You might also like

- Controlling & LeadershipDocument55 pagesControlling & LeadershipSaurabh PednekarNo ratings yet

- BIG Slide CopiesDocument31 pagesBIG Slide CopiesScara MungendjeNo ratings yet

- Sesi5 Internal Audit ApproachDocument13 pagesSesi5 Internal Audit ApproachMaitland RowesNo ratings yet

- Isms Final QBDocument26 pagesIsms Final QBGlowing StarNo ratings yet

- Assignment 3 - Methodological Planning in Audit DesignDocument7 pagesAssignment 3 - Methodological Planning in Audit DesignsadeadamNo ratings yet

- 9001LA MockExam-KeyDocument17 pages9001LA MockExam-KeyAamir Sirohi92% (26)

- Explain: Section One - Five Questions Worth Two Marks Each - Maximum 10 MarksDocument10 pagesExplain: Section One - Five Questions Worth Two Marks Each - Maximum 10 MarksAamir Sirohi91% (33)

- Solution Aud589 - Jul 2017Document8 pagesSolution Aud589 - Jul 2017LANGITBIRU100% (1)

- 45001LA-Mock Exam KeyDocument17 pages45001LA-Mock Exam KeyAamir Sirohi93% (15)

- Assignment # 3Document4 pagesAssignment # 3Elisabeth HenangerNo ratings yet

- Confidential AC/JULY 2021/AUD679: © Hak Cipta Universiti Teknologi MARADocument171 pagesConfidential AC/JULY 2021/AUD679: © Hak Cipta Universiti Teknologi MARAAnisNo ratings yet

- 09 Internal ControlsDocument15 pages09 Internal ControlsIbnu NugrohoNo ratings yet

- Risk Control Matrix Coso Framework CasestudyDocument3 pagesRisk Control Matrix Coso Framework Casestudyshakir ahmedNo ratings yet

- Internal Audit and Control MF0013 Spring Drive Assignment-2012Document26 pagesInternal Audit and Control MF0013 Spring Drive Assignment-2012Sneha JenaNo ratings yet

- Supplement To Syllabus (4 Pages)Document4 pagesSupplement To Syllabus (4 Pages)Yasmine NyouriNo ratings yet

- ACCT3043 Unit 3 For PostingDocument9 pagesACCT3043 Unit 3 For PostingKatrina EustaceNo ratings yet

- Chapter 9 NotesDocument12 pagesChapter 9 NotesSavy DhillonNo ratings yet

- Operational Audit Notes by RBDocument1 pageOperational Audit Notes by RBVrinda KNo ratings yet

- Internal AuditDocument39 pagesInternal AuditeosmostafaNo ratings yet

- 965QG Volume 4 Auditing in An IT Environment 2Document53 pages965QG Volume 4 Auditing in An IT Environment 2Jerwin ParallagNo ratings yet

- Chapter10Document2 pagesChapter10Keanne ArmstrongNo ratings yet

- RPS Pemeriksaan Akuntansi 2Document21 pagesRPS Pemeriksaan Akuntansi 2dennis wahyuda0% (1)

- TestPlan - Website Quan Ly Trung Tam Tin HocDocument10 pagesTestPlan - Website Quan Ly Trung Tam Tin HocHa NhNo ratings yet

- Aramco STD GuideDocument25 pagesAramco STD Guidehassan100% (10)

- Test of Controls MADocument19 pagesTest of Controls MAMëŕĕ ĻöľõmãNo ratings yet

- ISO IQA For DDFC by AJMAL29-04-14Document52 pagesISO IQA For DDFC by AJMAL29-04-14Waqas WaqasNo ratings yet

- Smu 4th Sem Operation Management AssignmentsDocument11 pagesSmu 4th Sem Operation Management AssignmentsProjectHelpForuNo ratings yet

- Internal Quality Auditing ProcedureDocument7 pagesInternal Quality Auditing ProcedurePrime CapNo ratings yet

- Isa 330 PDFDocument27 pagesIsa 330 PDFMarcos ViníciusNo ratings yet

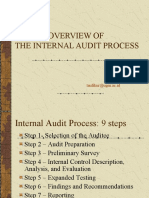

- Sesi6 Overview of The Internal Audit ProcessDocument14 pagesSesi6 Overview of The Internal Audit ProcessMaitland RowesNo ratings yet

- Testing - General and Automated Controls: Mentor: TS. Truong Tuan Anh Presenter: Huynh Thi NanDocument55 pagesTesting - General and Automated Controls: Mentor: TS. Truong Tuan Anh Presenter: Huynh Thi NanBi NguyễnNo ratings yet

- CHAPTER 1: Fundamentals of Testing 1.1 Why Is Testing Necessary (K2) 1.1.1 Software Systems Context (K1)Document9 pagesCHAPTER 1: Fundamentals of Testing 1.1 Why Is Testing Necessary (K2) 1.1.1 Software Systems Context (K1)Crystaly CrysNo ratings yet

- Control Testing Vs Substantive by CPA MADHAV BHANDARIDocument59 pagesControl Testing Vs Substantive by CPA MADHAV BHANDARIMacmilan Trevor JamuNo ratings yet

- Root Cause Analysis20188Document12 pagesRoot Cause Analysis20188Yasser BouzeghaiaNo ratings yet

- Chapter 10 - Risk Response Audit Strategy Approach and Program - NotesDocument9 pagesChapter 10 - Risk Response Audit Strategy Approach and Program - NotesSavy DhillonNo ratings yet

- At 04 Auditing PlanningDocument8 pagesAt 04 Auditing PlanningJelyn RuazolNo ratings yet

- Qual06 2 2Document20 pagesQual06 2 2paratevedant1403No ratings yet

- ECRS TrainingDocument23 pagesECRS Trainingdhalsin83No ratings yet

- QMS Internal Audit - 1 Day TrainngDocument104 pagesQMS Internal Audit - 1 Day TrainngFleur RoblesNo ratings yet

- Chapter 13 - AUDIT PRINCIPLESDocument38 pagesChapter 13 - AUDIT PRINCIPLESdipikamalpani1402No ratings yet

- Principle of AuditingDocument30 pagesPrinciple of Auditing21BCB27 Lakshmi.ENo ratings yet

- Combined Internal Auditor (ISO 9001 - 2015, ISO 14001 - 2015 and ISO 45001)Document28 pagesCombined Internal Auditor (ISO 9001 - 2015, ISO 14001 - 2015 and ISO 45001)tom_crekNo ratings yet

- Auditing in CIS EnvironmentDocument35 pagesAuditing in CIS Environmentcyrileecalata31No ratings yet

- Assignment 08Document9 pagesAssignment 08ammar mughalNo ratings yet

- Manager's Testing GuideDocument14 pagesManager's Testing Guidesender78No ratings yet

- Bab 1-Audit Approach P.pointDocument17 pagesBab 1-Audit Approach P.pointAslamaitulakma MohamadNo ratings yet

- Cisa Module 1 Part B ExecutionDocument32 pagesCisa Module 1 Part B ExecutionREJAY89No ratings yet

- LS 2.80C - PSA 315 - Identifying and Assessing The Risk of Material MissstatementDocument4 pagesLS 2.80C - PSA 315 - Identifying and Assessing The Risk of Material MissstatementSkye LeeNo ratings yet

- Crux of Matter - Tools and TechnologiesDocument32 pagesCrux of Matter - Tools and TechnologiesSir FarhanNo ratings yet

- Internal Audits: 1. PurposeDocument4 pagesInternal Audits: 1. PurposesumanNo ratings yet

- Difficulties, If There Are Concerns With Compliance, It Implies There Are ProblemsDocument4 pagesDifficulties, If There Are Concerns With Compliance, It Implies There Are ProblemsBrian GoNo ratings yet

- Auditing and Assurance PrinciplesDocument3 pagesAuditing and Assurance PrinciplesPrincess SagreNo ratings yet

- Ste - Unit3 - Presentation UpdatedDocument31 pagesSte - Unit3 - Presentation UpdatedBeastboyRahul GamingNo ratings yet

- What Is An Audit Committee? Discuss Its Value in An OrganizationDocument6 pagesWhat Is An Audit Committee? Discuss Its Value in An Organizationjoyce KimNo ratings yet

- F8-19 Audit SamplingDocument16 pagesF8-19 Audit SamplingReever RiverNo ratings yet

- Lec 2 Is Audit ProcessDocument14 pagesLec 2 Is Audit ProcessAtiya SharfNo ratings yet

- Effective Internal Auditing To ISO 9001:2008: Welza D. Gazo Dti-XiDocument52 pagesEffective Internal Auditing To ISO 9001:2008: Welza D. Gazo Dti-XipadhuskNo ratings yet

- Cisa Notes 2010Document26 pagesCisa Notes 2010Amanda Christine WijayaNo ratings yet

- Guidelines for Organization of Working Papers on Operational AuditsFrom EverandGuidelines for Organization of Working Papers on Operational AuditsNo ratings yet

- Fa Far Sesi 2Document28 pagesFa Far Sesi 2hdyhNo ratings yet

- Topic 8 - Financial Statement Audit InedDocument21 pagesTopic 8 - Financial Statement Audit InedhdyhNo ratings yet

- Question Test Far560 June 2017 Csofp DragonDocument3 pagesQuestion Test Far560 June 2017 Csofp DragonhdyhNo ratings yet

- Solution Aud589 - Jun 2015Document7 pagesSolution Aud589 - Jun 2015LANGITBIRUNo ratings yet

- Storyboard: Control Procedure Test of ControlDocument4 pagesStoryboard: Control Procedure Test of ControlhdyhNo ratings yet

- Past Year Questions Audit PlanningDocument1 pagePast Year Questions Audit PlanninghdyhNo ratings yet

- Datos - Analisis BibliométricoDocument383 pagesDatos - Analisis BibliométricoSofia RodiNo ratings yet

- SAP SecurityDocument6 pagesSAP SecuritySumanthNo ratings yet

- MIS, DSS and ERPDocument7 pagesMIS, DSS and ERPNaveen SarmaNo ratings yet

- Senior Director Solutions Implementation in Atlanta GA Resume Kyle LambertDocument3 pagesSenior Director Solutions Implementation in Atlanta GA Resume Kyle LambertKyleLambertNo ratings yet

- Higher Ed Search FirmsDocument4 pagesHigher Ed Search FirmsEizekel BronzskiNo ratings yet

- Zara Supply Chain Analysis - The Secret Behind Zara's Retail SuccessDocument14 pagesZara Supply Chain Analysis - The Secret Behind Zara's Retail Successarun mamu100% (1)

- HR Audit (MCQ)Document30 pagesHR Audit (MCQ)bijay100% (8)

- Coca Cola - Working InternationallyDocument21 pagesCoca Cola - Working InternationallyUsama ShahNo ratings yet

- Anki Updated ProjectDocument90 pagesAnki Updated ProjectPrints BindingsNo ratings yet

- Accounting - Introduction SummaryDocument2 pagesAccounting - Introduction SummaryWei HouNo ratings yet

- MMCDocument1 pageMMCJaspreet SinghNo ratings yet

- Future of MLM SoftwareDocument2 pagesFuture of MLM SoftwareRubin alexNo ratings yet

- The Executive S&Op Effectiveness ChecklistDocument7 pagesThe Executive S&Op Effectiveness ChecklistSanjay KshirsagarNo ratings yet

- 3 Hank Kolb, Director, Quality AssuranceDocument3 pages3 Hank Kolb, Director, Quality AssuranceEina Gupta100% (1)

- Saira Nokhaiz Saira - Nokhaiz@cs - Uol.edu - PKDocument18 pagesSaira Nokhaiz Saira - Nokhaiz@cs - Uol.edu - PKrooshanayNo ratings yet

- Project Quatity PlanDocument19 pagesProject Quatity PlanhanujaNo ratings yet

- State of Content Marketing 2023Document126 pagesState of Content Marketing 2023pavan teja100% (1)

- ACCT5432-17 - S2 - Seminar Week 1Document20 pagesACCT5432-17 - S2 - Seminar Week 1杨子偏No ratings yet

- Lesson 4 Planning 1Document63 pagesLesson 4 Planning 1Shunuan HuangNo ratings yet

- Ana Rose M. Dacuya: Address: Dar Al Aman 3 Karama, Dubai UAE Email: Mobile: +971 50 860 1578Document2 pagesAna Rose M. Dacuya: Address: Dar Al Aman 3 Karama, Dubai UAE Email: Mobile: +971 50 860 1578bisankhe2No ratings yet

- Closing Out Phase of A Construction Process PDFDocument5 pagesClosing Out Phase of A Construction Process PDFAmna BhullarNo ratings yet

- Issai 1520 PNDocument5 pagesIssai 1520 PNCharlie MaineNo ratings yet

- EMBA ResumeBook 2013 PDFDocument208 pagesEMBA ResumeBook 2013 PDFKC RayNo ratings yet

- Components of SCMDocument6 pagesComponents of SCMPraveen ShuklaNo ratings yet

- BBA 3rd Sem 2018Document62 pagesBBA 3rd Sem 2018Raaj BhandariNo ratings yet

- Auditing Theory SalosagcolDocument4 pagesAuditing Theory SalosagcolYuki CrossNo ratings yet

- Hand Book Management Accounting PDFDocument1,037 pagesHand Book Management Accounting PDFjiveNo ratings yet

- SAP Modules Presentation: Inventory ModuleDocument44 pagesSAP Modules Presentation: Inventory ModuleLaMin AgNo ratings yet

- Model Business Plan For Moringa Processing To Tea PDFDocument92 pagesModel Business Plan For Moringa Processing To Tea PDFUsman Bala86% (7)

- Adidas - Reebok MergerDocument21 pagesAdidas - Reebok MergerAnil KotagaNo ratings yet