You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Essay FIN202Document5 pagesEssay FIN202thaindnds180468No ratings yet

- Tugas 20.445cs4Document8 pagesTugas 20.445cs4ina aktNo ratings yet

- SummaryDocument11 pagesSummaryarmeneh khachoomianNo ratings yet

- Financial StatementsDocument10 pagesFinancial StatementsAirah MondonedoNo ratings yet

- Financial Statement - Is and NotesDocument31 pagesFinancial Statement - Is and NotesAlvin James OlayaNo ratings yet

- Budget 2021Document5 pagesBudget 2021Jobeth DaculaNo ratings yet

- University of Makati J.P. Rizal Ext. West Rembo, City of Makati College of Business and Financial ScienceDocument16 pagesUniversity of Makati J.P. Rizal Ext. West Rembo, City of Makati College of Business and Financial ScienceKarla OñasNo ratings yet

- I. Assets: 2018 2019Document7 pagesI. Assets: 2018 2019Kean DeeNo ratings yet

- Profit & Loss (Accrual)Document1 pageProfit & Loss (Accrual)SMK ASY-SYAFI'IYYAHNo ratings yet

- CL 3 Suggested Solution For Pilot PaperDocument15 pagesCL 3 Suggested Solution For Pilot PaperRoshanNo ratings yet

- Group 5Document16 pagesGroup 5Amelia AndrianiNo ratings yet

- INCOME STATEMENT (CTT Exam)Document1 pageINCOME STATEMENT (CTT Exam)Mharck AtienzaNo ratings yet

- Piliart Nuts Rizal Street, Sagpon, Daraga, AlbayDocument5 pagesPiliart Nuts Rizal Street, Sagpon, Daraga, AlbayHazel Mae HerreraNo ratings yet

- Lounge FS PresentationDocument136 pagesLounge FS PresentationJeremiah GonzagaNo ratings yet

- Lembar Jawaban 4-LAPORAN FixDocument7 pagesLembar Jawaban 4-LAPORAN FixClara Shinta OceeNo ratings yet

- Perry - SolutionsDocument4 pagesPerry - SolutionsCharles TuazonNo ratings yet

- Income Statement P2 JayatamaDocument1 pageIncome Statement P2 JayatamaShula KinantiNo ratings yet

- XYZ Company Profit and Loss: All DatesDocument2 pagesXYZ Company Profit and Loss: All DatesMatt Kelvin ParaisoNo ratings yet

- STC Answer A&BDocument2 pagesSTC Answer A&BJagvir Singh Jaglan ms21a025No ratings yet

- Advanced Corporate Finance Case 2Document3 pagesAdvanced Corporate Finance Case 2Adrien PortemontNo ratings yet

- Template 2 Task 3 Calculation Worksheet - BSBFIM601Document17 pagesTemplate 2 Task 3 Calculation Worksheet - BSBFIM601Writing Experts0% (1)

- Answer Key Chapter 10 Home OFFICE PART1Document8 pagesAnswer Key Chapter 10 Home OFFICE PART1karen perrerasNo ratings yet

- Profit & Loss PT TCP M Arif Rahman - 2005151018 - Akp-3aDocument1 pageProfit & Loss PT TCP M Arif Rahman - 2005151018 - Akp-3aM Arif RahmanNo ratings yet

- Revenue Projection:: 47.6 Accounts Receivable 37.6 Inventory Accounts PayableDocument8 pagesRevenue Projection:: 47.6 Accounts Receivable 37.6 Inventory Accounts Payablesaqibriaz8771No ratings yet

- Musanity Financial StatementsDocument20 pagesMusanity Financial StatementsRenelyn DavidNo ratings yet

- Profit and Loss ProjectionDocument1 pageProfit and Loss ProjectionAbel GetachewNo ratings yet

- Feasib Chapter 4Document9 pagesFeasib Chapter 4Red SecretarioNo ratings yet

- Cement Factory Financial PlanDocument4 pagesCement Factory Financial PlanJoey MWNo ratings yet

- Routine Expenses: FIXED COST: No Matter How Much Volume The Business ProducesDocument8 pagesRoutine Expenses: FIXED COST: No Matter How Much Volume The Business ProducesRazmen PintoNo ratings yet

- Sote Hub Summary For The Year Ended 2023Document2 pagesSote Hub Summary For The Year Ended 2023graceNo ratings yet

- NPV Lesson 2Document5 pagesNPV Lesson 2Barack MikeNo ratings yet

- Income Statement For The End of Period December 31, 2022 (RP)Document1 pageIncome Statement For The End of Period December 31, 2022 (RP)ahmadiNo ratings yet

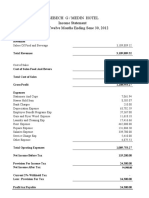

- Abebech G - Medin 2012 1Document19 pagesAbebech G - Medin 2012 1Deresegn NedaNo ratings yet

- Profit1 2005Document1 pageProfit1 2005aNo ratings yet

- Review On Financial Statements AnalysisDocument2 pagesReview On Financial Statements AnalysisJohn Carl SoledadNo ratings yet

- Working: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000Document8 pagesWorking: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000kudkhanNo ratings yet

- Nice Spring Icee Delight (Bohol) : For The Month Ended December 31, 2020Document2 pagesNice Spring Icee Delight (Bohol) : For The Month Ended December 31, 2020ARISNo ratings yet

- 19B135 Hallstead Jewellers CaseDocument23 pages19B135 Hallstead Jewellers CaseEashaa SaraogiNo ratings yet

- Laporan Laba Rugi - Nama AndaDocument1 pageLaporan Laba Rugi - Nama AndaGloria HanaNo ratings yet

- Chapter VDocument7 pagesChapter VJanella LorineNo ratings yet

- Chapter 4 - FINANCIAL STUDYDocument14 pagesChapter 4 - FINANCIAL STUDYRed SecretarioNo ratings yet

- HC P & L - Feb 2022 To March 2023Document9 pagesHC P & L - Feb 2022 To March 2023MaiNo ratings yet

- 1.november - 2018 - Monthly - ReportDocument1 page1.november - 2018 - Monthly - ReportShafin2008No ratings yet

- ZafaDocument3 pagesZafaDayavantiNo ratings yet

- Plywood Project Report by Yogesh AgrawalDocument22 pagesPlywood Project Report by Yogesh AgrawalYOGESH AGRAWALNo ratings yet

- Financial Assumptions: RevenueDocument12 pagesFinancial Assumptions: RevenueKathleeneNo ratings yet

- Financial PlanDocument7 pagesFinancial PlanRocheal DecenaNo ratings yet

- Financial-Plan-For Business PlanDocument15 pagesFinancial-Plan-For Business Planpogia24koNo ratings yet

- Final Costing at 10,000 Katha BookingDocument26 pagesFinal Costing at 10,000 Katha BookingJabedur RahmanNo ratings yet

- Investment Appraisal and Analysis Ide 2018Document4 pagesInvestment Appraisal and Analysis Ide 2018vincentNo ratings yet

- Class Discussion BLEMBA 31A Day2Document27 pagesClass Discussion BLEMBA 31A Day2Bayu Aji PrasetyoNo ratings yet

- Kunci Jawaban Laporan KeuanganDocument16 pagesKunci Jawaban Laporan KeuanganreiNo ratings yet

- Spending SummaryDocument1 pageSpending SummaryAnn Arbor Government DocumentsNo ratings yet

- Closing P2 JayatamaDocument2 pagesClosing P2 JayatamaShula KinantiNo ratings yet

- Items Cost Cost ( N ) : Cleaners Food Technicians Security Guards Other Total Salary Labor Salary in NairaDocument4 pagesItems Cost Cost ( N ) : Cleaners Food Technicians Security Guards Other Total Salary Labor Salary in NairababatundeNo ratings yet

- SECUREX (PVT.) Limited: Statement of Comprehensive Income For The Year Ended 29 February 2016 2016 Notes TakaDocument4 pagesSECUREX (PVT.) Limited: Statement of Comprehensive Income For The Year Ended 29 February 2016 2016 Notes TakaBiplob K. SannyasiNo ratings yet

- TsefaDocument4 pagesTsefaAhmed SaeedNo ratings yet

- Nice Spring Icee Delight (Cebu) : For The Month Ended December 31, 2020Document2 pagesNice Spring Icee Delight (Cebu) : For The Month Ended December 31, 2020ARISNo ratings yet

- Ampalaya Ice CreamDocument12 pagesAmpalaya Ice CreamEdhel Bryan Corsiga SuicoNo ratings yet

- Financial Markets Dba 302Document5 pagesFinancial Markets Dba 302mulenga lubembaNo ratings yet

- QUESTION (Minimizing Total Production Time) Sequencing Jobs Through Two Work CentersDocument4 pagesQUESTION (Minimizing Total Production Time) Sequencing Jobs Through Two Work Centersmulenga lubemba100% (1)

- The INTERNET 2Document14 pagesThe INTERNET 2mulenga lubembaNo ratings yet

- Research Combined DocumentDocument19 pagesResearch Combined Documentmulenga lubembaNo ratings yet

- Diploma in Accountancy and Government Accounting FinalDocument100 pagesDiploma in Accountancy and Government Accounting Finalmulenga lubemba100% (2)

- DPM 205 Financial Management AssignmentDocument2 pagesDPM 205 Financial Management Assignmentmulenga lubembaNo ratings yet

- Dba 302 Financial Management Test 4TH March 2020 Part TimeDocument6 pagesDba 302 Financial Management Test 4TH March 2020 Part Timemulenga lubembaNo ratings yet

- Dba 302 Accounting Rate of Return, NPV and Irr PresentationsDocument12 pagesDba 302 Accounting Rate of Return, NPV and Irr Presentationsmulenga lubembaNo ratings yet

- Dba 302 Financial Management Supplementary TestDocument3 pagesDba 302 Financial Management Supplementary Testmulenga lubembaNo ratings yet

- Dag 1070 Management SyllabusDocument3 pagesDag 1070 Management Syllabusmulenga lubembaNo ratings yet

- Introduction To Corporate Governance & Company Law: Enron, World. Parmalat Was The World' S Largest FoodDocument3 pagesIntroduction To Corporate Governance & Company Law: Enron, World. Parmalat Was The World' S Largest Foodmulenga lubembaNo ratings yet

- Introduction To Financial ManagementDocument10 pagesIntroduction To Financial Managementmulenga lubemba100% (1)

- Dag 305 Project FinanceDocument133 pagesDag 305 Project Financemulenga lubembaNo ratings yet

- Reverse Osmosis (RO) Is A Water Purification Process That Uses ADocument12 pagesReverse Osmosis (RO) Is A Water Purification Process That Uses Amulenga lubemba100% (1)

- Emmy Business PlanDocument11 pagesEmmy Business Planmulenga lubembaNo ratings yet

- Dag 205 Quantitative AnalysisDocument4 pagesDag 205 Quantitative Analysismulenga lubembaNo ratings yet

- Budgets and Budgetary Control and Behavioural Implications of BudgetingDocument3 pagesBudgets and Budgetary Control and Behavioural Implications of Budgetingmulenga lubembaNo ratings yet

- InterAcc 14-33Document11 pagesInterAcc 14-33Marinella LosaNo ratings yet

- Robotics Automation Project Sample ProposalDocument13 pagesRobotics Automation Project Sample ProposalVidhiNo ratings yet

- E-Mobile Business ProposalDocument22 pagesE-Mobile Business ProposalSabrina Abdurahman100% (2)

- ØÁ L Nu T Uz È: Federal Negarit GazetaDocument4 pagesØÁ L Nu T Uz È: Federal Negarit Gazetamikias musseNo ratings yet

- Organizational BehaviourDocument6 pagesOrganizational BehaviourJudNo ratings yet

- Consignment Accounting QuestionsDocument1 pageConsignment Accounting QuestionsAlbaksh BrockNo ratings yet

- AccountingDocument24 pagesAccountingAmmad Ud Din SabirNo ratings yet

- Student Fee Receipt GEUDocument1 pageStudent Fee Receipt GEUTushar GairolaNo ratings yet

- Home Stay Guest HouseDocument22 pagesHome Stay Guest HouseMaddu Janak RaoNo ratings yet

- Samples Are Required If You Get Order .It Will Be: S/S Hex BoltDocument2 pagesSamples Are Required If You Get Order .It Will Be: S/S Hex BoltSalim MullaNo ratings yet

- 3rd Assignment ABC AnalysisDocument9 pages3rd Assignment ABC AnalysisDivya ToppoNo ratings yet

- Chapter 2-Part 3Document19 pagesChapter 2-Part 3Puji dyukeNo ratings yet

- Module 7Document12 pagesModule 7Lannie GarinNo ratings yet

- GuthaliDocument4 pagesGuthaliJohnsey RoyNo ratings yet

- Chapter 4 Governmental AccountingDocument5 pagesChapter 4 Governmental Accountingmohamad ali osmanNo ratings yet

- Business Model Canvas BARBIEDocument2 pagesBusiness Model Canvas BARBIEd.tech.i.t.businessNo ratings yet

- E9-8 Dan E9-13 - AKL 1 - Elisabet Siregar - 023001801106Document2 pagesE9-8 Dan E9-13 - AKL 1 - Elisabet Siregar - 023001801106novita sariNo ratings yet

- MODULE 5 - Investment Property: 3.1.1 Definition & NatureDocument12 pagesMODULE 5 - Investment Property: 3.1.1 Definition & NatureCj BarrettoNo ratings yet

- Financial Ana Fundament Assessment Review - Corporate Finance InstituteDocument22 pagesFinancial Ana Fundament Assessment Review - Corporate Finance Instituteolaomotito hossanaNo ratings yet

- Macroeconomic Framework-Performance and Policies: Chapter #2Document28 pagesMacroeconomic Framework-Performance and Policies: Chapter #2Annam InayatNo ratings yet

- 2307 Jan - Feb 2020Document4 pages2307 Jan - Feb 2020Marvin CeledioNo ratings yet

- Accounting EnteriesDocument9 pagesAccounting Enterieskavita sihagNo ratings yet

- 2019 2020 Obe Syllabus in Monetary PolicyDocument6 pages2019 2020 Obe Syllabus in Monetary PolicySophiaEllaineYanggatLopezNo ratings yet

- Examination, 2015 Commerce Specialized Accounting: (Printed Pages 7) Roll. No.Document4 pagesExamination, 2015 Commerce Specialized Accounting: (Printed Pages 7) Roll. No.AbhishekNo ratings yet

- Legal Ethics MBA 5015Document27 pagesLegal Ethics MBA 5015Shakib HasanNo ratings yet

- Contract CostingDocument12 pagesContract Costingvivek rajakNo ratings yet

- Company Profile NingBoDocument5 pagesCompany Profile NingBorashid isaarNo ratings yet

- HC Ojas Sbiepay e ReceiptDocument2 pagesHC Ojas Sbiepay e ReceiptA53 DAVE JAYNo ratings yet

- Credit Creation by RbiDocument24 pagesCredit Creation by RbiABIGAIL SHIJU 20213116No ratings yet

- (Bea) 1Document28 pages(Bea) 1Rafika Hamidah HamdiNo ratings yet

- The United States of Beer: A Freewheeling History of the All-American DrinkFrom EverandThe United States of Beer: A Freewheeling History of the All-American DrinkRating: 4 out of 5 stars4/5 (7)

- Waiter Rant: Thanks for the Tip—Confessions of a Cynical WaiterFrom EverandWaiter Rant: Thanks for the Tip—Confessions of a Cynical WaiterRating: 3.5 out of 5 stars3.5/5 (487)

- AI Superpowers: China, Silicon Valley, and the New World OrderFrom EverandAI Superpowers: China, Silicon Valley, and the New World OrderRating: 4.5 out of 5 stars4.5/5 (399)

- All The Beauty in the World: The Metropolitan Museum of Art and MeFrom EverandAll The Beauty in the World: The Metropolitan Museum of Art and MeRating: 4.5 out of 5 stars4.5/5 (83)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (9)

- Summary: Unreasonable Hospitality: The Remarkable Power of Giving People More than They Expect by Will Guidara: Key Takeaways, Summary & Analysis IncludedFrom EverandSummary: Unreasonable Hospitality: The Remarkable Power of Giving People More than They Expect by Will Guidara: Key Takeaways, Summary & Analysis IncludedRating: 2.5 out of 5 stars2.5/5 (5)

- Dealers of Lightning: Xerox PARC and the Dawn of the Computer AgeFrom EverandDealers of Lightning: Xerox PARC and the Dawn of the Computer AgeRating: 4 out of 5 stars4/5 (88)

- The Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyFrom EverandThe Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyNo ratings yet

- The Formula: How Rogues, Geniuses, and Speed Freaks Reengineered F1 into the World's Fastest Growing SportFrom EverandThe Formula: How Rogues, Geniuses, and Speed Freaks Reengineered F1 into the World's Fastest Growing SportRating: 4 out of 5 stars4/5 (1)

- Getting Started in Consulting: The Unbeatable Comprehensive Guidebook for First-Time ConsultantsFrom EverandGetting Started in Consulting: The Unbeatable Comprehensive Guidebook for First-Time ConsultantsRating: 4.5 out of 5 stars4.5/5 (10)

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)

- What Customers Hate: Drive Fast and Scalable Growth by Eliminating the Things that Drive Away BusinessFrom EverandWhat Customers Hate: Drive Fast and Scalable Growth by Eliminating the Things that Drive Away BusinessRating: 5 out of 5 stars5/5 (1)

- The Toyota Way (Second Edition): 14 Management Principles from the World's Greatest ManufacturerFrom EverandThe Toyota Way (Second Edition): 14 Management Principles from the World's Greatest ManufacturerRating: 4 out of 5 stars4/5 (121)

- All You Need to Know About the Music Business: Eleventh EditionFrom EverandAll You Need to Know About the Music Business: Eleventh EditionNo ratings yet

- SkyTest® Airline Interview - The Exercise Book: Interview questions and tasks from real life selection procedures for pilots and ATCOsFrom EverandSkyTest® Airline Interview - The Exercise Book: Interview questions and tasks from real life selection procedures for pilots and ATCOsRating: 4 out of 5 stars4/5 (12)

- How Star Wars Conquered the Universe: The Past, Present, and Future of a Multibillion Dollar FranchiseFrom EverandHow Star Wars Conquered the Universe: The Past, Present, and Future of a Multibillion Dollar FranchiseRating: 4.5 out of 5 stars4.5/5 (14)

- Unveling The World Of One Piece: Decoding The Characters, Themes, And World Of The AnimeFrom EverandUnveling The World Of One Piece: Decoding The Characters, Themes, And World Of The AnimeRating: 4 out of 5 stars4/5 (1)

- Excellence Wins: A No-Nonsense Guide to Becoming the Best in a World of CompromiseFrom EverandExcellence Wins: A No-Nonsense Guide to Becoming the Best in a World of CompromiseRating: 5 out of 5 stars5/5 (79)

- All You Need to Know About the Music Business: 11th EditionFrom EverandAll You Need to Know About the Music Business: 11th EditionNo ratings yet

- Into the Raging Sea: Thirty-Three Mariners, One Megastorm, and the Sinking of El FaroFrom EverandInto the Raging Sea: Thirty-Three Mariners, One Megastorm, and the Sinking of El FaroRating: 4 out of 5 stars4/5 (78)

- Lean Six Sigma: The Ultimate Guide to Lean Six Sigma, Lean Enterprise, and Lean Manufacturing, with Tools Included for Increased Efficiency and Higher Customer SatisfactionFrom EverandLean Six Sigma: The Ultimate Guide to Lean Six Sigma, Lean Enterprise, and Lean Manufacturing, with Tools Included for Increased Efficiency and Higher Customer SatisfactionRating: 5 out of 5 stars5/5 (2)

- Network of Lies: The Epic Saga of Fox News, Donald Trump, and the Battle for American DemocracyFrom EverandNetwork of Lies: The Epic Saga of Fox News, Donald Trump, and the Battle for American DemocracyRating: 4 out of 5 stars4/5 (16)