You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Stephen Elias, Bethany K. Laurence - Bankruptcy For Small Business Owners - How To File For Chapter 7-Nolo (2010)Document612 pagesStephen Elias, Bethany K. Laurence - Bankruptcy For Small Business Owners - How To File For Chapter 7-Nolo (2010)anassNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionNo ratings yet

- James Wood ForestDocument2 pagesJames Wood Forestangel WebbNo ratings yet

- ACTG21C - Midterm ExamDocument8 pagesACTG21C - Midterm ExamJuanito TanamorNo ratings yet

- Acb239 Practice Final Exam Questions and AnswersDocument15 pagesAcb239 Practice Final Exam Questions and AnswersAshley Danielle NaquinNo ratings yet

- ACC 290 Final Exam AnswersDocument12 pagesACC 290 Final Exam AnswerszeshansidraNo ratings yet

- 6801 - Accounting Process PDFDocument5 pages6801 - Accounting Process PDFSheila Mae PioquintoNo ratings yet

- Accounting 101 FinalsDocument16 pagesAccounting 101 FinalsDanilo Diniay Jr100% (1)

- Principle of Accounting I Final ExamDocument3 pagesPrinciple of Accounting I Final ExamAbrha Giday100% (5)

- Wiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 2, Financial Decision Making (1-year access)No ratings yet

- CAE 2 Financial Accounting and Reporting: L-NU AA-23-02-01-18Document8 pagesCAE 2 Financial Accounting and Reporting: L-NU AA-23-02-01-18Amie Jane Miranda100% (1)

- Quickbooks Online Certification Practice TestDocument9 pagesQuickbooks Online Certification Practice TestErika Mie Ulat100% (1)

- Adjusting Entry Multiple Choice Question and Answer KeyDocument9 pagesAdjusting Entry Multiple Choice Question and Answer Keygnzg.bela50% (2)

- Bookkeeper Certification Practice TestDocument8 pagesBookkeeper Certification Practice TestLindcelle Jane Dalope100% (1)

- Level Three Theory (Knowledge) ChoiceDocument17 pagesLevel Three Theory (Knowledge) ChoiceYaa Rabbii100% (1)

- Second Grading Examination - Key AnswersDocument21 pagesSecond Grading Examination - Key AnswersAmie Jane Miranda100% (1)

- 1ST Exam Fabm1Document3 pages1ST Exam Fabm1rose gabonNo ratings yet

- Par Cor Accounting Cup - Average Round QuestionsDocument6 pagesPar Cor Accounting Cup - Average Round QuestionsShin YaeNo ratings yet

- Accounting MCQsDocument12 pagesAccounting MCQsLaraib AliNo ratings yet

- BFAR Qualifying Exam ReviewerDocument18 pagesBFAR Qualifying Exam ReviewerHappy MagdangalNo ratings yet

- SalaryDocument13 pagesSalaryErik Treasuryvala100% (1)

- 26u9ofk7l - FAR - FINAL EXAMDocument18 pages26u9ofk7l - FAR - FINAL EXAMLyra Mae De BotonNo ratings yet

- Test Financial AcountingDocument12 pagesTest Financial Acountingtouria100% (1)

- Activity No. 1 CA 2022 Financial Accounting and Reepeorting Far PCVDocument8 pagesActivity No. 1 CA 2022 Financial Accounting and Reepeorting Far PCVPrecious mae BarrientosNo ratings yet

- Part-2 Accounting QuestionsDocument7 pagesPart-2 Accounting QuestionslokeshNo ratings yet

- Chapter 4 - Article 1231-1241Document30 pagesChapter 4 - Article 1231-1241Jane CANo ratings yet

- Second Grading ExaminationDocument17 pagesSecond Grading ExaminationAmie Jane MirandaNo ratings yet

- Hidden DivergenceDocument5 pagesHidden DivergenceAccess LimitedNo ratings yet

- Accounting Fundamentals Practice TestDocument8 pagesAccounting Fundamentals Practice Testpetitfm0% (1)

- ACC 280 Final ExamDocument4 pagesACC 280 Final Examanon_624482436No ratings yet

- ACCT 2251 Practice FinalDocument20 pagesACCT 2251 Practice FinalHạnhNekoNo ratings yet

- FINALS EXAM - FinAcctg SetADocument4 pagesFINALS EXAM - FinAcctg SetAJennifer RasonabeNo ratings yet

- Ss 2 Objective Type BDocument6 pagesSs 2 Objective Type BUkoh OwoidohoNo ratings yet

- Cost-Accounting (Set 1)Document23 pagesCost-Accounting (Set 1)manglarohit423No ratings yet

- Cup 1 (Basic Accounting)Document4 pagesCup 1 (Basic Accounting)Hannah AbeloNo ratings yet

- Accouting ExamDocument7 pagesAccouting ExamThien PhuNo ratings yet

- REVIEWERDocument9 pagesREVIEWERHanns Lexter PadillaNo ratings yet

- Eco MCQDocument9 pagesEco MCQthis.is.goldensnowflakesNo ratings yet

- UntitledDocument10 pagesUntitledShravan A NekkarekaduNo ratings yet

- ACTG21C - Midterm Exam QuestionsDocument6 pagesACTG21C - Midterm Exam QuestionsJuanito TanamorNo ratings yet

- Far ReviewerDocument18 pagesFar RevieweremmanuelanecesitoNo ratings yet

- A191 BKAL1013 Tutorial 4 AnswersheetDocument11 pagesA191 BKAL1013 Tutorial 4 AnswersheetMan yeeNo ratings yet

- Quiz BeeDocument15 pagesQuiz Beejoshua100% (1)

- Theory of Debits & CreditsDocument4 pagesTheory of Debits & CreditsLiwliwa BrunoNo ratings yet

- March 2020 Insight Part IDocument88 pagesMarch 2020 Insight Part INifezNo ratings yet

- Sample Quiz Question 3Document7 pagesSample Quiz Question 3Sonam Dema DorjiNo ratings yet

- MC 0065 Financial Management and Accounting: Model Question Paper Subject Code: Subject Name: Credits: 4 Marks: 140Document16 pagesMC 0065 Financial Management and Accounting: Model Question Paper Subject Code: Subject Name: Credits: 4 Marks: 140jaypmauryaNo ratings yet

- Accounting (@JohnASTU)Document38 pagesAccounting (@JohnASTU)bezib7987No ratings yet

- 1 - Accounting ProcessDocument4 pages1 - Accounting ProcessJevanie CastroverdeNo ratings yet

- September 2021 Examinations: Joint Universities Preliminary Examinations BoardDocument15 pagesSeptember 2021 Examinations: Joint Universities Preliminary Examinations BoardBabawale KehindeNo ratings yet

- 6881 - Accounting ProcessDocument4 pages6881 - Accounting ProcessMaximusNo ratings yet

- Accounting and Finance Mock ExamDocument35 pagesAccounting and Finance Mock ExamAbdisen TeferaNo ratings yet

- Acctg 12 Premid Exam QuestionnaireDocument11 pagesAcctg 12 Premid Exam QuestionnaireJanet AnotdeNo ratings yet

- Accounting TestDocument15 pagesAccounting TestBenson WencenslausNo ratings yet

- Management-Accounting (Set 1)Document22 pagesManagement-Accounting (Set 1)Arul kumarNo ratings yet

- Financial Accounting & Reporting ReviewerDocument21 pagesFinancial Accounting & Reporting ReviewerRosemarie GoNo ratings yet

- ACC2010 Sample Final ExamDocument19 pagesACC2010 Sample Final ExamHarjot SinghNo ratings yet

- Accounting and Auditing MCQs Part-1 by Alisha Mahajan PDFDocument58 pagesAccounting and Auditing MCQs Part-1 by Alisha Mahajan PDFJamodvipulNo ratings yet

- Model Exit Exam Unity University A.ADocument36 pagesModel Exit Exam Unity University A.AMOLALIGNNo ratings yet

- Model Exit Exam 3Document36 pagesModel Exit Exam 3mearghaile4No ratings yet

- Theory of Accounts (No Ak)Document10 pagesTheory of Accounts (No Ak)Irish Joy AlaskaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- MA 2.1-Financial StatementDocument57 pagesMA 2.1-Financial Statementvini2710100% (1)

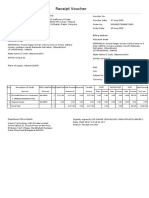

- Receipt Voucher: Xiaomi Technology India Private LimtiedDocument1 pageReceipt Voucher: Xiaomi Technology India Private LimtiedPankaj LohaniNo ratings yet

- Application To Adjudicating Authority - Form I AnnexureDocument3 pagesApplication To Adjudicating Authority - Form I AnnexureadityatnnlsNo ratings yet

- ISCA Insolvency Update 2017Document8 pagesISCA Insolvency Update 2017terencebctanNo ratings yet

- MAS CompiledDocument5 pagesMAS CompiledadorableperezNo ratings yet

- Primer - Quick and Easy Primer On Paying Your Taxes (BIR Issuance)Document11 pagesPrimer - Quick and Easy Primer On Paying Your Taxes (BIR Issuance)Diane JulianNo ratings yet

- SPM W4 130318150 Cindy Alexandra KP CDocument1 pageSPM W4 130318150 Cindy Alexandra KP Ccindy alexandraNo ratings yet

- Share MarketrDocument69 pagesShare Marketrduckman2009No ratings yet

- 21Document15 pages21AngelManuelCabacunganNo ratings yet

- Ibc ProjectDocument17 pagesIbc ProjectRaman PatelNo ratings yet

- AmcDocument9 pagesAmcerode els erodeNo ratings yet

- SBI Clerk Mains 2023 Exam PDF @crossword2022Document196 pagesSBI Clerk Mains 2023 Exam PDF @crossword2022Kannan KannanNo ratings yet

- Memorial For Petitioner PDFDocument28 pagesMemorial For Petitioner PDFdevil_3565No ratings yet

- Process Payments & ReceiptsDocument12 pagesProcess Payments & ReceiptsAnne FrondaNo ratings yet

- Adrian, T. & Brunnermeier, M. (2008) CoVaRDocument53 pagesAdrian, T. & Brunnermeier, M. (2008) CoVaRMateo ReinosoNo ratings yet

- Intellectual Capital A Human Capital PerspectiveDocument10 pagesIntellectual Capital A Human Capital PerspectivePedro GonçalvesNo ratings yet

- Statement of Income: P&L Account Can Also Be Named AsDocument5 pagesStatement of Income: P&L Account Can Also Be Named Asanand sanilNo ratings yet

- 2018 16-October Part-4 MemorandumDocument6 pages2018 16-October Part-4 MemorandumLucky NetshamutavhaNo ratings yet

- Home First Finance Company India Ltd. Notice of EGM 25-Aug-2020Document11 pagesHome First Finance Company India Ltd. Notice of EGM 25-Aug-2020Varun ChaudhariNo ratings yet

- Accounting For Receivables Accounts ReceivableDocument18 pagesAccounting For Receivables Accounts Receivablelocomotingkenya.co.keNo ratings yet

- B1 LicenseComparisonChartDocument9 pagesB1 LicenseComparisonChartcamperhpNo ratings yet

- Security Analysis and Portfolio Management Prof: C.S. Mishra Department of VGSOM Indian Institute of Technology, KharagpurDocument29 pagesSecurity Analysis and Portfolio Management Prof: C.S. Mishra Department of VGSOM Indian Institute of Technology, KharagpurviswanathNo ratings yet

- 2 - Case 8 QuestionsDocument1 page2 - Case 8 QuestionsSandip Agarwal0% (1)

- 3.03 Key TermsDocument95 pages3.03 Key Termsapi-262218593No ratings yet

- Solved Jennings Operated A Courier Service To Collect and Deliver MoneyDocument1 pageSolved Jennings Operated A Courier Service To Collect and Deliver MoneyAnbu jaromiaNo ratings yet