You might also like

- How To Build A Brand EbookDocument22 pagesHow To Build A Brand EbookyaswanthNo ratings yet

- Goodweek Tires SolutionDocument4 pagesGoodweek Tires SolutionEfri DwiyantoNo ratings yet

- E-Commerce and Its Impact On The WorldDocument32 pagesE-Commerce and Its Impact On The Worldfariha.swarna09No ratings yet

- RMIT International University Vietnam: Assignment Cover PageDocument28 pagesRMIT International University Vietnam: Assignment Cover PageHoang DoanNo ratings yet

- A Beginner's Guide To Mobile Marketing: Molly Garris Karen MishraDocument168 pagesA Beginner's Guide To Mobile Marketing: Molly Garris Karen MishraDipak ChauhanNo ratings yet

- Personal Statements To Robert Gordon UniversityDocument1 pagePersonal Statements To Robert Gordon Universitywalexlo210100% (4)

- Star Daks Co. Star Daks Iced - Coffee JellyDocument37 pagesStar Daks Co. Star Daks Iced - Coffee JellyGerald Nicolas33% (3)

- Framework For Business Analysis and Valuation Using Financial StatementsDocument18 pagesFramework For Business Analysis and Valuation Using Financial StatementsFarhat987No ratings yet

- Financial StatementDocument46 pagesFinancial StatementViNo ratings yet

- Marketing Tutorial AnsDocument28 pagesMarketing Tutorial AnssudishNo ratings yet

- Organizational StructureDocument14 pagesOrganizational Structurearlin67% (6)

- Nielsen BASES SolutionDocument59 pagesNielsen BASES SolutionkamblitusharNo ratings yet

- Dividend Policy and Retained Earnings: Foundations of Financial ManagementDocument38 pagesDividend Policy and Retained Earnings: Foundations of Financial ManagementBlack UnicornNo ratings yet

- Chapter 13 MK 2Document5 pagesChapter 13 MK 2Novelda100% (1)

- A Nut Case Assignment 2Document2 pagesA Nut Case Assignment 2Priya Murmu33% (3)

- PROG8520 - Week 10 - SlidesDocument96 pagesPROG8520 - Week 10 - Slidessimran sidhuNo ratings yet

- Valuation and Rates of Return: Foundations of Financial ManagementDocument42 pagesValuation and Rates of Return: Foundations of Financial ManagementBlack UnicornNo ratings yet

- Asset Recognition and Operating Assets: Fourth EditionDocument55 pagesAsset Recognition and Operating Assets: Fourth EditionAyush JainNo ratings yet

- PROG8520 - Week 9 - SlidesDocument43 pagesPROG8520 - Week 9 - Slidessimran sidhuNo ratings yet

- Student International Marketing 15th Edition Chapter 13Document14 pagesStudent International Marketing 15th Edition Chapter 13lmnop123whatNo ratings yet

- Chapter 1 5Document81 pagesChapter 1 5Anzene JasulNo ratings yet

- MA2 (100 QS)Document30 pagesMA2 (100 QS)Alina NaeemNo ratings yet

- Ahmad FA - Chapter4Document1 pageAhmad FA - Chapter4ahmadfaNo ratings yet

- Managerial Finance - Final ExamDocument3 pagesManagerial Finance - Final Examiqbal78651No ratings yet

- Seminar Practice 7 Solutions (Latest)Document54 pagesSeminar Practice 7 Solutions (Latest)Feeling_so_fly100% (1)

- Precision Worldwide, Inc.Document3 pagesPrecision Worldwide, Inc.karan_w3No ratings yet

- 151 0105Document37 pages151 0105api-27548664No ratings yet

- 0304 - Ec 1Document30 pages0304 - Ec 1haryhunter100% (3)

- The Cost of Capital: HKD 100,000,000 HKD 250,000,000 HKD 150,000,000 HKD 250,000,000Document24 pagesThe Cost of Capital: HKD 100,000,000 HKD 250,000,000 HKD 150,000,000 HKD 250,000,000chandel08No ratings yet

- Guna Fiber LTDDocument5 pagesGuna Fiber LTDKshitishNo ratings yet

- Problems: Week Crew Size Yards InstalledDocument2 pagesProblems: Week Crew Size Yards Installedfarnaz afshariNo ratings yet

- Beta Management QuestionsDocument1 pageBeta Management QuestionsbjhhjNo ratings yet

- Swati Anand - FRMcaseDocument5 pagesSwati Anand - FRMcaseBhavin MohiteNo ratings yet

- Lecture Slides - Fraud Schemes & Red Flags of FraudDocument11 pagesLecture Slides - Fraud Schemes & Red Flags of FraudJonnel Sadian AcobaNo ratings yet

- frm指定教材 risk management & derivativesDocument1,192 pagesfrm指定教材 risk management & derivativeszeno490No ratings yet

- 7 LP Sensitivity AnalysisDocument9 pages7 LP Sensitivity AnalysiszuluagagaNo ratings yet

- Marshall Chapter 3 Case StudyDocument2 pagesMarshall Chapter 3 Case Studyapi-3173686540% (1)

- Chapter # 6Document73 pagesChapter # 6Adil AliNo ratings yet

- Chapter 18Document17 pagesChapter 18queen hassaneenNo ratings yet

- Parkinmicro13 1300Document29 pagesParkinmicro13 1300saurabhNo ratings yet

- Presented by - Kshitiz Deepanshi Bhanu Pratap Singh Manali Aditya AnjulDocument13 pagesPresented by - Kshitiz Deepanshi Bhanu Pratap Singh Manali Aditya AnjulBhanu NirwanNo ratings yet

- NN 5 Chap 4 Review of AccountingDocument10 pagesNN 5 Chap 4 Review of AccountingNguyet NguyenNo ratings yet

- LP FormulationDocument21 pagesLP FormulationVarun Pillai100% (1)

- Exam 1 Review ProblemsDocument2 pagesExam 1 Review ProblemsAdamNo ratings yet

- Final Draft - MFIDocument38 pagesFinal Draft - MFIShaquille SmithNo ratings yet

- Unemployment and Its Natural Rate: Solutions To Textbook ProblemsDocument12 pagesUnemployment and Its Natural Rate: Solutions To Textbook ProblemsMainland FounderNo ratings yet

- Solutions Chapter 7Document39 pagesSolutions Chapter 7Brenda Wijaya100% (2)

- Chapter 008 Stock Valuation: Aacsb Topic: Analytic SECTION: 8.1 Topic: Stock Value Type: ProblemsDocument23 pagesChapter 008 Stock Valuation: Aacsb Topic: Analytic SECTION: 8.1 Topic: Stock Value Type: Problemsdarling assylaNo ratings yet

- Toon Eneco PDFDocument4 pagesToon Eneco PDFDHEEPIKANo ratings yet

- Zong BDocument3 pagesZong BAbdul Rehman AmiwalaNo ratings yet

- Fin516 Week5 HW ScribdDocument2 pagesFin516 Week5 HW ScribdmsspellaNo ratings yet

- Answer All The QuestionsDocument2 pagesAnswer All The QuestionsSunita Kumari50% (2)

- ACC 121 Chapter 1 Exercise SolutionsDocument12 pagesACC 121 Chapter 1 Exercise SolutionsDarrianAustinNo ratings yet

- Solutions - Chapter 5Document21 pagesSolutions - Chapter 5Dre ThathipNo ratings yet

- Question Bank Operations Management MGA 602Document6 pagesQuestion Bank Operations Management MGA 602Jennifer JosephNo ratings yet

- The Correct Answer For Each Question Is Indicated by ADocument19 pagesThe Correct Answer For Each Question Is Indicated by Aakash deepNo ratings yet

- GM588 - Practice Quiz 1Document4 pagesGM588 - Practice Quiz 1Chooy100% (1)

- Case Study 1: E-Procurement at IBM: Answer The Questions (A)Document5 pagesCase Study 1: E-Procurement at IBM: Answer The Questions (A)Zannatun NayeemNo ratings yet

- Cost Sheet For The Month of January: TotalDocument9 pagesCost Sheet For The Month of January: TotalgauravpalgarimapalNo ratings yet

- The Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeDocument3 pagesThe Quaker Oats Company and Subsidiaries Consolidated Statements of IncomeNaseer AhmedNo ratings yet

- Testbank Opmen For UTSDocument67 pagesTestbank Opmen For UTSPaskalis KrisnaaNo ratings yet

- MidlandDocument4 pagesMidlandsophieNo ratings yet

- Group 3 - Lending Club Case Study Solutions FinalDocument2 pagesGroup 3 - Lending Club Case Study Solutions FinalArpita GuptaNo ratings yet

- Did United Technologies Overpay For Rockwell CollinsDocument2 pagesDid United Technologies Overpay For Rockwell CollinsRadNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- The Truth About Material Wealth: Is It God’S Blessing in Disguise?From EverandThe Truth About Material Wealth: Is It God’S Blessing in Disguise?No ratings yet

- 1/340/chap15: Price ($) Quantity TR TC Profit MRDocument8 pages1/340/chap15: Price ($) Quantity TR TC Profit MRHồ Xuân PhátNo ratings yet

- Transfer Pricing SectionDocument12 pagesTransfer Pricing SectionMM Fakhrul IslamNo ratings yet

- Suppose Demand and SupplyDocument3 pagesSuppose Demand and Supplyvincent chandraNo ratings yet

- Chapter13 Transfer PricingDocument5 pagesChapter13 Transfer PricingDayan DudosNo ratings yet

- Major Association of Accounting President UniversityDocument1 pageMajor Association of Accounting President UniversityDicky Leonardo LoisNo ratings yet

- Audit Project 3Document3 pagesAudit Project 3Dicky Leonardo LoisNo ratings yet

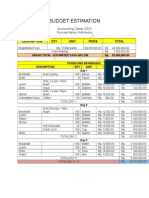

- Budget Estimation: Description QTY Unit Price TotalDocument4 pagesBudget Estimation: Description QTY Unit Price TotalDicky Leonardo LoisNo ratings yet

- LPJ KPMG 4seas ScholarshipDocument13 pagesLPJ KPMG 4seas ScholarshipDicky Leonardo LoisNo ratings yet

- Running Head: Qualitative Research 1Document36 pagesRunning Head: Qualitative Research 1Akanchha JoshiNo ratings yet

- Appointment-Setting Sales Script: Scenario 1: (Prospect Agrees)Document4 pagesAppointment-Setting Sales Script: Scenario 1: (Prospect Agrees)Kenn Guk-ongNo ratings yet

- Blue White and Black Geometric Mathematics Lesson Math Creative Presentation SlidesCarnivalDocument23 pagesBlue White and Black Geometric Mathematics Lesson Math Creative Presentation SlidesCarnivalUmer HanifNo ratings yet

- Retail Marketing200813 PDFDocument289 pagesRetail Marketing200813 PDFRaja .SNo ratings yet

- Mb0046 Marketing Management BookDocument285 pagesMb0046 Marketing Management BookeraseemaNo ratings yet

- Market Research Cover Letter SampleDocument7 pagesMarket Research Cover Letter Samplef5dgrnzh100% (2)

- Marketing Plan For: Jasli TradingDocument39 pagesMarketing Plan For: Jasli TradingDonita BinayNo ratings yet

- Coca Cola Sss MarketingDocument126 pagesCoca Cola Sss MarketingSrikanth DixitNo ratings yet

- Unit-4 Service MarketingDocument17 pagesUnit-4 Service MarketingRIYA JAINNo ratings yet

- MIS205 Final DarazDocument22 pagesMIS205 Final DarazSojib AliNo ratings yet

- TescoDocument3 pagesTescoSukrut ParikhNo ratings yet

- Wk. 10 - Aggregating Multiple Products in A Single OrderDocument10 pagesWk. 10 - Aggregating Multiple Products in A Single Orderpapa wawaNo ratings yet

- Unit 04 - Marketing Principles Front Sheet 1 PDFDocument29 pagesUnit 04 - Marketing Principles Front Sheet 1 PDFQuiela QueenNo ratings yet

- Buysiness of AdditivcesDocument17 pagesBuysiness of AdditivcesmohammedNo ratings yet

- Business NameDocument6 pagesBusiness NameMelodee Jackson100% (1)

- LakmeDocument39 pagesLakmepriyanka_gandhi280% (1)

- 303 Production and Operation Management Ajay PDFDocument10 pages303 Production and Operation Management Ajay PDFAnkita Dash100% (1)

- Chapter 18 - The Financial and Economic Impact of ServiceDocument23 pagesChapter 18 - The Financial and Economic Impact of ServiceKushal B GowdaNo ratings yet

- CustomerDocument2 pagesCustomerElliot RichardNo ratings yet

- Lehigh SteelDocument12 pagesLehigh SteelAto SumartoNo ratings yet