You might also like

- Multiple Choice Questions (MCQ) On Press Working - Page 2 of 2 - Scholarexpress2Document1 pageMultiple Choice Questions (MCQ) On Press Working - Page 2 of 2 - Scholarexpress2Prashant SinghNo ratings yet

- ME2029 DJF 2 Marks +16 Mark QuestionsDocument15 pagesME2029 DJF 2 Marks +16 Mark QuestionssureshkumarNo ratings yet

- Question Paper Code:: (10×2 20 Marks)Document2 pagesQuestion Paper Code:: (10×2 20 Marks)jastraNo ratings yet

- ME8073 - UNCONVENTIONAL MACHINING PROCESSES SyllabusDocument2 pagesME8073 - UNCONVENTIONAL MACHINING PROCESSES SyllabusP.N. MohankumarNo ratings yet

- Dsa 5500Document12 pagesDsa 5500Nguyen Van ToanNo ratings yet

- Fitter MCQDocument10 pagesFitter MCQRahul RawatNo ratings yet

- Computer Application in DesignDocument1 pageComputer Application in DesignAntony PrabuNo ratings yet

- GT MCQDocument11 pagesGT MCQgoreabhayNo ratings yet

- Subject Metal Cutting and Tool Design de PDFDocument2 pagesSubject Metal Cutting and Tool Design de PDFBabuli KumarNo ratings yet

- Cadcamcim MCQDocument9 pagesCadcamcim MCQRebecca MeyersNo ratings yet

- ASSIGNMENT - Modelling and Simulation of Manufacturing SystemDocument1 pageASSIGNMENT - Modelling and Simulation of Manufacturing SystemShabbir WahabNo ratings yet

- Sathyabama Question PaperDocument3 pagesSathyabama Question PaperamiestudentNo ratings yet

- Question Paper 2 PDFDocument4 pagesQuestion Paper 2 PDFfotickNo ratings yet

- Unit-2-Computer Aided DesignDocument42 pagesUnit-2-Computer Aided DesignMuthuvel M80% (5)

- Chapter 02 Multiple Choice Questions With AnswersDocument2 pagesChapter 02 Multiple Choice Questions With AnswersKuldeep Kushwaha100% (2)

- ME83691-Computer Aided Design and ManufacturingDocument15 pagesME83691-Computer Aided Design and Manufacturingraman thiru55No ratings yet

- Cad Cam Syllabus PDFDocument2 pagesCad Cam Syllabus PDFBrijesh Kumar ChaurasiyaNo ratings yet

- Manufacturing Technology Lab IDocument43 pagesManufacturing Technology Lab IMECHANICAL SMCETNo ratings yet

- Mass PropertiesDocument17 pagesMass Propertiespalaniappan_pandianNo ratings yet

- CAD/CAM - Objective Questions - Unit2Document2 pagesCAD/CAM - Objective Questions - Unit2Anonymous YkDJkSqNo ratings yet

- Simulation Lab ManualDocument60 pagesSimulation Lab Manualvensesfrank100% (1)

- CD 5291 Computer Aided Tools For ManufactiringDocument2 pagesCD 5291 Computer Aided Tools For ManufactiringGnaneswaran Narayanan63% (8)

- CNC Part A PDFDocument25 pagesCNC Part A PDFAKSHAY NambiarNo ratings yet

- Manufacturing Processes Set 2Document6 pagesManufacturing Processes Set 2Junaid ZafarNo ratings yet

- Fem Notes PDFDocument2 pagesFem Notes PDFRolandNo ratings yet

- MidTermExam CADCAM2019 FFDocument6 pagesMidTermExam CADCAM2019 FFkhalil alhatabNo ratings yet

- CAD CAM Unit - 3 PPT-ilovepdf-compressedDocument66 pagesCAD CAM Unit - 3 PPT-ilovepdf-compressedTaha SakriwalaNo ratings yet

- 300+ TOP THEORY of MACHINES Questions and Answers PDFDocument32 pages300+ TOP THEORY of MACHINES Questions and Answers PDFkrishnaNo ratings yet

- GE 6261 Final PDFDocument58 pagesGE 6261 Final PDFPrasath Murugesan0% (1)

- Unit-I Two Marks Questions and Answers 1. Explain CIMDocument4 pagesUnit-I Two Marks Questions and Answers 1. Explain CIMKailashNo ratings yet

- Machine Design Unit 1 Design PhilosophyDocument12 pagesMachine Design Unit 1 Design PhilosophyAnand Babu100% (3)

- Unit 4 & 5 ME8691 Computer Aided Design and ManufacturingDocument26 pagesUnit 4 & 5 ME8691 Computer Aided Design and ManufacturingMECHGOKUL KRISHNA KNo ratings yet

- Casting, Forming and Joining Processes - Materials, Manufacturing and Industrial Engineering - ME - GATE Syllabus, Paper Solution, Question AnswerDocument44 pagesCasting, Forming and Joining Processes - Materials, Manufacturing and Industrial Engineering - ME - GATE Syllabus, Paper Solution, Question Answerraja375205No ratings yet

- Mechanics of Material - SyllabusDocument2 pagesMechanics of Material - SyllabusRahul PatilNo ratings yet

- Question Answer On Lathe Milling Drilling Grinding (Join AICTE Telegram Group)Document74 pagesQuestion Answer On Lathe Milling Drilling Grinding (Join AICTE Telegram Group)Vivek SharmaNo ratings yet

- AIP Lab Manual - 012110050524 - 1Document11 pagesAIP Lab Manual - 012110050524 - 1Martin De Boras PragashNo ratings yet

- Me6703 Cim - QBDocument22 pagesMe6703 Cim - QBMukesh SaravananNo ratings yet

- Unit IV Assembly of Parts PDFDocument16 pagesUnit IV Assembly of Parts PDFSudhakarNo ratings yet

- PPC Model ExamDocument3 pagesPPC Model ExambalajimeieNo ratings yet

- Unit II Curves & SurfacesDocument57 pagesUnit II Curves & Surfacesvishwajeet patilNo ratings yet

- Tool Design 2 MarksDocument85 pagesTool Design 2 MarksKesava PrasadNo ratings yet

- Cad MCQ Unit 5Document3 pagesCad MCQ Unit 5ddeepak123No ratings yet

- Important Questions MetrologyDocument5 pagesImportant Questions Metrologyswathi_ipe100% (1)

- Unit-4-Computer Aided DesignDocument15 pagesUnit-4-Computer Aided DesignMuthuvel M100% (2)

- Autocad MCQDocument5 pagesAutocad MCQmulayharsh003No ratings yet

- Engineering Materials and Metallurgy QBDocument13 pagesEngineering Materials and Metallurgy QBAnand Jayakumar ArumughamNo ratings yet

- MCQs On SCBDocument9 pagesMCQs On SCBjigardesai100% (1)

- 12ed11 - Advanced Machine Tool DesignDocument15 pages12ed11 - Advanced Machine Tool DesignBradeesh MoorthyNo ratings yet

- Me2304 - Engineering Metrology and Measurements Question Bank For Regulation 2008Document29 pagesMe2304 - Engineering Metrology and Measurements Question Bank For Regulation 2008Ashok Kumar Rajendran75% (4)

- Design of Machine Element ProblemsDocument2 pagesDesign of Machine Element Problemsmaxpayne5550% (1)

- ME8793 Process Planning & Cost EstimationDocument35 pagesME8793 Process Planning & Cost Estimationarulmurugu100% (1)

- Cadm MCQ RevisionDocument17 pagesCadm MCQ Revision312817115009 D. Barathraj (IV - MHT)No ratings yet

- Top 350 MCQ PomDocument91 pagesTop 350 MCQ PomjaivikNo ratings yet

- UNIT 1 PPC MCQDocument9 pagesUNIT 1 PPC MCQSundara Selvam100% (1)

- Operations Management MCQsDocument32 pagesOperations Management MCQsVipin MisraNo ratings yet

- CAD CAM CIM Quiz 1Document1 pageCAD CAM CIM Quiz 1Jayesh BarveNo ratings yet

- FMS MCQDocument6 pagesFMS MCQSaran Ramachandran (RA1911002020032)No ratings yet

- Fees Change PDFDocument1 pageFees Change PDFAnonymous uHT7dDNo ratings yet

- SMETI 2020 Program Schedule With Paper ID Updated at 6.15 PMDocument8 pagesSMETI 2020 Program Schedule With Paper ID Updated at 6.15 PMGunasekaran JagadeesanNo ratings yet

- Tamilnadu Cements Corporation Limited: Recruitment Notification Notification No.3/ACW/2018 Date:06.01.2021Document12 pagesTamilnadu Cements Corporation Limited: Recruitment Notification Notification No.3/ACW/2018 Date:06.01.2021Gunasekaran JagadeesanNo ratings yet

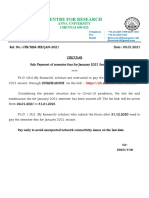

- Centre For Research: Dr. K.P. Jaya DirectorDocument1 pageCentre For Research: Dr. K.P. Jaya DirectorGunasekaran JagadeesanNo ratings yet

- TTD - FAQs dt.4-6-2016Document6 pagesTTD - FAQs dt.4-6-2016Srinivas KrishnaNo ratings yet

- Pra BHUDocument27 pagesPra BHUuismechprojectNo ratings yet

- 321 LT ServiceDocument3 pages321 LT ServiceGokul MurugesanNo ratings yet

- Tamilnadu Cements Corporation Limited: Recruitment Notification Notification No.3/ACW/2018 Date:06.01.2021Document12 pagesTamilnadu Cements Corporation Limited: Recruitment Notification Notification No.3/ACW/2018 Date:06.01.2021Gunasekaran JagadeesanNo ratings yet

- Format For Application For TransferDocument1 pageFormat For Application For TransferRishi KathirNo ratings yet

- Format For Application For TransferDocument1 pageFormat For Application For TransferRishi KathirNo ratings yet

- Tariff Change Form: Terms and ConditionsDocument2 pagesTariff Change Form: Terms and ConditionsGunasekaran JagadeesanNo ratings yet

- Me6019 NDTM Unit 1 NotesDocument16 pagesMe6019 NDTM Unit 1 NotesAnonymous 6SivdzjNo ratings yet

- MCQ Au Mech Sem ViiDocument2 pagesMCQ Au Mech Sem ViiGunasekaran JagadeesanNo ratings yet

- Application Format For Principal (Senior Secondary School)Document10 pagesApplication Format For Principal (Senior Secondary School)Gunasekaran JagadeesanNo ratings yet

- ME6019 NDTM Unit 2 NotesDocument27 pagesME6019 NDTM Unit 2 NotesGunasekaran JagadeesanNo ratings yet

- Unit I - Non-Destructive Testing:: An Introduction, Visual Inspection & Liquid Penetrant TestingDocument22 pagesUnit I - Non-Destructive Testing:: An Introduction, Visual Inspection & Liquid Penetrant TestingGunasekaran JagadeesanNo ratings yet

- Sensors: Non-Destructive Techniques Based On Eddy Current TestingDocument41 pagesSensors: Non-Destructive Techniques Based On Eddy Current TestingRohan JoshiNo ratings yet

- 4 MMCsDocument33 pages4 MMCsGunasekaran JagadeesanNo ratings yet

- Agricultural Mechanics Fundamentals and Applications 7th Edition Herren Solutions Manual 1Document5 pagesAgricultural Mechanics Fundamentals and Applications 7th Edition Herren Solutions Manual 1owen100% (26)

- Saic M 1030Document3 pagesSaic M 1030Hussain Nasser Al- NowiesserNo ratings yet

- 08R KG20 Sheet Metal FormingDocument82 pages08R KG20 Sheet Metal FormingFajar PutraNo ratings yet

- Stamped Metal Jewelry: Creative Techniques & Designs For Making Custom JewelryDocument8 pagesStamped Metal Jewelry: Creative Techniques & Designs For Making Custom JewelryInterweave100% (1)

- 1946 Rusnok Mill Heads Cat PDFDocument25 pages1946 Rusnok Mill Heads Cat PDFfgrefeNo ratings yet

- Types of Pattern and Its ApplicationDocument27 pagesTypes of Pattern and Its ApplicationKarthik GanesanNo ratings yet

- Plant Register TemplateDocument4 pagesPlant Register TemplateimamtaNo ratings yet

- TVET 1 Worksheet 12 AlontagaDocument3 pagesTVET 1 Worksheet 12 AlontagaJohn Vince ReclaNo ratings yet

- Knuth Ecoturn 650-1000Document2 pagesKnuth Ecoturn 650-1000Iacob CornelNo ratings yet

- SPCCDocument10 pagesSPCCDeepak JainNo ratings yet

- Summer Training Presentation At: Chanderpur Works Pvt. LTDDocument14 pagesSummer Training Presentation At: Chanderpur Works Pvt. LTDPreet ChahalNo ratings yet

- Drilling of GFRP Composites To Achieve oDocument4 pagesDrilling of GFRP Composites To Achieve oanaya KhanNo ratings yet

- AskelandPhuleNotes CH07PrintableDocument56 pagesAskelandPhuleNotes CH07PrintableManoj Janardan Jayashree TerekarNo ratings yet

- Turning Grades GC3225 and GC3210: Two Grades Covering All Cast Iron Turning OperationsDocument4 pagesTurning Grades GC3225 and GC3210: Two Grades Covering All Cast Iron Turning OperationsBilal AhmedNo ratings yet

- Unit 7 Basic Operation of A Milling MachineDocument15 pagesUnit 7 Basic Operation of A Milling Machinegsudhanta1604No ratings yet

- Cosmos Imtex Die MouldDocument2 pagesCosmos Imtex Die MouldAbhishek Velaga100% (2)

- Table Thread ReferenceDocument40 pagesTable Thread Referencejesse_w_petersNo ratings yet

- Machining Recommendations: Advice For Reducing Vibrations and Increasing The Drill Life LengthDocument3 pagesMachining Recommendations: Advice For Reducing Vibrations and Increasing The Drill Life LengthbasaricaNo ratings yet

- Full Annealing Full Annealing Is The Process of Slowly Raising The Temperature About 50Document10 pagesFull Annealing Full Annealing Is The Process of Slowly Raising The Temperature About 50scorpionarnoldNo ratings yet

- AReviewof Cylindrical Grinding ProcessDocument12 pagesAReviewof Cylindrical Grinding ProcessSardar HamzaNo ratings yet

- Sae J513 (1997)Document44 pagesSae J513 (1997)elangopi89100% (3)

- Fitter Mechanical Assembly (CSCQ0304)Document7 pagesFitter Mechanical Assembly (CSCQ0304)yudiar djamaldilliahNo ratings yet

- AI - Socket Set Screw Flat PointDocument57 pagesAI - Socket Set Screw Flat PointHugo Mario Ariza PalacioNo ratings yet

- Weld Defects CswipDocument10 pagesWeld Defects CswipOLiver RobertNo ratings yet

- Tech D (001-047)Document47 pagesTech D (001-047)Alejandro CouceiroNo ratings yet

- Lab Report On Robotic WeldingDocument8 pagesLab Report On Robotic WeldingSanatan ChoudhuryNo ratings yet

- FastenersDocument4 pagesFastenersjohanNo ratings yet

- Sip 8 PDocument13 pagesSip 8 Pappireddy_scribdNo ratings yet

- Photos of Defects Found in RadiographyDocument14 pagesPhotos of Defects Found in RadiographyKavipriyan KaviNo ratings yet

- CNC 101Document13 pagesCNC 101Hendi RofiansyahNo ratings yet