You might also like

- What To Do SystemDocument38 pagesWhat To Do SystemCheryl Mountainclear100% (1)

- ICICI Bank Cash Deposit Pay in Slip in Hindi English PDFDocument1 pageICICI Bank Cash Deposit Pay in Slip in Hindi English PDFNarendra Kadam100% (1)

- Original PDF Personal Finance 4th Canadian Edition PDFDocument41 pagesOriginal PDF Personal Finance 4th Canadian Edition PDFwilliams.allen71798% (43)

- Digest of Sps Yap Vs Dy (2011)Document2 pagesDigest of Sps Yap Vs Dy (2011)Racquel LevNo ratings yet

- Aula 4 - Colunas - Parte 1Document9 pagesAula 4 - Colunas - Parte 1Anas ShamsudinNo ratings yet

- Agenda-B Details For The Month of Octo 2019 (NIGAMA FORMET) - CE TumkurDocument31 pagesAgenda-B Details For The Month of Octo 2019 (NIGAMA FORMET) - CE Tumkurumera shah aliNo ratings yet

- Econ 111 - Monetary Economics: Summer Session I Tue-Thu, 5:00PM - 7:50PM Center Hall 216 Dr. Hisham FoadDocument18 pagesEcon 111 - Monetary Economics: Summer Session I Tue-Thu, 5:00PM - 7:50PM Center Hall 216 Dr. Hisham FoadJayant Kumar JhaNo ratings yet

- Pengayaan 12Document12 pagesPengayaan 12Supit StevanusNo ratings yet

- IIFL Multicap Advantage PMSDocument30 pagesIIFL Multicap Advantage PMSGokul SudhakaranNo ratings yet

- Base Metals Q2 2010 - OutlookDocument14 pagesBase Metals Q2 2010 - Outlookkoderi100% (1)

- Nations Trust Bank Sri LankaDocument3 pagesNations Trust Bank Sri Lankaudita7208100% (1)

- Aviation Biofuels Develp Conference Oct 2012, Zia Haq, Advanced Biofuels Cost of ProductionDocument10 pagesAviation Biofuels Develp Conference Oct 2012, Zia Haq, Advanced Biofuels Cost of ProductionJuanFleitesNo ratings yet

- Accomplishment-August UpdDocument53 pagesAccomplishment-August UpdGeofel SorianoNo ratings yet

- CIMB-Principal Greater China Equity Fund: Fund Objective Investment VolatilityDocument2 pagesCIMB-Principal Greater China Equity Fund: Fund Objective Investment VolatilityJackie Kennedy JustinNo ratings yet

- GSA SanfranpresentationDocument13 pagesGSA Sanfranpresentationrichardck50No ratings yet

- Long Term ChartsDocument13 pagesLong Term Chartshunghl9726No ratings yet

- Pirates of The ComexDocument10 pagesPirates of The Comexgaoup100% (1)

- Performance (Net) : Lakefront PartnersDocument6 pagesPerformance (Net) : Lakefront Partnersfindgood100% (2)

- Stock ReportDocument2 pagesStock ReportMilton Chilquillo RebattaNo ratings yet

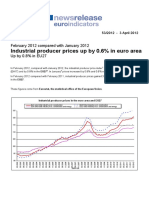

- Industrial Producer Prices Up by 0.6% in Euro AreaDocument6 pagesIndustrial Producer Prices Up by 0.6% in Euro AreaEKAI CenterNo ratings yet

- 3 QTD MCO and Cumulative Outflow AnalysisDocument1 page3 QTD MCO and Cumulative Outflow AnalysisAlberto EstanesNo ratings yet

- Global Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandsDocument16 pagesGlobal Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandslukeniaNo ratings yet

- Odisha SpeechDocument16 pagesOdisha SpeechHari SahooNo ratings yet

- Returns and Risks of Financial SecuritiesDocument71 pagesReturns and Risks of Financial SecuritiesLucas GNo ratings yet

- Sample Letter For All SchemesDocument3 pagesSample Letter For All SchemesChediel MugetaNo ratings yet

- Invest Update - January 2011Document8 pagesInvest Update - January 2011geetanjali04No ratings yet

- Rate Changes - NatWest International 20150731Document1 pageRate Changes - NatWest International 20150731i1153315No ratings yet

- Shree Balaji Interprises: Particulars AmountDocument7 pagesShree Balaji Interprises: Particulars AmountPrajwal MaharjanNo ratings yet

- DSSHD00352800000000029 NewDocument13 pagesDSSHD00352800000000029 Newombir sainiNo ratings yet

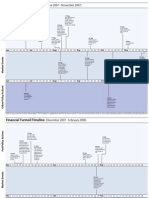

- Crisis TimelineDocument8 pagesCrisis TimelineSoberLookNo ratings yet

- Confronting Economic SlowdownDocument26 pagesConfronting Economic Slowdownepra100% (1)

- Chapter 1Document18 pagesChapter 1asifanisNo ratings yet

- Opening Bell: Market Outlook Today's HighlightsDocument7 pagesOpening Bell: Market Outlook Today's HighlightsShivangi RathiNo ratings yet

- TheArgentineEconomy IAE - Marzo 2011Document43 pagesTheArgentineEconomy IAE - Marzo 2011norbertoNo ratings yet

- Gmo - For Whom The Bond TollsDocument8 pagesGmo - For Whom The Bond Tollsfreemind3682No ratings yet

- The Balance of Payments: Speech Given by DR Martin WealeDocument14 pagesThe Balance of Payments: Speech Given by DR Martin WealeImamjafar SiddiqNo ratings yet

- Daily BonosDocument2 pagesDaily BonosFernando Aaron Zavaleta BurgaNo ratings yet

- LNL Iklcqd /: Page 1 of 5Document5 pagesLNL Iklcqd /: Page 1 of 5Shakeel RizviNo ratings yet

- IIFLAMC Multicap Advantage Presentation Online Version December 2017Document32 pagesIIFLAMC Multicap Advantage Presentation Online Version December 2017paresh revarNo ratings yet

- Aug 03 Erste Group Forex NewsDocument7 pagesAug 03 Erste Group Forex NewsMiir ViirNo ratings yet

- Reza SiregarDocument35 pagesReza SiregarKhoirul AnwarNo ratings yet

- RBI Annual Policy 2011-12 ReviewDocument2 pagesRBI Annual Policy 2011-12 ReviewclevinnashNo ratings yet

- Functional Currency: Proposed Solution Validation 15 September 2015Document7 pagesFunctional Currency: Proposed Solution Validation 15 September 2015caneparuizNo ratings yet

- Money Matters 6 - 2011Document4 pagesMoney Matters 6 - 2011Peggy DoviakNo ratings yet

- Final Porfolio PaperDocument15 pagesFinal Porfolio PaperDeep DualNo ratings yet

- Presentation Amit Oza TFS 080214Document28 pagesPresentation Amit Oza TFS 080214amitozaNo ratings yet

- LNL Iklcqd /: Page 1 of 11Document11 pagesLNL Iklcqd /: Page 1 of 11Sunny KumarNo ratings yet

- FRH Coverage 6Document6 pagesFRH Coverage 6mbaaddiNo ratings yet

- Regulatory Map (2) 2017Document94 pagesRegulatory Map (2) 2017beverly villaruelNo ratings yet

- Statistics Using UNFCCC, IGES and UNEP/Risoe DataDocument10 pagesStatistics Using UNFCCC, IGES and UNEP/Risoe DatacarbonmetricsNo ratings yet

- GNGGN00272440000000066 NewDocument18 pagesGNGGN00272440000000066 NewGajender RaiNo ratings yet

- Managerial Accounting For Managers 3Rd Edition Noreen Test Bank Full Chapter PDFDocument67 pagesManagerial Accounting For Managers 3Rd Edition Noreen Test Bank Full Chapter PDFKennethRiosmqoz100% (12)

- Budget 2009-10: Preview: Expectations A Mirage or RealityDocument11 pagesBudget 2009-10: Preview: Expectations A Mirage or Realityapi-12317095No ratings yet

- Plantation:Closer To B5 Biodiesel Mandate Implementation - 25/03/2010Document3 pagesPlantation:Closer To B5 Biodiesel Mandate Implementation - 25/03/2010Rhb InvestNo ratings yet

- BH Macro Limited 2015Document44 pagesBH Macro Limited 2015Samira SubasicNo ratings yet

- DSNHP15921520000010002 NewDocument6 pagesDSNHP15921520000010002 NewKundan KumarNo ratings yet

- LNL Iklcqd /: Page 1 of 14Document14 pagesLNL Iklcqd /: Page 1 of 14Narendra Singh SimghNo ratings yet

- The Case For Currency Boards: Argentina's Currency Board: From Monetary Panacea To Fiscal StraitjacketDocument7 pagesThe Case For Currency Boards: Argentina's Currency Board: From Monetary Panacea To Fiscal StraitjacketNishit RastogiNo ratings yet

- Presentation On Albanian Financial Management Information System - Afmis November 19th 2020Document40 pagesPresentation On Albanian Financial Management Information System - Afmis November 19th 2020Jacob YeboaNo ratings yet

- Probability Distribution and Statistics: Key Points of LearningDocument24 pagesProbability Distribution and Statistics: Key Points of LearningMohamed HussienNo ratings yet

- No. 6 Oil BanDocument8 pagesNo. 6 Oil BanDom PugliaresiNo ratings yet

- Loan SharkDocument18 pagesLoan SharkPhara MustaphaNo ratings yet

- Bloomberg Rates 2-19-10Document2 pagesBloomberg Rates 2-19-10DonnaAntonucciNo ratings yet

- The Authority To Negotiate and Secure Grants Receive Donations Float Bonds Build Operate Transfer.Document25 pagesThe Authority To Negotiate and Secure Grants Receive Donations Float Bonds Build Operate Transfer.Ressha Gabrielle DomoghoNo ratings yet

- Ethiopia Financial Sector Development The Path To An Efficient Stable and Inclusive Financial SectorDocument112 pagesEthiopia Financial Sector Development The Path To An Efficient Stable and Inclusive Financial SectorAli HassenNo ratings yet

- Act 110 Activity 4 (Answe Sheet - Dimalawang)Document2 pagesAct 110 Activity 4 (Answe Sheet - Dimalawang)Norkan DimalawangNo ratings yet

- Banking Question PapersDocument12 pagesBanking Question Papersmohak khinNo ratings yet

- Reading Comprehension: Skill 2 - Recognizing The Organization of Ideas Skill 3 - Answer Stated Detail QuestionsDocument26 pagesReading Comprehension: Skill 2 - Recognizing The Organization of Ideas Skill 3 - Answer Stated Detail Questionsefha syukurNo ratings yet

- Alexander Van Dyke Math 1050 Project 2 - Mortgage CostsDocument5 pagesAlexander Van Dyke Math 1050 Project 2 - Mortgage Costsapi-233311543No ratings yet

- Ncba Ipf Form - 2022Document12 pagesNcba Ipf Form - 2022san sesNo ratings yet

- Internship Report: Procedure of Letter of Credit (LC), Import, Export and Local Trade of Mutual Trust Bank.'Document84 pagesInternship Report: Procedure of Letter of Credit (LC), Import, Export and Local Trade of Mutual Trust Bank.'Suman AminNo ratings yet

- Impact of Working Capital ManagementDocument77 pagesImpact of Working Capital ManagementYasirNo ratings yet

- Impact of Scripless TradingDocument8 pagesImpact of Scripless TradingAshutosh PandeyNo ratings yet

- Application Form of Society RegistrationDocument7 pagesApplication Form of Society RegistrationShashi K MishraNo ratings yet

- Cash Flow-at-Risk and Debt CapacityDocument18 pagesCash Flow-at-Risk and Debt CapacityC.R. SilvaNo ratings yet

- Garri Potter I Proklyatoe Ditya Chasti Pervaya I Vtoraya Spetsialnoe Repetitsionnoe Izdanie Stsenariya 24149438 2Document44 pagesGarri Potter I Proklyatoe Ditya Chasti Pervaya I Vtoraya Spetsialnoe Repetitsionnoe Izdanie Stsenariya 24149438 2Valeriya SychovaNo ratings yet

- Pangea Mortgage Capital Closes $8.5 Million LoanDocument3 pagesPangea Mortgage Capital Closes $8.5 Million LoanPR.comNo ratings yet

- To MADE EASY Final EditionDocument183 pagesTo MADE EASY Final EditionAnonymous Ey8uMU5n0% (1)

- Cash and Accrual DiscussionDocument2 pagesCash and Accrual DiscussionGloria Beltran100% (1)

- Champaran Gurukul: Banking Made EasyDocument6 pagesChamparan Gurukul: Banking Made EasybiplabmajumderNo ratings yet

- Loan Application FormDocument2 pagesLoan Application Formal lakwenaNo ratings yet

- Quiz 2 TheoryDocument3 pagesQuiz 2 TheoryVanessa SisonNo ratings yet

- Consumer FinanceDocument4 pagesConsumer FinancerhythmkannanNo ratings yet

- UDAANCASESTUDYANSLYSISDocument9 pagesUDAANCASESTUDYANSLYSISMUPPALLA HEMA VARSHITANo ratings yet

- Askari Bank Schedule of Charges PDFDocument20 pagesAskari Bank Schedule of Charges PDFJHKJHKJHKHJHKNo ratings yet

- Enquiry Type Table PDFDocument3 pagesEnquiry Type Table PDFhimanshu khatriNo ratings yet

- Practical Attachment Report 1Document22 pagesPractical Attachment Report 1Tesfu HettoNo ratings yet