You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Valuing Compulsorily Convertible Debentures: ExampleDocument3 pagesValuing Compulsorily Convertible Debentures: ExamplePRITEENo ratings yet

- Cell Name Original Value Final ValueDocument6 pagesCell Name Original Value Final ValuePRITEENo ratings yet

- Exercise #1: Transactions of Bud's Computer Are As FollowsDocument19 pagesExercise #1: Transactions of Bud's Computer Are As FollowsMejias, Janrey80% (10)

- IRC AAA Notes (Clean) - Kindly Print This OutDocument101 pagesIRC AAA Notes (Clean) - Kindly Print This OutAhmad Rizal100% (1)

- Ch11 Beams12ge SMDocument28 pagesCh11 Beams12ge SMKharisma Pardede33% (3)

- RECRUITMENT AND SELECTION in HDFC BANK PDFDocument81 pagesRECRUITMENT AND SELECTION in HDFC BANK PDFapura desai100% (1)

- 202E13Document24 pages202E13Sammy Ben MenahemNo ratings yet

- Standing Order ActDocument13 pagesStanding Order ActPRITEENo ratings yet

- Walter and Gordon Models - ExamplesDocument4 pagesWalter and Gordon Models - ExamplesPRITEENo ratings yet

- Case Problem 3Document11 pagesCase Problem 3PRITEENo ratings yet

- Texago Corporation Case ExhibitDocument7 pagesTexago Corporation Case ExhibitPRITEENo ratings yet

- Relative Valuation - Example PDFDocument1 pageRelative Valuation - Example PDFPRITEENo ratings yet

- Class 01 (A) Masih - IIM-Microsoft Advanced Excel TrainingDocument85 pagesClass 01 (A) Masih - IIM-Microsoft Advanced Excel TrainingPRITEENo ratings yet

- Coverage and Related Ratios - CompletedDocument8 pagesCoverage and Related Ratios - CompletedPRITEENo ratings yet

- Cell Name Original Value Final ValueDocument4 pagesCell Name Original Value Final ValuePRITEENo ratings yet

- Cell Name Original Value Final ValueDocument6 pagesCell Name Original Value Final ValuePRITEENo ratings yet

- Finance Quiz - 1 2019 SET A: (3 Marks)Document2 pagesFinance Quiz - 1 2019 SET A: (3 Marks)PRITEENo ratings yet

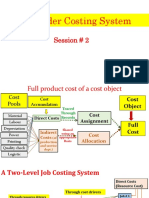

- Session # 7: Lilac Flour Mills: Joint Product and By-Product CostingDocument8 pagesSession # 7: Lilac Flour Mills: Joint Product and By-Product CostingPRITEENo ratings yet

- BRAND: Frito-Lay PRODUCT: Lay's: Missed ImagesDocument2 pagesBRAND: Frito-Lay PRODUCT: Lay's: Missed ImagesPRITEENo ratings yet

- Brand Name: Cadbury Dairy Milk Product Category: ChocolateDocument15 pagesBrand Name: Cadbury Dairy Milk Product Category: ChocolatePRITEE100% (1)

- Destin Brass 2019 (SV)Document11 pagesDestin Brass 2019 (SV)PRITEENo ratings yet

- COLORSCOPE 2019 (SV)Document15 pagesCOLORSCOPE 2019 (SV)PRITEENo ratings yet

- Chapter 1: An Overview: What Is An Organization?Document13 pagesChapter 1: An Overview: What Is An Organization?PRITEENo ratings yet

- ME Quiz 3 PDFDocument15 pagesME Quiz 3 PDFPRITEENo ratings yet

- Assignment OR1Document5 pagesAssignment OR1PRITEENo ratings yet

- Macro NotesDocument29 pagesMacro NotesPRITEENo ratings yet

- ME SingaporeDocument2 pagesME SingaporePRITEENo ratings yet

- Group 7 SingaporeDocument7 pagesGroup 7 SingaporePRITEENo ratings yet

- Mail Notes After Midterm - MacroDocument14 pagesMail Notes After Midterm - MacroPRITEENo ratings yet

- Tata Consultancy Services LimitedDocument4 pagesTata Consultancy Services LimitedPRITEENo ratings yet

- IGD ProjectDocument3 pagesIGD ProjectPRITEENo ratings yet

- Tata Consultancy Services LimitedDocument4 pagesTata Consultancy Services LimitedPRITEENo ratings yet

- ACT421 Term PaperDocument30 pagesACT421 Term PaperNadia IslamNo ratings yet

- Efficient Capital MarketsDocument25 pagesEfficient Capital MarketsAshik Ahmed NahidNo ratings yet

- DoneDocument275 pagesDoneNeha TalwarNo ratings yet

- Goa Institute of Management: Post Graduate Diploma in Management (PGDM) Term IVDocument4 pagesGoa Institute of Management: Post Graduate Diploma in Management (PGDM) Term IVAKASH BODHANINo ratings yet

- Cenon Cervantes in His Own Behalf. Office of The Solicitor General Pompeyo Diaz and Solicitor Felix V. Makasiar For RespondentDocument7 pagesCenon Cervantes in His Own Behalf. Office of The Solicitor General Pompeyo Diaz and Solicitor Felix V. Makasiar For RespondentPrinceNo ratings yet

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument9 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balancesourav84No ratings yet

- Fortress FundDocument5 pagesFortress FundTuriyaNo ratings yet

- Cfa Level III 4 Months Study PlanDocument21 pagesCfa Level III 4 Months Study Planzev zNo ratings yet

- ITDocument4 pagesITNamnam PacheNo ratings yet

- Internship ReportDocument30 pagesInternship ReportSmriti BhattaraiNo ratings yet

- 1519 Loza, JesusDocument17 pages1519 Loza, JesusIsabella Kings100% (1)

- b8.Makro-Monetary PolicyDocument19 pagesb8.Makro-Monetary PolicyEvan AlviyanNo ratings yet

- FRM StudyGuide Changes FINAL 2Document12 pagesFRM StudyGuide Changes FINAL 2Saurabh PramanickNo ratings yet

- Performance Appr Comm BankDocument12 pagesPerformance Appr Comm Bankbipinjaiswal123No ratings yet

- P01Document11 pagesP01loveshare0% (1)

- Chapter 11Document27 pagesChapter 11Sufyan KhanNo ratings yet

- VKDocument4 pagesVKjyottsnaNo ratings yet

- National Highways Infra Trust: and Thus To Raise Further Debt." On Page 36Document1,837 pagesNational Highways Infra Trust: and Thus To Raise Further Debt." On Page 36Someshwar Rao ThakkallapallyNo ratings yet

- Academy ForumIAS Prelims Test 10 Dec 22Document197 pagesAcademy ForumIAS Prelims Test 10 Dec 22Shoukath ShaikNo ratings yet

- Advanced ExcelDocument6 pagesAdvanced ExcelKeith Parker100% (4)

- "Foreign Exchange Management": Summer Project ONDocument59 pages"Foreign Exchange Management": Summer Project ONbhushanpawar5No ratings yet

- Dollar To Naira Black Market Exchange Rate NGNRDocument1 pageDollar To Naira Black Market Exchange Rate NGNRaprildacayananNo ratings yet

- Private Sector Banks Comparative Analysis 1HFY22Document12 pagesPrivate Sector Banks Comparative Analysis 1HFY22Tushar Mohan0% (1)

- Gold Is Money and Nothing Else 100120Document60 pagesGold Is Money and Nothing Else 100120mengesha abyeNo ratings yet

- Assignment On Financial ManagementDocument22 pagesAssignment On Financial ManagementSimran VirmaniNo ratings yet