You might also like

- Control of Non-Conformity & Corrective ActionDocument5 pagesControl of Non-Conformity & Corrective ActionAli Kaya83% (6)

- Balance Sheet AnalysisDocument3 pagesBalance Sheet AnalysisNishant SinghNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- What Is Ratio AnalysisDocument19 pagesWhat Is Ratio AnalysisMarie Frances Sayson100% (1)

- Ra 8791 General Banking Law: Maria Ginalyn CalderonDocument67 pagesRa 8791 General Banking Law: Maria Ginalyn CalderonVAT CLIENTS100% (1)

- Financial Ratio IntrepretationDocument47 pagesFinancial Ratio IntrepretationRavi Singla100% (1)

- Pricing DecisionsDocument15 pagesPricing DecisionsHosahalli Narayana Murthy PrasannaNo ratings yet

- Discipline and Grievance ManagementDocument176 pagesDiscipline and Grievance ManagementTMTCS HR100% (1)

- Note On Financial Ratio AnalysisDocument9 pagesNote On Financial Ratio Analysisabhilash831989No ratings yet

- Odoo Inventory Management FeaturesDocument5 pagesOdoo Inventory Management FeaturesyudiNo ratings yet

- Bank ReconciliationDocument9 pagesBank ReconciliationhoxhiiNo ratings yet

- Strategic Outsourcing at Bharti Airtel: Should Network and IT Infrastructure be OutsourcedDocument9 pagesStrategic Outsourcing at Bharti Airtel: Should Network and IT Infrastructure be OutsourcedNIKHILA TUMMALANo ratings yet

- What Are Liquidity RatiosDocument2 pagesWhat Are Liquidity RatiosDarlene SarcinoNo ratings yet

- Far 2Document8 pagesFar 2Sonu NayakNo ratings yet

- Liquidity Ratio: What Are Liquidity Ratios?Document11 pagesLiquidity Ratio: What Are Liquidity Ratios?Ritesh KumarNo ratings yet

- Financial Analysis - Solvency VsDocument7 pagesFinancial Analysis - Solvency VsMohd MirulNo ratings yet

- Financial Analysis - Solvency VsDocument4 pagesFinancial Analysis - Solvency VsAndra L.No ratings yet

- Current RatioDocument16 pagesCurrent RatioamnllhgllNo ratings yet

- Answer 5Document3 pagesAnswer 5sharmamohitNo ratings yet

- Liquidity RatioDocument3 pagesLiquidity RatioJodette Karyl NuyadNo ratings yet

- Unit-12 Liquidity Vs ProfitabilityDocument14 pagesUnit-12 Liquidity Vs ProfitabilityKusum JaiswalNo ratings yet

- What Is The Current Ratio?Document10 pagesWhat Is The Current Ratio?Rica Princess MacalinaoNo ratings yet

- Acid-Test RatioDocument4 pagesAcid-Test RatioJonna NoveleroNo ratings yet

- Quick RatioDocument15 pagesQuick RatioAin roseNo ratings yet

- Financial LeverageDocument7 pagesFinancial LeverageGeanelleRicanorEsperonNo ratings yet

- Current RatioDocument22 pagesCurrent RatioAsawarNo ratings yet

- Read Ung Nasa Powerpoint.: LiquidityDocument3 pagesRead Ung Nasa Powerpoint.: Liquiditysharomeo castroNo ratings yet

- Cas Ii Assignment ON Importance of Liquidity Ratios in The IndustryDocument7 pagesCas Ii Assignment ON Importance of Liquidity Ratios in The IndustrySanchali GoraiNo ratings yet

- Financial Statement Analysis-IIDocument45 pagesFinancial Statement Analysis-IINeelisetty Satya SaiNo ratings yet

- Table of ContentsDocument57 pagesTable of ContentsAbhishek AbhiNo ratings yet

- Group Members:: Sameer Ahmed Muhammad Hamza Sheikh Muhammad Bilal Kasi Mir Hammal Baloch Lutf UllahDocument18 pagesGroup Members:: Sameer Ahmed Muhammad Hamza Sheikh Muhammad Bilal Kasi Mir Hammal Baloch Lutf UllahsameerbadeniNo ratings yet

- Financial Ratio TutorialDocument41 pagesFinancial Ratio Tutorialabhi2244inNo ratings yet

- Financial RatioDocument56 pagesFinancial RatioSaran JlNo ratings yet

- Current Ratio:: Definition of Current Ratio Formula Components Example Significance Limitations of Current RatioDocument3 pagesCurrent Ratio:: Definition of Current Ratio Formula Components Example Significance Limitations of Current RatioRachamalla KrishnareddyNo ratings yet

- Financial Ratio AnalysisDocument6 pagesFinancial Ratio AnalysishraigondNo ratings yet

- PROJECTDocument25 pagesPROJECTMUHAMMAD UMARNo ratings yet

- What Is The Current RatioDocument5 pagesWhat Is The Current RatioRijo RejiNo ratings yet

- Impact of Liquidity On ProfitabilityDocument44 pagesImpact of Liquidity On ProfitabilityRavi ShankarNo ratings yet

- Liquidity Ratios GuideDocument25 pagesLiquidity Ratios GuideVaishnavi DeolekarNo ratings yet

- Ratio Analysis Classification of Ratios: The Above Classification Further Grouped IntoDocument5 pagesRatio Analysis Classification of Ratios: The Above Classification Further Grouped IntoWaqar AmjadNo ratings yet

- Ratio Analysis.Document3 pagesRatio Analysis.রুবাইয়াত নিবিড়No ratings yet

- Theoretical PerspectiveDocument12 pagesTheoretical PerspectivepopliyogeshanilNo ratings yet

- Classification of RatiosDocument25 pagesClassification of RatiosAnonymous XZ376GGmNo ratings yet

- Tata Motors.: Liquidity RatiosDocument11 pagesTata Motors.: Liquidity RatiosAamir ShadNo ratings yet

- Assignment On: Financial Statement Analysis FIN 4218Document28 pagesAssignment On: Financial Statement Analysis FIN 4218নাফিস ইকবাল আকিলNo ratings yet

- Liquidity and Working Capital Analysis ToolsDocument48 pagesLiquidity and Working Capital Analysis ToolsMisratul AiniNo ratings yet

- Assignment Liquidity Vs ProfitabilityDocument14 pagesAssignment Liquidity Vs Profitabilityrihan198780% (5)

- LiquidityDocument5 pagesLiquidityMobin ShaleeNo ratings yet

- Analyze Financial Ratios to Measure LiquidityDocument17 pagesAnalyze Financial Ratios to Measure LiquidityNancy DsouzaNo ratings yet

- Understanding Liquidity & Leverage RatiosDocument2 pagesUnderstanding Liquidity & Leverage RatiosphoebjaetanNo ratings yet

- Investopedia - Financial Ratio TutorialDocument55 pagesInvestopedia - Financial Ratio TutorialKoh See Hui RoxanneNo ratings yet

- Liquidity Ratio-Is Used To Determine A Company's Ability To Pay Its Short-Term Debt ObligationsDocument3 pagesLiquidity Ratio-Is Used To Determine A Company's Ability To Pay Its Short-Term Debt Obligationsjeshelle annNo ratings yet

- How To Analyse Stock Using Simple RatioDocument31 pagesHow To Analyse Stock Using Simple RatioKrishnamoorthy SubramaniamNo ratings yet

- 5 AbcDocument3 pages5 AbcMohammed ThousifNo ratings yet

- Venkatesh ProjectDocument61 pagesVenkatesh ProjectAnonymous 0MQ3zR100% (1)

- Financial RatioDocument69 pagesFinancial RatioSwaroop VarmaNo ratings yet

- Literature Review on Financial Ratio AnalysisDocument10 pagesLiterature Review on Financial Ratio AnalysisLaarnie PantinoNo ratings yet

- (FM121) Assessment 1Document3 pages(FM121) Assessment 1cmpaguntalanNo ratings yet

- Ratio Analysis PROJECTDocument25 pagesRatio Analysis PROJECTimrataNo ratings yet

- Federal Reserve Bank: 'Flow of Funds - FOF'Document3 pagesFederal Reserve Bank: 'Flow of Funds - FOF'Ridskiee VivanggNo ratings yet

- Financial Ratio AnalysisDocument21 pagesFinancial Ratio AnalysisVaibhav Trivedi0% (1)

- Liquidity Risk ManagementDocument4 pagesLiquidity Risk Managementzaheer shahzadNo ratings yet

- Financial RatiosDocument1 pageFinancial RatiosNneka OkwuosaNo ratings yet

- Ratio Analysis of The Balance SheetDocument14 pagesRatio Analysis of The Balance SheetAtif KhosoNo ratings yet

- Solvency Ratios: Solvency Ratios Come in A Variety of FormsDocument3 pagesSolvency Ratios: Solvency Ratios Come in A Variety of FormssanskritiNo ratings yet

- Financial Ratios Topic (MFP 1) PDFDocument9 pagesFinancial Ratios Topic (MFP 1) PDFsrinivasa annamayyaNo ratings yet

- Hibernation 201013 063815 PDFDocument3 pagesHibernation 201013 063815 PDFskylarNo ratings yet

- Operating Cash Flow RatioDocument3 pagesOperating Cash Flow RatioskylarNo ratings yet

- Price To Book RatioDocument4 pagesPrice To Book RatioskylarNo ratings yet

- Key RatioDocument2 pagesKey RatioskylarNo ratings yet

- Price To Cash Flow RatioDocument2 pagesPrice To Cash Flow RatioskylarNo ratings yet

- Adamantium 201013 064225 PDFDocument5 pagesAdamantium 201013 064225 PDFskylarNo ratings yet

- United States Response To COVIDDocument4 pagesUnited States Response To COVIDskylarNo ratings yet

- NetProfitRatiosAnalysis 201013 064547Document2 pagesNetProfitRatiosAnalysis 201013 064547skylarNo ratings yet

- Vibranium 201013 064031 PDFDocument3 pagesVibranium 201013 064031 PDFskylarNo ratings yet

- Ratio Analysis TypesDocument2 pagesRatio Analysis TypesSara AbidNo ratings yet

- Japan Response To COVIDDocument2 pagesJapan Response To COVIDskylarNo ratings yet

- China Response To CovidDocument3 pagesChina Response To CovidskylarNo ratings yet

- Germany Response To COVIDDocument2 pagesGermany Response To COVIDskylarNo ratings yet

- European Union Response To COVIDDocument2 pagesEuropean Union Response To COVIDskylarNo ratings yet

- Overview of Hedge FundsDocument3 pagesOverview of Hedge FundsskylarNo ratings yet

- REP - Rural Engagement ProgramDocument2 pagesREP - Rural Engagement ProgramskylarNo ratings yet

- Emergent Phase of BurnDocument15 pagesEmergent Phase of BurnskylarNo ratings yet

- What is an investment? Understanding investments and key conceptsDocument2 pagesWhat is an investment? Understanding investments and key conceptsskylarNo ratings yet

- Ranking Using DEADocument20 pagesRanking Using DEAskylarNo ratings yet

- AMPL LearningDocument5 pagesAMPL LearningskylarNo ratings yet

- Main Study AnalysisDocument13 pagesMain Study AnalysisskylarNo ratings yet

- Acqualisa: 1. Is This A Good Product?Document39 pagesAcqualisa: 1. Is This A Good Product?Sirsha PattanayakNo ratings yet

- A Guidance Framework For Developing and Implementing Vulnerability ManagementDocument4 pagesA Guidance Framework For Developing and Implementing Vulnerability ManagementL CaroliNo ratings yet

- Punjab Rubber ProductDocument9 pagesPunjab Rubber ProductSohail GhakkarNo ratings yet

- HRM Chapter 5Document19 pagesHRM Chapter 5Rajat ManandharNo ratings yet

- Bending The Curve Tv+Digital VideoDocument8 pagesBending The Curve Tv+Digital VideoCarolina GutierrezNo ratings yet

- An Overview of PRANDocument18 pagesAn Overview of PRANMd.Shariful IslamNo ratings yet

- Foreign Direct Investment Theory and StrategyDocument28 pagesForeign Direct Investment Theory and Strategyshivakumar N50% (2)

- 4 PlanningDocument3 pages4 Planningnaeem_whdNo ratings yet

- Info Sheet Assessing RiskDocument5 pagesInfo Sheet Assessing RiskalkalkiaNo ratings yet

- HP Supply Chain ManagmentDocument25 pagesHP Supply Chain ManagmentEr Pradip Patel100% (1)

- II 2022 06 Baena-Rojas CanoDocument11 pagesII 2022 06 Baena-Rojas CanoSebastian GaonaNo ratings yet

- Office Communication and Interpersonal SkillsDocument6 pagesOffice Communication and Interpersonal SkillsRanjan MayanglambamNo ratings yet

- Ferrell Hirt Ferrell: A Changing WorldDocument36 pagesFerrell Hirt Ferrell: A Changing WorldYogha IndraNo ratings yet

- Tranfer PricingDocument36 pagesTranfer PricingSrikrishna DharNo ratings yet

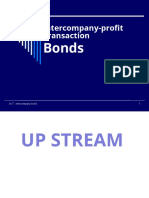

- Transaksi Interperusahaan - Obligasi UpstreamDocument11 pagesTransaksi Interperusahaan - Obligasi UpstreaminugNo ratings yet

- Department of Agrarian Reform: "Gil" de Los ReyesDocument10 pagesDepartment of Agrarian Reform: "Gil" de Los ReyesGNCDWNo ratings yet

- Who Is Director?Document20 pagesWho Is Director?Pankaj KhindriaNo ratings yet

- Strategic Partnership Development & Industry Analysis - WheatDocument11 pagesStrategic Partnership Development & Industry Analysis - WheatAnshika SinghNo ratings yet

- Effective Job Analysis: Fundamentals of Human Resource Management, 10/E, Decenzo/RobbinsDocument24 pagesEffective Job Analysis: Fundamentals of Human Resource Management, 10/E, Decenzo/RobbinsFarhana MituNo ratings yet

- Oblicon 12 - Contracts CH 2 Notes PDFDocument7 pagesOblicon 12 - Contracts CH 2 Notes PDFJoy LuNo ratings yet

- Indian Institute of Management Udaipur: Master of Business Administration 2020-22Document3 pagesIndian Institute of Management Udaipur: Master of Business Administration 2020-22Aishwarya OgreyNo ratings yet

- HRM Case Study GodrejDocument8 pagesHRM Case Study GodrejRashi RamolaNo ratings yet

- Calculating interest rate risk using duration gap analysisDocument14 pagesCalculating interest rate risk using duration gap analysissushant ahujaNo ratings yet