You might also like

- Financial Markets and Investments: Modern Portfolio Theory Session No. III 1.0Document9 pagesFinancial Markets and Investments: Modern Portfolio Theory Session No. III 1.0Lipika haldarNo ratings yet

- Week 3 Tutorials - PDF PDFDocument9 pagesWeek 3 Tutorials - PDF PDFDaniel NgoNo ratings yet

- 2012 - 1st ExamDocument3 pages2012 - 1st ExamcataNo ratings yet

- Tutorial 3 Efficient Diversification Chapter 6Document7 pagesTutorial 3 Efficient Diversification Chapter 6Noah Maratua ResortNo ratings yet

- Corporate Finance European Edition 2nd Edition Hillier Solutions ManualDocument30 pagesCorporate Finance European Edition 2nd Edition Hillier Solutions Manualthuyhai3a656100% (31)

- Assignment 2Document3 pagesAssignment 2Gabriel PodolskyNo ratings yet

- BKM CH 07 Answers W CFADocument14 pagesBKM CH 07 Answers W CFAGhulam Hassan100% (5)

- Efficient DiversificationDocument40 pagesEfficient DiversificationKoon Sing ChanNo ratings yet

- Aps502h1 20209 6316201532472020Document4 pagesAps502h1 20209 6316201532472020HannaNo ratings yet

- 4 - Problem - Set FRM - PS PDFDocument3 pages4 - Problem - Set FRM - PS PDFValentin IsNo ratings yet

- ps3 2010Document6 pagesps3 2010Ives LeeNo ratings yet

- A 109 SMDocument39 pagesA 109 SMRam Krishna KrishNo ratings yet

- 1 19Document8 pages1 19Yilei RenNo ratings yet

- Chapter 7: Optimal Risky Portfolios: Problem SetsDocument13 pagesChapter 7: Optimal Risky Portfolios: Problem SetsBiloni KadakiaNo ratings yet

- Econ 252 Spring 2011 Problem Set 2Document5 pagesEcon 252 Spring 2011 Problem Set 2Tu ShirotaNo ratings yet

- Risk and Return - Capital Marketing TheoryDocument19 pagesRisk and Return - Capital Marketing TheoryKEZIAH REVE B. RODRIGUEZNo ratings yet

- Advanced Portfolio Management: A Quant's Guide for Fundamental InvestorsFrom EverandAdvanced Portfolio Management: A Quant's Guide for Fundamental InvestorsNo ratings yet

- Assignment1 2020 PDFDocument8 pagesAssignment1 2020 PDFmonalNo ratings yet

- 2011 - 1st ExamDocument10 pages2011 - 1st ExamcataNo ratings yet

- Assig 2Document7 pagesAssig 2Katie CookNo ratings yet

- Asset ValuationDocument3 pagesAsset ValuationHassanRana0% (1)

- Handout FIN F313Document5 pagesHandout FIN F313Shubham JainNo ratings yet

- Chap 7 Bodie 9eDocument13 pagesChap 7 Bodie 9eChristan LambertNo ratings yet

- Bkm9e Answers Chap007Document12 pagesBkm9e Answers Chap007AhmadYaseenNo ratings yet

- HASC402 Financial Economics Assignment 1 Solutions FinDocument14 pagesHASC402 Financial Economics Assignment 1 Solutions FinVelaphi MudzikiNo ratings yet

- CH 11 Home Work - 05-01-2024Document2 pagesCH 11 Home Work - 05-01-2024besanwail367No ratings yet

- Tutorial 6: Chap 7 Efficient Diversification: The Following Data Apply To Problem 4 Through 10: A Pension Fund Manager IsDocument4 pagesTutorial 6: Chap 7 Efficient Diversification: The Following Data Apply To Problem 4 Through 10: A Pension Fund Manager IsLim Xiaopei100% (1)

- Integrated Case Merril Finch IncDocument10 pagesIntegrated Case Merril Finch IncEmman DtrtNo ratings yet

- Problem Set 1Document3 pagesProblem Set 1ikramraya0No ratings yet

- 2018 Exam Ifm Sample Questions PDFDocument89 pages2018 Exam Ifm Sample Questions PDFSujith GopinathanNo ratings yet

- FM 8th Edition Chapter 12 - Risk and ReturnDocument20 pagesFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoNo ratings yet

- Chapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnDocument9 pagesChapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnBiloni KadakiaNo ratings yet

- The Benefits of Diversification: Portfolio Construction & SelectionDocument25 pagesThe Benefits of Diversification: Portfolio Construction & Selectionastro9jyotish9asim9mNo ratings yet

- Session 5-6 PORTFOLIO CONSTRUCTION - SELECTIONDocument65 pagesSession 5-6 PORTFOLIO CONSTRUCTION - SELECTIONastro9jyotish9asim9mNo ratings yet

- Chap 10 Bodie 9eDocument9 pagesChap 10 Bodie 9eCatherine WuNo ratings yet

- ECMC49F Midterm Solution 2Document13 pagesECMC49F Midterm Solution 2Wissal RiyaniNo ratings yet

- Complet J M1eg Uef1 M24451ac GaumontDocument4 pagesComplet J M1eg Uef1 M24451ac GaumontNoel RaharinantenainaNo ratings yet

- Lab2-2 Portfolio Formation ModelDocument4 pagesLab2-2 Portfolio Formation ModelHarneet ChughNo ratings yet

- LECTURE 5b - Advances On Portfolio ManagementDocument36 pagesLECTURE 5b - Advances On Portfolio ManagementKim Hương Hoàng ThịNo ratings yet

- Efficient FrontierDocument7 pagesEfficient Frontierdubuli123No ratings yet

- Minicase-1 1Document1 pageMinicase-1 1JudWintonNo ratings yet

- Introduction To Risk and Return: Principles of Corporate FinanceDocument30 pagesIntroduction To Risk and Return: Principles of Corporate FinancechooisinNo ratings yet

- In The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingDocument62 pagesIn The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingRahmat M JayaatmadjaNo ratings yet

- Lecture # 6: Optimal Risky PortfolioDocument36 pagesLecture # 6: Optimal Risky PortfolioNguyễn VânNo ratings yet

- Chap 5-Pages-45-46,63-119Document59 pagesChap 5-Pages-45-46,63-119RITZ BROWNNo ratings yet

- Portfolio RiskDocument24 pagesPortfolio RiskABC DEFNo ratings yet

- Risk and Rates of Return CH06 PDFDocument16 pagesRisk and Rates of Return CH06 PDFLily DaniaNo ratings yet

- CML Vs SMLDocument9 pagesCML Vs SMLJoanna JacksonNo ratings yet

- Examination Paper Portfolio TheoryDocument5 pagesExamination Paper Portfolio TheoryApeksha netlizNo ratings yet

- Ch. 7, Problem 2: Which of The Properties of Real Estate Returns Affect Portfolio Risk?Document15 pagesCh. 7, Problem 2: Which of The Properties of Real Estate Returns Affect Portfolio Risk?RickNo ratings yet

- Chapter 2Document61 pagesChapter 2Meseret HailemichaelNo ratings yet

- RISK AND RETURN: Portfolio Theory and Asset Pricing Models - Chapter 5Document62 pagesRISK AND RETURN: Portfolio Theory and Asset Pricing Models - Chapter 5RabinNo ratings yet

- Can Tail Risk Hedging Be ProfitableDocument14 pagesCan Tail Risk Hedging Be Profitablejpaslowski1No ratings yet

- Sy CH - 3Document12 pagesSy CH - 3Rafayeat Hasan MehediNo ratings yet

- Ac.f215 Exam 2018-2019 PDFDocument6 pagesAc.f215 Exam 2018-2019 PDFWilliam NogueraNo ratings yet

- Return and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)Document52 pagesReturn and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)anna_alwanNo ratings yet

- BANK3011 Workshop Week 5 SolutionsDocument3 pagesBANK3011 Workshop Week 5 SolutionsZahraaNo ratings yet

- Strategic Risk Management: Designing Portfolios and Managing RiskFrom EverandStrategic Risk Management: Designing Portfolios and Managing RiskNo ratings yet

- Pcab LlimDocument634 pagesPcab LlimPankaj RaneNo ratings yet

- 03 Caso Swimmer Headphone (REV MAX)Document9 pages03 Caso Swimmer Headphone (REV MAX)Jorge Andres GutierrezNo ratings yet

- Duration 2 Hours Max Marks 70Document25 pagesDuration 2 Hours Max Marks 70AgANo ratings yet

- Netscape ProformaDocument6 pagesNetscape ProformabobscribdNo ratings yet

- Fin Model of Hydro Power PlantDocument7 pagesFin Model of Hydro Power PlantVivek SinghalNo ratings yet

- Admission of A New Partner: Total AssetsDocument10 pagesAdmission of A New Partner: Total AssetsJuliana Cheng100% (5)

- Accounting Module 1 AnswerDocument6 pagesAccounting Module 1 AnswerMariel Mae MoralesNo ratings yet

- Amortization Pattern Check Reconciliation: Andreea Lungu-Tranole Alexandra-Elena DrugaDocument15 pagesAmortization Pattern Check Reconciliation: Andreea Lungu-Tranole Alexandra-Elena DrugaAdrian StefanescuNo ratings yet

- Ind AS 113Document31 pagesInd AS 113rajan tiwariNo ratings yet

- Part A & BDocument6 pagesPart A & BRiya PrajapatiNo ratings yet

- ContentsDocument12 pagesContentsGhierainne SalvadorNo ratings yet

- AAAA Final ProgramDocument10 pagesAAAA Final ProgramShahifol Arbi IsmailNo ratings yet

- Hmcost3e SM Ch19Document32 pagesHmcost3e SM Ch19jhouvan100% (1)

- Error DiscussionDocument2 pagesError DiscussionGloria Beltran100% (1)

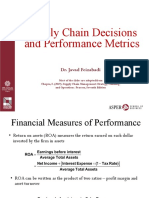

- 3-Supply Chain Decisions and Performance Metrics (A)Document21 pages3-Supply Chain Decisions and Performance Metrics (A)eeman kNo ratings yet

- Bus 5111 Financial Management Written Assignment Unit 7Document5 pagesBus 5111 Financial Management Written Assignment Unit 7Andika GintingNo ratings yet

- FundroomDocument6 pagesFundroomTalib KhanNo ratings yet

- Chapter 9 - Accounting Cycle of A Service BusinessDocument15 pagesChapter 9 - Accounting Cycle of A Service Businessgeyb away0% (1)

- 05 Investment PropertyDocument39 pages05 Investment Property林義哲No ratings yet

- Case Study 3 - EditedDocument8 pagesCase Study 3 - EditedSVPSNo ratings yet

- Stock Analysis Excel Revised March 2017Document26 pagesStock Analysis Excel Revised March 2017Sangram Panda100% (1)

- My Watchlist - Value ResearchDocument1 pageMy Watchlist - Value ResearchpksNo ratings yet

- Chapter 6 VocabDocument7 pagesChapter 6 VocabBrian MartinNo ratings yet

- Home Office Books Branch Books: Pro-FormaDocument8 pagesHome Office Books Branch Books: Pro-FormaMarianeNo ratings yet

- Time Value of Money: TVM, Risk and ReturnDocument11 pagesTime Value of Money: TVM, Risk and ReturnKath LeynesNo ratings yet

- Colgate - 10 Year DataDocument10 pagesColgate - 10 Year DataAmal RoyNo ratings yet

- Bank Reconciliation StatementsDocument7 pagesBank Reconciliation StatementsLeon ElblingNo ratings yet

- Engro Fertilizer - Financial AnalysisDocument16 pagesEngro Fertilizer - Financial AnalysisHasan AshrafNo ratings yet

- Forms of Business Organisation EOBDocument2 pagesForms of Business Organisation EOBmisha003No ratings yet

- Q1 - LK Konsolidasian PT Garuda Metalindo TBK Q1-2018Document89 pagesQ1 - LK Konsolidasian PT Garuda Metalindo TBK Q1-2018RISMA NAJWA KIRANINo ratings yet