You might also like

- Slide Presentasi Ketua KNKG - Kuliah Umum UMS (Juni 2023)Document41 pagesSlide Presentasi Ketua KNKG - Kuliah Umum UMS (Juni 2023)Wahyu Sekar WijayaningtyasNo ratings yet

- Uniathena - Basic Accounting CourseDocument21 pagesUniathena - Basic Accounting CourseAdalia MahabirNo ratings yet

- ACCOUNTS NotesDocument11 pagesACCOUNTS Noteslalteshsharma335No ratings yet

- Shahjalal University of Science &technologyDocument12 pagesShahjalal University of Science &technologyপ্রজ্ঞা লাবনীNo ratings yet

- Introduction To AccountingDocument8 pagesIntroduction To Accountingjesi zamoraNo ratings yet

- Introduction To AccountingDocument8 pagesIntroduction To Accountingjesi zamora0% (1)

- Introduction To AccountingDocument8 pagesIntroduction To Accountingjesi zamoraNo ratings yet

- The Basic Structure of AccountingDocument7 pagesThe Basic Structure of Accountingsabeen ansari0% (1)

- Module #1 in BookkeepingDocument3 pagesModule #1 in Bookkeepingrowena marambaNo ratings yet

- Unit 1 KMBN103Document16 pagesUnit 1 KMBN103Anuj YadavNo ratings yet

- Chapter One: Accounting Practice and PrinciplesDocument16 pagesChapter One: Accounting Practice and PrinciplesTesfamlak MulatuNo ratings yet

- FAR-Module 1 Introduction To Accounting and BusinessDocument14 pagesFAR-Module 1 Introduction To Accounting and BusinessNathaniel MerillesNo ratings yet

- Basic Accounting NotesDocument40 pagesBasic Accounting NotesRae Slaughter100% (1)

- ACFrOgATh4ll eme4yN9J4wE AeppX61MycYp6b kxBGKNDWYW-hlLHNxG6Q1dm3Sb308YSnEn6A1UWx25Q qH7wawCiSvt3tGP3z2KExB-Rn6mziCuybpphN60S2ujKR W7nR4pvK32c0pxu12pDocument16 pagesACFrOgATh4ll eme4yN9J4wE AeppX61MycYp6b kxBGKNDWYW-hlLHNxG6Q1dm3Sb308YSnEn6A1UWx25Q qH7wawCiSvt3tGP3z2KExB-Rn6mziCuybpphN60S2ujKR W7nR4pvK32c0pxu12pMd. Sojib KhanNo ratings yet

- Assignment IDocument12 pagesAssignment ITeke TarekegnNo ratings yet

- Introduction To Accounting-2Document10 pagesIntroduction To Accounting-2Taonga Jean BandaNo ratings yet

- Fa&a All Unit (KMBN 103)Document41 pagesFa&a All Unit (KMBN 103)abdheshkumar7897No ratings yet

- Far ReviewerDocument16 pagesFar ReviewerAizle Trixia AlcarazNo ratings yet

- Fama - Unit 1Document10 pagesFama - Unit 1Shivam TiwariNo ratings yet

- Financial Reporting Objectives and FunctionsDocument12 pagesFinancial Reporting Objectives and FunctionsIsha Manzano LacuestaNo ratings yet

- Finiii Ma PDFDocument299 pagesFiniii Ma PDFNarendraNo ratings yet

- Chapter 1Document7 pagesChapter 1Janah MirandaNo ratings yet

- BCA, BBA, BCOM-Financial AccountingDocument67 pagesBCA, BBA, BCOM-Financial AccountingThrisha Papa (Baby girl)No ratings yet

- EC1 Module-2 2023Document5 pagesEC1 Module-2 2023Reymond MondoñedoNo ratings yet

- Lesson 1 - Review of Basic Accounting (Part 1)Document14 pagesLesson 1 - Review of Basic Accounting (Part 1)Laila RodaviaNo ratings yet

- Accounting and FinanceDocument301 pagesAccounting and FinanceLuvnica Verma100% (2)

- AccountingDocument129 pagesAccountingearl nerpio100% (1)

- Explanation: AccountingDocument7 pagesExplanation: AccountingrbalitreNo ratings yet

- Unit 1 THE FIELD OF ACCOUNTINGDocument9 pagesUnit 1 THE FIELD OF ACCOUNTINGHang NguyenNo ratings yet

- Introduction To Accounting 1st SemDocument15 pagesIntroduction To Accounting 1st SemANJALI KUMARI100% (1)

- Intro to Accounting Lecture NotesDocument15 pagesIntro to Accounting Lecture NotesSaffa IbrahimNo ratings yet

- Fa 1Document18 pagesFa 1Rahul KotagiriNo ratings yet

- BA Module (Day 1)Document60 pagesBA Module (Day 1)Jamie CantubaNo ratings yet

- Accounts UNIT 1Document13 pagesAccounts UNIT 1ayushi dagarNo ratings yet

- Unit - I Management AccountingDocument241 pagesUnit - I Management AccountingABITHA KARANNo ratings yet

- Introduction to Accounting FundamentalsDocument10 pagesIntroduction to Accounting FundamentalsHehe Hehe50No ratings yet

- Introduction to Accounting LectureDocument15 pagesIntroduction to Accounting LectureMary FolawumiNo ratings yet

- ABM - FABM11 IIIa 5Document4 pagesABM - FABM11 IIIa 5Kayelle BelinoNo ratings yet

- Unit 1 - Ffa Study Material-DrjDocument19 pagesUnit 1 - Ffa Study Material-DrjTushar Singh SanuNo ratings yet

- 1. Chap 1 Accounting Nature scope concept and conventionDocument5 pages1. Chap 1 Accounting Nature scope concept and conventionyousaf.mast777No ratings yet

- LESSON 2 Branches of AccountingDocument5 pagesLESSON 2 Branches of AccountingUnamadable UnleomarableNo ratings yet

- B - Fund - Acc - 1 & 2Document248 pagesB - Fund - Acc - 1 & 2newaybeyene5No ratings yet

- Accounting For Managers Chapter 1Document53 pagesAccounting For Managers Chapter 1Filomena AndjambaNo ratings yet

- P of AccDocument113 pagesP of AccYalew WondmnewNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- AccountingDocument4 pagesAccountingFadia CHNo ratings yet

- Accounts 1Document14 pagesAccounts 1Piyush PatelNo ratings yet

- The Whole System of Double Entry Bookkeeping Can Be Summarised in The Following Two RulesDocument13 pagesThe Whole System of Double Entry Bookkeeping Can Be Summarised in The Following Two RuleskhusboojainNo ratings yet

- Bagabag National High School Instructional Modules in FABM 1Document2 pagesBagabag National High School Instructional Modules in FABM 1marissa casareno almueteNo ratings yet

- FA UNIT 1Document24 pagesFA UNIT 1VTNo ratings yet

- Introduction to Accounting and BusinessDocument16 pagesIntroduction to Accounting and BusinessHussen Abdulkadir100% (1)

- Concept / Meaning of AccountingDocument15 pagesConcept / Meaning of AccountingSophiya PrabinNo ratings yet

- Philippine Best Training Systems Colleges Senior High School DepartmentDocument16 pagesPhilippine Best Training Systems Colleges Senior High School DepartmentAllysa Nicole BalinasNo ratings yet

- Accounting and Finance For Managers - Course Material PDFDocument94 pagesAccounting and Finance For Managers - Course Material PDFbil gossayw100% (1)

- 5 Management AccountingDocument299 pages5 Management AccountingChaitanya MulukutlaNo ratings yet

- Financial Accounting FrameworkDocument45 pagesFinancial Accounting Frameworkajit_satapathy1988No ratings yet

- Introduction To Financial Accountin1Document27 pagesIntroduction To Financial Accountin1yug.rokadia100% (1)

- Introduction To Employee Training and DevelopmentDocument28 pagesIntroduction To Employee Training and DevelopmentMahima GirdharNo ratings yet

- Add OnDocument1 pageAdd OnMahima GirdharNo ratings yet

- Formats of SOPL & BS S9 StandardsDocument1 pageFormats of SOPL & BS S9 StandardsMahima GirdharNo ratings yet

- 7 Cs of Business CommunicationDocument15 pages7 Cs of Business CommunicationMahima GirdharNo ratings yet

- Communication For Employment - ResumeDocument15 pagesCommunication For Employment - ResumeMahima Girdhar80% (5)

- Session 6 ContentsDocument1 pageSession 6 ContentsMahima GirdharNo ratings yet

- Balance Sheet FormatDocument1 pageBalance Sheet FormatMahima GirdharNo ratings yet

- HyattDocument2 pagesHyattMahima GirdharNo ratings yet

- Vol1a1' (: / O.7' OnrDocument4 pagesVol1a1' (: / O.7' OnrMahima GirdharNo ratings yet

- Information System For ManagersDocument13 pagesInformation System For ManagersMahima GirdharNo ratings yet

- BA-NCP-1-By SubhodipDocument147 pagesBA-NCP-1-By SubhodipMahima GirdharNo ratings yet

- Analysing and Understanding The Perception of Customers With Reference To AmazonDocument31 pagesAnalysing and Understanding The Perception of Customers With Reference To AmazonMahima GirdharNo ratings yet

- Session 6 ContentsDocument1 pageSession 6 ContentsMahima GirdharNo ratings yet

- BC Loreal ProposalDocument3 pagesBC Loreal ProposalMahima GirdharNo ratings yet

- HUL Mumbai Marketing Report Distribution Channels ProductsDocument2 pagesHUL Mumbai Marketing Report Distribution Channels ProductsMahima GirdharNo ratings yet

- OB Test 3 (Assignment) GuidelinesDocument7 pagesOB Test 3 (Assignment) GuidelinesMahima GirdharNo ratings yet

- Marketing Management ProjectDocument3 pagesMarketing Management ProjectMahima GirdharNo ratings yet

- Varanasi HULDocument2 pagesVaranasi HULMahima GirdharNo ratings yet

- Information System For ManagersDocument13 pagesInformation System For ManagersMahima GirdharNo ratings yet

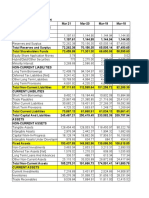

- Financial Management - I SLFI501: AssignmentDocument6 pagesFinancial Management - I SLFI501: AssignmentMahima GirdharNo ratings yet

- Varanasi HULDocument2 pagesVaranasi HULMahima GirdharNo ratings yet

- Analysing and Understanding The Perception of Customers With Reference To AmazonDocument31 pagesAnalysing and Understanding The Perception of Customers With Reference To AmazonMahima GirdharNo ratings yet

- BC Loreal ProposalDocument3 pagesBC Loreal ProposalMahima GirdharNo ratings yet

- RubricsDocument1 pageRubricsMahima GirdharNo ratings yet

- PrivatizationDocument12 pagesPrivatizationMahima GirdharNo ratings yet

- 4 LPGDocument26 pages4 LPGRahul RanjanNo ratings yet

- XYZ Finance Manager ABC Ltd. New Delhi - 110039Document4 pagesXYZ Finance Manager ABC Ltd. New Delhi - 110039Mahima GirdharNo ratings yet

- Afm NotesDocument45 pagesAfm NotesMahima GirdharNo ratings yet

- Employee EngagementDocument7 pagesEmployee EngagementMahima GirdharNo ratings yet

- Monetary Policy Analysis: A Dynamic Stochastic General Equilibrium ApproachDocument45 pagesMonetary Policy Analysis: A Dynamic Stochastic General Equilibrium Approachندى الريحانNo ratings yet

- The Impact of Taxes on Capital Investment DecisionsDocument11 pagesThe Impact of Taxes on Capital Investment DecisionsKariza ReyesNo ratings yet

- Economic & Financial Evaluation of Transportation Projects: Prof. S. L. DhingraDocument165 pagesEconomic & Financial Evaluation of Transportation Projects: Prof. S. L. DhingraHemanth GowdaNo ratings yet

- Tata Steel Annual Report 2022-23-413Document1 pageTata Steel Annual Report 2022-23-413mudikpatwariNo ratings yet

- First E-Bank Tower Condo v. CIRDocument8 pagesFirst E-Bank Tower Condo v. CIRcdacasidsidNo ratings yet

- Six Step Validation Application FormsDocument3 pagesSix Step Validation Application FormsJanardhan ChNo ratings yet

- Corporate Finance FundamentalsDocument171 pagesCorporate Finance FundamentalsMai Nữ Song NgânNo ratings yet

- Cost-Benefit Analysis Excel TemplateDocument5 pagesCost-Benefit Analysis Excel TemplateMustafa Ricky Pramana SeNo ratings yet

- Advanced Financial Accounting Midterm: For Questions 2-4Document13 pagesAdvanced Financial Accounting Midterm: For Questions 2-4Mister MysteriousNo ratings yet

- IAS 33 Earnings Per Share: (Conceptual Framework and Standards)Document8 pagesIAS 33 Earnings Per Share: (Conceptual Framework and Standards)Joyce ManaloNo ratings yet

- Mark Scheme (Results) January 2020: Pearson Edexcel International GCSE in Accounting 4AC1 Paper 02 Financial StatementsDocument6 pagesMark Scheme (Results) January 2020: Pearson Edexcel International GCSE in Accounting 4AC1 Paper 02 Financial Statementssci fi100% (1)

- Quiz 1: Introduction To Accounting and BookkeepingDocument37 pagesQuiz 1: Introduction To Accounting and BookkeepingDiana Rose BassigNo ratings yet

- Duff CoDocument1 pageDuff CoAli HussainNo ratings yet

- Assignment On: Managerial Economics Mid Term and AssignmentDocument14 pagesAssignment On: Managerial Economics Mid Term and AssignmentFaraz Khoso BalochNo ratings yet

- Key Metrics: March 9, 2018Document31 pagesKey Metrics: March 9, 2018RenadNo ratings yet

- 250,000 300,000 400,000 500,000 Cash Flow: Year 1 2 3 4Document9 pages250,000 300,000 400,000 500,000 Cash Flow: Year 1 2 3 4Kai ZhaoNo ratings yet

- Income TaxDocument14 pagesIncome Taxanjuu2806No ratings yet

- Tata Steel FinancialsDocument8 pagesTata Steel FinancialsManan GuptaNo ratings yet

- Lesson 6 Activity On Business Transactions and Their AnalysisDocument3 pagesLesson 6 Activity On Business Transactions and Their AnalysisBerto ZerimarNo ratings yet

- INVESTAGRAMSDocument26 pagesINVESTAGRAMScathbarragaNo ratings yet

- Mergers and Acquisitions (A Case Study On PVR and Cinemax) : Submitted byDocument40 pagesMergers and Acquisitions (A Case Study On PVR and Cinemax) : Submitted byVANSHIKA SHROFFNo ratings yet

- Audit of Shareholders Equity RecordsDocument6 pagesAudit of Shareholders Equity Recordsaira nialaNo ratings yet

- GMO Quality-FundDocument2 pagesGMO Quality-Fundb1OSphereNo ratings yet

- Financial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreDocument18 pagesFinancial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreAnirban Roy ChowdhuryNo ratings yet

- EC1B1 - Intro TaxationDocument38 pagesEC1B1 - Intro TaxationZen Marcus RodasNo ratings yet

- New Method of National Income Accounting: Courses Offered: Rbi Grade B Sebi NabardDocument6 pagesNew Method of National Income Accounting: Courses Offered: Rbi Grade B Sebi NabardSai harshaNo ratings yet

- Trắc nghiệmDocument8 pagesTrắc nghiệmHồ Đan Thục0% (1)

- Ifrs 02Document205 pagesIfrs 02Ehsan GaditNo ratings yet

- 22087-047 Hoermann Geschaeftsbericht 2019 EN Web Sec 2 PDFDocument53 pages22087-047 Hoermann Geschaeftsbericht 2019 EN Web Sec 2 PDFPARAS JATANANo ratings yet

- CustomerDocument2 pagesCustomerElliot RichardNo ratings yet