You might also like

- The Consummate Fitness Professional: A Guide to Starting & Growing Your Personal Training BusinessFrom EverandThe Consummate Fitness Professional: A Guide to Starting & Growing Your Personal Training BusinessNo ratings yet

- Practice Case 2 - Private Fitness LLCDocument2 pagesPractice Case 2 - Private Fitness LLCannisashriNo ratings yet

- Case Study Private Fitness IncDocument2 pagesCase Study Private Fitness IncKris Miralles100% (2)

- 01.3 Private Fitness, Inc.Document2 pages01.3 Private Fitness, Inc.JeevesNo ratings yet

- CASE STUDY - Private Fitness Inc.Document3 pagesCASE STUDY - Private Fitness Inc.RAFANOMEZANTSOANo ratings yet

- Case Study Private Fitness, Inc (S1)Document8 pagesCase Study Private Fitness, Inc (S1)Faishal Alghi FariNo ratings yet

- The Fitness Profits Road Map Chris McCombsDocument74 pagesThe Fitness Profits Road Map Chris McCombsBen WatNo ratings yet

- 15 1Document3 pages15 1Industry ReportNo ratings yet

- Career Exploration Part 4Document4 pagesCareer Exploration Part 4api-569796169No ratings yet

- From Zero To 205 Clients Case StudyDocument29 pagesFrom Zero To 205 Clients Case StudyNicolae MihaliNo ratings yet

- Spirituality in Business: Pricing Your ServicesDocument20 pagesSpirituality in Business: Pricing Your ServicesMark Silver - Heart of BusinessNo ratings yet

- E-Book - How To Find Clients For Your Personal Training BusinessDocument5 pagesE-Book - How To Find Clients For Your Personal Training BusinessRoberto GuanipaNo ratings yet

- Ent241 - Ei Report - Grace HakimDocument5 pagesEnt241 - Ei Report - Grace Hakimapi-631688854No ratings yet

- Literature Review WorksheetDocument3 pagesLiterature Review WorksheetLori HillNo ratings yet

- Choosing An OrgDocument3 pagesChoosing An OrgAlyssa AzevedoNo ratings yet

- PSP Application Short AnswersDocument2 pagesPSP Application Short AnswersSabrinaNo ratings yet

- Online Training Ebook For MF1OT Course PDFDocument46 pagesOnline Training Ebook For MF1OT Course PDFBlaz Jurecic100% (2)

- How We Broke Through The Five Roadblocks To Earning $100K As A Fitness ProDocument10 pagesHow We Broke Through The Five Roadblocks To Earning $100K As A Fitness ProtobyNo ratings yet

- Eos Fitness ManualDocument75 pagesEos Fitness ManualVăn Thế NamNo ratings yet

- Documento de Coach Sergio Cruzado 5Document32 pagesDocumento de Coach Sergio Cruzado 5Sergio CruzadoNo ratings yet

- Documento de Coach Sergio Cruzado 6Document35 pagesDocumento de Coach Sergio Cruzado 6Sergio CruzadoNo ratings yet

- 11 Business Mistakes To AvoidDocument14 pages11 Business Mistakes To Avoidmyotherone100% (1)

- COMPONENTS-OF-CASE-STUDYDocument3 pagesCOMPONENTS-OF-CASE-STUDYLy RieNo ratings yet

- Unlimited FreelancerDocument200 pagesUnlimited FreelancerBánh BaoNo ratings yet

- Two Brain Business Retention Guide 2022 UpdateDocument31 pagesTwo Brain Business Retention Guide 2022 UpdateAhmed KandilNo ratings yet

- The Business of Personal TrainingDocument12 pagesThe Business of Personal TrainingJohnNo ratings yet

- Freedom From Self-Employment Traps: A Blueprint for Small Business OwnersFrom EverandFreedom From Self-Employment Traps: A Blueprint for Small Business OwnersRating: 2 out of 5 stars2/5 (1)

- The Unlimited FreelancerDocument200 pagesThe Unlimited FreelancerBrandon WhiteNo ratings yet

- The Everything Guide To Being A Personal Trainer: All You Need to Get Started on a Career in FitnessFrom EverandThe Everything Guide To Being A Personal Trainer: All You Need to Get Started on a Career in FitnessRating: 4.5 out of 5 stars4.5/5 (5)

- 24 Hour Fitness Organizational AnalysisDocument18 pages24 Hour Fitness Organizational Analysisapi-308319164No ratings yet

- Dynamic Business Duos: Succeed Like a Superhero in Your Own Business With a Pow!er PartnerFrom EverandDynamic Business Duos: Succeed Like a Superhero in Your Own Business With a Pow!er PartnerNo ratings yet

- The Seven Stages of Practice BuildingDocument8 pagesThe Seven Stages of Practice BuildingarchangelsfeatherNo ratings yet

- Chapter Test IDocument11 pagesChapter Test IKath LapuzNo ratings yet

- 线上教练wfpg Ot eBookDocument182 pages线上教练wfpg Ot eBookWantong LaoNo ratings yet

- SUMMARY Of Gym Launch Secrets By Alex Hormozi: The Step-By-Step Guide To Building A Massively Profitable GymFrom EverandSUMMARY Of Gym Launch Secrets By Alex Hormozi: The Step-By-Step Guide To Building A Massively Profitable GymNo ratings yet

- Chapter 1 ObDocument3 pagesChapter 1 ObKeon Screeven100% (1)

- Summary of Gym Launch Secrets by Alex Hormozi: by Alex Hormozi - The Step-By-Step Guide To Building A Massively Profitable Gym - A Comprehensive SummaryFrom EverandSummary of Gym Launch Secrets by Alex Hormozi: by Alex Hormozi - The Step-By-Step Guide To Building A Massively Profitable Gym - A Comprehensive SummaryNo ratings yet

- Career Guidance for Now and for the Future: Rci Program to SuccessFrom EverandCareer Guidance for Now and for the Future: Rci Program to SuccessNo ratings yet

- Myo Frozen Yogurt _ Official HandbookDocument7 pagesMyo Frozen Yogurt _ Official Handbookqweenie ;No ratings yet

- Healthcare Providers: How to Promote Your Practice to a Well-Pay, Self-Pay ClienteleFrom EverandHealthcare Providers: How to Promote Your Practice to a Well-Pay, Self-Pay ClienteleNo ratings yet

- Group 5 Action Reseach ShakeysDocument7 pagesGroup 5 Action Reseach ShakeysLady Lyn LorNo ratings yet

- Top 1 Jim PalmerDocument31 pagesTop 1 Jim PalmerSergio CruzadoNo ratings yet

- American Muscle & Fitness Kick Boxing Aerobics ManualDocument37 pagesAmerican Muscle & Fitness Kick Boxing Aerobics Manualfavoloso1No ratings yet

- Jaclyn Resume New 1Document4 pagesJaclyn Resume New 1api-297244528No ratings yet

- Amagram59 PDFDocument32 pagesAmagram59 PDFJagannath DasNo ratings yet

- Moneh - Kim PalmerDocument26 pagesMoneh - Kim PalmerSergio CruzadoNo ratings yet

- DōTERRA University Building Brochure v2Document8 pagesDōTERRA University Building Brochure v2Maht Rigpa100% (1)

- Evercoach - Evercoach TribeDocument56 pagesEvercoach - Evercoach TribeAtul Kapoor100% (4)

- Secret Service: Hidden Systems That Deliver Unforgettable Customer ServiceFrom EverandSecret Service: Hidden Systems That Deliver Unforgettable Customer ServiceRating: 5 out of 5 stars5/5 (1)

- Module 1: Beginning A Career in The Fitness IndustryDocument11 pagesModule 1: Beginning A Career in The Fitness IndustryMarkus KaltenhauserNo ratings yet

- Virtual Gal Friday's Virtual Assistant Start Up GuideFrom EverandVirtual Gal Friday's Virtual Assistant Start Up GuideRating: 4 out of 5 stars4/5 (2)

- (Onboarding) Start HereDocument3 pages(Onboarding) Start HereStephanny de PaulaNo ratings yet

- MKT 135 Final ProjectDocument13 pagesMKT 135 Final Projectapi-707222924No ratings yet

- Carter Case StudyDocument4 pagesCarter Case StudyHarshu RaoNo ratings yet

- Ethics Assignment 1Document2 pagesEthics Assignment 1Komal mushtaqNo ratings yet

- MemoDocument2 pagesMemoAboubakr SoultanNo ratings yet

- Diamond Rush GuideDocument14 pagesDiamond Rush GuideDacian Florin Dedu100% (1)

- Group PresentationDocument2 pagesGroup PresentationMuhaddisaNo ratings yet

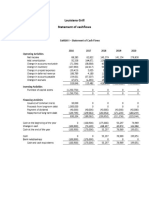

- Lousiana Grill Cashflow StatementDocument1 pageLousiana Grill Cashflow StatementMuhaddisaNo ratings yet

- Weekly Schedule (IAF841) Advanced Management Accounting W2021Document2 pagesWeekly Schedule (IAF841) Advanced Management Accounting W2021MuhaddisaNo ratings yet

- Sensations Athletic ClubDocument2 pagesSensations Athletic ClubMuhaddisaNo ratings yet

- Topic Outline Fall 2020Document1 pageTopic Outline Fall 2020MuhaddisaNo ratings yet

- Yakky Yak Inclass Exercise Handout To PostDocument3 pagesYakky Yak Inclass Exercise Handout To PostMuhaddisaNo ratings yet

- Yakky Yak Governance QuestionDocument2 pagesYakky Yak Governance QuestionMuhaddisaNo ratings yet

- (CPA Sample) MAMMA JILL Pizza QuestionDocument2 pages(CPA Sample) MAMMA JILL Pizza QuestionMuhaddisaNo ratings yet

- Midterm Exam: Male-Female Relationships Course HREQ 1920 ADocument2 pagesMidterm Exam: Male-Female Relationships Course HREQ 1920 AMuhaddisaNo ratings yet

- Case Analysis # 1 Sit-Up Fitness Center Yuchen BaiDocument5 pagesCase Analysis # 1 Sit-Up Fitness Center Yuchen BaiMuhaddisaNo ratings yet

- Weekly Schedule (IAF841) Advanced Management Accounting W2021Document2 pagesWeekly Schedule (IAF841) Advanced Management Accounting W2021MuhaddisaNo ratings yet

- Midterm Exam Concepts for Male/Female Relationships CourseDocument1 pageMidterm Exam Concepts for Male/Female Relationships CourseMuhaddisaNo ratings yet

- Mid Term Exam NotesDocument1 pageMid Term Exam NotesMuhaddisaNo ratings yet

- Flexib Ility T Rainin G: By: Jeric E. Suguis/ Cristine A. CarreonDocument43 pagesFlexib Ility T Rainin G: By: Jeric E. Suguis/ Cristine A. CarreonCrislieNo ratings yet

- 2 Lesson Fitt PrinciplesDocument3 pages2 Lesson Fitt PrinciplesKen CastroNo ratings yet

- Lesson 1 Physical FitnessDocument9 pagesLesson 1 Physical FitnessLIMOS JR. ROMEO P.No ratings yet

- BaXaCD-6 - 3 April - 2 Week Pilates Sculpt Fat Burn Guide - Lilly SabriDocument4 pagesBaXaCD-6 - 3 April - 2 Week Pilates Sculpt Fat Burn Guide - Lilly SabriAndra CosmaNo ratings yet

- Self-Testing for a Healthy MeDocument9 pagesSelf-Testing for a Healthy MejuanNo ratings yet

- Week 3 P.E Grade 8Document14 pagesWeek 3 P.E Grade 8Israel MarquezNo ratings yet

- Arm Workout PDFDocument1 pageArm Workout PDFYenyen Quirog-PalmesNo ratings yet

- Intro To P.EDocument59 pagesIntro To P.EPrincess Liban RumusudNo ratings yet

- Daily School Fitness Activity LessonDocument3 pagesDaily School Fitness Activity LessonJana MarisNo ratings yet

- Personal Safety TipsDocument4 pagesPersonal Safety TipsCharles CabarlesNo ratings yet

- Lower Extremity Exercise Packet 3Document5 pagesLower Extremity Exercise Packet 3api-487110724No ratings yet

- BBR 28 Day Shred 2.0Document26 pagesBBR 28 Day Shred 2.0Zineb El Mellouki100% (2)

- TotalGym ResistanceChart 12levelsDocument1 pageTotalGym ResistanceChart 12levelsJerryNo ratings yet

- A Patient's Guide To Exercise and Stretching - CMT UK PDFDocument12 pagesA Patient's Guide To Exercise and Stretching - CMT UK PDFMajda BajramovićNo ratings yet

- Fitness, Health and Combative Sports ReviewDocument20 pagesFitness, Health and Combative Sports ReviewBENJAMIN III BIDANGNo ratings yet

- Phrasal Verbs About Exercising and SportDocument12 pagesPhrasal Verbs About Exercising and SportAndres AngaritaNo ratings yet

- Direction: Circle The Correct Verb in Each of The Sentences BelowDocument5 pagesDirection: Circle The Correct Verb in Each of The Sentences BelowAEJNo ratings yet

- Lesson Plan in P.E (June 25)Document2 pagesLesson Plan in P.E (June 25)Camelah CadigoyNo ratings yet

- Edit Spreadsheet Strength ProgramDocument2 pagesEdit Spreadsheet Strength ProgramDank StankNo ratings yet

- Hope1 - Module2 - Q1 - V5 - Final VersionDocument10 pagesHope1 - Module2 - Q1 - V5 - Final VersionBlink G.No ratings yet

- Untitled DocumentDocument3 pagesUntitled DocumentRazerNo ratings yet

- Mapeh 7Document5 pagesMapeh 7Czz ThhNo ratings yet

- Mapeh 7 Week 7Document2 pagesMapeh 7 Week 7Edmar MejiaNo ratings yet

- 20 Minute Ab Workout - No Equipment NeededDocument3 pages20 Minute Ab Workout - No Equipment NeededJamesNo ratings yet

- Efc February NewsletterDocument4 pagesEfc February Newsletterapi-453358603No ratings yet

- SYM 1 U07 ReadingWorksheetsDocument6 pagesSYM 1 U07 ReadingWorksheetsSelena ReyesNo ratings yet

- P-E Physical Fitness Test BatteryDocument9 pagesP-E Physical Fitness Test BatteryAl Brelzhiv SarsalejoNo ratings yet

- O41S BW WorkoutDocument37 pagesO41S BW WorkoutPaulo AlmacenNo ratings yet

- Circuit TrainingDocument259 pagesCircuit TrainingLynseyNo ratings yet

- Hanna Oberg at Home Workout (P.D.F) - EbayDocument4 pagesHanna Oberg at Home Workout (P.D.F) - EbayAdelina Nicoleta0% (4)