You might also like

- Bridgewater Presentation 2017-10 San JoaquinDocument28 pagesBridgewater Presentation 2017-10 San Joaquinrdarty100% (2)

- Case Study: Vodafone EgyptDocument2 pagesCase Study: Vodafone EgyptIslam Ayman Mashaly50% (2)

- Ryan Higa's How To Write Good: PrologueDocument9 pagesRyan Higa's How To Write Good: PrologueIsabella Biedenharn89% (9)

- Combinepdf PDFDocument4 pagesCombinepdf PDFAnonymous suPM2lLcNo ratings yet

- The Artisan - Northland Wealth Management - Spring 2016Document8 pagesThe Artisan - Northland Wealth Management - Spring 2016Victor KNo ratings yet

- BUY BUY BUY BUY: Johnson & JohnsonDocument5 pagesBUY BUY BUY BUY: Johnson & Johnsonderek_2010No ratings yet

- Short Put Put Spread Put Backspre Ad Put Ratio Backspre Ad Strangle Iron CondorDocument9 pagesShort Put Put Spread Put Backspre Ad Put Ratio Backspre Ad Strangle Iron CondorSean GilbertNo ratings yet

- Public Expert - Trend IndicatorsDocument21 pagesPublic Expert - Trend Indicatorsrayan comp100% (1)

- BUY BUY BUY BUY: First Solar IncDocument5 pagesBUY BUY BUY BUY: First Solar IncCarlos TresemeNo ratings yet

- Master of Arts : EconomicsDocument21 pagesMaster of Arts : EconomicsnitikanehiNo ratings yet

- Terms-Of-Trade-Shocks-Are-Not-All-Alike - BOEDocument30 pagesTerms-Of-Trade-Shocks-Are-Not-All-Alike - BOEjkkjkdNo ratings yet

- LME FerrousDocument4 pagesLME Ferrousstendley busanNo ratings yet

- Women S Prints Graphics Forecast A W 22 23 Rerooted NatureDocument21 pagesWomen S Prints Graphics Forecast A W 22 23 Rerooted Naturepaula venancioNo ratings yet

- Slater Investments: Managed Funds ServiceDocument1 pageSlater Investments: Managed Funds Serviceyeray MoreiraNo ratings yet

- Put Back Spread Non RatioDocument1 pagePut Back Spread Non RatioSean GilbertNo ratings yet

- Campeonato Power 1Document2 pagesCampeonato Power 1BastianNo ratings yet

- Daily Trading Stance - 2009-12-08Document3 pagesDaily Trading Stance - 2009-12-08Trading FloorNo ratings yet

- FLRY3.SA Tearsheet 2021-11-13Document7 pagesFLRY3.SA Tearsheet 2021-11-13Matheus Augusto Campos PiresNo ratings yet

- 03 Fine Fare 126 Clarke STDocument1 page03 Fine Fare 126 Clarke STteto degNo ratings yet

- Arketeer: 59 Glenridge Ave. - Montclair - 973-783-3333Document16 pagesArketeer: 59 Glenridge Ave. - Montclair - 973-783-3333CoolerAdsNo ratings yet

- Untitled NotebookDocument2 pagesUntitled NotebookRafif KastaraNo ratings yet

- Next Generation Credit CurvesDocument2 pagesNext Generation Credit CurvesbobmezzNo ratings yet

- Numis PE DataDocument12 pagesNumis PE Datarf_1238No ratings yet

- BARILOCHE Masonry APRIL 18-24,2016 PDFDocument1 pageBARILOCHE Masonry APRIL 18-24,2016 PDFJubi SevillaNo ratings yet

- Reach Half Year Presentation FINAL Low Res PDFDocument41 pagesReach Half Year Presentation FINAL Low Res PDFflorintrmNo ratings yet

- Probability Distribution and Statistics: Key Points of LearningDocument24 pagesProbability Distribution and Statistics: Key Points of LearningMohamed HussienNo ratings yet

- BUY BUY BUY BUY: Novo Nordisk A/SDocument5 pagesBUY BUY BUY BUY: Novo Nordisk A/Sderek_2010No ratings yet

- New Horizons in Blasting - The Innovation ImperativeDocument14 pagesNew Horizons in Blasting - The Innovation ImperativeKasse VarillasNo ratings yet

- A320 Ata 32 (5) CattsDocument1 pageA320 Ata 32 (5) CattsabmedhussNo ratings yet

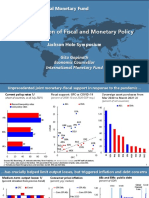

- The Interaction of Fiscal and Monetary Policy 1630094576Document11 pagesThe Interaction of Fiscal and Monetary Policy 1630094576AngeNo ratings yet

- Unit-2 - Index NumbersDocument9 pagesUnit-2 - Index NumbersManas KumarNo ratings yet

- School Form 5 Report On Promotion and Learning Progress AchievementDocument4 pagesSchool Form 5 Report On Promotion and Learning Progress AchievementTinTinNo ratings yet

- Oxygen - October 2018 AUDocument132 pagesOxygen - October 2018 AUJulioNo ratings yet

- Three Key Surprises For 2011: Ronan Carr, CFADocument3 pagesThree Key Surprises For 2011: Ronan Carr, CFAmittleNo ratings yet

- BrandZ - Top100 Global Brands (Kantar-WPP)Document189 pagesBrandZ - Top100 Global Brands (Kantar-WPP)Aadhar BhardwajNo ratings yet

- Set To Pop vs. Initial Audible DischargeDocument1 pageSet To Pop vs. Initial Audible DischargeDANIEL LIMNo ratings yet

- P036 Rebel Morley 10.02.16Document1,147 pagesP036 Rebel Morley 10.02.16Michelle PendletonNo ratings yet

- Dec23 OvpdfDocument12 pagesDec23 OvpdfmeNo ratings yet

- Daily Trading Stance - 2009-12-23Document3 pagesDaily Trading Stance - 2009-12-23Trading FloorNo ratings yet

- Gilbarco LegacyDocument14 pagesGilbarco LegacyRick AlingalanNo ratings yet

- 03 Fine Fare 126 Clark St-5Document1 page03 Fine Fare 126 Clark St-5teto degNo ratings yet

- Charting Basics 2 PDFDocument7 pagesCharting Basics 2 PDFLita HerdianingrumNo ratings yet

- Daily Trading Stance - 2009-12-22Document3 pagesDaily Trading Stance - 2009-12-22Trading FloorNo ratings yet

- Dollar Tree, Inc.: Michael Zhu Will SmithDocument18 pagesDollar Tree, Inc.: Michael Zhu Will SmithShonit ChamadiaNo ratings yet

- NSW20110202Document24 pagesNSW20110202masoudjounNo ratings yet

- Optimization Modelling For Business AnalysisDocument3 pagesOptimization Modelling For Business AnalysispranavNo ratings yet

- Your Choice Your Future Oyap PosterDocument1 pageYour Choice Your Future Oyap Posterapi-300259780No ratings yet

- ExpeditorsDocument11 pagesExpeditorsderek_2010100% (1)

- Hilton Food Group PLCDocument4 pagesHilton Food Group PLCHoa ĐặngNo ratings yet

- ADMISSION BROUCHER 22.06.2021 FOR PRINT (Final)Document2 pagesADMISSION BROUCHER 22.06.2021 FOR PRINT (Final)Santosh Kumar GowdaNo ratings yet

- Flyer ExperienceDocument5 pagesFlyer ExperienceKmnzmnNo ratings yet

- BUY BUY BUY BUY: Skyworks Solutions IncDocument5 pagesBUY BUY BUY BUY: Skyworks Solutions Incderek_2010No ratings yet

- BlackRock Asian Tiger Bond FundDocument2 pagesBlackRock Asian Tiger Bond FundDavid LamNo ratings yet

- Controle de Estoque de Equipamento de Proteção Individual: S S S S S S S S S S S S S S S S S S S S S S S S S S S S S S SDocument14 pagesControle de Estoque de Equipamento de Proteção Individual: S S S S S S S S S S S S S S S S S S S S S S S S S S S S S S SHeitor ConstantinoNo ratings yet

- 03 Musgrave Thin (1948)Document18 pages03 Musgrave Thin (1948)Alvaro ArroyoNo ratings yet

- BrandZ Global Top 100 2020 InfographicDocument1 pageBrandZ Global Top 100 2020 InfographicKaran MusaleNo ratings yet

- October 2020 Independence TitleDocument78 pagesOctober 2020 Independence TitleKent ReddingNo ratings yet

- BUY BUY BUY BUY: Pepsico IncDocument5 pagesBUY BUY BUY BUY: Pepsico Incderek_2010No ratings yet

- Framing TerraceDocument1 pageFraming TerraceSimran KaurNo ratings yet

- The Beertija Cjenik 06.03.2023Document1 pageThe Beertija Cjenik 06.03.2023Ivan VučinaNo ratings yet

- Australian Motorcycle News 24.09.2020Document116 pagesAustralian Motorcycle News 24.09.2020autotech master100% (1)

- Morg Stan Investment 1Document3 pagesMorg Stan Investment 1mittleNo ratings yet

- Funding Position of Banks Improving. Spanish Banks'Document3 pagesFunding Position of Banks Improving. Spanish Banks'mittleNo ratings yet

- Water Market Insights 4Document5 pagesWater Market Insights 4mittleNo ratings yet

- Morg Stan 4Document4 pagesMorg Stan 4mittleNo ratings yet

- ISO Country Codes: Government Commonly Exerts Great Influence On Water IndustryDocument5 pagesISO Country Codes: Government Commonly Exerts Great Influence On Water IndustrymittleNo ratings yet

- Valuation Dispersion Has Widened by 1SD Since Sep: Exhibit 46Document4 pagesValuation Dispersion Has Widened by 1SD Since Sep: Exhibit 46mittleNo ratings yet

- Three Key Surprises For 2011: Ronan Carr, CFADocument3 pagesThree Key Surprises For 2011: Ronan Carr, CFAmittleNo ratings yet

- Morg Stan 3Document4 pagesMorg Stan 3mittleNo ratings yet

- Morg Stan 2Document4 pagesMorg Stan 2mittleNo ratings yet

- Water Market Insights 1Document5 pagesWater Market Insights 1mittleNo ratings yet

- DB Food Insights 2Document9 pagesDB Food Insights 2mittleNo ratings yet

- DB Food Insights 4Document9 pagesDB Food Insights 4mittleNo ratings yet

- Water Market Insights 3Document5 pagesWater Market Insights 3mittleNo ratings yet

- DB Food Insights 1Document9 pagesDB Food Insights 1mittleNo ratings yet

- Water Market Insights 5Document8 pagesWater Market Insights 5mittleNo ratings yet

- DB Food Insights 3Document9 pagesDB Food Insights 3mittleNo ratings yet

- JSWE Results ReviewDocument7 pagesJSWE Results ReviewmittleNo ratings yet

- BGR Upside Buy RecoDocument11 pagesBGR Upside Buy RecomittleNo ratings yet

- Capex JSWE InitiateDocument13 pagesCapex JSWE InitiatemittleNo ratings yet

- Gujrat On The RoadDocument15 pagesGujrat On The RoadmittleNo ratings yet

- MacroEco Initiate BuyDocument21 pagesMacroEco Initiate BuymittleNo ratings yet

- Kotak Stratgy Whose Wealth Report PDFDocument5 pagesKotak Stratgy Whose Wealth Report PDFmittleNo ratings yet

- Binging Big On BTG : BUY Key Take AwayDocument17 pagesBinging Big On BTG : BUY Key Take AwaymittleNo ratings yet

- Sugar Space Update 2010Document2 pagesSugar Space Update 2010mittleNo ratings yet

- FMCG 20101112 RelgareDocument6 pagesFMCG 20101112 RelgaremittleNo ratings yet

- Polaris Software Lab: A Tale of Two BusinessesDocument32 pagesPolaris Software Lab: A Tale of Two BusinessesmittleNo ratings yet

- MSFL Result UpdateDocument6 pagesMSFL Result UpdatemittleNo ratings yet

- JSW Steel LTD Results ReviewDocument7 pagesJSW Steel LTD Results ReviewmittleNo ratings yet

- Larsen & Toubro: Margins Take A HitDocument6 pagesLarsen & Toubro: Margins Take A HitmittleNo ratings yet

- Sterlite Industries: Management Meet NoteDocument5 pagesSterlite Industries: Management Meet NotemittleNo ratings yet

- Hm70 Mobile Chipset BriefDocument4 pagesHm70 Mobile Chipset BriefUmair Latif KhanNo ratings yet

- Multotec Trommel ScreensDocument6 pagesMultotec Trommel Screensalfredo_17110% (1)

- Week 1 Tutorial ProblemsDocument7 pagesWeek 1 Tutorial ProblemsWOP INVESTNo ratings yet

- Spareparts Air Suspension BPW 2022 EN 31052201Document154 pagesSpareparts Air Suspension BPW 2022 EN 31052201cursor10No ratings yet

- CHP 6. Cost Sheet - CapranavDocument14 pagesCHP 6. Cost Sheet - CapranavMonikaNo ratings yet

- ACCT 250 - Principles of Auditing Spring 2022, Section 2 Handout 11 - Power BI Exercise QuestionsDocument6 pagesACCT 250 - Principles of Auditing Spring 2022, Section 2 Handout 11 - Power BI Exercise QuestionsRaza HashmeNo ratings yet

- Internship ReportDocument54 pagesInternship ReportAparnaNo ratings yet

- Factorytalk View Studio: Manually Removing An Application From Existing Application ListDocument3 pagesFactorytalk View Studio: Manually Removing An Application From Existing Application ListAndrea CupelloNo ratings yet

- Manta Aislante ThermalceramicsDocument2 pagesManta Aislante Thermalceramicsjast111No ratings yet

- Mike O'Hearn's Power Bodybuilding 12-Week Training ProgramDocument7 pagesMike O'Hearn's Power Bodybuilding 12-Week Training ProgramRay0% (1)

- SDDSDDocument2 pagesSDDSDKaushalya PereraNo ratings yet

- Step 1. Getting Started.: CounterclaimDocument15 pagesStep 1. Getting Started.: CounterclaimballNo ratings yet

- SIP5 7SK82-85 V07.90 Manual C024-8 en PDFDocument1,750 pagesSIP5 7SK82-85 V07.90 Manual C024-8 en PDFPetre GabrielNo ratings yet

- Salary Report Enterprise Architecture 2Document12 pagesSalary Report Enterprise Architecture 2osNo ratings yet

- Electrochimica Acta 50 (2005) 4174-4181Document8 pagesElectrochimica Acta 50 (2005) 4174-4181Dulce BaezaNo ratings yet

- Slides - Walmart UndergradDocument23 pagesSlides - Walmart UndergradRon BourbondyNo ratings yet

- Blender Annual Report 2020 v1Document32 pagesBlender Annual Report 2020 v1nallabelipavanNo ratings yet

- Land Transfer FormDocument5 pagesLand Transfer FormKarma WangdiNo ratings yet

- BENGUET A TOUR ITINERARY PROPOSAL-1Document7 pagesBENGUET A TOUR ITINERARY PROPOSAL-1Jupiter MercaderoNo ratings yet

- TYBAF 138 Mohnish MehtaDocument10 pagesTYBAF 138 Mohnish MehtaKomal JainNo ratings yet

- Chapter 4 Audit f8 - 2.3Document43 pagesChapter 4 Audit f8 - 2.3JosephineMicheal17No ratings yet

- Mep Risk AssessmentDocument2 pagesMep Risk AssessmentIm Chinith100% (1)

- Writing Process Worksheet (Accompanies Unit 7, Page 59) : Name: DateDocument3 pagesWriting Process Worksheet (Accompanies Unit 7, Page 59) : Name: DateselvinNo ratings yet

- Tarea Bodegas de Datos Capítulos 4 y 5 PDFDocument5 pagesTarea Bodegas de Datos Capítulos 4 y 5 PDFOscar Mauricio AragónNo ratings yet

- Product Cycle TheoryDocument10 pagesProduct Cycle TheoryPalak Sonam Paryani100% (1)

- PPG-Self Directed Workforce Company OverviewDocument3 pagesPPG-Self Directed Workforce Company OverviewKrishNo ratings yet

- 50 Globe Mackay Cable and Radio COrporation vs. Court of AppealsDocument4 pages50 Globe Mackay Cable and Radio COrporation vs. Court of AppealsGlomarie GonayonNo ratings yet

- Project Management For Managers My Notes 1Document27 pagesProject Management For Managers My Notes 1DaisyNo ratings yet