You might also like

- Kabir-Kumar (BB Conf Pres)Document30 pagesKabir-Kumar (BB Conf Pres)akbersundraniNo ratings yet

- Banking Business Model CanvasDocument1 pageBanking Business Model CanvasSetiyo BirowoNo ratings yet

- Bankingsystem Structureinpakistan:: Prepared by & Syed Ali Abbas Zaidi MoinDocument12 pagesBankingsystem Structureinpakistan:: Prepared by & Syed Ali Abbas Zaidi MoinmoeenNo ratings yet

- Banking Services Guide - What is a Bank and its FunctionsDocument24 pagesBanking Services Guide - What is a Bank and its Functions004. Amlikar ChaitaliNo ratings yet

- Blueprint of Banking SectorDocument33 pagesBlueprint of Banking SectormayankNo ratings yet

- Indra Itecban Core Banking en BajaDocument4 pagesIndra Itecban Core Banking en BajaJerry KellyNo ratings yet

- Industrial Analysis-Financial Services: Presented To - Prof. Tarun Agarwal SirDocument19 pagesIndustrial Analysis-Financial Services: Presented To - Prof. Tarun Agarwal SirGEETESH KUMAR JAINNo ratings yet

- Axis Mission Statement:: PortfolioDocument5 pagesAxis Mission Statement:: PortfolioHimesh BhaiNo ratings yet

- 66576bos53772 cp5Document75 pages66576bos53772 cp5HemanthNo ratings yet

- HegvakbvhjaDocument12 pagesHegvakbvhjaVamshiNo ratings yet

- Banking Corporate Global Industry PrimerDocument8 pagesBanking Corporate Global Industry PrimerJorge Daniel Aguirre PeraltaNo ratings yet

- How To Make SME Segment ProfitableDocument35 pagesHow To Make SME Segment ProfitableTariq HasanNo ratings yet

- New PPT Ia Group 5Document22 pagesNew PPT Ia Group 5GEETESH KUMAR JAINNo ratings yet

- Banking - Retail - Global Industry PrimerDocument7 pagesBanking - Retail - Global Industry PrimerAnonymous NeRBrZyAUbNo ratings yet

- Assignment 1Document15 pagesAssignment 1Jhilik PradhanNo ratings yet

- EPM-3.1 Performance Evaluation of BanksDocument19 pagesEPM-3.1 Performance Evaluation of BanksSandeep Sonawane100% (1)

- Systems Thinking Assignment Hard & Soft Systems ThinkingDocument9 pagesSystems Thinking Assignment Hard & Soft Systems ThinkingAnshul MehtaNo ratings yet

- A Study of Customer Satisfaction in Yes Bank: Dr. Vibhor Paliwal & Kokila GuptaDocument4 pagesA Study of Customer Satisfaction in Yes Bank: Dr. Vibhor Paliwal & Kokila GuptaDharashree PrustyNo ratings yet

- FintechDocument22 pagesFintechazim asyraf67% (3)

- Overview of Changing Financial ServicesDocument14 pagesOverview of Changing Financial ServicesNazmul H. PalashNo ratings yet

- Development of Financial Institutions On Icici Idbi Ifci - PPTX Suraj KumarDocument48 pagesDevelopment of Financial Institutions On Icici Idbi Ifci - PPTX Suraj Kumarsuraj kumarNo ratings yet

- Cognizant Banking & Financial Services: Solutions OverviewDocument3 pagesCognizant Banking & Financial Services: Solutions Overviewkenfouet ouamba gabinNo ratings yet

- ProjectDocument20 pagesProjectNikhil PatniNo ratings yet

- Value Chain Finance (VCF) : Resource Person: Lisette Van Benthum - FSASDocument20 pagesValue Chain Finance (VCF) : Resource Person: Lisette Van Benthum - FSASHyip ManNo ratings yet

- Corporate Banking: Products & Credit Analysis: Course OutlinesDocument7 pagesCorporate Banking: Products & Credit Analysis: Course OutlinesJhilik PradhanNo ratings yet

- Wolf in Sheep's Clothing - Disruption Ahead For Transaction BankingDocument12 pagesWolf in Sheep's Clothing - Disruption Ahead For Transaction BankingFranzNo ratings yet

- ch-5 EIS PDFDocument75 pagesch-5 EIS PDFInvestor GurujiNo ratings yet

- Intro Mon Pol - Oct 19 ABRDocument150 pagesIntro Mon Pol - Oct 19 ABRSoumya JainNo ratings yet

- Core Banking Systems (CBS)Document19 pagesCore Banking Systems (CBS)Yasir Mohsin KazmiNo ratings yet

- Banking Operations and Products ObjectivesDocument70 pagesBanking Operations and Products ObjectivesShashidhar ReddyNo ratings yet

- Project ppt.-1Document21 pagesProject ppt.-1Shraddha TripathiNo ratings yet

- Commercial Banking OverviewDocument26 pagesCommercial Banking OverviewChinmay KhetanNo ratings yet

- Banking Ope Art IonsDocument26 pagesBanking Ope Art IonsPurti TiwariNo ratings yet

- 4 Corporate BankingDocument31 pages4 Corporate BankingKartik BhartiaNo ratings yet

- Fintech 6Document30 pagesFintech 6Taaran ReddyNo ratings yet

- Business Model - Group 2Document22 pagesBusiness Model - Group 2Akil AfzalNo ratings yet

- Icici Bank: E-Finance For Development - An Indian PerspectiveDocument33 pagesIcici Bank: E-Finance For Development - An Indian Perspectivewasi28No ratings yet

- Retail Banking Services & StrategiesDocument20 pagesRetail Banking Services & StrategiesPurti TiwariNo ratings yet

- Project Management in Banking Industry LDocument73 pagesProject Management in Banking Industry LAnkita ChakravartyNo ratings yet

- SSRN Id3084057Document21 pagesSSRN Id3084057PRINCE PATELNo ratings yet

- Easy Bank Pitch DeckDocument12 pagesEasy Bank Pitch DeckSami LoukilNo ratings yet

- Financial Markets and Services (FMSDocument60 pagesFinancial Markets and Services (FMSPrachi AsawaNo ratings yet

- Advancements in BankingDocument16 pagesAdvancements in BankingGaneshan ParamathmaNo ratings yet

- HW SD-WAN 07 Design Practice (FSI Scenarios)Document53 pagesHW SD-WAN 07 Design Practice (FSI Scenarios)xem phimNo ratings yet

- AUTONO FINTECH Digital Lending Jan 2016 PDFDocument27 pagesAUTONO FINTECH Digital Lending Jan 2016 PDFHitesh DhaddhaNo ratings yet

- Retail BankingDocument20 pagesRetail Bankingjyotinegi1250% (2)

- INDIAN FINANCIAL SYSTEM OVERVIEWDocument35 pagesINDIAN FINANCIAL SYSTEM OVERVIEWRitesh RamanNo ratings yet

- Economics of Banking and Money Seminar 1 SolutionDocument6 pagesEconomics of Banking and Money Seminar 1 SolutionMel AlvaroNo ratings yet

- Topic 2 Financia System and Commerical Bank ManagementDocument60 pagesTopic 2 Financia System and Commerical Bank Managementtalalalmintakh05No ratings yet

- Financial MGT Chapter 1 LectDocument42 pagesFinancial MGT Chapter 1 LectYitayih AsnakeNo ratings yet

- Financial ServicesDocument30 pagesFinancial Servicesmanojkumartanwar05No ratings yet

- Unit I ADocument30 pagesUnit I AManoj Kumar JoshiNo ratings yet

- Indian Banking System and Its Emerging Trends - 2020Document36 pagesIndian Banking System and Its Emerging Trends - 2020RAJ PATELNo ratings yet

- Retail Loans GuideDocument57 pagesRetail Loans Guidemithilesh tabhaneNo ratings yet

- EBF PPT Part 1 Unit 2 Financial Systems NEU 2022Document73 pagesEBF PPT Part 1 Unit 2 Financial Systems NEU 2022Trà My NguyễnNo ratings yet

- Commercial BankDocument21 pagesCommercial Bankafif bin mustakimNo ratings yet

- Notes On Introduction To Financial ServicesDocument18 pagesNotes On Introduction To Financial ServicesKirti Giyamalani100% (1)

- Supply Chain of IciciDocument17 pagesSupply Chain of Icicishan birla100% (1)

- Bank Fundamentals: An Introduction to the World of Finance and BankingFrom EverandBank Fundamentals: An Introduction to the World of Finance and BankingRating: 4.5 out of 5 stars4.5/5 (4)

- Payment Services +payment BanksDocument45 pagesPayment Services +payment BanksSuvajitLaikNo ratings yet

- Bank Regulations 2020Document35 pagesBank Regulations 2020SuvajitLaikNo ratings yet

- Payment Services +payment BanksDocument45 pagesPayment Services +payment BanksSuvajitLaikNo ratings yet

- CBPTM S01-02Document39 pagesCBPTM S01-02SuvajitLaikNo ratings yet

- Bank Marketing - 2020 S 3Document21 pagesBank Marketing - 2020 S 3SuvajitLaikNo ratings yet

- Bank Financial Statements 2020 SDocument54 pagesBank Financial Statements 2020 SSuvajitLaikNo ratings yet

- Bank Regulations 2020Document35 pagesBank Regulations 2020SuvajitLaikNo ratings yet

- A Study On Safety and Supply-Chain of Essentials During The C-19 LockdownDocument8 pagesA Study On Safety and Supply-Chain of Essentials During The C-19 LockdownSuvajitLaikNo ratings yet

- Capital Market Services - Issue Management and Processing (Chapter 8)Document24 pagesCapital Market Services - Issue Management and Processing (Chapter 8)SuvajitLaikNo ratings yet

- 7th & 8th Session SH BB & DelistingDocument23 pages7th & 8th Session SH BB & DelistingSuvajitLaikNo ratings yet

- Private Placements and Private Equity: (CHAPTER 11 & 12)Document22 pagesPrivate Placements and Private Equity: (CHAPTER 11 & 12)SuvajitLaikNo ratings yet

- Bank Marketing - 2020 S 3Document21 pagesBank Marketing - 2020 S 3SuvajitLaikNo ratings yet

- Bank Financial Statements 2020 SDocument54 pagesBank Financial Statements 2020 SSuvajitLaikNo ratings yet

- 3rd & 4th Sesion - UnderwritingDocument32 pages3rd & 4th Sesion - UnderwritingSuvajitLaikNo ratings yet

- Narayana Case SolDocument9 pagesNarayana Case SolSuvajitLaikNo ratings yet

- 5th & 6th Sesion - Debt IssueDocument25 pages5th & 6th Sesion - Debt IssueSuvajitLaikNo ratings yet

- Investment Banking - : Introduction, History, and Their Business Portfolio (Chapter 5 & 6)Document16 pagesInvestment Banking - : Introduction, History, and Their Business Portfolio (Chapter 5 & 6)SuvajitLaikNo ratings yet

- 7th & 8th Session SH BB & DelistingDocument23 pages7th & 8th Session SH BB & DelistingSuvajitLaikNo ratings yet

- Session7 BUYBACKSDocument5 pagesSession7 BUYBACKSSuvajitLaikNo ratings yet

- Session 5 NHL Case StudyDocument9 pagesSession 5 NHL Case StudySuvajitLaikNo ratings yet

- All Numericals Discussed in Class So Far (Excluding Narayana Case)Document17 pagesAll Numericals Discussed in Class So Far (Excluding Narayana Case)SuvajitLaikNo ratings yet

- Manual Instructions Surcharge 80EEBDocument11 pagesManual Instructions Surcharge 80EEBSuprasannaPradhanNo ratings yet

- Solved Carlos Opens A Dry Cleaning Store During The Year He PDFDocument1 pageSolved Carlos Opens A Dry Cleaning Store During The Year He PDFAnbu jaromiaNo ratings yet

- Jiban Bima CorporationDocument88 pagesJiban Bima CorporationPromiti SarkerNo ratings yet

- Who Is The Ostensible OwnerDocument10 pagesWho Is The Ostensible OwnerdeepakNo ratings yet

- Average Rate of Return ExampleDocument1 pageAverage Rate of Return Examplefxn fndNo ratings yet

- Murrey Trading Strategy Lines and Price Action - Trading Strategy GuidesDocument9 pagesMurrey Trading Strategy Lines and Price Action - Trading Strategy Guideshansley cook100% (2)

- Cash and Cash Equivalents GuideDocument15 pagesCash and Cash Equivalents GuideSofia NadineNo ratings yet

- Sri Sai Srinivasa Cotton Industries PVT LTDDocument36 pagesSri Sai Srinivasa Cotton Industries PVT LTDManisha NerellaNo ratings yet

- Screenshot 2022-09-09 at 8.19.41 AMDocument3 pagesScreenshot 2022-09-09 at 8.19.41 AMLaila RamosNo ratings yet

- A Study On Some Financial Ratios of Bangladeshi Companies by TURINDocument41 pagesA Study On Some Financial Ratios of Bangladeshi Companies by TURINTurin Iqbal100% (1)

- 1519545495372Document6 pages1519545495372sumit malikNo ratings yet

- Cfap 5 2019 PKDocument194 pagesCfap 5 2019 PKSummar FarooqNo ratings yet

- How Credit Influences the Business CycleDocument129 pagesHow Credit Influences the Business CycleKim Ritua - Tabudlo40% (5)

- Narrations of Account BooksDocument9 pagesNarrations of Account Bookssham sunderNo ratings yet

- Swan Energy LTDDocument29 pagesSwan Energy LTDvsrsNo ratings yet

- Taxation Law 2 ReviewerDocument34 pagesTaxation Law 2 ReviewerMa. Cielito Carmela Gabrielle G. Mateo100% (1)

- Sierra Leone Fiscal Guide 2020 PDFDocument10 pagesSierra Leone Fiscal Guide 2020 PDFMAlek AMARANo ratings yet

- Analisis Stock Split Terhadap Harga Saham Dan Volume Perdagangan PT Telekomunikasi Indonesia Dan PT Jaya Real PropertyDocument12 pagesAnalisis Stock Split Terhadap Harga Saham Dan Volume Perdagangan PT Telekomunikasi Indonesia Dan PT Jaya Real PropertyIlham MaulanaNo ratings yet

- Teacher's Manual - Financial Acctg 2Document233 pagesTeacher's Manual - Financial Acctg 2Adrian Mallari71% (21)

- IBP Part 05 Inventory Warehouse v02Document77 pagesIBP Part 05 Inventory Warehouse v02Rajesh Kumar Sugumaran100% (1)

- Executive SummaryDocument45 pagesExecutive SummarymaachudaapniNo ratings yet

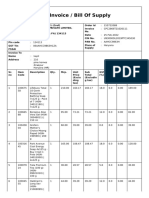

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKapil SinglaNo ratings yet

- CFM Graph DataDocument11 pagesCFM Graph DataMohammed NazeerNo ratings yet

- Section 2. Original Certificates of Title Shall Be Reconstituted From Such of TheDocument2 pagesSection 2. Original Certificates of Title Shall Be Reconstituted From Such of TheAlexylle ConcepcionNo ratings yet

- Answer KeyDocument9 pagesAnswer KeyDeepakshiNo ratings yet

- Post Transactions: Account Title Account Code Debit Credit Balance Date Item Ref Debit CreditDocument5 pagesPost Transactions: Account Title Account Code Debit Credit Balance Date Item Ref Debit CreditPaolo IcangNo ratings yet

- Akrss RegformDocument2 pagesAkrss Regformapi-308916869No ratings yet

- Chap 21 - Leasing (PSAK 73) - E12-12Document27 pagesChap 21 - Leasing (PSAK 73) - E12-12Happy MichaelNo ratings yet

- Internship Report On Allied Bank of PakistanDocument86 pagesInternship Report On Allied Bank of Pakistanshrewd_tycoon94% (17)

- Abu Girma - Determinants Domestic Savings in EthDocument34 pagesAbu Girma - Determinants Domestic Savings in Ethwondimg100% (3)