You might also like

- Personality Type Investment IntentionDocument18 pagesPersonality Type Investment Intentionrashid awanNo ratings yet

- Overconfidence and Investment Decisions in Nepalese Stock MarketDocument10 pagesOverconfidence and Investment Decisions in Nepalese Stock MarketMgc RyustailbNo ratings yet

- Individual Investors Herding BehaviorDocument20 pagesIndividual Investors Herding BehaviorHina MasoodNo ratings yet

- How Financial Literacy and Demographic Variables Relate To Behavioral BiasesDocument40 pagesHow Financial Literacy and Demographic Variables Relate To Behavioral BiasesYuri SouzaNo ratings yet

- An Analysis of Behavioral Biases in Investment Decision-MakingDocument13 pagesAn Analysis of Behavioral Biases in Investment Decision-MakingZubaria BashirNo ratings yet

- (Group 7) Risk Aversion and Personality Type PDFDocument12 pages(Group 7) Risk Aversion and Personality Type PDFmeidaNo ratings yet

- Influence of Behavioual Bias On Investment Decisions of Individual Investors in Delhi NCRDocument11 pagesInfluence of Behavioual Bias On Investment Decisions of Individual Investors in Delhi NCRDS ReishenNo ratings yet

- Behavioral Biases Influenced by Demographics and Personality TraitsDocument17 pagesBehavioral Biases Influenced by Demographics and Personality TraitsRenuka SharmaNo ratings yet

- B FinanceDocument14 pagesB Financehinabatool777_651379No ratings yet

- Proposal MehmodDocument4 pagesProposal MehmodManzoor KhanNo ratings yet

- The Impact of Behavioural Factors on Investment DecisionsDocument4 pagesThe Impact of Behavioural Factors on Investment DecisionsAbdul LathifNo ratings yet

- Influence of Investor and Advisor Big Five Personality Congruence On Futures Trading BehaviorDocument17 pagesInfluence of Investor and Advisor Big Five Personality Congruence On Futures Trading Behaviorsonia969696No ratings yet

- Imran ResearchDocument20 pagesImran Researchwaheed mohmandNo ratings yet

- Intro N Literature Review FinalDocument23 pagesIntro N Literature Review FinalHasnain SialNo ratings yet

- An Empirical Research On Investor Biases in Financial Decision-Making, Financial Risk Tolerance and Financial PersonalityDocument12 pagesAn Empirical Research On Investor Biases in Financial Decision-Making, Financial Risk Tolerance and Financial PersonalityrajaniNo ratings yet

- The Financial Behavior of Major Players: Part TwoDocument21 pagesThe Financial Behavior of Major Players: Part TwoEvhil's Lucia Kaito-Kid 洋一No ratings yet

- BF Kerala Q 7Document21 pagesBF Kerala Q 7SarikaNo ratings yet

- (2019) Gambetti & Giusberti - Personality, Decision-Making Styles and InvestmentsDocument11 pages(2019) Gambetti & Giusberti - Personality, Decision-Making Styles and InvestmentsGabriela De Abreu PassosNo ratings yet

- My PaperDocument10 pagesMy PaperAtique Arif KhanNo ratings yet

- Research ProjectDocument14 pagesResearch ProjectAsad KaziNo ratings yet

- Factors Influencing Individual Investor BehaviourDocument13 pagesFactors Influencing Individual Investor BehavioursheetalNo ratings yet

- Report On Behavioral FinanceDocument22 pagesReport On Behavioral Financemuhammad shahid ullahNo ratings yet

- MPRA Paper 53849Document8 pagesMPRA Paper 53849Vipul GhoghariNo ratings yet

- Factors Affecting Investment Behaviour Among Young ProfessionalsDocument6 pagesFactors Affecting Investment Behaviour Among Young ProfessionalsInternational Jpurnal Of Technical Research And ApplicationsNo ratings yet

- Review of Literature on Investor Behavior and Factors Influencing Investment DecisionsDocument8 pagesReview of Literature on Investor Behavior and Factors Influencing Investment Decisionsammukhan khanNo ratings yet

- International Institution For Special Education Lucknow: CaseletDocument9 pagesInternational Institution For Special Education Lucknow: Caseletsaurabh dixitNo ratings yet

- Science 8Document19 pagesScience 8Sasha ApartsinNo ratings yet

- Personality Type and Investment ManagementDocument14 pagesPersonality Type and Investment ManagementMohammad Ali DhamrahNo ratings yet

- GVcef CunhaDocument25 pagesGVcef Cunhaabdullahzahoor987No ratings yet

- Samsuri 2019 E RDocument15 pagesSamsuri 2019 E RlaluaNo ratings yet

- ISSN: 1804-0527 (Online) 1804-0519 (Print) : Study On Relevance of Demographic Factors in Investment DecisionsDocument14 pagesISSN: 1804-0527 (Online) 1804-0519 (Print) : Study On Relevance of Demographic Factors in Investment DecisionsRohini VNo ratings yet

- Role of Psychological Factors in Individuals Investment Decisions (#352310) - 363199Document9 pagesRole of Psychological Factors in Individuals Investment Decisions (#352310) - 363199ADINo ratings yet

- IJMRES 7 Paper Vol 8 No1 2018Document8 pagesIJMRES 7 Paper Vol 8 No1 2018International Journal of Management Research and Emerging SciencesNo ratings yet

- Hayat 2016 Invesment DecisionDocument14 pagesHayat 2016 Invesment DecisionNyoman RiyoNo ratings yet

- The Factors That Affects The Investment Behavior (PPT c1)Document24 pagesThe Factors That Affects The Investment Behavior (PPT c1)Jiezle JavierNo ratings yet

- Does Investors' Personality Influence Their Portfolios?: Alessandro Bucciol and Luca ZarriDocument38 pagesDoes Investors' Personality Influence Their Portfolios?: Alessandro Bucciol and Luca ZarriAmir HayatNo ratings yet

- Assistant Professor, Maharaja Prithvi Engineering College, Tiruchirappalli, Tamilnadu, IndiaDocument33 pagesAssistant Professor, Maharaja Prithvi Engineering College, Tiruchirappalli, Tamilnadu, IndiaAbdul LathifNo ratings yet

- Exploring Behavioural Biases among Indian InvestorsDocument12 pagesExploring Behavioural Biases among Indian Investorsmoinahmed99No ratings yet

- Influence of Personality Traits On Herding Bias of Individual Investors in Indian Capital MarketDocument11 pagesInfluence of Personality Traits On Herding Bias of Individual Investors in Indian Capital Marketarcherselevators100% (2)

- BF Dima Q 4Document16 pagesBF Dima Q 4SarikaNo ratings yet

- Study of Behavioural Finance With Reference To Investor BehaviourDocument5 pagesStudy of Behavioural Finance With Reference To Investor BehaviourInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Behavioral Biases and Financial Decision MakingDocument68 pagesBehavioral Biases and Financial Decision MakingBikashRanaNo ratings yet

- Superstition and Financial Decision MakingDocument44 pagesSuperstition and Financial Decision Makingaditya kumar pandeyNo ratings yet

- Financial literacy paperDocument33 pagesFinancial literacy papersufaid aliNo ratings yet

- Personality TraitsDocument10 pagesPersonality TraitskringNo ratings yet

- I JB Mer 2010010103Document12 pagesI JB Mer 2010010103sanskritiNo ratings yet

- Eview of Life Style SegmentationDocument4 pagesEview of Life Style SegmentationQuan FuNo ratings yet

- Investor Sentiments and Stock Returns: A Study On Noise TradersDocument12 pagesInvestor Sentiments and Stock Returns: A Study On Noise TradersImran KhanNo ratings yet

- Review PaperDocument6 pagesReview PaperNeha Rajora 4701No ratings yet

- Behavioral Finance: Investors Psychology Nuel Chinedu Ani Çiğdem ÖzarıDocument11 pagesBehavioral Finance: Investors Psychology Nuel Chinedu Ani Çiğdem ÖzarıOptimAds DigMarkNo ratings yet

- 05-Aug-2021 EmpiricalBehavioralFinance PDF 24Document14 pages05-Aug-2021 EmpiricalBehavioralFinance PDF 24Barani Kumar NNo ratings yet

- The Impact of Behavioral Finance On Stock Markets PDFDocument11 pagesThe Impact of Behavioral Finance On Stock Markets PDFprema100% (1)

- Paper-1 Published IJTRD3877Document6 pagesPaper-1 Published IJTRD3877Vineet ChouhanNo ratings yet

- Chapter 1Document15 pagesChapter 1Saurav KumarNo ratings yet

- Effect of Loss Aversion Bias On Investment Decision: A StudyDocument6 pagesEffect of Loss Aversion Bias On Investment Decision: A Studyarun kumarNo ratings yet

- (Draft) Lit ReviewDocument16 pages(Draft) Lit ReviewHoang OanhNo ratings yet

- Factors Influencing Indian Individual in PDFDocument41 pagesFactors Influencing Indian Individual in PDFTarique HusenNo ratings yet

- Sahi2017 PDFDocument25 pagesSahi2017 PDFshaharyarkhanNo ratings yet

- 1684-Article Text-6733-1-10-20220416Document12 pages1684-Article Text-6733-1-10-20220416Salman KhanNo ratings yet

- T and PDocument10 pagesT and PashNo ratings yet

- Legal Rules As To AcceptanceDocument21 pagesLegal Rules As To AcceptanceashNo ratings yet

- Managing StoresDocument57 pagesManaging StoresashNo ratings yet

- Bailment: A Delivers His Car To B, For Repair. Y Lends Her Cycle To B To Be Returned After A WeekDocument16 pagesBailment: A Delivers His Car To B, For Repair. Y Lends Her Cycle To B To Be Returned After A WeekashNo ratings yet

- Lab 1Document20 pagesLab 1ashNo ratings yet

- Marketing Research Brief Note On Unit IiDocument13 pagesMarketing Research Brief Note On Unit IiashNo ratings yet

- Transportation Method of Linear ProgrammingDocument7 pagesTransportation Method of Linear ProgrammingashNo ratings yet

- 5.1 Org & Controlling Marketing FunctionsDocument8 pages5.1 Org & Controlling Marketing FunctionsashNo ratings yet

- HypothesisDocument5 pagesHypothesisashNo ratings yet

- Group 18 - ProjectDocument14 pagesGroup 18 - ProjectashNo ratings yet

- Equifax Analytics Launches InterconnectDocument5 pagesEquifax Analytics Launches InterconnectashNo ratings yet

- Aravind Eye Care SystemDocument5 pagesAravind Eye Care SystemashNo ratings yet

- Satisfaction With Healthcare Access Lacking in Spain, ItalyDocument4 pagesSatisfaction With Healthcare Access Lacking in Spain, ItalyashNo ratings yet

- Baskin-Robbins Study Customer Logo ChangeDocument1 pageBaskin-Robbins Study Customer Logo Changeash0% (1)

- VisionDocument1 pageVisionashNo ratings yet

- Information Strategy ManagementDocument2 pagesInformation Strategy ManagementashNo ratings yet

- MalaDocument1 pageMalaashNo ratings yet

- This Is Used To Download MisDocument1 pageThis Is Used To Download MisashNo ratings yet

- Institute of Management Studies and Research: KLE Society'sDocument22 pagesInstitute of Management Studies and Research: KLE Society'sRutuja HukkeriNo ratings yet

- Challenges For Implementing Renewable Energy in A Cooperative Driven Off-Grid System in The Philippines Bertheau Et AlDocument24 pagesChallenges For Implementing Renewable Energy in A Cooperative Driven Off-Grid System in The Philippines Bertheau Et AlDiana Rose B. DatinguinooNo ratings yet

- CRT 3rd Year NewDocument232 pagesCRT 3rd Year NewAkshat agrawalNo ratings yet

- CV Example (Dubal Avinash)Document3 pagesCV Example (Dubal Avinash)Rajkumar KhaseraoNo ratings yet

- INTERVIEW GUIDE For BMADocument6 pagesINTERVIEW GUIDE For BMAJale Ann A. EspañolNo ratings yet

- Grameen BankDocument28 pagesGrameen Bankalpha34567No ratings yet

- MSc Sales & Marketing Statement of PurposeDocument1 pageMSc Sales & Marketing Statement of PurposeDaud LawrenceNo ratings yet

- Homework 2Document3 pagesHomework 2Tú QuyênNo ratings yet

- Nepal Health Service Act 2053 BSDocument72 pagesNepal Health Service Act 2053 BSDinesh YadavNo ratings yet

- Barangay transparency monitoring form titleDocument1 pageBarangay transparency monitoring form titleOmar Dizon100% (1)

- Stupid Data Miner Tricks Overfitting The SP 500Document12 pagesStupid Data Miner Tricks Overfitting The SP 500hpschreiNo ratings yet

- Macroeconomics Encapsulated in Three Models (Recovered)Document33 pagesMacroeconomics Encapsulated in Three Models (Recovered)Katherine Asis NatinoNo ratings yet

- Meridian, B. (2000) - Lunar Cycle & Stock Market (13 P.)Document13 pagesMeridian, B. (2000) - Lunar Cycle & Stock Market (13 P.)Alexa CosimaNo ratings yet

- ES 301 Assignment #1 engineering economy problems and solutionsDocument2 pagesES 301 Assignment #1 engineering economy problems and solutionsErika Rez LapatisNo ratings yet

- Durado RRLDocument3 pagesDurado RRLJohneen DungqueNo ratings yet

- Responsibility AccountingDocument4 pagesResponsibility AccountingEllise FreniereNo ratings yet

- Differences between startups and spinoffsDocument4 pagesDifferences between startups and spinoffsRafael CavalcanteNo ratings yet

- GST101Document1 pageGST101ANKIT KUMAR IPM 2018 BatchNo ratings yet

- Rajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Document1 pageRajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Bhavy Kumar JainNo ratings yet

- Types of POS SystemsDocument3 pagesTypes of POS SystemsCabdulahi CumarNo ratings yet

- Interbrand Breakthrough Brands 2020 ReportDocument44 pagesInterbrand Breakthrough Brands 2020 ReportThu Hà NguyễnNo ratings yet

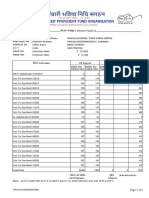

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Deposits in Transit and Outstanding Checks PDFDocument1 pageDeposits in Transit and Outstanding Checks PDFAaliyah Joize LegaspiNo ratings yet

- Export Oriented UnitsDocument10 pagesExport Oriented UnitsMansi GuptaNo ratings yet

- Quotation - Householders - LAPSONDocument1 pageQuotation - Householders - LAPSONCredsureNo ratings yet

- Befa Question BankDocument9 pagesBefa Question Bank20bd1a6655No ratings yet

- The Prevention of Corruption Act, 1988: A Critical StudyDocument33 pagesThe Prevention of Corruption Act, 1988: A Critical StudyRAJARAJESHWARI M GNo ratings yet

- DHL DissertationDocument8 pagesDHL DissertationJahangir AliNo ratings yet

- Zain Ufone Best 1 Strategic Management ProjectDocument50 pagesZain Ufone Best 1 Strategic Management Projectzain_lion2009372280% (10)

- Tata Tea - FADocument27 pagesTata Tea - FASagar BsNo ratings yet