You might also like

- Cir Vs Estate of Benigno TodaDocument2 pagesCir Vs Estate of Benigno TodaHarvey Leo RomanoNo ratings yet

- CIR v. Estate of TodaDocument2 pagesCIR v. Estate of TodaJayzell Mae FloresNo ratings yet

- CIR vs. ESTATE OF BENIGNO TODADocument2 pagesCIR vs. ESTATE OF BENIGNO TODAAngela Mericci G. Mejia100% (1)

- Cases To Be Digest TAX 2 ATTY LIM No. 1 - 17 OnlyDocument131 pagesCases To Be Digest TAX 2 ATTY LIM No. 1 - 17 OnlyAngelo FulgencioNo ratings yet

- Tax1 Assigned CasesDocument5 pagesTax1 Assigned CasesflorencemanulatNo ratings yet

- 5 Case Digest Cir Vs Estate of TodaDocument2 pages5 Case Digest Cir Vs Estate of TodaChrissy Sabella0% (1)

- CIR vs Estate Tax Evasion CaseDocument2 pagesCIR vs Estate Tax Evasion CaseJf Maneja100% (2)

- Part G 2F - CIR vs. Estate of Benigno Toda JRDocument2 pagesPart G 2F - CIR vs. Estate of Benigno Toda JRCyruz TuppalNo ratings yet

- Tax Evasion Scheme ReversedDocument21 pagesTax Evasion Scheme ReversedYale Brendan CatabayNo ratings yet

- CIR vs. Estate of Benigno Toda, JR., SCRA 438 SCRA 291 (2004)Document3 pagesCIR vs. Estate of Benigno Toda, JR., SCRA 438 SCRA 291 (2004)I took her to my penthouse and i freaked itNo ratings yet

- Cir VS Estate of TodaDocument3 pagesCir VS Estate of TodaGraziella AndayaNo ratings yet

- CIR vs Estate of Toda: Tax Evasion, Prescription Period, Personal LiabilityDocument2 pagesCIR vs Estate of Toda: Tax Evasion, Prescription Period, Personal LiabilityBrent Christian Taeza TorresNo ratings yet

- TAX RULES ON MERGERS AND ACQUISITIONSDocument29 pagesTAX RULES ON MERGERS AND ACQUISITIONSEarl TagraNo ratings yet

- Doctrine:: Commissioner of Internal Revenue vs. The Estate of Benigno TodaDocument2 pagesDoctrine:: Commissioner of Internal Revenue vs. The Estate of Benigno TodaElla CanuelNo ratings yet

- CIR Vs The Estate of TodaDocument3 pagesCIR Vs The Estate of TodaLDNo ratings yet

- CIR, vs. THE ESTATE OF BENIGNO P. TODA, JR., G.R. No. 147188. September 14, 2004 FactsDocument1 pageCIR, vs. THE ESTATE OF BENIGNO P. TODA, JR., G.R. No. 147188. September 14, 2004 Factsian ballartaNo ratings yet

- CIR vs. THE ESTATE OF BENIGNO P. TODA, JR.Document9 pagesCIR vs. THE ESTATE OF BENIGNO P. TODA, JR.Rhett Vincent De La rosaNo ratings yet

- CIR v. TodaDocument8 pagesCIR v. TodaLovely ZyrenjcNo ratings yet

- CIR v. Estate of Benigno Toda, 438 SCRA 290, 2004Document8 pagesCIR v. Estate of Benigno Toda, 438 SCRA 290, 2004JMae MagatNo ratings yet

- CIR Vs Benigno TodaDocument10 pagesCIR Vs Benigno TodaAlvin CabreraNo ratings yet

- G.R. No. 147188 September 14, 2004 Commissioner of Internal Revenue Vs - The Estate of Benigno P. Toda, JR.Document2 pagesG.R. No. 147188 September 14, 2004 Commissioner of Internal Revenue Vs - The Estate of Benigno P. Toda, JR.micheleNo ratings yet

- Tax Evasion Scheme Uncovered in Simulated Property SaleDocument3 pagesTax Evasion Scheme Uncovered in Simulated Property SaleMichael TampengcoNo ratings yet

- Chamber Challenges Minimum Corporate Income Tax, Withholding Tax RulesDocument13 pagesChamber Challenges Minimum Corporate Income Tax, Withholding Tax RulesAngelie Fei CuirNo ratings yet

- Estate of Benigno Toda JRDocument2 pagesEstate of Benigno Toda JRMary AnneNo ratings yet

- Tax Cases Nos 1-5Document68 pagesTax Cases Nos 1-5Dimple VillaminNo ratings yet

- Recit Digest 1Document9 pagesRecit Digest 1Vincent NifasNo ratings yet

- CIR v. Estate of Benigno Toda JR DIGESTDocument2 pagesCIR v. Estate of Benigno Toda JR DIGESTPia SottoNo ratings yet

- Cir Vs Estate of TodaDocument3 pagesCir Vs Estate of TodaPia SottoNo ratings yet

- Purple Wings Tax DigestsDocument36 pagesPurple Wings Tax DigestsJf LarongNo ratings yet

- CIR V Estate of Benigno Toda JRDocument9 pagesCIR V Estate of Benigno Toda JRParis LisonNo ratings yet

- Tax Digest CompilationDocument37 pagesTax Digest CompilationVerine SagunNo ratings yet

- Republic of The Philippines Manila: CIR v. Estate of Toda G.R. No. 147188Document8 pagesRepublic of The Philippines Manila: CIR v. Estate of Toda G.R. No. 147188Jopan SJNo ratings yet

- Tax Avoidance Vs Tax EvasionDocument3 pagesTax Avoidance Vs Tax EvasionJames Ryan AlzonaNo ratings yet

- G.R. No. 147188: Tax Digest: CIR V. Estate of Benigno Toda Jr. (2004)Document2 pagesG.R. No. 147188: Tax Digest: CIR V. Estate of Benigno Toda Jr. (2004)BrenPeñarandaNo ratings yet

- Tax Evasion-Cir v. TodaDocument4 pagesTax Evasion-Cir v. TodaPax YabutNo ratings yet

- CIR v. Estate of Benigno Toda - G.R. No. 147188Document9 pagesCIR v. Estate of Benigno Toda - G.R. No. 147188Ash SatoshiNo ratings yet

- VAT 5 - CIR vs. Commonwealth MGTDocument1 pageVAT 5 - CIR vs. Commonwealth MGTFrances CruzNo ratings yet

- CIR v. The Estate of Benigno P. TodaDocument2 pagesCIR v. The Estate of Benigno P. TodaKyle DionisioNo ratings yet

- Taxation Cases 2Document16 pagesTaxation Cases 2Joji Marie PalecNo ratings yet

- Commissioner of Internal Revenue v. Toda, Jr.Document1 pageCommissioner of Internal Revenue v. Toda, Jr.Mica ArceNo ratings yet

- Tax CasesDocument8 pagesTax CasesLaUnion ProvincialHeadquarters Bfp RegionOneNo ratings yet

- Digested Cases in Taxation I, Part 1Document35 pagesDigested Cases in Taxation I, Part 1lonitsuaf89% (9)

- 099 - Chamber of Real Estate and Builders Associations Inc v. Romulo DigestDocument6 pages099 - Chamber of Real Estate and Builders Associations Inc v. Romulo DigestCharvan CharengNo ratings yet

- 06 CIR vs. Estate of TodDocument9 pages06 CIR vs. Estate of Todada mae santoniaNo ratings yet

- MSCJ Tax Evasion CaseDocument10 pagesMSCJ Tax Evasion Casejovelyn.nicolasNo ratings yet

- CIR v. Estate of Toda, JR., G.R. No. 147188, September 14, 2004Document2 pagesCIR v. Estate of Toda, JR., G.R. No. 147188, September 14, 2004John Cyrus DangananNo ratings yet

- Tax Review Cases SummaryDocument20 pagesTax Review Cases SummaryNeri DelfinNo ratings yet

- CIR V Benigno TodaDocument2 pagesCIR V Benigno TodaAl PaglinawanNo ratings yet

- CIR V Benguet Corporation DIGESTDocument3 pagesCIR V Benguet Corporation DIGESTGretchen MondragonNo ratings yet

- Magsaysay Lines VS. CIR Tax RulingDocument13 pagesMagsaysay Lines VS. CIR Tax RulingVictor LimNo ratings yet

- CIR Vs Estate of TodaDocument1 pageCIR Vs Estate of Todaerica pejiNo ratings yet

- CIR v. Benigno TodaDocument1 pageCIR v. Benigno TodaChou TakahiroNo ratings yet

- Taxation Q&ADocument18 pagesTaxation Q&AZsazsaNo ratings yet

- Taxation Case Law SummaryDocument94 pagesTaxation Case Law SummaryMichael jay sarmientoNo ratings yet

- Nature, Construction, Application, and Sources of Tax Laws ExplainedDocument23 pagesNature, Construction, Application, and Sources of Tax Laws ExplainedIam YengNo ratings yet

- CIR Vs Commonwealth ManagementDocument3 pagesCIR Vs Commonwealth ManagementGoody100% (1)

- CIR Vs CA GR 125355Document6 pagesCIR Vs CA GR 125355Melo Ponce de LeonNo ratings yet

- Facts:: 1 CIR vs. Seagate Technology (Philippines) G.R. NO. 153866, February 11, 2005Document5 pagesFacts:: 1 CIR vs. Seagate Technology (Philippines) G.R. NO. 153866, February 11, 2005JV PagunuranNo ratings yet

- CIR vs Aichi Forging- Tax Refund DeadlineDocument13 pagesCIR vs Aichi Forging- Tax Refund DeadlineSherleen Anne Agtina DamianNo ratings yet

- Gomez Vs PalomarDocument2 pagesGomez Vs PalomarKent Ugalde50% (2)

- Francia vs. Intermediate Appellate Court (G.R. No. 67649, June 28,1988)Document1 pageFrancia vs. Intermediate Appellate Court (G.R. No. 67649, June 28,1988)Kent UgaldeNo ratings yet

- PKMMSN vs. Executive Secretary: Coco-levy funds are public fundsDocument3 pagesPKMMSN vs. Executive Secretary: Coco-levy funds are public fundsKent UgaldeNo ratings yet

- Gerochi, Et Al. vs. Department of Energy, Et Al.Document2 pagesGerochi, Et Al. vs. Department of Energy, Et Al.Kent UgaldeNo ratings yet

- Drugstores Association of The Philippines, Inc., Et Al. vs. National Council On Disability Affairs, Et AlDocument2 pagesDrugstores Association of The Philippines, Inc., Et Al. vs. National Council On Disability Affairs, Et Alanne labuyo100% (1)

- Domingo vs. Garlitos (8 SCRA 443, G.R. No. L-18994, June 29, 1963)Document2 pagesDomingo vs. Garlitos (8 SCRA 443, G.R. No. L-18994, June 29, 1963)Kent UgaldeNo ratings yet

- Rdo 042 Sanjuan - Do7696Document1 pageRdo 042 Sanjuan - Do7696Kent UgaldeNo ratings yet

- CIR Vs Filinvest Development CorporationDocument2 pagesCIR Vs Filinvest Development CorporationKent UgaldeNo ratings yet

- Diaz vs. Secretary of Finance (G.R. No. 193007, July 19, 2011)Document2 pagesDiaz vs. Secretary of Finance (G.R. No. 193007, July 19, 2011)Kent UgaldeNo ratings yet

- Zoleta Vs SandiganbayanDocument4 pagesZoleta Vs SandiganbayanKent Ugalde100% (3)

- ACAB Vs CADocument2 pagesACAB Vs CAKent UgaldeNo ratings yet

- Unauthorized Military Interventions Plea of NecessityDocument5 pagesUnauthorized Military Interventions Plea of NecessityKent UgaldeNo ratings yet

- DFA Vs NLRCDocument2 pagesDFA Vs NLRCKent UgaldeNo ratings yet

- Zoleta Vs SandiganbayanDocument4 pagesZoleta Vs SandiganbayanKent Ugalde100% (3)

- Citizen Surety CaseDocument2 pagesCitizen Surety CaseKent UgaldeNo ratings yet

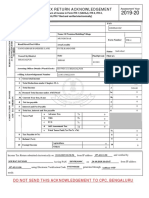

- Indian Income Tax Return Acknowledgement for AY 2019-20Document1 pageIndian Income Tax Return Acknowledgement for AY 2019-20Sourav KumarNo ratings yet

- Rizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)Document2 pagesRizwan & Co. Chartered Accountants: Completed by Schedule Reviewed by (SPS/AM) Reviewed by (Partner)faheemNo ratings yet

- EFD - Receipt Verification2Document1 pageEFD - Receipt Verification2Ramadhani YahayaNo ratings yet

- Getcre8Ive: CorporationDocument1 pageGetcre8Ive: CorporationBeverly VelascoNo ratings yet

- Income Tax Calculator - TaxScoutsDocument1 pageIncome Tax Calculator - TaxScoutsnadine.massabkiNo ratings yet

- Analyze financial trends with horizontal analysisDocument5 pagesAnalyze financial trends with horizontal analysissexy samuelNo ratings yet

- Taxation Law 1 Taxation Law 1 Atty. Vicente V. Cañoneo Atty. Vicente V. CañoneoDocument3 pagesTaxation Law 1 Taxation Law 1 Atty. Vicente V. Cañoneo Atty. Vicente V. CañoneoHannah Beatriz Cabral0% (1)

- Income Tax Officers Rank HierarchyDocument7 pagesIncome Tax Officers Rank Hierarchyganesh bhaiNo ratings yet

- Student Activity Packet SC-1.2Document3 pagesStudent Activity Packet SC-1.2Kenneth ReedNo ratings yet

- Pocket Films RevenueDocument1 pagePocket Films RevenueAkshay HamandNo ratings yet

- W 8Document4 pagesW 8Gary S. Wolfe80% (5)

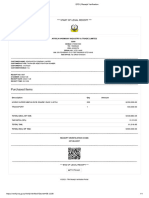

- Tax Invoice SummaryDocument1 pageTax Invoice SummaryJignesh UpadhyayNo ratings yet

- ReceiptDocument1 pageReceiptmmshaikh5791No ratings yet

- Policy receipt for life insurance premium paymentDocument1 pagePolicy receipt for life insurance premium paymentMotilal HembramNo ratings yet

- Assignment 4.2 VAT and non-VAT Registered Taxpayers Comparative Business Tax DueDocument3 pagesAssignment 4.2 VAT and non-VAT Registered Taxpayers Comparative Business Tax DueTriciaMarieArguellesNo ratings yet

- 1575 Tania Sultana (Taxation I)Document28 pages1575 Tania Sultana (Taxation I)Tania SultanaNo ratings yet

- New W4Document1 pageNew W4Roberto MonterrosaNo ratings yet

- Rutendo KamukonoDocument3 pagesRutendo KamukonoHazel ChatsNo ratings yet

- Profit & Loss (Standard) : Resa Harisma 195154024Document1 pageProfit & Loss (Standard) : Resa Harisma 195154024Bikin OrtubanggaNo ratings yet

- Tax DefinitionDocument2 pagesTax DefinitionZainab Aftab 5221-FMS/BBA/S18No ratings yet

- Aicte Arrears G.O. (MS) 575 2013 H.ednDocument1 pageAicte Arrears G.O. (MS) 575 2013 H.ednu19n6735No ratings yet

- CompleteDocument2 pagesCompleteappledeja7829No ratings yet

- Senior Citizen Tax FormDocument3 pagesSenior Citizen Tax FormRajanNo ratings yet

- 2011 Pub 4491WDocument208 pages2011 Pub 4491WRefundOhioNo ratings yet

- PayslipDocument1 pagePayslipMaureen D. FloresNo ratings yet

- Year Long Bill 23Document3 pagesYear Long Bill 23Kewal GuglaniNo ratings yet

- Hdfcergo 9920 Jan 2022 Payslip 9920Document1 pageHdfcergo 9920 Jan 2022 Payslip 9920Pramila DeviNo ratings yet

- CBIC issues notifications providing COVID-19 relief for GST filingsDocument3 pagesCBIC issues notifications providing COVID-19 relief for GST filingssunshineNo ratings yet

- 30 Apr 2021Document1 page30 Apr 2021Madhuri MadhuNo ratings yet

- Tax InvoiceDocument3 pagesTax InvoiceMansi JaiswalNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASFrom EverandIFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASRating: 3 out of 5 stars3/5 (5)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementFrom EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementRating: 4.5 out of 5 stars4.5/5 (20)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessFrom EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNo ratings yet

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- What Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemFrom EverandWhat Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemNo ratings yet

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseFrom EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNo ratings yet

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersFrom EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo ratings yet