You might also like

- Unit IDocument28 pagesUnit I20ce018No ratings yet

- ETM forASEANwebinarDocument14 pagesETM forASEANwebinarTiara SyNo ratings yet

- 140723-d1s2 IndoDocument9 pages140723-d1s2 IndoGinting BerthNo ratings yet

- Draft General Plan of Electricity (Rukn) 2012Document15 pagesDraft General Plan of Electricity (Rukn) 2012Ali Zainal AbidinNo ratings yet

- Pres Kenji AndoDocument35 pagesPres Kenji AndoMikhail BiryukovNo ratings yet

- Chapter 2Document23 pagesChapter 2upper paunglaungNo ratings yet

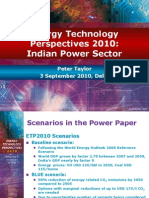

- Power Development Oppourtunites in MyanmarDocument36 pagesPower Development Oppourtunites in MyanmarArun KumarNo ratings yet

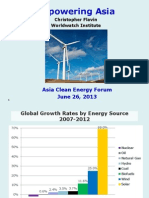

- 3 CFlavin AasdfDB Asia PP Draft June 26 2013Document14 pages3 CFlavin AasdfDB Asia PP Draft June 26 2013aimingzhouadbNo ratings yet

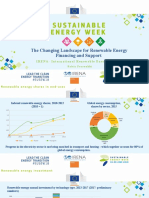

- The Changing Landscape For RE Financing and Support R FerroukhiDocument14 pagesThe Changing Landscape For RE Financing and Support R Ferroukhikarikalcholan mayavanNo ratings yet

- Energy Efficiency and Conservation: GREENSHIP Associate TrainingDocument60 pagesEnergy Efficiency and Conservation: GREENSHIP Associate TrainingNurul Aulia SaputriNo ratings yet

- Growing Energy Nedd and Mitigation Options in IndiaDocument36 pagesGrowing Energy Nedd and Mitigation Options in Indiasm3013No ratings yet

- IRENA REmap Indonesia Summary 2017 PDFDocument14 pagesIRENA REmap Indonesia Summary 2017 PDFwitdono100% (1)

- Key World Energy Statistics 2020Document81 pagesKey World Energy Statistics 2020Amin DehghaniNo ratings yet

- 7th Annual Global Conference On Energy EfficiencyDocument12 pages7th Annual Global Conference On Energy EfficiencyGoh Chin HockNo ratings yet

- Paparan ASTECHNOVA 2021Document13 pagesPaparan ASTECHNOVA 2021nazilul hamidiNo ratings yet

- SIRIM - Overview of PV Industry Rev 1kks by SEDADocument34 pagesSIRIM - Overview of PV Industry Rev 1kks by SEDAIrwan OmarNo ratings yet

- Maderazo Rodriguez Sangalang CE 2103 EDADocument5 pagesMaderazo Rodriguez Sangalang CE 2103 EDAjocelNo ratings yet

- Highlight of RUEN - Ver EnglishDocument15 pagesHighlight of RUEN - Ver EnglishLuthfieSangKaptenNo ratings yet

- Global Electricity Review 2021 IndonesiaDocument15 pagesGlobal Electricity Review 2021 Indonesiaon tanrionoNo ratings yet

- Anurag Atre 3Document19 pagesAnurag Atre 3Kshitij TareNo ratings yet

- Mr. Sabar MD Hashim - Malaysia PresentationDocument27 pagesMr. Sabar MD Hashim - Malaysia PresentationSube OhNo ratings yet

- 04 Chapter1Document21 pages04 Chapter1SALMAN K 2ndNo ratings yet

- 1 - GCEPsymposium2014 - SallyIntroFinalDocument30 pages1 - GCEPsymposium2014 - SallyIntroFinalMoonNo ratings yet

- Energy: Pakistan's Energy Sector 15.1 Energy ConsumptionDocument18 pagesEnergy: Pakistan's Energy Sector 15.1 Energy ConsumptionAmanullah Bashir GilalNo ratings yet

- Energy Efficiency and Conservation Policy in Indonesia: Maritje HutapeaDocument24 pagesEnergy Efficiency and Conservation Policy in Indonesia: Maritje Hutapeapetercheng072No ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFDocument107 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFAnwaruddin SalehNo ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFDocument107 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFIreg TraxNo ratings yet

- Laying The Groundwork For Jatropha-Based Biofuel Industry in The PhilippinesDocument20 pagesLaying The Groundwork For Jatropha-Based Biofuel Industry in The PhilippinesUPLB Office of the Vice Chancellor for Research and ExtensionNo ratings yet

- Country Fiche and Annexes KenyaDocument15 pagesCountry Fiche and Annexes KenyaNyasclemNo ratings yet

- Steve KooninDocument51 pagesSteve KooninMikaela MennenNo ratings yet

- Energy Policy: Swaminathan Mani, Tarun DhingraDocument12 pagesEnergy Policy: Swaminathan Mani, Tarun DhingraAkshat SinghNo ratings yet

- SWITCH-Asia EE MEPS Labeling in Indonesia MR HarrisDocument19 pagesSWITCH-Asia EE MEPS Labeling in Indonesia MR HarrisMuhammad Anjas Abdul KholikNo ratings yet

- ASEAN Energy Statistics Leaflet 2023Document17 pagesASEAN Energy Statistics Leaflet 2023Aom SakornNo ratings yet

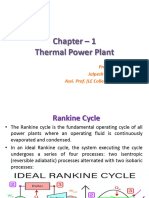

- Thermal Power Plant 355Document11 pagesThermal Power Plant 355rajushamla9927No ratings yet

- Global Energy ConsumptionDocument67 pagesGlobal Energy ConsumptionjuoyjeNo ratings yet

- Policies and Programs On Energy Efficiency and Conservation in IndonesiaDocument35 pagesPolicies and Programs On Energy Efficiency and Conservation in Indonesiapetercheng072No ratings yet

- Role of Ongc in The India's Road Map For Energy SecurityDocument65 pagesRole of Ongc in The India's Road Map For Energy SecuritynanimbaNo ratings yet

- Content Handbook of Energy Economic Statistics of Indonesia 2014 It06jkmDocument135 pagesContent Handbook of Energy Economic Statistics of Indonesia 2014 It06jkmkktahunanNo ratings yet

- Road Map Menuju Kedaulatan Energi Dr. Tumiran DENDocument52 pagesRoad Map Menuju Kedaulatan Energi Dr. Tumiran DENmmissuari100% (2)

- Article On Renewable EnergyDocument14 pagesArticle On Renewable EnergyPoonam YadavNo ratings yet

- Potential of Concentrated Solar Power (CSP) in IndiaDocument27 pagesPotential of Concentrated Solar Power (CSP) in Indiayugam0077No ratings yet

- Ohio's Renewable Portfolio StandardsDocument17 pagesOhio's Renewable Portfolio StandardsglasscityjungleNo ratings yet

- Transportation: University of South FloridaDocument12 pagesTransportation: University of South FloridaSamir ZaghloolNo ratings yet

- Roadmap Biodiesel IndonesiaDocument22 pagesRoadmap Biodiesel IndonesiaSyartina SNo ratings yet

- Key Energy Statistics Handbook 21Document64 pagesKey Energy Statistics Handbook 21Samuel G. Korkulo Jr.No ratings yet

- RE in MalaysiaDocument25 pagesRE in MalaysiaAzraqul IlmiNo ratings yet

- Corporate Catalyst India A Report On Indian Power and Energy IndustryDocument35 pagesCorporate Catalyst India A Report On Indian Power and Energy IndustryThanga PrakashNo ratings yet

- Country Fiche and Annexes Ethiopia PDFDocument15 pagesCountry Fiche and Annexes Ethiopia PDFheaven jadaNo ratings yet

- Areva - OverviewDocument187 pagesAreva - OverviewAnamika singhNo ratings yet

- Energy Transition Mechanism in Indonesia-Seminar ETM-ASEANDocument29 pagesEnergy Transition Mechanism in Indonesia-Seminar ETM-ASEANTiara SyNo ratings yet

- Dirty Business: A Greenpeace Philippines Briefing PaperDocument32 pagesDirty Business: A Greenpeace Philippines Briefing PaperKaykay MoleNo ratings yet

- Dirty Business: A Greenpeace Philippines Briefing PaperDocument32 pagesDirty Business: A Greenpeace Philippines Briefing PaperKaykay MoleNo ratings yet

- Energy Sector Assignment - FinalDocument18 pagesEnergy Sector Assignment - FinalWalid HasanNo ratings yet

- 10 55581-Ejeas 1217357-2824541Document18 pages10 55581-Ejeas 1217357-2824541kanbur.191No ratings yet

- Important PowerDocument14 pagesImportant PowerZoeb MatinNo ratings yet

- 2016 11 01 Webinar 1 1124.04Document67 pages2016 11 01 Webinar 1 1124.04Afian Dwi PrasetyoNo ratings yet

- 2 Energy Vision Pak MZDocument20 pages2 Energy Vision Pak MZbitf03m030100% (2)

- NITI Aayog Government of India: Methanol: A Competitive Alternate FuelDocument24 pagesNITI Aayog Government of India: Methanol: A Competitive Alternate Fuelcivil servicesNo ratings yet

- Renewable Power Generation Costs in 2020From EverandRenewable Power Generation Costs in 2020No ratings yet

- Renewable Power Generation Costs in 2021From EverandRenewable Power Generation Costs in 2021No ratings yet

- Advances in UHV Transmission and DistributionDocument24 pagesAdvances in UHV Transmission and DistributionsalehknNo ratings yet

- Samsung Moteur FrigoDocument27 pagesSamsung Moteur Frigomeone99No ratings yet

- Traditiona L RefrigeratorDocument10 pagesTraditiona L RefrigeratorDara Faye FajardaNo ratings yet

- PH Diagram (R404A)Document5 pagesPH Diagram (R404A)ric leoniso100% (1)

- Steady State Analysis of PMSG PDFDocument16 pagesSteady State Analysis of PMSG PDF1balamanianNo ratings yet

- Privatization of Government AgenciesDocument3 pagesPrivatization of Government AgenciesAristina CantonaNo ratings yet

- Systemair - Вентиляторы 2012Document403 pagesSystemair - Вентиляторы 2012andreys_k-g-uNo ratings yet

- Prices Effective Dated December 01 2022Document8 pagesPrices Effective Dated December 01 2022Ayesha Khan JamilNo ratings yet

- Contents and Function: Institute of Instrumentation and ControlDocument6 pagesContents and Function: Institute of Instrumentation and Controldevidutta_pandaNo ratings yet

- Fuel Injection Pump - InstallDocument9 pagesFuel Injection Pump - InstallYousef RedaNo ratings yet

- MeasurIT Flexim ADMX7407 Project EDF 0809Document1 pageMeasurIT Flexim ADMX7407 Project EDF 0809cwiejkowskaNo ratings yet

- Flygt F-Pump Series PDFDocument8 pagesFlygt F-Pump Series PDFLungisani100% (1)

- Program GECS 2023 - FinalDocument3 pagesProgram GECS 2023 - Finalhuilemoteur2020100% (1)

- 9702 w11 QP 43Document24 pages9702 w11 QP 43Hubbak KhanNo ratings yet

- Eastman 2380 Tech SheetDocument2 pagesEastman 2380 Tech SheetAndy MaxNo ratings yet

- Project Report Hybrid Electric VehicleDocument19 pagesProject Report Hybrid Electric VehicleMeet MehtaNo ratings yet

- GAVSDs - Atlas Copco - Launch New ProductDocument23 pagesGAVSDs - Atlas Copco - Launch New ProductquocthaitnNo ratings yet

- 5555 FT141121 Teslastuff 4 Inch Tesla Coil Plans Vs 1.3sDocument33 pages5555 FT141121 Teslastuff 4 Inch Tesla Coil Plans Vs 1.3sedgarpol100% (1)

- MG-3010 ManualDocument8 pagesMG-3010 ManualRomulo Oliveira AraujoNo ratings yet

- Friction ChartDocument4 pagesFriction ChartSupawat RangsiwongNo ratings yet

- Solar RoadwaysDocument16 pagesSolar RoadwaysAnkit KumarNo ratings yet

- Water in Morocco (1)Document3 pagesWater in Morocco (1)maryam.biroukNo ratings yet

- A Closer Look at State of Charge and State Health Estimation Techniques ...Document8 pagesA Closer Look at State of Charge and State Health Estimation Techniques ...Adri PratamaNo ratings yet

- 1996-2004 - Ford4.6Mustang Mustang Mustang Mustang GTDocument40 pages1996-2004 - Ford4.6Mustang Mustang Mustang Mustang GTPa RaNo ratings yet

- TOFD by TempleDocument444 pagesTOFD by TempleAlejandro Mejia RodriguezNo ratings yet

- KT The LoraxDocument4 pagesKT The Loraxapi-291571366No ratings yet

- Structure of Atom PDFDocument0 pagesStructure of Atom PDFabhishekaks97No ratings yet

- DesconDocument3 pagesDesconUnza TabassumNo ratings yet

- Philips Technical Review, Volume 19, 1957/58, No.1-2Document369 pagesPhilips Technical Review, Volume 19, 1957/58, No.1-2MarcoNo ratings yet

- Petromoc, SA Petr Ó Leos de Mo Ç AmbiqueDocument16 pagesPetromoc, SA Petr Ó Leos de Mo Ç AmbiqueFredNo ratings yet