scale Cycle InventoryRohit DuttaNo ratings yet

- Backflush Accounting Feb 2020: Traditional Cost Accounting SystemDocument9 pagesBackflush Accounting Feb 2020: Traditional Cost Accounting SystemMuhammad Noman AnserNo ratings yet

- Costing Booster Batch: Ca InterDocument204 pagesCosting Booster Batch: Ca InterAG GuptaNo ratings yet

- Throughput Accounting: Prepared by Gwizu KDocument26 pagesThroughput Accounting: Prepared by Gwizu KTapiwa Tbone Madamombe100% (1)

- MA2 Mock 1-As - 2023-24Document8 pagesMA2 Mock 1-As - 2023-24daniel.maina2005No ratings yet

- Tools and Techniques of Inventory ManagementDocument4 pagesTools and Techniques of Inventory ManagementNizana p s0% (1)

- Cycle InventoryDocument40 pagesCycle InventoryNiranjan ThirNo ratings yet

- OMT 8604 Logistics in Supply Chain Management: Master of Business AdministrationDocument42 pagesOMT 8604 Logistics in Supply Chain Management: Master of Business AdministrationMr. JahirNo ratings yet

- Coa B1Document39 pagesCoa B1imamulNo ratings yet

- Acct 260 CHAPTER 8Document25 pagesAcct 260 CHAPTER 8John Guy0% (1)

- SCM 13 InventoryDocument39 pagesSCM 13 InventoryVishesh khandelwalNo ratings yet

- Cycle InventoryDocument40 pagesCycle InventoryNiranjan ThirNo ratings yet

- Cycle InventoryDocument13 pagesCycle InventoryUmang ZehenNo ratings yet

- Cost Analysis of Coca-Cola Company - by HakimzadDocument18 pagesCost Analysis of Coca-Cola Company - by HakimzadHakimzad9001 Faisal9001100% (1)

- CHAPTER 10 - Inventory ManagementDocument15 pagesCHAPTER 10 - Inventory ManagementAaminah BeathNo ratings yet

- Material Math SolutionDocument6 pagesMaterial Math SolutionRajibNo ratings yet

- Opm Assignment 2019-1-95-114Document24 pagesOpm Assignment 2019-1-95-114NavidEhsan100% (2)

- Inventory Management: MeaningDocument6 pagesInventory Management: MeaningJeeshan IdrisiNo ratings yet

- Inventory Management: MeaningDocument6 pagesInventory Management: MeaningJeeshan IdrisiNo ratings yet

- Chapter 4Document46 pagesChapter 4Angel Jake Iglesia QuizadaNo ratings yet

- Unit 2Document25 pagesUnit 2din zahurNo ratings yet

- Question1: What Is The EOQ and What Is The Lowest Total Cost?Document7 pagesQuestion1: What Is The EOQ and What Is The Lowest Total Cost?Ali Akand AsifNo ratings yet

- Ac5 HZSTDocument9 pagesAc5 HZSTRafols AnnabelleNo ratings yet

- SOLUTION#01:: WorkingDocument9 pagesSOLUTION#01:: Workingsameed iqbalNo ratings yet

- Backflush Accounting: Traditional Cost Accounting SystemDocument9 pagesBackflush Accounting: Traditional Cost Accounting SystemMuhammad Noman AnserNo ratings yet

- 14 InventoryDocument61 pages14 InventoryraviNo ratings yet

- 16-500 Mcqs of Fundamentals of Accounting PDF For All ExamsDocument50 pages16-500 Mcqs of Fundamentals of Accounting PDF For All ExamsQasim AliNo ratings yet

- Fallsem2017-18 Bmt2013 TH Sjt601 Vl2017181002989 Reference Material I Course Matrl-3 SCM JPM F Sem 2017-18Document39 pagesFallsem2017-18 Bmt2013 TH Sjt601 Vl2017181002989 Reference Material I Course Matrl-3 SCM JPM F Sem 2017-18Pulkit JainNo ratings yet

- Inventory ModelsDocument38 pagesInventory ModelsAngela MenesesNo ratings yet

- Unit 2.2 InventoryDocument90 pagesUnit 2.2 InventorySridhara tvNo ratings yet

- BOB Finance & Credit Specialist Officer SII Model Question Paper 4Document147 pagesBOB Finance & Credit Specialist Officer SII Model Question Paper 4Pranav KumarNo ratings yet

- Costing FormatsDocument43 pagesCosting FormatsUsman KhiljiNo ratings yet

- Cost Booster May 24Document186 pagesCost Booster May 24311812922nishanthininkNo ratings yet

- Short - Term and Mid - Term Finance Chapter - 5 Inventory ManagementDocument1 pageShort - Term and Mid - Term Finance Chapter - 5 Inventory Managementrashed_8929685No ratings yet

- QF207 - Tee Chyng WenDocument4 pagesQF207 - Tee Chyng WenHohoho134No ratings yet

- Bank AlflahDocument39 pagesBank AlflahAli MalikNo ratings yet

- Impact of Gig EconomyDocument8 pagesImpact of Gig EconomyWalaa IbrahimNo ratings yet

- Understanding Business PlanDocument19 pagesUnderstanding Business PlanMalik MohamedNo ratings yet

- PWC To Acquire PRTMDocument2 pagesPWC To Acquire PRTMBRR_DAGNo ratings yet

- 18bba63c U3Document6 pages18bba63c U3Thangamani.R ManiNo ratings yet

- Stock Transaction TaxDocument2 pagesStock Transaction TaxlyzleejoieNo ratings yet

- Green Tech SolutionsDocument5 pagesGreen Tech SolutionsAnadi SaxenaNo ratings yet

- ABIR Global Underwriting Report - 2021Document2 pagesABIR Global Underwriting Report - 2021BernewsAdminNo ratings yet

- EMC Case StudyDocument1 pageEMC Case Studyomar gamalNo ratings yet

- LavazzaDocument2 pagesLavazzajendakimNo ratings yet

- Timestamp: 17-Apr-2023 10:26:01 AMDocument1 pageTimestamp: 17-Apr-2023 10:26:01 AMPruzzwal NandiNo ratings yet

- Receivables Management: Chapter - 4Document7 pagesReceivables Management: Chapter - 4Hussen AbdulkadirNo ratings yet

- Case Study - Visual Merchandising at TitanDocument9 pagesCase Study - Visual Merchandising at TitanVipin Mandyam KadubiNo ratings yet

- Proforma Invoice No - SI20171103 of PONo. 02KINGDAINDEX-2017Document1 pageProforma Invoice No - SI20171103 of PONo. 02KINGDAINDEX-2017lê thu phươngNo ratings yet

- BF - MODULE 1 - INTRO TO FMpart2Document32 pagesBF - MODULE 1 - INTRO TO FMpart2katherine marimonNo ratings yet

- Challenges of International Standards On AuditingDocument7 pagesChallenges of International Standards On AuditingMuhammad Haiqhal Bin Mohd Noor AzmanNo ratings yet

- Sample Agreement To Deliver BitcoinsDocument2 pagesSample Agreement To Deliver BitcoinsMike Caldwell100% (1)

- Client Server ComputingDocument223 pagesClient Server ComputingPuspala Manojkumar100% (5)

- Ranked Positional Weight Method: of Assembly Line BalancingDocument11 pagesRanked Positional Weight Method: of Assembly Line Balancingsai venkata krishnaNo ratings yet

- Final Assignment 3 - HRM in CanadaDocument26 pagesFinal Assignment 3 - HRM in CanadaangeliaNo ratings yet

- UntitledDocument26 pagesUntitledsunil_panchal34100% (1)