You might also like

- Advanced Broken - Wing Butterfly Spreads - Random Walk TradingDocument8 pagesAdvanced Broken - Wing Butterfly Spreads - Random Walk TradingjprakashusNo ratings yet

- Home Depot Case StudyDocument5 pagesHome Depot Case StudyAli Shahbaz100% (1)

- Solutions Manual to accompany Engineering Materials ScienceFrom EverandSolutions Manual to accompany Engineering Materials ScienceRating: 4 out of 5 stars4/5 (1)

- PayPal Instant Refunds (Up To 24 Hours) & 7 Days Refunding Method + Ftid 9.1 BonusDocument7 pagesPayPal Instant Refunds (Up To 24 Hours) & 7 Days Refunding Method + Ftid 9.1 Bonusadeel100% (2)

- Potassium in PlantsDocument13 pagesPotassium in PlantsTantoh RowlandNo ratings yet

- Companies Data 2Document15 pagesCompanies Data 2ahmedNo ratings yet

- Chapter 5 MASDocument3 pagesChapter 5 MASDemie demsNo ratings yet

- Miwah Presentation TGDGDocument34 pagesMiwah Presentation TGDGannidadhanizhpoppoNo ratings yet

- Energy Efficiency Copper HydrometallurgyDocument41 pagesEnergy Efficiency Copper Hydrometallurgyalexis diaz0% (1)

- 2022 01 17 - StatementDocument3 pages2022 01 17 - Statementng, ashley yuet heiNo ratings yet

- Capex - Loma Larga - INV MetalsDocument2 pagesCapex - Loma Larga - INV MetalsEzequiel Guillermo Trejo NavasNo ratings yet

- Indonesia's World Class Copper Gold Champion: Investor PresentationDocument21 pagesIndonesia's World Class Copper Gold Champion: Investor PresentationVivi Agustini SampelanNo ratings yet

- Indonesia's World Class Copper Gold Champion: Investor PresentationDocument23 pagesIndonesia's World Class Copper Gold Champion: Investor PresentationPandhuDewantoNo ratings yet

- BandaraJ 1993 EffectsZincBaronFertilizerDocument27 pagesBandaraJ 1993 EffectsZincBaronFertilizerLouise LaneNo ratings yet

- Bewerage Industry RecheckDocument4 pagesBewerage Industry RecheckdishaenvirocareNo ratings yet

- Geology of The Bingham Canyon Porphyry Cu-Mo-Au Deposits, UtahDocument20 pagesGeology of The Bingham Canyon Porphyry Cu-Mo-Au Deposits, UtahajreateguicNo ratings yet

- Bewerage Industry RecheckDocument4 pagesBewerage Industry RecheckdishaenvirocareNo ratings yet

- Answer Marco v1Document4 pagesAnswer Marco v1Marco Augusto Robles AncajimaNo ratings yet

- 388 Ipi Booklet Potassium A Nutrient For LifeDocument24 pages388 Ipi Booklet Potassium A Nutrient For LifeDeepak MeenaNo ratings yet

- Fe Oxide Cu-Au: New FrontiersDocument2 pagesFe Oxide Cu-Au: New Frontiersjlo127No ratings yet

- Aplikasi Pemakaian PocaDocument5 pagesAplikasi Pemakaian PocaAbdul AzizNo ratings yet

- Analysis of Heavy Metals in Soil Samples From The Jakara River Catchment in Kano State, NigeriaDocument7 pagesAnalysis of Heavy Metals in Soil Samples From The Jakara River Catchment in Kano State, NigeriaBrahma Hakim Yuanda HutabaratNo ratings yet

- Eco OrocomsangosturaaspDocument3 pagesEco OrocomsangosturaaspJulian AndresNo ratings yet

- Characteristics and 40Ar/39Ar Geochronology of The Erdenet Cu-Mo Deposit, MongoliaDocument23 pagesCharacteristics and 40Ar/39Ar Geochronology of The Erdenet Cu-Mo Deposit, MongoliaLedPort DavidNo ratings yet

- App August 2017 4Document5 pagesApp August 2017 4Hafizullah AbbaNo ratings yet

- 5.0 Porphyritic Rocks FINAL PDFDocument79 pages5.0 Porphyritic Rocks FINAL PDFOscar Kana HuamaniNo ratings yet

- BBQ 302 Research Presentation: Indian Institute of Technology DelhiDocument28 pagesBBQ 302 Research Presentation: Indian Institute of Technology DelhiMukharJainNo ratings yet

- Sierra Metals Significantly Increases Mineral Reserve Estimate For Yauricocha Mine PeruDocument7 pagesSierra Metals Significantly Increases Mineral Reserve Estimate For Yauricocha Mine PeruSamuel LuisNo ratings yet

- Titian Ulin NewDocument3 pagesTitian Ulin Newjual sepatuNo ratings yet

- The Murchison Goldfields The Murchison GoldfieldsDocument10 pagesThe Murchison Goldfields The Murchison GoldfieldsRegina EfraimNo ratings yet

- Bahan BANGUNANDocument1 pageBahan BANGUNANZhen BuhangNo ratings yet

- 5F. Momentos M1 y M2 - Viga 3 TramosDocument26 pages5F. Momentos M1 y M2 - Viga 3 TramosCriśtian AnðinoNo ratings yet

- 2003 Eng BrochureDocument14 pages2003 Eng Brochure박희상No ratings yet

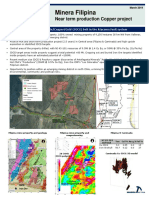

- Minera Filipina: Near Term Production Copper ProjectDocument2 pagesMinera Filipina: Near Term Production Copper ProjectBotacura Minerals acuña moralesNo ratings yet

- DistanceDocument2 pagesDistanceMike Raphy T. VerdonNo ratings yet

- Soybean Foliar FertilizationDocument3 pagesSoybean Foliar FertilizationkasikayichipunzaNo ratings yet

- Redwood Marmato Vs Kori Kollo Memorias XXIII CGB 2018 PDFDocument10 pagesRedwood Marmato Vs Kori Kollo Memorias XXIII CGB 2018 PDFAngela PerillaNo ratings yet

- The Metalliferous Mineral PotentialDocument44 pagesThe Metalliferous Mineral PotentialLIANo ratings yet

- Feasibility Study On The Mesquite Mine Expansion, Imperial County, California Executive SummaryDocument20 pagesFeasibility Study On The Mesquite Mine Expansion, Imperial County, California Executive SummaryLFNo ratings yet

- 10 Years of History of Antamina's Sag MillDocument15 pages10 Years of History of Antamina's Sag MillEdmundo Alfaro DelgadoNo ratings yet

- MINES AUSTRALASIA SEG-Newsletter-80-2010-January-ESDocument27 pagesMINES AUSTRALASIA SEG-Newsletter-80-2010-January-ESAnonymous C0lBgO24iNo ratings yet

- Fertilizare Cu PaieDocument8 pagesFertilizare Cu PaieVadim CodreanNo ratings yet

- Growth and Trace Metal Absorption by in Wetlands Constructed For Landfill Leachate TreatmentDocument15 pagesGrowth and Trace Metal Absorption by in Wetlands Constructed For Landfill Leachate TreatmentAspirant MNo ratings yet

- Reprocessing Historic Tailings - Three Chilean Case StudiesDocument11 pagesReprocessing Historic Tailings - Three Chilean Case StudiesEstebanNo ratings yet

- Existing Coal Storage 1 Coal Storage 2 Stand-By DataDocument5 pagesExisting Coal Storage 1 Coal Storage 2 Stand-By Dataaman131No ratings yet

- Tran 2016Document9 pagesTran 2016raminNo ratings yet

- Sokoman Minerals Corp - May 12, 2020Document2 pagesSokoman Minerals Corp - May 12, 2020johnnemanicNo ratings yet

- Assignment-1: Global Status of Mining in CopperDocument7 pagesAssignment-1: Global Status of Mining in Coppermanikanta nagaNo ratings yet

- Asx Announcement: Drilling Results From Eloise DeepsDocument13 pagesAsx Announcement: Drilling Results From Eloise Deepsenaobona shopNo ratings yet

- 02 FaramarzDocument10 pages02 FaramarzUtibe basseyNo ratings yet

- No. Description Qty Size Total Qty Berat/pc Total Berat Harga (Juta)Document13 pagesNo. Description Qty Size Total Qty Berat/pc Total Berat Harga (Juta)Stevenly HeskiNo ratings yet

- Vadim Fong - MOT AS 91911 Chemistry 2.2B - Part B SubmissionDocument3 pagesVadim Fong - MOT AS 91911 Chemistry 2.2B - Part B SubmissionVadim FongNo ratings yet

- FCR T P R S: Oral Roject Esource TatementDocument11 pagesFCR T P R S: Oral Roject Esource TatementMutlu ZenginNo ratings yet

- To Be ReadyDocument22 pagesTo Be ReadybrhanNo ratings yet

- New PDF Sherwan ReaserchDocument125 pagesNew PDF Sherwan Reaserchsherwan TahseenNo ratings yet

- Australia, New Zealand & Southeast Asia: Vietnam RisingDocument4 pagesAustralia, New Zealand & Southeast Asia: Vietnam RisingStas KuleshNo ratings yet

- Price List: Sole AgentDocument8 pagesPrice List: Sole AgentditoNo ratings yet

- Temperatures and H20 Contents of Low-Mgo High-Alumina BasaltsDocument18 pagesTemperatures and H20 Contents of Low-Mgo High-Alumina BasaltsNiaziBashirNo ratings yet

- Rencana Anggaran BiayaDocument1 pageRencana Anggaran BiayaFajar HarapanNo ratings yet

- Studi Analisis Pengujian Logam Berat Pada Badan Air, Biota Dan Sedimen Di Perairan Muara Das BaritoDocument15 pagesStudi Analisis Pengujian Logam Berat Pada Badan Air, Biota Dan Sedimen Di Perairan Muara Das Baritoimam wahyudiNo ratings yet

- Stachel MAC Shortcourse 2014 Chap01Document29 pagesStachel MAC Shortcourse 2014 Chap01Ali JanNo ratings yet

- Ore Deposit FormationDocument43 pagesOre Deposit FormationGg GNo ratings yet

- Borax As An Alternative Method To Mercury For Gold RecoveryDocument7 pagesBorax As An Alternative Method To Mercury For Gold RecoveryFonfo LawrenceNo ratings yet

- Mineral Beneficiation: Pamphlet 84 APRIL, 1949Document16 pagesMineral Beneficiation: Pamphlet 84 APRIL, 1949Russell HartillNo ratings yet

- Silo - Tips Periodic Table Valency and FormulaDocument7 pagesSilo - Tips Periodic Table Valency and Formulamainakdas73No ratings yet

- Adsorption of Heavy Metals by Exhausted Coffee Grounds As A Potential Treatment Method For Waste WaterDocument4 pagesAdsorption of Heavy Metals by Exhausted Coffee Grounds As A Potential Treatment Method For Waste Waterdesan89923No ratings yet

- HealthcareDocument4 pagesHealthcareClaudia GarciaNo ratings yet

- Birch Gold Information KitDocument20 pagesBirch Gold Information KitRexrgisNo ratings yet

- Dwnload Full Introduction To Contemporary Geography 1st Edition Rubenstein Test Bank PDFDocument27 pagesDwnload Full Introduction To Contemporary Geography 1st Edition Rubenstein Test Bank PDFundidsmartly1944h100% (15)

- Consumer Behaviour For CigarettesDocument14 pagesConsumer Behaviour For CigarettesHarmeet SinghNo ratings yet

- About UsDocument3 pagesAbout UsHamidul Khondoker100% (1)

- A Critique of The Bretton Woods System Other Important Economic OrganizationDocument12 pagesA Critique of The Bretton Woods System Other Important Economic OrganizationKenneth Dave Calucag AguilaNo ratings yet

- HMCost3e PPT Ch16Document36 pagesHMCost3e PPT Ch16GodfreyFrankMwakalingaNo ratings yet

- IC Project Management Project Charter 8556Document7 pagesIC Project Management Project Charter 8556Anh Thi Nguyễn ThịNo ratings yet

- Appellant FinalDocument47 pagesAppellant FinalRoop ChaudharyNo ratings yet

- Global Strategy: Competing Around The WorldDocument26 pagesGlobal Strategy: Competing Around The WorldAIZA BALBALLEGONo ratings yet

- Unit 2: Financial Instruments: Equity and Financial LiabilitiesDocument32 pagesUnit 2: Financial Instruments: Equity and Financial LiabilitiesIsavic AlsinaNo ratings yet

- CP8D Information 2023Document4 pagesCP8D Information 2023Jenson ElectricalNo ratings yet

- Session 7 & 8 - Services BusinessDocument19 pagesSession 7 & 8 - Services BusinessEshan JainNo ratings yet

- Real Property NotesDocument62 pagesReal Property NotesJack ChenowethNo ratings yet

- Part BDocument64 pagesPart Bvandv printsNo ratings yet

- Marketing MixDocument74 pagesMarketing MixVarshaNo ratings yet

- Meeting 6 Setting Prices and Implementing Revenue ManagementDocument35 pagesMeeting 6 Setting Prices and Implementing Revenue Managementsteven sanjayaNo ratings yet

- Proprietary SpecificationDocument6 pagesProprietary SpecificationDebbie Jhem DicamNo ratings yet

- Course List Mena Scholarship ProgrammeDocument7 pagesCourse List Mena Scholarship ProgrammeKassi ZidaneNo ratings yet

- Noon Business SchoolDocument1 pageNoon Business SchoolNaveed Akhtar ButtNo ratings yet

- Letter To Pyramid Altia - 18092022Document3 pagesLetter To Pyramid Altia - 18092022Leh TripNo ratings yet

- Part 5: Distribution DecisionsDocument36 pagesPart 5: Distribution Decisionsumav16No ratings yet

- Using The CRSP/Compustat Merged Database (CCM)Document36 pagesUsing The CRSP/Compustat Merged Database (CCM)sreedharbharathNo ratings yet

- Digital Basics Training - FinalDocument45 pagesDigital Basics Training - Finaldeepika71188No ratings yet