You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Introduction To The Stock Market Part One: AssetDocument3 pagesIntroduction To The Stock Market Part One: AssetkimmoNo ratings yet

- 2021-22 JRHMSF Academic FAQsDocument16 pages2021-22 JRHMSF Academic FAQskimmoNo ratings yet

- More Eq Questions AnswersDocument2 pagesMore Eq Questions AnswerskimmoNo ratings yet

- AGR 3000-MD-Assignment 1Document6 pagesAGR 3000-MD-Assignment 1kimmoNo ratings yet

- 9.6 Keynesian MultiplierDocument23 pages9.6 Keynesian MultiplierkimmoNo ratings yet

- Biology 30 Unit C - Cell Division, Genetics, and Molecular Genetics - Chapter 18Document165 pagesBiology 30 Unit C - Cell Division, Genetics, and Molecular Genetics - Chapter 18kimmoNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Partnership Accounting: FormationDocument6 pagesPartnership Accounting: FormationLee SuarezNo ratings yet

- Cinco vs. Court of AppealsDocument5 pagesCinco vs. Court of AppealsDiana Rose OngotanNo ratings yet

- Prescription PeriodDocument3 pagesPrescription Periodjaylibee100% (1)

- Bulatao V ZenaidaDocument3 pagesBulatao V ZenaidaMaisie ZabalaNo ratings yet

- SHG Bookkeeping Training ModularDocument27 pagesSHG Bookkeeping Training ModularAdi DasNo ratings yet

- Group 2 Housing Development and ManagementDocument29 pagesGroup 2 Housing Development and ManagementTumwesigye AllanNo ratings yet

- Solution Manual For Introduction To Finance 17th Edition Ronald W MelicherDocument23 pagesSolution Manual For Introduction To Finance 17th Edition Ronald W MelicherJonathanLindseymepj100% (44)

- Truth in Lending Act - Data BankDocument2 pagesTruth in Lending Act - Data Bankjeongchaeng no jam brotherNo ratings yet

- Grimes Federal Amended ComplaintDocument26 pagesGrimes Federal Amended ComplaintQb SimmsNo ratings yet

- Indoor ManagementDocument59 pagesIndoor ManagementgauravNo ratings yet

- P&I Certificate of EntryDocument6 pagesP&I Certificate of EntryWILLINTON HINOJOSA0% (1)

- Oil & Gas Property AcquisitionDocument4 pagesOil & Gas Property AcquisitionIkhwanushafa DjailaniNo ratings yet

- Department of Education: Learning Activity Sheet in Business MathematicsDocument14 pagesDepartment of Education: Learning Activity Sheet in Business MathematicsJanna GunioNo ratings yet

- Export FinanceDocument29 pagesExport FinanceAishu KrishnanNo ratings yet

- What Is Legal and Technical Verification in Home Loan Processing, NIDHIDocument9 pagesWhat Is Legal and Technical Verification in Home Loan Processing, NIDHIVivek LedwaniNo ratings yet

- Final OrderDocument10 pagesFinal OrderThe Press-Enterprise / pressenterprise.comNo ratings yet

- About The 2008 Financial Crisis-GocelaDocument3 pagesAbout The 2008 Financial Crisis-GocelaCervantes LeonaNo ratings yet

- Toa 41 42 PDFDocument22 pagesToa 41 42 PDFspur iousNo ratings yet

- Villa Crista Monte Realty vs. Equitable PCI BankDocument1 pageVilla Crista Monte Realty vs. Equitable PCI BankabbywinsterNo ratings yet

- Reading 45 Introduction To Asset-Backed SecuritiesDocument15 pagesReading 45 Introduction To Asset-Backed SecuritiesNeerajNo ratings yet

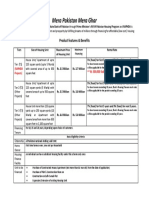

- Mera Pakistan Mera Ghar: Product Features & BenefitsDocument1 pageMera Pakistan Mera Ghar: Product Features & BenefitsAli Azhar KhanNo ratings yet

- Credit Transactions: Final ExamDocument1 pageCredit Transactions: Final ExamMayette Belgica-ClederaNo ratings yet

- Sample Letter To Bank Extension in Loan RepaymentDocument4 pagesSample Letter To Bank Extension in Loan RepaymentangelNo ratings yet

- Elective - I - 506 Financial Markets and Services (F)Document13 pagesElective - I - 506 Financial Markets and Services (F)dominic wurdaNo ratings yet

- Appraisal Ce Exam 4 Review PDFDocument30 pagesAppraisal Ce Exam 4 Review PDFAmeerNo ratings yet

- Teachers ATM Cards As Loan Collateral: The In-Depth Look Into ATM "Sangla" SchemeDocument17 pagesTeachers ATM Cards As Loan Collateral: The In-Depth Look Into ATM "Sangla" SchemeJan Reindonn MabanagNo ratings yet

- Sione and Andrea (Rework)Document10 pagesSione and Andrea (Rework)Ammer Yaser MehetanNo ratings yet

- 9.10 Case DigestsDocument22 pages9.10 Case DigestsSharla Louisse Arizabal CastilloNo ratings yet

- CFAF Std. T&C (EL) - Standard Terms and Conditions Governing Education LoanDocument5 pagesCFAF Std. T&C (EL) - Standard Terms and Conditions Governing Education LoanAvinab PandeyNo ratings yet

- Tax 1st Preboard Questionnaire BDocument6 pagesTax 1st Preboard Questionnaire BAlexis Kaye DayagNo ratings yet