You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Public Enterprises:: Issues and Challenges With The Philippines' Public Corporate SectorDocument12 pagesPublic Enterprises:: Issues and Challenges With The Philippines' Public Corporate SectorRomel Torres100% (7)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- UFA Orange Book CompleteDocument212 pagesUFA Orange Book CompleteThe Estimator67% (3)

- MKT406 Assignment 1Document2 pagesMKT406 Assignment 1Neha ReddyNo ratings yet

- NEW PROSPECTUS Bsba-Human Resource MangementDocument2 pagesNEW PROSPECTUS Bsba-Human Resource MangementMikail YuNo ratings yet

- Đề thi thử Lần 5.2020Document6 pagesĐề thi thử Lần 5.2020Hoa ĐỗNo ratings yet

- Enterance ExamDocument4 pagesEnterance Examtagay mengeshaNo ratings yet

- RFBT 2 Worksheet No. 3: PRESENT Forms of PartnershipDocument7 pagesRFBT 2 Worksheet No. 3: PRESENT Forms of PartnershipCharena BandulaNo ratings yet

- Exotic Options: D.Pradeep Kumar Exe-MBA, IIPM, HydDocument21 pagesExotic Options: D.Pradeep Kumar Exe-MBA, IIPM, Hydpradeep3673No ratings yet

- Chapter 26 Acctg For Derivatives Hedging Transactions Part 3 Afar Part 2Document13 pagesChapter 26 Acctg For Derivatives Hedging Transactions Part 3 Afar Part 2Kathrina Roxas100% (1)

- Procedure For Fresh Application DLC 17032022Document11 pagesProcedure For Fresh Application DLC 17032022surajit jatiNo ratings yet

- At Aud001Document4 pagesAt Aud001KathleenNo ratings yet

- The Business Case For Employees Health and Wellbeing: A Report Prepared For Investors in People UKDocument36 pagesThe Business Case For Employees Health and Wellbeing: A Report Prepared For Investors in People UKHafsaNo ratings yet

- Marking Criteria Infographics Assignment1Document2 pagesMarking Criteria Infographics Assignment1John JohnNo ratings yet

- EH Students Essays Subjects 2022Document5 pagesEH Students Essays Subjects 2022Алтынгуль ЕрежеповаNo ratings yet

- Handbook PMBDocument188 pagesHandbook PMBgsakthivel2008No ratings yet

- Maricalum Mining Corp. vs. FlorentinodocxDocument6 pagesMaricalum Mining Corp. vs. FlorentinodocxMichelle Marie TablizoNo ratings yet

- Analisis Pembebanan Biaya Overhead Terhadap Harga Jual Waroeng Ibu Noeng Di BekasiDocument6 pagesAnalisis Pembebanan Biaya Overhead Terhadap Harga Jual Waroeng Ibu Noeng Di BekasiMaulana AmriNo ratings yet

- Judges CredentialsDocument2 pagesJudges CredentialsJERWIN SAMSONNo ratings yet

- Digital Marketing For Farm Equipment Companies - 4 TacticsDocument13 pagesDigital Marketing For Farm Equipment Companies - 4 TacticsSanat KumbharNo ratings yet

- Startup Valuation Formulas - Quantic - EduDocument11 pagesStartup Valuation Formulas - Quantic - EduAnibal MauricioNo ratings yet

- Assignment Managerial EconomicsDocument2 pagesAssignment Managerial EconomicsdanigeletaNo ratings yet

- Kampar Creditor Update 31.07.2021Document5,271 pagesKampar Creditor Update 31.07.2021gracious pharmacy 2No ratings yet

- Ebay Millionaire Secrets PDFDocument44 pagesEbay Millionaire Secrets PDFPragmaticu25% (4)

- Mechanical Engineering Syllabus Kurukshetra UniversityDocument22 pagesMechanical Engineering Syllabus Kurukshetra Universityjasvindersinghsaggu100% (1)

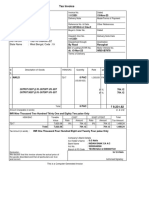

- Tax Invoice: 34 Rath Danga Road Ranaghat Gstin/Uin: 19BYRPS9845M1ZZ State Name: West Bengal, Code: 19Document1 pageTax Invoice: 34 Rath Danga Road Ranaghat Gstin/Uin: 19BYRPS9845M1ZZ State Name: West Bengal, Code: 19Online tally guideNo ratings yet

- Villanueva v. SantosDocument3 pagesVillanueva v. SantosJose Edmundo DayotNo ratings yet

- Shaft or DeclineDocument10 pagesShaft or DeclineTamani MoyoNo ratings yet

- 2021-01-27 Tegus Former-Senior-Business-Development-Advisor-at-Alibaba-GroupDocument7 pages2021-01-27 Tegus Former-Senior-Business-Development-Advisor-at-Alibaba-GroupDDNo ratings yet

- AgBus 8 BUSINESS PLAN 11Document15 pagesAgBus 8 BUSINESS PLAN 11MrAce MendozaNo ratings yet

- IT Governance Is Killing InnovationDocument5 pagesIT Governance Is Killing InnovationDEPLAPRES SUBDIPRESNo ratings yet