You might also like

- University of West London The Claude Littner Business SchoolDocument18 pagesUniversity of West London The Claude Littner Business SchoolNishani PoornimaNo ratings yet

- Thibault FALLY C181 - International Trade Spring 2018Document58 pagesThibault FALLY C181 - International Trade Spring 2018JYJB WangNo ratings yet

- 1 WtoDocument16 pages1 WtoPrashant SharmaNo ratings yet

- European Business Environment Doing Business in Europe PDFDocument2 pagesEuropean Business Environment Doing Business in Europe PDFTammyNo ratings yet

- Econ 1000 - Test 3Document176 pagesEcon 1000 - Test 3Akram SaiyedNo ratings yet

- Brexit WriteupDocument22 pagesBrexit WriteupHannast Lee0% (1)

- BdE - 2019-Brexit Macro ImpactDocument38 pagesBdE - 2019-Brexit Macro ImpactIrene GarcíaNo ratings yet

- Nafta Safta FinalDocument21 pagesNafta Safta FinalGulab VatsNo ratings yet

- Liou 2016 Political Distance and OwnershipDocument12 pagesLiou 2016 Political Distance and OwnershipSơn Thái HồngNo ratings yet

- Standardization of International Marketing Strategy by Firms From A Developing CountryDocument17 pagesStandardization of International Marketing Strategy by Firms From A Developing CountrynoorNo ratings yet

- Unit 1 IprDocument37 pagesUnit 1 IprVaibhavNo ratings yet

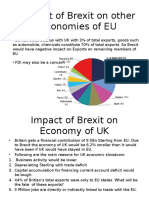

- Impact of Brexit On Other Economies of EUDocument3 pagesImpact of Brexit On Other Economies of EUSumair KhatriNo ratings yet

- Trade: Free Trade Is A Source of Economic GrowthDocument16 pagesTrade: Free Trade Is A Source of Economic GrowthCetty RotondoNo ratings yet

- Interllectual PropertyDocument8 pagesInterllectual PropertyTimothy NshimbiNo ratings yet

- Free Movement of Eu and Non-Eu CitizensDocument6 pagesFree Movement of Eu and Non-Eu CitizensDajana GrgicNo ratings yet

- Chapter Two: International Trade and Investment TheoriesDocument42 pagesChapter Two: International Trade and Investment TheoriesAlayou TeferaNo ratings yet

- CuiWalshZou2014 PDFDocument20 pagesCuiWalshZou2014 PDFLEIDI RUANO ARCOSNo ratings yet

- What Is Brexit?: Enrollment No: 16BSP0092MMDocument4 pagesWhat Is Brexit?: Enrollment No: 16BSP0092MMAbhishek MallikNo ratings yet

- A Study On MIGA (Multilateral Investment Guarantee: Agency)Document26 pagesA Study On MIGA (Multilateral Investment Guarantee: Agency)Pallavi Agarwal100% (2)

- Role of WtoDocument7 pagesRole of Wtomuna1990No ratings yet

- India Infrastructure PPP KPMGDocument37 pagesIndia Infrastructure PPP KPMGAnant Aima100% (1)

- EXPROPRIATIONDocument3 pagesEXPROPRIATIONSAMUEL ManthiNo ratings yet

- Fair and Equitable Treatment in International Investment Law - Taxguru - inDocument6 pagesFair and Equitable Treatment in International Investment Law - Taxguru - inThaleia AndreouNo ratings yet

- Brasserie Du Pêcheur v. Germany, Joined Cases C-46/93 and C-48/93Document2 pagesBrasserie Du Pêcheur v. Germany, Joined Cases C-46/93 and C-48/93Simran BaggaNo ratings yet

- EY BrexitDocument16 pagesEY BrexitInganiour ReillyNo ratings yet

- Name - Adekunle Adesuyi MATRIC NO - 225724 Course Code - Mba 720 Course Title - Business Policy and Strategy AssignmentDocument5 pagesName - Adekunle Adesuyi MATRIC NO - 225724 Course Code - Mba 720 Course Title - Business Policy and Strategy AssignmentRichard AdekunleNo ratings yet

- Ireland and The Impacts of BrexitDocument62 pagesIreland and The Impacts of BrexitSeabanNo ratings yet

- Nagoya Protocol and Its Implications On Pharmaceutical IndustryDocument10 pagesNagoya Protocol and Its Implications On Pharmaceutical IndustryBeroe Inc.No ratings yet

- Sovereign Wealth FundDocument11 pagesSovereign Wealth FundNiharika Satyadev JaiswalNo ratings yet

- Entry Mode StrategyDocument12 pagesEntry Mode StrategyMetiya RatimartNo ratings yet

- US-China Trade Conflict - The Bottom Line PDFDocument8 pagesUS-China Trade Conflict - The Bottom Line PDFMurad Ahmed NiaziNo ratings yet

- The Treaty of Basseterre & OECS Economic UnionDocument15 pagesThe Treaty of Basseterre & OECS Economic UnionOffice of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- The Digital Economy Fact Book 2007Document188 pagesThe Digital Economy Fact Book 2007index8100% (25)

- ECOWAS Trade Liberalization Procedure (ECOWAS)Document10 pagesECOWAS Trade Liberalization Procedure (ECOWAS)watradehub100% (1)

- Theories of International Trade and Investment-Chapter 10 (Textbook - Chapter 5)Document49 pagesTheories of International Trade and Investment-Chapter 10 (Textbook - Chapter 5)Dinesh DinnuNo ratings yet

- O WTO A: Verview of The GreementsDocument12 pagesO WTO A: Verview of The GreementsnobitaenokiNo ratings yet

- Influence of Bilateral Investment Treaties On Customary International LawDocument4 pagesInfluence of Bilateral Investment Treaties On Customary International LawBhavana ChowdaryNo ratings yet

- Qatar Statista DossierDocument54 pagesQatar Statista DossierhhdNo ratings yet

- EY Survey GoodDocument24 pagesEY Survey Goodrserg100No ratings yet

- Foreign Market EntryDocument8 pagesForeign Market EntryMartin Meister GuzmanNo ratings yet

- Introduction of Multilateral Investment Guarantee Agency (Miga)Document34 pagesIntroduction of Multilateral Investment Guarantee Agency (Miga)Minal DalviNo ratings yet

- Regional Economic Integration - Term PaperDocument31 pagesRegional Economic Integration - Term PaperAsm Towheed0% (1)

- Judicial Review of Government ProcurementDocument22 pagesJudicial Review of Government ProcurementMargaret RoseNo ratings yet

- LAW3840 Worksheet1ADROverviewDocument11 pagesLAW3840 Worksheet1ADROverviewRondelleKellerNo ratings yet

- Deloitte On PPPDocument15 pagesDeloitte On PPPindiangal1984No ratings yet

- Impact of Innovation On Economic Development CrossDocument9 pagesImpact of Innovation On Economic Development Crossمصطفى محمود مهديNo ratings yet

- Bahrain Economic Vision 2030Document26 pagesBahrain Economic Vision 2030Thanasate PrasongsookNo ratings yet

- Ical and Comparative Study: Force Majeure and Hardship in The Age of Corona: A HistorDocument54 pagesIcal and Comparative Study: Force Majeure and Hardship in The Age of Corona: A HistorJumadi SarjaNo ratings yet

- APRI PB On Trade AfCFTADocument40 pagesAPRI PB On Trade AfCFTATeniNo ratings yet

- Assignment International Economic LawDocument16 pagesAssignment International Economic LawreazNo ratings yet

- MIGADocument19 pagesMIGAKartikNo ratings yet

- Building The Kra Canal andDocument9 pagesBuilding The Kra Canal andPete Maverick MitchellNo ratings yet

- Presented By: David D'Penha 33 Deepa Thakkar 34 Gayatri Das 48 Kunali Shah 69Document21 pagesPresented By: David D'Penha 33 Deepa Thakkar 34 Gayatri Das 48 Kunali Shah 69David Jonathan D'PenhaNo ratings yet

- Free Movement of GoodsDocument1 pageFree Movement of Goodssiegfried_92No ratings yet

- IMLAM 2013 Moot Problem PDFDocument77 pagesIMLAM 2013 Moot Problem PDFSalma IzzatiiNo ratings yet

- WTO - StructureDocument1 pageWTO - StructureshubhamiitrNo ratings yet

- Lecture - 8 - CompLaw - Shares N DebenturesDocument16 pagesLecture - 8 - CompLaw - Shares N DebenturestaxicoNo ratings yet

- Climate Change and FloodingDocument14 pagesClimate Change and FloodingAlissa MorriesNo ratings yet

- A Corporate Solution to Global Poverty: How Multinationals Can Help the Poor and Invigorate Their Own LegitimacyFrom EverandA Corporate Solution to Global Poverty: How Multinationals Can Help the Poor and Invigorate Their Own LegitimacyNo ratings yet

- Estimating The Effects of Brexit On UKDocument5 pagesEstimating The Effects of Brexit On UKAstha AhujaNo ratings yet

- Sudan Media AssessmentDocument80 pagesSudan Media AssessmentSnehalPoteNo ratings yet

- CookiesDocument14 pagesCookiescodigocarnetNo ratings yet

- Thesis Statement To Kill A MockingbirdDocument6 pagesThesis Statement To Kill A MockingbirdINeedHelpWritingAPaperSiouxFalls100% (2)

- Tube Repair and Protection For DamageDocument112 pagesTube Repair and Protection For Damagesandipwarbhe1234100% (1)

- Weak and Strong WordsDocument12 pagesWeak and Strong WordsCésar MoraisNo ratings yet

- Noise, Nonlinear Distortion and System Parameters: Trinh Xuan Dung, PHDDocument200 pagesNoise, Nonlinear Distortion and System Parameters: Trinh Xuan Dung, PHDKhang Nguyen0% (1)

- Acsnano2c06701 220919 155221Document12 pagesAcsnano2c06701 220919 155221Lee Jay aNo ratings yet

- A Choice of Three BookcasesDocument8 pagesA Choice of Three Bookcasesdanio69No ratings yet

- Application of Lean Six Sigma Methodology Application in Banking FINALDocument58 pagesApplication of Lean Six Sigma Methodology Application in Banking FINALimran24No ratings yet

- 0150511191-A-MH2VYHAS - 150506 Standard Ambinent Outdoor 380-3-50&60 PDFDocument52 pages0150511191-A-MH2VYHAS - 150506 Standard Ambinent Outdoor 380-3-50&60 PDFArshad Mahmood100% (1)

- Top Linux Monitoring ToolsDocument38 pagesTop Linux Monitoring ToolsRutch ChintamasNo ratings yet

- A Study On Students Attitude Towards EntrepreneurshipDocument11 pagesA Study On Students Attitude Towards EntrepreneurshipbevinNo ratings yet

- Netscout Tap Connect Guide 733-0604 PDFDocument76 pagesNetscout Tap Connect Guide 733-0604 PDFFabricio VindasNo ratings yet

- Sir - Tds.taishanc - csm.EB 450GDocument1 pageSir - Tds.taishanc - csm.EB 450GAbdullah SahlyNo ratings yet

- Ternary Phase DiagramDocument34 pagesTernary Phase DiagramCindy PancaNo ratings yet

- Material Safety Data SheetDocument31 pagesMaterial Safety Data SheetDito Anggriawan PrasetyoNo ratings yet

- Gujarat Technological UniversityDocument1 pageGujarat Technological UniversityJainam JoshiNo ratings yet

- Assignments Abroad Times Today 5 April 2023 - 230405 - 102202Document7 pagesAssignments Abroad Times Today 5 April 2023 - 230405 - 102202Blacking MagnonNo ratings yet

- Vertical Structure SystemsDocument51 pagesVertical Structure SystemsANJALI GAUTAMNo ratings yet

- Analysis and Quantification of Mechanical Properties of Various ERW Seam Steel Tubes Manufacturing Processes Using Drift Expanding TestDocument4 pagesAnalysis and Quantification of Mechanical Properties of Various ERW Seam Steel Tubes Manufacturing Processes Using Drift Expanding TestInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Practical Foresight Guide Complete PDFDocument218 pagesPractical Foresight Guide Complete PDFMarlon Flavier TagordaNo ratings yet

- TakeHomeQuiz2.CalcI&II Compre.2ndsem1718Document2 pagesTakeHomeQuiz2.CalcI&II Compre.2ndsem1718Dianne Aicie ArellanoNo ratings yet

- Interactive Form U-1ADocument1 pageInteractive Form U-1ADimas AnugrahNo ratings yet

- RW Correction SymbolsDocument4 pagesRW Correction SymbolsJudyNo ratings yet

- Summary OracleDocument39 pagesSummary OracleRoel DonkerNo ratings yet

- 1.4-Core, Types of Cores, Core Box, Core PrintsDocument39 pages1.4-Core, Types of Cores, Core Box, Core PrintsRamu AmaraNo ratings yet

- Rachna Singh ResumeDocument4 pagesRachna Singh ResumeRachnaSinghNo ratings yet

- Judy Moody Girl Detective Activity KitDocument6 pagesJudy Moody Girl Detective Activity KitCandlewick PressNo ratings yet

- In002174 2020Document1 pageIn002174 2020Bagus DaraNo ratings yet