You might also like

- College of Accountancy and Finance: 1st Semester, S.Y. 2018-2019 Page 1 of 4 Prof. GMDocument4 pagesCollege of Accountancy and Finance: 1st Semester, S.Y. 2018-2019 Page 1 of 4 Prof. GMPpp BbbNo ratings yet

- Cpar - Ap 09.15.13Document18 pagesCpar - Ap 09.15.13KamilleNo ratings yet

- CBS Corporation Purchased 10Document12 pagesCBS Corporation Purchased 10Stella SabaoanNo ratings yet

- Auditing Problem 2Document1 pageAuditing Problem 2jhobs100% (1)

- A Home Office InventoryDocument1 pageA Home Office InventoryJulrick Cubio EgbusNo ratings yet

- Balbin, Ma. Margarette P. Assignment #1Document7 pagesBalbin, Ma. Margarette P. Assignment #1Margaveth P. BalbinNo ratings yet

- Coursehero 12Document2 pagesCoursehero 12nhbNo ratings yet

- Cash BasisDocument4 pagesCash BasisMark DiezNo ratings yet

- Chapter 1Document13 pagesChapter 1Ella Marie WicoNo ratings yet

- LAWDocument5 pagesLAWFrancis AbuyuanNo ratings yet

- Department of Accountancy: Page - 1Document16 pagesDepartment of Accountancy: Page - 1NoroNo ratings yet

- Rmbe Afar For PrintingDocument18 pagesRmbe Afar For PrintingjxnNo ratings yet

- NU - Correction of Errors Single Entry Cash To AccrualDocument8 pagesNU - Correction of Errors Single Entry Cash To AccrualJem ValmonteNo ratings yet

- TX 1102 Deductions from Gross Income Itemized and Special DeductionsDocument10 pagesTX 1102 Deductions from Gross Income Itemized and Special DeductionsJulz0% (1)

- Accounting ForDocument18 pagesAccounting ForKriztleKateMontealtoGelogoNo ratings yet

- Toa.m-1402. Review of The Accounting ProcessDocument5 pagesToa.m-1402. Review of The Accounting ProcessLINDIE MARIE RABENo ratings yet

- Homework on investment property analysisDocument2 pagesHomework on investment property analysisCharles TuazonNo ratings yet

- Seatwork - Advacc1Document2 pagesSeatwork - Advacc1David DavidNo ratings yet

- D5Document12 pagesD5Mark Lord Morales BumagatNo ratings yet

- RFBT AssessmentDocument9 pagesRFBT AssessmentJirah Bernal100% (1)

- A Government Employee May Claim The Tax InformerDocument3 pagesA Government Employee May Claim The Tax InformerYuno NanaseNo ratings yet

- Midterm Exam No. 2Document1 pageMidterm Exam No. 2Anie MartinezNo ratings yet

- Quiz 2 - Corp Liqui and Installment SalesDocument8 pagesQuiz 2 - Corp Liqui and Installment SalesKenneth Christian WilburNo ratings yet

- ReportDocument4 pagesReportryan angelica allanicNo ratings yet

- Ac3a Qe Oct2014 (TQ)Document15 pagesAc3a Qe Oct2014 (TQ)Julrick Cubio EgbusNo ratings yet

- Assignment 3.2 Inventory CutoffDocument3 pagesAssignment 3.2 Inventory CutoffHannah NolongNo ratings yet

- LiabilitiesDocument15 pagesLiabilitiesegroj arucalamNo ratings yet

- AFAR 01 Partnership AccountingDocument6 pagesAFAR 01 Partnership AccountingAriel DimalantaNo ratings yet

- MGA DAMBIEEE!!!! Complete AnswerDocument12 pagesMGA DAMBIEEE!!!! Complete AnswerHannah Jane UmbayNo ratings yet

- Assignment Transfer Tax ComputationDocument3 pagesAssignment Transfer Tax ComputationAngelyn SamandeNo ratings yet

- 11.11.2017 Audit of PPEDocument9 pages11.11.2017 Audit of PPEPatOcampoNo ratings yet

- Group Quizbowl FormattedDocument17 pagesGroup Quizbowl FormattedSarah BalisacanNo ratings yet

- Exercises - Percentage TaxesDocument2 pagesExercises - Percentage TaxesMaristella GatonNo ratings yet

- Acctg 2 QuizDocument4 pagesAcctg 2 QuizAshNor RandyNo ratings yet

- There May Be A Property Relationship of Conjugal PDocument6 pagesThere May Be A Property Relationship of Conjugal PJunho ChaNo ratings yet

- An SME Prepared The Following Post Closing Trial Balance at YearDocument1 pageAn SME Prepared The Following Post Closing Trial Balance at YearRaca DesuNo ratings yet

- Unit 7 Audit of IntangiblesDocument10 pagesUnit 7 Audit of IntangiblesVianca Isabel PagsibiganNo ratings yet

- Correction of Errors: Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument5 pagesCorrection of Errors: Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionmaurNo ratings yet

- G.M4 HW GWDocument3 pagesG.M4 HW GWClint Agustin M. RoblesNo ratings yet

- Conceptual FrameworkDocument9 pagesConceptual FrameworkAveryl Lei Sta.Ana0% (1)

- Quiz Number One Without AnswerDocument8 pagesQuiz Number One Without AnswerKpop updates 24/7No ratings yet

- Drill Problems - ConsolidationDocument6 pagesDrill Problems - Consolidationgun attaphanNo ratings yet

- Acct. 162 - EPS, BVPS, DividendsDocument5 pagesAcct. 162 - EPS, BVPS, DividendsAngelli LamiqueNo ratings yet

- Gialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingDocument12 pagesGialogo, Jessie Lyn San Sebastian College - Recoletos Quiz: Required: Answer The FollowingMeidrick Rheeyonie Gialogo AlbaNo ratings yet

- Afar 107 - Business Combination Part 2Document4 pagesAfar 107 - Business Combination Part 2Maria LopezNo ratings yet

- Consolidation at Acquisition DateDocument29 pagesConsolidation at Acquisition DateLee DokyeomNo ratings yet

- Installment Sales Accounting CalculationsDocument12 pagesInstallment Sales Accounting CalculationsJocel Ann GuerraNo ratings yet

- PUP - Assignment No. 3 - Income Taxation - 2nd Sem AY 2020-2021: RequiredDocument12 pagesPUP - Assignment No. 3 - Income Taxation - 2nd Sem AY 2020-2021: RequiredGabrielle Marie RiveraNo ratings yet

- Audit of Investments - Set ADocument4 pagesAudit of Investments - Set AZyrah Mae SaezNo ratings yet

- Audit of SheDocument3 pagesAudit of ShegbenjielizonNo ratings yet

- Auditing Problems SolvedDocument9 pagesAuditing Problems SolvedGlizette SamaniegoNo ratings yet

- DocxDocument10 pagesDocxAiziel OrenseNo ratings yet

- College: of Business AdministrationDocument5 pagesCollege: of Business AdministrationAna Mae HernandezNo ratings yet

- Father Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)Document10 pagesFather Saturnino Urios University Accountancy Program AIR-Cluster 1 (Drill #4)marygraceomacNo ratings yet

- Competency Appraisal UM Digos (PARTNERSHIP)Document10 pagesCompetency Appraisal UM Digos (PARTNERSHIP)Diana Faye CaduadaNo ratings yet

- PRTC 1st Preboard Solution GuideDocument48 pagesPRTC 1st Preboard Solution GuideAnonymous Lih1laax100% (2)

- Mock Deparmentals MASQDocument6 pagesMock Deparmentals MASQHannah Joyce MirandaNo ratings yet

- INSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyDocument15 pagesINSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyMendoza Ron NixonNo ratings yet

- Seatwork in Audit 2-3Document8 pagesSeatwork in Audit 2-3Shr BnNo ratings yet

- ReceivableDocument3 pagesReceivableBellaNo ratings yet

- Government Accounting: Chapters 1-3 Sets of QuestionsDocument6 pagesGovernment Accounting: Chapters 1-3 Sets of QuestionsnovyNo ratings yet

- VCM QuizDocument4 pagesVCM QuiznovyNo ratings yet

- Seat WorkDocument2 pagesSeat WorknovyNo ratings yet

- Seat WorkDocument2 pagesSeat WorknovyNo ratings yet

- Essential Characteristics of A Contract of SaleDocument4 pagesEssential Characteristics of A Contract of SalenovyNo ratings yet

- Summary of Responsibility AccountingDocument2 pagesSummary of Responsibility AccountingnovyNo ratings yet

- Audit Program for KMJS Pineapple CorporationDocument6 pagesAudit Program for KMJS Pineapple CorporationnovyNo ratings yet

- Mind Your Own BusinessDocument1 pageMind Your Own BusinessnovyNo ratings yet

- Remedies of Unpiad SellerDocument17 pagesRemedies of Unpiad SellernovyNo ratings yet

- Ajhd HDDocument5 pagesAjhd HDnovyNo ratings yet

- The Baguio District Branch of Kapa EnterprisesDocument1 pageThe Baguio District Branch of Kapa EnterprisesnovyNo ratings yet

- Audit Procedures for Accounts Payable, Interest Payable, Notes Payable, and WarrantiesDocument1 pageAudit Procedures for Accounts Payable, Interest Payable, Notes Payable, and WarrantiesnovyNo ratings yet

- For All YouDocument2 pagesFor All YounovyNo ratings yet

- Tax Assign.Document1 pageTax Assign.novyNo ratings yet

- For All YouDocument2 pagesFor All YounovyNo ratings yet

- Related Review LiteratureDocument1 pageRelated Review LiteraturenovyNo ratings yet

- Risk of Unsold Fruit: Marketing Risk: Pineapple ExportingDocument1 pageRisk of Unsold Fruit: Marketing Risk: Pineapple ExportingnovyNo ratings yet

- Final Requirement in AdvaccDocument143 pagesFinal Requirement in AdvaccShaina Kaye De Guzman100% (1)

- Executive SummaryDocument1 pageExecutive SummarynovyNo ratings yet

- DISCUSSION Group 3Document2 pagesDISCUSSION Group 3novyNo ratings yet

- StratDocument3 pagesStratnovyNo ratings yet

- Tax Assign.Document1 pageTax Assign.novyNo ratings yet

- Ched Midterm ExamDocument1 pageChed Midterm ExamnovyNo ratings yet

- It Should Be Separated Because To Prevent Fraud and Promote Accountability Ensuring That The Prepared Financial Statements Are ReliableDocument1 pageIt Should Be Separated Because To Prevent Fraud and Promote Accountability Ensuring That The Prepared Financial Statements Are ReliablenovyNo ratings yet

- According To PSADocument1 pageAccording To PSAnovyNo ratings yet

- ATOM IncDocument1 pageATOM IncnovyNo ratings yet

- ConclusionDocument1 pageConclusionnovyNo ratings yet

- Book Value Fair Value Building (10 Years Life) 10,000 8,000 Equipment (4 Years Life) 14,000 18,000 Land 5,000 12,000Document1 pageBook Value Fair Value Building (10 Years Life) 10,000 8,000 Equipment (4 Years Life) 14,000 18,000 Land 5,000 12,000novyNo ratings yet

- Afar ResearchDocument1 pageAfar ResearchnovyNo ratings yet

- The 5 Best Accounting Software For Small Business of 2021Document4 pagesThe 5 Best Accounting Software For Small Business of 2021novyNo ratings yet

- FinancialAnalysis - EQUIPOS DEL NORTEDocument6 pagesFinancialAnalysis - EQUIPOS DEL NORTEOscar TrujilloNo ratings yet

- Quality Control ChecklistDocument7 pagesQuality Control Checklistdarma bonarNo ratings yet

- Banking Laws 2018 2019 SummerDocument5 pagesBanking Laws 2018 2019 SummerJonathanNo ratings yet

- Sub: Risk Assumption Letter: Insured & Vehicle DetailsDocument3 pagesSub: Risk Assumption Letter: Insured & Vehicle DetailsPRA SUNo ratings yet

- ETF Screener - JustETF A2Document4 pagesETF Screener - JustETF A2fish0123No ratings yet

- RBL Aspire Banking benefits and criteriaDocument1 pageRBL Aspire Banking benefits and criteriaBadri ShaikhNo ratings yet

- 500 Practice Questions For BRBL PaperDocument89 pages500 Practice Questions For BRBL PaperJyoti LahaneNo ratings yet

- Operational Guidelines of Rural Godown Scheme 1. BackgroundDocument11 pagesOperational Guidelines of Rural Godown Scheme 1. BackgroundVivek SoniNo ratings yet

- Payment Receipt PDFDocument1 pagePayment Receipt PDFHardikNo ratings yet

- Acst PDFDocument3 pagesAcst PDFkazliNo ratings yet

- e-StatementBRImo 666201008493534 Jun2023 20230605 234408-1Document3 pagese-StatementBRImo 666201008493534 Jun2023 20230605 234408-1Tri AriestaNo ratings yet

- Pearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test BankDocument45 pagesPearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test Bankloanazura7k6bl100% (27)

- Handout 11 2021 Oblicon Online ClassDocument3 pagesHandout 11 2021 Oblicon Online ClassGella B. RequilloNo ratings yet

- FM 2012 WorksheetDocument9 pagesFM 2012 WorksheetBeing ShonuNo ratings yet

- Junk Bond Risks and ReturnsDocument3 pagesJunk Bond Risks and ReturnsFatima ZahidNo ratings yet

- MCQ QuestionsDocument6 pagesMCQ QuestionsANo ratings yet

- Askari Bank Personal Loan CBD Excel SheetDocument4 pagesAskari Bank Personal Loan CBD Excel Sheetsumbul imranNo ratings yet

- Muat TurunDocument3 pagesMuat Turunhadifanna18No ratings yet

- Padma Islami Life Insurance Ltd. at a glanceDocument8 pagesPadma Islami Life Insurance Ltd. at a glancebiswasjoyNo ratings yet

- 50 Sow Unit Piggery Business Plan Financials - USDDocument15 pages50 Sow Unit Piggery Business Plan Financials - USDonward marumuraNo ratings yet

- Project Report On Icici Bank by Gaurav NarangDocument103 pagesProject Report On Icici Bank by Gaurav NarangsagarNo ratings yet

- Comparison of Eastern Shipping vs CA and Nacar vs Gallery Frames RulingsDocument13 pagesComparison of Eastern Shipping vs CA and Nacar vs Gallery Frames RulingsBeth's NotThat HumanNo ratings yet

- Ross 12e PPT Ch05 Formulas (1) - 1Document19 pagesRoss 12e PPT Ch05 Formulas (1) - 1JNo ratings yet

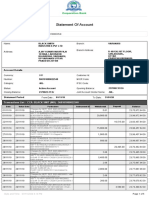

- Statement of AccountDocument5 pagesStatement of AccountAjay MauryaNo ratings yet

- Jupiter International LimitedDocument6 pagesJupiter International LimitedRahul syalNo ratings yet

- Paulson Credit Opportunity 2007 Year EndDocument16 pagesPaulson Credit Opportunity 2007 Year EndjackefellerNo ratings yet

- Questionnaire "A Study On Investment Behaviour of Academician With Special Reference To Surat City"Document7 pagesQuestionnaire "A Study On Investment Behaviour of Academician With Special Reference To Surat City"Bhakti MehtaNo ratings yet

- Chap 15, 16, 17 AssignmentDocument12 pagesChap 15, 16, 17 AssignmentSamantha Charlize VizcondeNo ratings yet

- Asset-Liability Management: Society of Actuaries Professional Actuarial Specialty GuideDocument129 pagesAsset-Liability Management: Society of Actuaries Professional Actuarial Specialty GuideMarina Markovic Stefanovic100% (2)

- HADM 2250 Prelim Review QuestionsDocument52 pagesHADM 2250 Prelim Review QuestionsPrithvi BhushanNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Business Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsFrom EverandBusiness Valuation: Private Equity & Financial Modeling 3 Books In 1: 27 Ways To Become A Successful Entrepreneur & Sell Your Business For BillionsNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Basic Accounting: Service Business Study GuideFrom EverandBasic Accounting: Service Business Study GuideRating: 5 out of 5 stars5/5 (2)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- NLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsFrom EverandNLP:The Essential Handbook for Business: The Essential Handbook for Business: Communication Techniques to Build Relationships, Influence Others, and Achieve Your GoalsRating: 4.5 out of 5 stars4.5/5 (4)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Emprender un Negocio: Paso a Paso Para PrincipiantesFrom EverandEmprender un Negocio: Paso a Paso Para PrincipiantesRating: 3 out of 5 stars3/5 (1)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- The CEO X factor: Secrets for Success from South Africa's Top Money MakersFrom EverandThe CEO X factor: Secrets for Success from South Africa's Top Money MakersNo ratings yet