You might also like

- Parfums Cacharel de L'Oréal 1997-2007:: Decoding and Revitalizing A Classic BrandDocument21 pagesParfums Cacharel de L'Oréal 1997-2007:: Decoding and Revitalizing A Classic BrandrheaNo ratings yet

- Google 2020 E-Conomy SEA 2020 IndonesiaDocument18 pagesGoogle 2020 E-Conomy SEA 2020 IndonesiaFarjumzalNo ratings yet

- Wheelen Smbp13 PPT 01Document36 pagesWheelen Smbp13 PPT 01Ah BiiNo ratings yet

- 51 - Rewarding Special GroupsDocument10 pages51 - Rewarding Special GroupsmitalptNo ratings yet

- Corporate-Level Strategy: Three Key Issues Facing The CorporationDocument30 pagesCorporate-Level Strategy: Three Key Issues Facing The CorporationAshish ShuklaNo ratings yet

- Establishing A Customer FocusDocument5 pagesEstablishing A Customer FocusAditya KurniawanNo ratings yet

- Questionnaire DesignDocument24 pagesQuestionnaire Designशिशिर ढकालNo ratings yet

- Basil Dellor - Driving Innovation - CompletedDocument23 pagesBasil Dellor - Driving Innovation - CompletedEric Frempong AmponsahNo ratings yet

- CHAPTER 1 - Race Without A Finish Line PDFDocument2 pagesCHAPTER 1 - Race Without A Finish Line PDFEduardo WanderleyNo ratings yet

- OrientationDocument8 pagesOrientationNitesh KhatiwadaNo ratings yet

- Ilham Habibie-Wantiknas-Audiensi Menteri BappenasDocument21 pagesIlham Habibie-Wantiknas-Audiensi Menteri BappenasumarhidayatNo ratings yet

- Wheelen 14e ch01Document40 pagesWheelen 14e ch01franky sunaryo100% (1)

- Strategic Intent 3Document22 pagesStrategic Intent 3niteshvnair100% (1)

- Wheelen 14e ch02Document33 pagesWheelen 14e ch02franky sunaryoNo ratings yet

- Business StrategyDocument23 pagesBusiness Strategywilsonngary100% (1)

- Economic Outlook 2021Document198 pagesEconomic Outlook 2021Die EwigkeitNo ratings yet

- PLN UIP Kitsum Quarterly SummitDocument37 pagesPLN UIP Kitsum Quarterly SummitEnggal FurniajiNo ratings yet

- 2022 Tech Education Day - Info DeckDocument10 pages2022 Tech Education Day - Info DeckAnonymous UpWci5No ratings yet

- How To Design A QuestionnaireDocument3 pagesHow To Design A QuestionnaireMithun SahaNo ratings yet

- Building Customer Satisfaction Through Quality, Service, and ValueDocument19 pagesBuilding Customer Satisfaction Through Quality, Service, and ValueHenry PamungkasNo ratings yet

- Strategic Management & Business Policy: Thomas L. Wheelen J. David HungerDocument35 pagesStrategic Management & Business Policy: Thomas L. Wheelen J. David HungerkishiNo ratings yet

- Economic Outlook 2023 OCE BMRIDocument21 pagesEconomic Outlook 2023 OCE BMRIjoenatan 2020No ratings yet

- External Environment Analysis of Airline IndustryDocument3 pagesExternal Environment Analysis of Airline IndustryJoey Tay100% (1)

- Strategic Management ModelDocument124 pagesStrategic Management Modelrocky_arunNo ratings yet

- Corporate StrategyDocument29 pagesCorporate StrategyIrene PonticelliNo ratings yet

- Orchestration of Network Slicing For Next Generation NetworkDocument76 pagesOrchestration of Network Slicing For Next Generation Networkchandan kumarNo ratings yet

- TomtomDocument9 pagesTomtomli100% (1)

- Driving Innovation and IdeasDocument30 pagesDriving Innovation and Ideastrial123No ratings yet

- Marketing Theory with a Strategic OrientationDocument12 pagesMarketing Theory with a Strategic OrientationNarmin Abida0% (1)

- Debt Collection Recovery Management Sea BankDocument4 pagesDebt Collection Recovery Management Sea BankPranav KhannaNo ratings yet

- The Strategy PaletteDocument11 pagesThe Strategy PaletteFathimaNo ratings yet

- Galanz's Operations Strategy for Future GrowthDocument11 pagesGalanz's Operations Strategy for Future Growthkokot123_100% (1)

- Summary of Vm#1 Customer FocusDocument6 pagesSummary of Vm#1 Customer FocusShekinah Faith RequintelNo ratings yet

- Contoh Five Forces AnalysisDocument17 pagesContoh Five Forces AnalysisChaeMJNo ratings yet

- Techniques For Analyzing Corporate Diversification StrategiesDocument7 pagesTechniques For Analyzing Corporate Diversification Strategiesapi-3738338100% (1)

- Traditional Consolidation End-Game Framework - v1.0Document12 pagesTraditional Consolidation End-Game Framework - v1.0batrarishu123No ratings yet

- Strategic Leadership: Michael A. Hitt R. Duane Ireland Robert E. HoskissonDocument29 pagesStrategic Leadership: Michael A. Hitt R. Duane Ireland Robert E. HoskissonDivya MalikNo ratings yet

- Indonesia e Conomy Sea 2021 ReportDocument17 pagesIndonesia e Conomy Sea 2021 ReportEep Saefulloh FatahNo ratings yet

- Hill & Jones - Ch03 - External AnalysisDocument19 pagesHill & Jones - Ch03 - External Analysisoushiza21No ratings yet

- Strategic Intent and Organizational VisionDocument21 pagesStrategic Intent and Organizational VisionAbhishek SoniNo ratings yet

- 8 Types of Business ManagementDocument3 pages8 Types of Business ManagementHerbert RulononaNo ratings yet

- War in Ukraine: Global Update: BCG Global Advantage Practice AreaDocument11 pagesWar in Ukraine: Global Update: BCG Global Advantage Practice AreaAyush MathurNo ratings yet

- DIGITAL 2020: IndonesiaDocument92 pagesDIGITAL 2020: Indonesia김연준No ratings yet

- Functional StrategyDocument35 pagesFunctional StrategyvishakhaNo ratings yet

- Agency Theory Family BusinessDocument8 pagesAgency Theory Family Businessusef100% (1)

- BCG MatrixDocument22 pagesBCG Matrixnomanfaisal1No ratings yet

- Ethical Issues in MarketingDocument30 pagesEthical Issues in MarketingDeepak KumarNo ratings yet

- Roland Berger Saudi Arabian Pharmaceuticals 2 PDFDocument20 pagesRoland Berger Saudi Arabian Pharmaceuticals 2 PDFVJ Reddy RNo ratings yet

- NTT Docomo Vol20 e en TotalDocument68 pagesNTT Docomo Vol20 e en TotalscribdenerNo ratings yet

- Chapter 5 The Five Generic ... StrategiesDocument20 pagesChapter 5 The Five Generic ... Strategieschelinti100% (1)

- Value Innovation PDFDocument12 pagesValue Innovation PDFDipankar GhoshNo ratings yet

- Slides Business Level StrategyDocument24 pagesSlides Business Level StrategyThảo PhạmNo ratings yet

- PP Ch03Document35 pagesPP Ch03FistareniNirbitaWardhoyoNo ratings yet

- Cost Leadership StrategyDocument11 pagesCost Leadership StrategyMahima GotekarNo ratings yet

- Blue Ocean Strategy For Medical and PharmaceuticalsDocument25 pagesBlue Ocean Strategy For Medical and PharmaceuticalsMohamed MahmoudNo ratings yet

- First Do No Harm Mar 2012 Tcm9-106817Document31 pagesFirst Do No Harm Mar 2012 Tcm9-106817nazNo ratings yet

- Radical Product Innovations in SMEs - The Dominance of Entrepreneurial Orientation PDFDocument15 pagesRadical Product Innovations in SMEs - The Dominance of Entrepreneurial Orientation PDFTitaneuropeNo ratings yet

- INFORMS Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Organization ScienceDocument22 pagesINFORMS Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Organization ScienceRachid El MoutahafNo ratings yet

- Evaluating Market Attractiveness: Individual Incentives vs. Industrial ProfitabilityDocument38 pagesEvaluating Market Attractiveness: Individual Incentives vs. Industrial ProfitabilityrerereNo ratings yet

- Karantininis, Sauer, Furtan, INNOVATION AND INTEGRATION IN THE AGRI-FOOD INDUSTRYDocument17 pagesKarantininis, Sauer, Furtan, INNOVATION AND INTEGRATION IN THE AGRI-FOOD INDUSTRYKostas KarantininisNo ratings yet

- Sustainable Innovation: The impact on the success of US large capsFrom EverandSustainable Innovation: The impact on the success of US large capsNo ratings yet

- Price, Value and Performance: Understanding the Tesla CaseDocument9 pagesPrice, Value and Performance: Understanding the Tesla CaseRodrigo BressanNo ratings yet

- Aghion2009 PDFDocument20 pagesAghion2009 PDFRodrigo BressanNo ratings yet

- Information Attention and Decision MakingDocument9 pagesInformation Attention and Decision MakingRodrigo BressanNo ratings yet

- Mastering StrategyDocument2 pagesMastering StrategyRodrigo BressanNo ratings yet

- MaslachScoringAbbreviated PDFDocument1 pageMaslachScoringAbbreviated PDFRatih AchiNo ratings yet

- Blue Ocean Strategy: Amazon Alexa CaseDocument10 pagesBlue Ocean Strategy: Amazon Alexa CaseMila SumpterNo ratings yet

- Artificial Intelligence:: Implications For Business StrategyDocument12 pagesArtificial Intelligence:: Implications For Business StrategyWilliam PolhmannNo ratings yet

- Aghion2009 PDFDocument20 pagesAghion2009 PDFRodrigo BressanNo ratings yet

- Hydroxychloroquine With or Without Azithromycin in Mild-to-Moderate Covid-19Document12 pagesHydroxychloroquine With or Without Azithromycin in Mild-to-Moderate Covid-19chamwick4567No ratings yet

- 2020.05.13.20094193v1.full 2Document22 pages2020.05.13.20094193v1.full 2Rodrigo BressanNo ratings yet

- RP Requirements For Selection and Justification of Starting Materials For The Manufacture of CASDocument10 pagesRP Requirements For Selection and Justification of Starting Materials For The Manufacture of CASRodrigo BressanNo ratings yet

- Artificial Intelligence:: Implications For Business StrategyDocument12 pagesArtificial Intelligence:: Implications For Business StrategyWilliam PolhmannNo ratings yet

- ICH Q2 R1 GuidelineDocument17 pagesICH Q2 R1 GuidelineRicard Castillejo HernándezNo ratings yet

- Analytical Procedures and Methods Validation For Drugs and Biologics - US FDA Final GuidanceDocument18 pagesAnalytical Procedures and Methods Validation For Drugs and Biologics - US FDA Final GuidanceDan StantonNo ratings yet

- QBD MaterialDocument5 pagesQBD MaterialRodrigo BressanNo ratings yet

- E8043 M5a99fx Pro R2Document178 pagesE8043 M5a99fx Pro R2Rodrigo BressanNo ratings yet

- MICLAB-110 Appendix 1 - Flow Chart For Processing Microbiology Laboratory OOS/OOL Investigations OOS/OOL Result GeneratedDocument1 pageMICLAB-110 Appendix 1 - Flow Chart For Processing Microbiology Laboratory OOS/OOL Investigations OOS/OOL Result GeneratedRodrigo BressanNo ratings yet

- QBD PresentationDocument12 pagesQBD PresentationRodrigo BressanNo ratings yet

- Pre-Test - Performing The EngagementDocument2 pagesPre-Test - Performing The EngagementSHARMAINE CORPUZ MIRANDANo ratings yet

- 25-RBA (Responsible Business Alliance) Member - LenovoDocument3 pages25-RBA (Responsible Business Alliance) Member - LenovoHernani BergamoNo ratings yet

- ISB - GAMP Nov 2018Document12 pagesISB - GAMP Nov 2018reddyrajashekarNo ratings yet

- PettyferMichaelAKarl 2011 MonopoliesTheoryEffectivenessandRegulatiDocument151 pagesPettyferMichaelAKarl 2011 MonopoliesTheoryEffectivenessandRegulatiAndres IslasNo ratings yet

- Warehouse Management Software WMS System Selection RFP Template 2013Document217 pagesWarehouse Management Software WMS System Selection RFP Template 2013SusanLK100% (1)

- Basics of Business Mathematics in 40 CharactersDocument17 pagesBasics of Business Mathematics in 40 CharactersAbhishek JainNo ratings yet

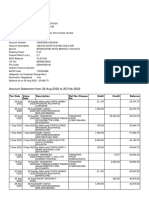

- Bank StatementDocument5 pagesBank StatementSANJIB GHOSHNo ratings yet

- Online Tutorial 8 Audit of Human Resources and Payment CycleDocument3 pagesOnline Tutorial 8 Audit of Human Resources and Payment CycleleiannetumamaoNo ratings yet

- Remedies in BankruptcyDocument34 pagesRemedies in BankruptcyfeyNo ratings yet

- The Application of Machine Learning and Deep LearnDocument20 pagesThe Application of Machine Learning and Deep LearnFran MoralesNo ratings yet

- Circular Guidelines and Schedule of Design Engineering Module ForDocument3 pagesCircular Guidelines and Schedule of Design Engineering Module ForAnmol KingNo ratings yet

- How To Use This Template: Delete This Slide Before Submitting Your AssignmentDocument11 pagesHow To Use This Template: Delete This Slide Before Submitting Your AssignmentAnnah AnnNo ratings yet

- SYZ Mining Audit Problem AnalysisDocument26 pagesSYZ Mining Audit Problem AnalysisKate NuevaNo ratings yet

- CA 08105001 eDocument3 pagesCA 08105001 eRicardo LopezNo ratings yet

- Saving Canada's Tallest TreeDocument7 pagesSaving Canada's Tallest TreeNarcisa Anabel Valeriano Veliz.No ratings yet

- Annual Report 2020-21Document121 pagesAnnual Report 2020-21Chhavi GajnaniNo ratings yet

- Work: Waterproofing Works For The Proposed 'Residential & Commercial Complex at Mohili, Sakinaka Mumbai 400 072' ContractorDocument11 pagesWork: Waterproofing Works For The Proposed 'Residential & Commercial Complex at Mohili, Sakinaka Mumbai 400 072' ContractorShubham DubeyNo ratings yet

- Trends in Ethics in Computing Assignment # 05 Sap Ids of Group MembersDocument2 pagesTrends in Ethics in Computing Assignment # 05 Sap Ids of Group Memberswardah mukhtarNo ratings yet

- Sales Order FormDocument1 pageSales Order FormDeepthireddyNo ratings yet

- Building International Brand Architecture: Integrating Branding Strategy Across MarketsDocument19 pagesBuilding International Brand Architecture: Integrating Branding Strategy Across MarketsDiana GuceaNo ratings yet

- Week 3 ModuleDocument14 pagesWeek 3 ModuleSofia Biangca M. BalderasNo ratings yet

- Which HR Bundles Are Utilized in Social Enterprises (Slide)Document2 pagesWhich HR Bundles Are Utilized in Social Enterprises (Slide)serofNo ratings yet

- European Union: Name - Ajay Bba - 6 SemesterDocument17 pagesEuropean Union: Name - Ajay Bba - 6 Semesterajay DahiyaNo ratings yet

- Swot of AbinbevDocument3 pagesSwot of AbinbevSanjeev Kumar SharmaNo ratings yet

- Group 9 Eabdm s13Document3 pagesGroup 9 Eabdm s13DIOUF SHAJAHAN K TNo ratings yet

- MPU3222 - Course Introduction Briefing For Student (Sem 1 - 2022-2023) (I)Document24 pagesMPU3222 - Course Introduction Briefing For Student (Sem 1 - 2022-2023) (I)trickyhunter9999No ratings yet

- Understanding Mergers and Acquisitions (M&A) Introduction: Mergers and Acquisitions (M&A) Are Complex Financial Transactions That InvolveDocument2 pagesUnderstanding Mergers and Acquisitions (M&A) Introduction: Mergers and Acquisitions (M&A) Are Complex Financial Transactions That InvolveSebastian StolkinerNo ratings yet

- Group Assignment - A211 QUESTIONNAIREDocument9 pagesGroup Assignment - A211 QUESTIONNAIREMuhammad NafisNo ratings yet

- Exercise 1 Key PDF Cost of Goods Sold InvenDocument1 pageExercise 1 Key PDF Cost of Goods Sold InvenAl BertNo ratings yet