You might also like

- Taxation Sia/Tabag TAX.2807-Income Tax On Corporations MAY 2020Document12 pagesTaxation Sia/Tabag TAX.2807-Income Tax On Corporations MAY 2020Ramainne Ronquillo100% (1)

- Lecture 3 - Income Taxation (Corporate)Document5 pagesLecture 3 - Income Taxation (Corporate)Paula MerrilesNo ratings yet

- Income Taxation Ind PracticeDocument3 pagesIncome Taxation Ind PracticeJanine Tividad100% (1)

- Answers - Business Taxation - Exempt Sales (Chapter 4)Document3 pagesAnswers - Business Taxation - Exempt Sales (Chapter 4)Gino CajoloNo ratings yet

- Local Government Tax PDFDocument9 pagesLocal Government Tax PDFNikko ParNo ratings yet

- Module 1. Transfer TaxesDocument4 pagesModule 1. Transfer TaxesYolly DiazNo ratings yet

- Deductions From Gross Estate (Presentation Slides)Document24 pagesDeductions From Gross Estate (Presentation Slides)KezNo ratings yet

- MSC-Audited FS With Notes - 2014 - CaseDocument12 pagesMSC-Audited FS With Notes - 2014 - CaseMikaela SalvadorNo ratings yet

- Introduction To Donor's Tax (Presentation Slides)Document22 pagesIntroduction To Donor's Tax (Presentation Slides)KezNo ratings yet

- Quiz 1Document11 pagesQuiz 1VIRGIL KIT AUGUSTIN ABANILLANo ratings yet

- TX02 Individual Income Taxpayer and Fringe BenefitDocument15 pagesTX02 Individual Income Taxpayer and Fringe BenefitAce DesabilleNo ratings yet

- Allowable Deductions Part 1Document3 pagesAllowable Deductions Part 1John Rich GamasNo ratings yet

- CPAR Deductions (Batch 89) HandoutDocument26 pagesCPAR Deductions (Batch 89) HandoutlllllNo ratings yet

- Input:Output Tax ReviewerDocument2 pagesInput:Output Tax ReviewerHiedi SugamotoNo ratings yet

- How Much Is The Distributable Income of The GPP?Document2 pagesHow Much Is The Distributable Income of The GPP?Katrina Dela CruzNo ratings yet

- BFINMAX Handout - Gross Profit Variance AnalysisDocument6 pagesBFINMAX Handout - Gross Profit Variance AnalysisDeo CoronaNo ratings yet

- Mas Solutions To Problems Solutions 2018Document14 pagesMas Solutions To Problems Solutions 2018Jahanna Martorillas0% (1)

- Reo Notes - TaxDocument20 pagesReo Notes - TaxgeexellNo ratings yet

- Solution To Donors Vat Other Perecetnages Taxes ExerciseDocument6 pagesSolution To Donors Vat Other Perecetnages Taxes ExerciseMarco Alejandro IbayNo ratings yet

- Final Examination - Income TaxationDocument28 pagesFinal Examination - Income TaxationAisah ReemNo ratings yet

- 2 General Principles of Income TaxationDocument9 pages2 General Principles of Income TaxationDenise ZurbanoNo ratings yet

- Local Government Taxation CasesDocument1 pageLocal Government Taxation CasesRichard Rhamil Carganillo Garcia Jr.No ratings yet

- Mock Deparmentals MASQDocument6 pagesMock Deparmentals MASQHannah Joyce MirandaNo ratings yet

- Dealings in PropertiesDocument9 pagesDealings in PropertiesJoyce Leeann ManansalaNo ratings yet

- VAT Exempt Transactions (TRAIN Law)Document2 pagesVAT Exempt Transactions (TRAIN Law)Pau SantosNo ratings yet

- 05 Input TaxesDocument4 pages05 Input TaxesJaneLayugCabacunganNo ratings yet

- The Regular Corporate Income TaxDocument4 pagesThe Regular Corporate Income TaxReniel Renz AterradoNo ratings yet

- Financial Management RiskDocument11 pagesFinancial Management RisknevadNo ratings yet

- PFRS of SME and SE - Concept MapDocument1 pagePFRS of SME and SE - Concept MapRey OñateNo ratings yet

- A. Four-Variance MethodDocument3 pagesA. Four-Variance MethodMeghan Kaye LiwenNo ratings yet

- (CPAR2016) TAX-8002 (+llamado Notes - INTRODUCTION TO INCOME TAX & TAXATION OF INDIVIDUALS)Document21 pages(CPAR2016) TAX-8002 (+llamado Notes - INTRODUCTION TO INCOME TAX & TAXATION OF INDIVIDUALS)Ralph SantosNo ratings yet

- VAT Exempt TransactionsDocument4 pagesVAT Exempt TransactionsAndehl AguinaldoNo ratings yet

- Construction ContractDocument17 pagesConstruction ContractYvonne Gam-oyNo ratings yet

- Corporate Income TaxDocument6 pagesCorporate Income TaxMark Domingo MendozaNo ratings yet

- Lemon LawDocument5 pagesLemon LawApril VillanuevaNo ratings yet

- Deductions From Gi (Part 2)Document4 pagesDeductions From Gi (Part 2)Koibitz WarrenNo ratings yet

- General Principles of Taxation ReviewerDocument24 pagesGeneral Principles of Taxation ReviewerDaphneNo ratings yet

- CPA Exam Room Assignment May 2019Document22 pagesCPA Exam Room Assignment May 2019Shei La MhaeNo ratings yet

- Activity 5 Gross IncomeDocument6 pagesActivity 5 Gross IncomeRussel Jay CardeñoNo ratings yet

- When, What and How of Insurance Contract (Perfection) When Is It Perfected?Document9 pagesWhen, What and How of Insurance Contract (Perfection) When Is It Perfected?Jexelle Marteen Tumibay PestañoNo ratings yet

- Discuss The Components and Characteristics of Maximization and Minimization ModelDocument5 pagesDiscuss The Components and Characteristics of Maximization and Minimization ModelNicole AutrizNo ratings yet

- Items of Gross Income Subject To RegularDocument2 pagesItems of Gross Income Subject To Regularace zeroNo ratings yet

- Fria QuizDocument2 pagesFria QuizdavidgollaNo ratings yet

- A-Basic Share Capital Transactions2Document4 pagesA-Basic Share Capital Transactions2Sophia Santos0% (1)

- CPAR Estate Tax (Batch 89) HandoutDocument18 pagesCPAR Estate Tax (Batch 89) HandoutlllllNo ratings yet

- Deductions On Gross Estate Part 1Document19 pagesDeductions On Gross Estate Part 1Angel Clarisse JariolNo ratings yet

- CPA Dreams Test BankDocument6 pagesCPA Dreams Test BankMayla MasxcxlNo ratings yet

- Business & Transfer Taxation: Rex B. Banggawan, Cpa, MbaDocument38 pagesBusiness & Transfer Taxation: Rex B. Banggawan, Cpa, Mbajustine reine cornicoNo ratings yet

- Week 1 Principles of Taxation True or FalseDocument4 pagesWeek 1 Principles of Taxation True or FalsekemeeNo ratings yet

- Chapter 01 Introduction To Internal Revenue TaxesDocument12 pagesChapter 01 Introduction To Internal Revenue TaxesNikki BucatcatNo ratings yet

- Tax RemediesDocument13 pagesTax RemediesYan MoretzNo ratings yet

- TAX-401 (Other Percentage Taxes - Part 1)Document5 pagesTAX-401 (Other Percentage Taxes - Part 1)Princess ManaloNo ratings yet

- 3.2 Exercise - RCIT v. MCITDocument1 page3.2 Exercise - RCIT v. MCITGiselle MartinezNo ratings yet

- At Last Minute by HerculesDocument19 pagesAt Last Minute by HerculesFranklin ValdezNo ratings yet

- RFBT - CPAR Pre-Boards in RFBT Batch 87 RFBT - CPAR Pre-Boards in RFBT Batch 87Document11 pagesRFBT - CPAR Pre-Boards in RFBT Batch 87 RFBT - CPAR Pre-Boards in RFBT Batch 87Adelio BalmezNo ratings yet

- ReSA CPA Review Batch 45 Pre-Recorded Lecture VideosDocument2 pagesReSA CPA Review Batch 45 Pre-Recorded Lecture VideosMarielle GonzalvoNo ratings yet

- San Beda College of Law: 2005 C B O Annex B T R CDocument3 pagesSan Beda College of Law: 2005 C B O Annex B T R CRachel LeachonNo ratings yet

- Ch04 Taxation of Corp. TRAIN With Answers 1Document15 pagesCh04 Taxation of Corp. TRAIN With Answers 1Nicole100% (1)

- Ch04 Taxation of CorporationsDocument13 pagesCh04 Taxation of CorporationsKyla ArcillaNo ratings yet

- Acco 20133 - Unit Iii & Iv - CreateDocument35 pagesAcco 20133 - Unit Iii & Iv - CreateHarvey AguilarNo ratings yet

- REO CPA Review: Amendments To The Anti-Money Laundering ActDocument2 pagesREO CPA Review: Amendments To The Anti-Money Laundering ActJuliana ChengNo ratings yet

- 17Q June 2018Document96 pages17Q June 2018Juliana ChengNo ratings yet

- 17Q March 2015Document74 pages17Q March 2015Juliana ChengNo ratings yet

- Bank Secrecy Law and Truth in Lending ActDocument23 pagesBank Secrecy Law and Truth in Lending ActJuliana ChengNo ratings yet

- Anti - Bouncing Checks Law: Batas Pambansa Blg. 22Document36 pagesAnti - Bouncing Checks Law: Batas Pambansa Blg. 22Juliana ChengNo ratings yet

- 17Q June 2016Document95 pages17Q June 2016Juliana ChengNo ratings yet

- 17Q June 2015Document82 pages17Q June 2015Juliana ChengNo ratings yet

- The Greedy and Egoistic LeaderDocument5 pagesThe Greedy and Egoistic LeaderJuliana ChengNo ratings yet

- 17Q June 2017Document104 pages17Q June 2017Juliana ChengNo ratings yet

- 17Q June 2014Document81 pages17Q June 2014Juliana ChengNo ratings yet

- Luxembourg Education SystemDocument6 pagesLuxembourg Education SystemJuliana ChengNo ratings yet

- Audit PlanningDocument15 pagesAudit PlanningJuliana ChengNo ratings yet

- June 26 - Assignemnt 3 CISDocument2 pagesJune 26 - Assignemnt 3 CISJuliana ChengNo ratings yet

- Introduction To AuditingDocument20 pagesIntroduction To AuditingJuliana ChengNo ratings yet

- Completing The AuditDocument26 pagesCompleting The AuditJuliana ChengNo ratings yet

- Module 2 - Relevant CostingDocument7 pagesModule 2 - Relevant CostingJuliana ChengNo ratings yet

- Chapter 8 Discussion QuestionsDocument3 pagesChapter 8 Discussion QuestionsJuliana ChengNo ratings yet

- Module 4 BASIC CONSOLIDATION PROCEDURESDocument21 pagesModule 4 BASIC CONSOLIDATION PROCEDURESJuliana ChengNo ratings yet

- Preliminary Enga Gement ActivitiesDocument7 pagesPreliminary Enga Gement ActivitiesJuliana ChengNo ratings yet

- Over Not Over Tax: Basic Income Table (Tax Code, Section 24 A)Document2 pagesOver Not Over Tax: Basic Income Table (Tax Code, Section 24 A)Juliana ChengNo ratings yet

- UST Golden Notes - Intellectual Property LawDocument32 pagesUST Golden Notes - Intellectual Property LawRay Macote96% (26)

- Admission of A New Partner: Total AssetsDocument10 pagesAdmission of A New Partner: Total AssetsJuliana Cheng100% (5)

- De MinimisDocument5 pagesDe MinimisJuliana ChengNo ratings yet

- IA3 Chapter 2Document7 pagesIA3 Chapter 2Juliana ChengNo ratings yet

- A Joint Project of The Government Accountancy Sector and Corporate Government SectorDocument55 pagesA Joint Project of The Government Accountancy Sector and Corporate Government SectorJuliana ChengNo ratings yet

- IA3 Chapter 1Document4 pagesIA3 Chapter 1Juliana ChengNo ratings yet

- PSA 210 RedraftedDocument40 pagesPSA 210 RedraftedVal Benedict MedinaNo ratings yet

- MQ 1 Inventories Ak PDFDocument4 pagesMQ 1 Inventories Ak PDFJuliana ChengNo ratings yet

- Auditing ProcessDocument11 pagesAuditing ProcessJuliana ChengNo ratings yet

- RR 11 2018 - Annex C - Withholding Agent Sworn DeclarationDocument2 pagesRR 11 2018 - Annex C - Withholding Agent Sworn DeclarationGlaze LlagasNo ratings yet

- Telangana State Power Generation Corporation LTD Kothagudem Thermal Power Station: PalonchaDocument1 pageTelangana State Power Generation Corporation LTD Kothagudem Thermal Power Station: PalonchaKANNE NITHINNo ratings yet

- LIM2019PROBLEMEXERCISESININCOMETAXATIONandTRAINLAW BDocument11 pagesLIM2019PROBLEMEXERCISESININCOMETAXATIONandTRAINLAW BMark MagnoNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BArun SasidharanNo ratings yet

- Ebook Concepts in Federal Taxation 2018 25Th Edition Murphy Test Bank Full Chapter PDFDocument67 pagesEbook Concepts in Federal Taxation 2018 25Th Edition Murphy Test Bank Full Chapter PDFbeckhamquangi9avb100% (9)

- Final Exam Practice - Comprehensive (With Answers)Document22 pagesFinal Exam Practice - Comprehensive (With Answers)Brandon ErbNo ratings yet

- DTP Full NotesDocument114 pagesDTP Full NotesCHAITHRANo ratings yet

- RR No. 25-2020Document2 pagesRR No. 25-2020Kram Ynothna BulahanNo ratings yet

- Pro Forma Balance Sheet Template: Company NameDocument5 pagesPro Forma Balance Sheet Template: Company NamePhương ĐinhNo ratings yet

- PPE - Part - 1. CHAPTER 15Document22 pagesPPE - Part - 1. CHAPTER 15Ms VampireNo ratings yet

- Release NotesDocument10 pagesRelease NotesSirc ElocinNo ratings yet

- Limited Liabilities Partnership FirmDocument14 pagesLimited Liabilities Partnership FirmPraveen JoeNo ratings yet

- The County Collector of Sun Coast County Is Responsible ForDocument1 pageThe County Collector of Sun Coast County Is Responsible ForMuhammad ShahidNo ratings yet

- 01-18-2020 Payslip PDFDocument1 page01-18-2020 Payslip PDFCarla ZanteNo ratings yet

- Final CTPM Chapter 1-ProblemDocument14 pagesFinal CTPM Chapter 1-Problembalaji RNo ratings yet

- Aakansha Sethi - A15 (Direct Tax Assignment)Document19 pagesAakansha Sethi - A15 (Direct Tax Assignment)Aakansha SethiNo ratings yet

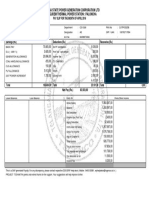

- Concentrix CVG Philippines, Inc.: Description Hrs Total Description Total Taxable Earnings Mandatory Govt ContributionsDocument2 pagesConcentrix CVG Philippines, Inc.: Description Hrs Total Description Total Taxable Earnings Mandatory Govt Contributionszayn malikNo ratings yet

- TDS & VDS Percentage With Section or Service Code - BMCDocument7 pagesTDS & VDS Percentage With Section or Service Code - BMCSyedur RahmanNo ratings yet

- Purchase Order Goods Vat or Non Vat With 2306 and 2307Document17 pagesPurchase Order Goods Vat or Non Vat With 2306 and 2307marivic dyNo ratings yet

- RUB Payment Instructions: Effective As of 1 May 2016Document3 pagesRUB Payment Instructions: Effective As of 1 May 2016Alex10505No ratings yet

- Contemporaray Taxation Acc: 300: PerquisitesDocument5 pagesContemporaray Taxation Acc: 300: PerquisitesALEEM MANSOORNo ratings yet

- Form - 6251Document2 pagesForm - 6251Anonymous JqimV1ENo ratings yet

- Kuis AkuntansiDocument3 pagesKuis AkuntansiNurul Khalishah AzzahraNo ratings yet

- Cost - Vi SemDocument18 pagesCost - Vi SemAR Ananth Rohith BhatNo ratings yet

- Capital Versus Revenue: Some Guidance: Pyott V CIRDocument7 pagesCapital Versus Revenue: Some Guidance: Pyott V CIRAbigail Ruth NawashaNo ratings yet

- Assessment and Returns of IncomeDocument13 pagesAssessment and Returns of IncomeMaster KihimbwaNo ratings yet

- BackgroundDocument6 pagesBackgroundSyed Ali Hussain BokhariNo ratings yet

- SS and SSS Chap 1 To 10 (2020)Document215 pagesSS and SSS Chap 1 To 10 (2020)Dinh TranNo ratings yet

- VE Banking Tests PrTest03Document4 pagesVE Banking Tests PrTest03trivanthNo ratings yet

- SW06Document6 pagesSW06Nadi HoodNo ratings yet