You might also like

- Forex Trading For BeginnersDocument13 pagesForex Trading For BeginnersChiedozie Onuegbu100% (2)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Lecture 2728 Prospective Analysis Process of Projecting Income Statement Balance SheetDocument36 pagesLecture 2728 Prospective Analysis Process of Projecting Income Statement Balance SheetRahul GautamNo ratings yet

- AHM13e - Chapter 01 - Key To EOC Problems and CasesDocument14 pagesAHM13e - Chapter 01 - Key To EOC Problems and CasesArunesh SN100% (1)

- Fundamentals of Accounting 2 Draft PDFDocument123 pagesFundamentals of Accounting 2 Draft PDFCzaeshel Edades100% (5)

- Form16 W0000000 GS186523X 2021 20211Document1 pageForm16 W0000000 GS186523X 2021 20211Raman OjhaNo ratings yet

- ASPL3 Activity 3-6 DoneDocument7 pagesASPL3 Activity 3-6 DoneConcepcion Family33% (3)

- SPL Updated Syllabus - 2020 PDFDocument6 pagesSPL Updated Syllabus - 2020 PDFCiara De LeonNo ratings yet

- Interview Questions and AnswersDocument9 pagesInterview Questions and AnswersHariNo ratings yet

- Kzten 000 Po Tme0 03492 - 2022 09 03 - 09 54 44 284Document2 pagesKzten 000 Po Tme0 03492 - 2022 09 03 - 09 54 44 284MadiyarNo ratings yet

- Tutorial - Session W1 - SolutionsDocument15 pagesTutorial - Session W1 - SolutionslizaNo ratings yet

- 6 - Business Transactions and Their AnalysisDocument23 pages6 - Business Transactions and Their AnalysisJarred FranciscoNo ratings yet

- Lecture 2Document36 pagesLecture 2Aram NawaisehNo ratings yet

- Chapter 1 - Accounting Equation - CorporationDocument37 pagesChapter 1 - Accounting Equation - CorporationadriamNo ratings yet

- Chapter 1 (Mathematical)Document18 pagesChapter 1 (Mathematical)Sabbir HossainNo ratings yet

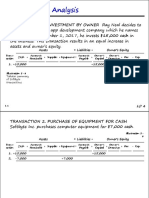

- Transaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToDocument31 pagesTransaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToSophia LocreNo ratings yet

- Ch+1b+-+accounting+in+actionDocument29 pagesCh+1b+-+accounting+in+actionUcup Blak-blakanNo ratings yet

- CH 01 Fin. Acc - Lec 02 EditedDocument16 pagesCH 01 Fin. Acc - Lec 02 Editednumber oneNo ratings yet

- Tugas Accounting 1 With NotesDocument14 pagesTugas Accounting 1 With Notesvico lorenzoNo ratings yet

- Transaction Analysis-Ch-1 Session 2, 3 4Document17 pagesTransaction Analysis-Ch-1 Session 2, 3 4rj OpuNo ratings yet

- Principles of Accounting Second Year, Semester 1Document38 pagesPrinciples of Accounting Second Year, Semester 1Sara Abdelrahim MakkawiNo ratings yet

- Principles of Accounting Second Year, Semester 1: Transactions AnalysisDocument38 pagesPrinciples of Accounting Second Year, Semester 1: Transactions AnalysisSara Abdelrahim MakkawiNo ratings yet

- Fundametals of Acct I CH 1-5Document382 pagesFundametals of Acct I CH 1-5Zerihun GetachewNo ratings yet

- Fundamantels of Accounting PresentationDocument24 pagesFundamantels of Accounting PresentationAmy TabaconNo ratings yet

- Module-1 SolutionsDocument6 pagesModule-1 SolutionsARYA GOWDANo ratings yet

- Chapter 2Document49 pagesChapter 2haiderasim1212No ratings yet

- Accounting EquationfinalDocument40 pagesAccounting EquationfinalChowdhury Mobarrat Haider AdnanNo ratings yet

- ACCT 207 CHAPTER 3 - No - Video PDFDocument56 pagesACCT 207 CHAPTER 3 - No - Video PDFRoxy BobadillaNo ratings yet

- Principles of Accounting Lecture 2Document11 pagesPrinciples of Accounting Lecture 2Masum HossainNo ratings yet

- Accounting Equation: Fundamentals of ABM 1Document97 pagesAccounting Equation: Fundamentals of ABM 1ediwowNo ratings yet

- Chapter Accounting EquationDocument24 pagesChapter Accounting Equationpriyam.200409No ratings yet

- Transaction Analysis-Ch-1 Session 2, 3 4Document17 pagesTransaction Analysis-Ch-1 Session 2, 3 4Parvej ahmedNo ratings yet

- Studies in Accounting 3Document19 pagesStudies in Accounting 3amirrashad141No ratings yet

- Assets Are Resources Owned by A Business. They Are Things of Value Used in Carrying Out Such Activities As Production and ExchangeDocument24 pagesAssets Are Resources Owned by A Business. They Are Things of Value Used in Carrying Out Such Activities As Production and ExchangeRegine Alesna AlcoberNo ratings yet

- Group Work FA 1 - Group 7Document9 pagesGroup Work FA 1 - Group 7Tri HuynhNo ratings yet

- Business Combinations: Answers To Questions 1Document12 pagesBusiness Combinations: Answers To Questions 1Sin TungNo ratings yet

- HUM 121assignment 1Document6 pagesHUM 121assignment 1Nayeem HossainNo ratings yet

- ID 193120001 Final Assignment.Document64 pagesID 193120001 Final Assignment.CSE 1033Naymur RahmanNo ratings yet

- Assignment 1Document14 pagesAssignment 1azimlitamellaNo ratings yet

- Eshetu Gelagay Ind Ass Acc - For ManagersDocument12 pagesEshetu Gelagay Ind Ass Acc - For ManagersabiyNo ratings yet

- Lecture03 FSDocument17 pagesLecture03 FS錢永健No ratings yet

- Chapter 1 Accounting in ActionDocument24 pagesChapter 1 Accounting in Actionshemon.diuNo ratings yet

- Chapter 1 - IntroductionDocument15 pagesChapter 1 - IntroductionsaputraNo ratings yet

- Burguita Myrel D. Eco 2 Exercise 5Document5 pagesBurguita Myrel D. Eco 2 Exercise 5Elle Villanueva VlogNo ratings yet

- Accounting ExercisesDocument17 pagesAccounting ExercisesKarenNo ratings yet

- Financial Accounting: Accounting Equation and Double Entry SystemDocument27 pagesFinancial Accounting: Accounting Equation and Double Entry SystemNurulHuda Auni Binti Ab RahmanNo ratings yet

- Lecture02-Introduction To AccountingDocument38 pagesLecture02-Introduction To Accounting錢永健No ratings yet

- CH 3 Work PacketDocument8 pagesCH 3 Work Packetana sosaNo ratings yet

- FA Assignment 1 Non-GradedDocument11 pagesFA Assignment 1 Non-GradedVishal RajNo ratings yet

- 01 Intro To Basic Acctg - Recording AnalyzingDocument37 pages01 Intro To Basic Acctg - Recording AnalyzingJerah Marie PepitoNo ratings yet

- College Accounting A Contemporary Approach 3rd Edition Haddock Price Farina ISBN Solution ManualDocument22 pagesCollege Accounting A Contemporary Approach 3rd Edition Haddock Price Farina ISBN Solution Manualdonald100% (24)

- Pembahasan Soal AC Part 1Document34 pagesPembahasan Soal AC Part 1suci monalia putriNo ratings yet

- College Accounting 14th Edition Price Haddock Farina ISBN Solution ManualDocument22 pagesCollege Accounting 14th Edition Price Haddock Farina ISBN Solution Manualdonald100% (23)

- Session 2 Ma (9th May 2012)Document31 pagesSession 2 Ma (9th May 2012)KamauWafulaWanyamaNo ratings yet

- Principles of AccountingDocument7 pagesPrinciples of AccountingMuốn Đi Ngủ CơNo ratings yet

- Accounting Chapter 1: Transaction AnalysisDocument12 pagesAccounting Chapter 1: Transaction Analysiskareem abozeedNo ratings yet

- Transactions of AccountingDocument7 pagesTransactions of Accountingayele gebremichaelNo ratings yet

- CHAPTER 1 Trial - ACC101Document9 pagesCHAPTER 1 Trial - ACC101An nguyên Trương ĐỗNo ratings yet

- Acc 1 QuizDocument7 pagesAcc 1 QuizAyat MukahalNo ratings yet

- Rule of Debit and Credit (2023)Document26 pagesRule of Debit and Credit (2023)TEE Yu Yang TEENo ratings yet

- Liabilities + Equity Assets + Net IncomeDocument1 pageLiabilities + Equity Assets + Net IncomeValenzuela F. WinnielynNo ratings yet

- GMA Correcting EntriesDocument6 pagesGMA Correcting EntriesRaff LesiaaNo ratings yet

- Legal Services Company Ltd. Book1Document9 pagesLegal Services Company Ltd. Book1Firomsa Ahmednur TesfayeNo ratings yet

- Accounting Transaction Processing Chapter 3Document73 pagesAccounting Transaction Processing Chapter 3Rupesh PolNo ratings yet

- Accounting IDocument18 pagesAccounting IMohammed mostafaNo ratings yet

- Class Exercise 4 MKTG 344 - 2Document3 pagesClass Exercise 4 MKTG 344 - 2Ali Zain ParharNo ratings yet

- SBM Case Study Group 6 - FinalDocument26 pagesSBM Case Study Group 6 - FinalAli Zain ParharNo ratings yet

- Risk Attitude - Assessing Risk ToleranceDocument4 pagesRisk Attitude - Assessing Risk ToleranceAli Zain ParharNo ratings yet

- CB Quiz1 KeyDocument5 pagesCB Quiz1 KeyAli Zain ParharNo ratings yet

- Class Exercise 4 MKTG 344 - 2Document4 pagesClass Exercise 4 MKTG 344 - 2Ali Zain ParharNo ratings yet

- Famine, Affluence and HypocrisyDocument17 pagesFamine, Affluence and HypocrisyAli Zain ParharNo ratings yet

- CB Quiz 3 KeyDocument5 pagesCB Quiz 3 KeyAli Zain ParharNo ratings yet

- Data Stars PresentationDocument18 pagesData Stars PresentationAli Zain ParharNo ratings yet

- Session 19Document23 pagesSession 19Ali Zain ParharNo ratings yet

- DDM Guest Session Key Points - Osman KhairiDocument1 pageDDM Guest Session Key Points - Osman KhairiAli Zain ParharNo ratings yet

- Risk Attitude - Eagle - AirlinesDocument3 pagesRisk Attitude - Eagle - AirlinesAli Zain ParharNo ratings yet

- Writing and Communications S10Document20 pagesWriting and Communications S10Ali Zain ParharNo ratings yet

- MGMT Presentation 1Document8 pagesMGMT Presentation 1Ali Zain ParharNo ratings yet

- ACCT 100, Fall Semester 2020-21 Quiz 2Document48 pagesACCT 100, Fall Semester 2020-21 Quiz 2Ali Zain ParharNo ratings yet

- Information Systems (IS), Organizations and StrategyDocument10 pagesInformation Systems (IS), Organizations and StrategyAli Zain ParharNo ratings yet

- Wk1 - Lesson 1Document13 pagesWk1 - Lesson 1Ali Zain ParharNo ratings yet

- POFA (ACCT 100) Tutorial: Week 1 Chapter 1 - Accounting in Action Topics CoveredDocument3 pagesPOFA (ACCT 100) Tutorial: Week 1 Chapter 1 - Accounting in Action Topics CoveredAli Zain ParharNo ratings yet

- Saadia Shahid Math-101-Fall-2021 Assignment Definite Integrals Due 12/21/2020 at 10:00am ESTDocument2 pagesSaadia Shahid Math-101-Fall-2021 Assignment Definite Integrals Due 12/21/2020 at 10:00am ESTAli Zain ParharNo ratings yet

- ExportedDocument4 pagesExportedAli Zain ParharNo ratings yet

- Principles of Financial Accounting: Chapter 7 - Fraud, Internal Controls, & CashDocument12 pagesPrinciples of Financial Accounting: Chapter 7 - Fraud, Internal Controls, & CashAli Zain Parhar100% (2)

- POFA (ACCT 100) Tutorial: Week 2 Chapter 2 - The Recording Process Topics CoveredDocument3 pagesPOFA (ACCT 100) Tutorial: Week 2 Chapter 2 - The Recording Process Topics CoveredAli Zain ParharNo ratings yet

- Saadia Shahid Math-101-Fall-2021 Assignment Fundamental Theorm of Calculus Due 12/21/2020 at 08:00am ESTDocument2 pagesSaadia Shahid Math-101-Fall-2021 Assignment Fundamental Theorm of Calculus Due 12/21/2020 at 08:00am ESTAli Zain ParharNo ratings yet

- Tutorial Slides-Chap 8-Accounting For Receivables PDFDocument20 pagesTutorial Slides-Chap 8-Accounting For Receivables PDFAli Zain ParharNo ratings yet

- Quiz 2 DeliveryDocument20 pagesQuiz 2 DeliveryAli Zain ParharNo ratings yet

- ACCT 100 - Principles of Financial Accounting Fall 2020, Section 6 Week 10 Chapter 10 - LiabilitiesDocument2 pagesACCT 100 - Principles of Financial Accounting Fall 2020, Section 6 Week 10 Chapter 10 - LiabilitiesAli Zain ParharNo ratings yet

- Week 10 - CH 10 Questions in Class TutorialDocument2 pagesWeek 10 - CH 10 Questions in Class TutorialAli Zain ParharNo ratings yet

- Auditing and Assurance PrinciplesDocument2 pagesAuditing and Assurance PrinciplesJohn Francis Escayde UrlandaNo ratings yet

- Application Note Metallography of WeldsDocument8 pagesApplication Note Metallography of WeldsLorena Grijalba LeónNo ratings yet

- Contracts Under Labour and ServicesDocument3 pagesContracts Under Labour and ServicesYash SinghNo ratings yet

- Chapter 2Document25 pagesChapter 2JOSEPH LEE ZE LOONG MoeNo ratings yet

- Chapter 3.transportation Regulation and Public PolicyDocument45 pagesChapter 3.transportation Regulation and Public PolicyMosNo ratings yet

- Astm A20 PDFDocument33 pagesAstm A20 PDFJhon Edison Posada MuñozNo ratings yet

- National Green Export Review of Vanuatu: Copra-Coconut, Cocoa-Chocolate and SandalwoodDocument42 pagesNational Green Export Review of Vanuatu: Copra-Coconut, Cocoa-Chocolate and SandalwoodTun Lin WinNo ratings yet

- Lakshya Final 6th Project PDFDocument76 pagesLakshya Final 6th Project PDFPrabhat Kumar DeshwalNo ratings yet

- General Collection CollegeDocument5 pagesGeneral Collection Collegejeysel calumbaNo ratings yet

- 3.2 Commissioner V CADocument8 pages3.2 Commissioner V CAJayNo ratings yet

- Mpu3223 - V2 Entrepreneurship IiDocument10 pagesMpu3223 - V2 Entrepreneurship IiSimon RajNo ratings yet

- Factors Influencing The Use of Ewallet As A Payment Method Among Malaysian Young AdultsDocument12 pagesFactors Influencing The Use of Ewallet As A Payment Method Among Malaysian Young AdultsNhi NguyenNo ratings yet

- Probate - WillDocument8 pagesProbate - WillClarence MbeteraNo ratings yet

- 013 Esmr en - 2Document14 pages013 Esmr en - 2EliasNo ratings yet

- LATIHAN1Document15 pagesLATIHAN1iqbal HilmawanNo ratings yet

- M9-Exporting, Importing and Global SourcingDocument5 pagesM9-Exporting, Importing and Global SourcingSharon Cadampog Mananguite100% (1)

- Ethiopian Research PaperDocument4 pagesEthiopian Research Paperfvet7q93100% (1)

- Grievance and Grievance ProcedureDocument9 pagesGrievance and Grievance ProcedurePatricia Bianca ArceoNo ratings yet

- Cultural Drivers of Corruption in GovernanceDocument2 pagesCultural Drivers of Corruption in GovernanceJonalvin KENo ratings yet

- ZL30320 DataSheetDocument87 pagesZL30320 DataSheetPhongNo ratings yet

- PCTG ActivitiesDocument41 pagesPCTG ActivitiesDave MatusalemNo ratings yet

- Master Supplier Services Agreement (MSSA) US EnglishDocument21 pagesMaster Supplier Services Agreement (MSSA) US English21flybabyNo ratings yet

- BA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Document42 pagesBA 123 2 Sem AY 22-23 (Aratea/Magana/Placido)Becky GonzagaNo ratings yet

- Proof of Payment-3Document1 pageProof of Payment-3Lucas NegotaNo ratings yet