You might also like

- Fasten Case AnalysisDocument7 pagesFasten Case AnalysisSam Dhuri33% (3)

- Marketing Plan ATTDocument17 pagesMarketing Plan ATTDora Wan100% (1)

- Hot Wheel Case Analysis - VikasDocument9 pagesHot Wheel Case Analysis - VikasVikas MotwaniNo ratings yet

- Cloudstrat Case StudyDocument10 pagesCloudstrat Case StudyAbhirami PromodNo ratings yet

- Westlake Lanes Case Analysis - EditedDocument5 pagesWestlake Lanes Case Analysis - EditedAditya DashNo ratings yet

- Case Study Analysis: Voice War: Hey Google Vs Alexa Vs Siri Case SummaryDocument4 pagesCase Study Analysis: Voice War: Hey Google Vs Alexa Vs Siri Case SummaryRuhi chandelNo ratings yet

- A CASE STUDY ON SERVICE MANDI (Princy)Document4 pagesA CASE STUDY ON SERVICE MANDI (Princy)Amruta ChavanNo ratings yet

- BUSINESS and INDUSTRIAL ECONOMICS ASSDocument1 pageBUSINESS and INDUSTRIAL ECONOMICS ASSAlessandra GuidoNo ratings yet

- Marvel Case SolutionsDocument3 pagesMarvel Case Solutionsmayur7894No ratings yet

- BigbasketDocument1 pageBigbasketKritikaNo ratings yet

- Kuestermann Megan Case Greg James at SunDocument5 pagesKuestermann Megan Case Greg James at SunAdil Huseyin HeymunNo ratings yet

- Airbus SWOT AnalysisDocument4 pagesAirbus SWOT AnalysisTameem NadeemNo ratings yet

- Assignment Apple'S Iphone in India Ringing in New FortunesDocument3 pagesAssignment Apple'S Iphone in India Ringing in New FortunesAditya ShettyNo ratings yet

- Big Data at GAP - Group 6 - Section ADocument9 pagesBig Data at GAP - Group 6 - Section AARKO MUKHERJEE100% (1)

- This Study Resource WasDocument3 pagesThis Study Resource WasHanishaNo ratings yet

- Dr4000procedures ManualDocument1,004 pagesDr4000procedures ManualedgarseveniNo ratings yet

- Assignment Case 1 - Alexa: A Pandora's Box of RisksDocument3 pagesAssignment Case 1 - Alexa: A Pandora's Box of RisksBibari BoroNo ratings yet

- Purple Innovation, Inc: The Online To Offline Marketing ChallengeDocument3 pagesPurple Innovation, Inc: The Online To Offline Marketing ChallengeAnoushka BhatiaNo ratings yet

- Marcopolo:: The Making of A Global LatinaDocument3 pagesMarcopolo:: The Making of A Global LatinaShachin Shibi100% (2)

- Group - 6 MobileyeDocument14 pagesGroup - 6 MobileyevNo ratings yet

- Group3 La Presse CaseDocument4 pagesGroup3 La Presse CaseRanjith RoshanNo ratings yet

- 2016 01 1720161144casoDocument4 pages2016 01 1720161144casoGiselli Castillo Gárate0% (1)

- VOLKSWAGEN INDIA - Group 11Document4 pagesVOLKSWAGEN INDIA - Group 11Shubham PariharNo ratings yet

- Case StudyDocument6 pagesCase StudyXZJFUHNo ratings yet

- L'Oréal of Paris: Bringing "Class To Mass" With PlénitudeDocument30 pagesL'Oréal of Paris: Bringing "Class To Mass" With Plénitudeariefakbar100% (6)

- Artificial Intelligence & Marketing: Anujk@iima - Ac.inDocument6 pagesArtificial Intelligence & Marketing: Anujk@iima - Ac.inKartik MittalNo ratings yet

- CARCRIS Case AnalysisDocument8 pagesCARCRIS Case AnalysismsbinuNo ratings yet

- Clean Hands in Dirty Business Case AnalysisDocument4 pagesClean Hands in Dirty Business Case AnalysisSam Dhuri100% (1)

- Case STPD NiveaDocument6 pagesCase STPD NiveaSam DhuriNo ratings yet

- Apple Case A1Document3 pagesApple Case A1Nishtha GargNo ratings yet

- FinalDocument17 pagesFinalParveNo ratings yet

- DGIS SiemensDocument3 pagesDGIS SiemensJuhee PritanjaliNo ratings yet

- GAP Case Study SolutionsDocument2 pagesGAP Case Study SolutionsAditya HonguntiNo ratings yet

- Online Marketing at Big Skinny: Submitted by Group - 6Document2 pagesOnline Marketing at Big Skinny: Submitted by Group - 6Saumadeep GuharayNo ratings yet

- IMC - Magellan BoatworksDocument12 pagesIMC - Magellan Boatworksaniket verma100% (2)

- The O. M. Scott & Sons CompanyDocument4 pagesThe O. M. Scott & Sons Companycarolina120209100% (1)

- LedgerDocument1 pageLedgervinay jaiswalNo ratings yet

- B2B - Group 3 - Jackson Case StudyDocument5 pagesB2B - Group 3 - Jackson Case Studyriya agrawallaNo ratings yet

- GE Health Care Case: Executive SummaryDocument4 pagesGE Health Care Case: Executive SummarykpraneethkNo ratings yet

- Jabong CaseDocument23 pagesJabong CaseSatish GuraddiNo ratings yet

- Predicting Consumer With Big Data at GAPDocument10 pagesPredicting Consumer With Big Data at GAPNhư NgọcNo ratings yet

- Reversing The AMD Fusion Launch (Case Study)Document6 pagesReversing The AMD Fusion Launch (Case Study)SanyamRajvanshiNo ratings yet

- Uttam Kumar Sec-A Dividend Policy Linear TechnologyDocument11 pagesUttam Kumar Sec-A Dividend Policy Linear TechnologyUttam Kumar100% (1)

- Q1. GE's Industrial Internet Initiative Was Necessary and Valuable Given GE Was Able ToDocument1 pageQ1. GE's Industrial Internet Initiative Was Necessary and Valuable Given GE Was Able ToishaNo ratings yet

- NTT Docomo Case StudyDocument4 pagesNTT Docomo Case StudyLy Nguyen LeNo ratings yet

- Investment Banking: Individual Assignment 2Document5 pagesInvestment Banking: Individual Assignment 2Aakash Ladha100% (3)

- Gillette Dry Idea (B)Document3 pagesGillette Dry Idea (B)Anosh DoodhmalNo ratings yet

- OM Foldrite 1Document9 pagesOM Foldrite 1Rohit Kiran0% (1)

- GE Case Study Team AkbarDocument12 pagesGE Case Study Team AkbarLakshya AnandNo ratings yet

- Digital MatrixDocument2 pagesDigital MatrixKeshavNo ratings yet

- Building A Backdoor To The IphoneDocument2 pagesBuilding A Backdoor To The IphoneAngga EkhariedoNo ratings yet

- Polaroid Corporation Case Solution Final PDFDocument8 pagesPolaroid Corporation Case Solution Final PDFNovel ArianNo ratings yet

- Lifebuoy Case StudyDocument4 pagesLifebuoy Case StudyRitika GautamNo ratings yet

- Netscape Initial Public OfferingDocument1 pageNetscape Initial Public Offeringaruncec2001No ratings yet

- Gathering Data: Advertisem EntDocument7 pagesGathering Data: Advertisem EntLilitNo ratings yet

- Oberoi Hotels: Train Whistle in The Tiger Reserve: Assignment Case ReportDocument7 pagesOberoi Hotels: Train Whistle in The Tiger Reserve: Assignment Case ReportJyotsna JeswaniNo ratings yet

- Apple Inc. in 2012: SolutionDocument5 pagesApple Inc. in 2012: Solutionnish_d1100% (2)

- CASE Kent Chemical - DiscussionDocument3 pagesCASE Kent Chemical - DiscussionBoryana StamenovaNo ratings yet

- CASE STUDY Godrej Assingnment AnswersDocument2 pagesCASE STUDY Godrej Assingnment AnswersNiveditaNo ratings yet

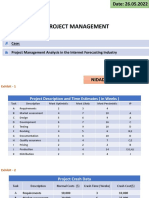

- Project Management Analysis in The Internet Forecasting IndustryDocument14 pagesProject Management Analysis in The Internet Forecasting IndustryNiranjan NidadavoluNo ratings yet

- Porters 5 Forces: Industry: Automation VehiclesDocument3 pagesPorters 5 Forces: Industry: Automation VehiclesSam DhuriNo ratings yet

- PGP37235 BDC Assignment 4Document1 pagePGP37235 BDC Assignment 4mavin avengersNo ratings yet

- Case Study-4 EcommerceDocument2 pagesCase Study-4 EcommerceAnaadilNo ratings yet

- Group 8Document3 pagesGroup 8Parth Hemant PurandareNo ratings yet

- Project Finance 1 Network of Contracts PDFDocument41 pagesProject Finance 1 Network of Contracts PDFSam DhuriNo ratings yet

- The Syndication Process: Week 2Document26 pagesThe Syndication Process: Week 2Sam DhuriNo ratings yet

- Financial SustainabilityDocument33 pagesFinancial SustainabilitySam DhuriNo ratings yet

- Capital Budgeting For Infra InvestmentDocument41 pagesCapital Budgeting For Infra InvestmentSam DhuriNo ratings yet

- Bonollo Energia CaseDocument10 pagesBonollo Energia CaseSam DhuriNo ratings yet

- Porters 5 Forces: Industry: Automation VehiclesDocument3 pagesPorters 5 Forces: Industry: Automation VehiclesSam DhuriNo ratings yet

- Compaq - Group 7 AnalysisDocument1 pageCompaq - Group 7 AnalysisSam DhuriNo ratings yet

- A Journey From Being Stooges To Leaders: 6 Wise Men: The BeginningDocument2 pagesA Journey From Being Stooges To Leaders: 6 Wise Men: The BeginningSam DhuriNo ratings yet

- Circular Economy HUL TechtonicDocument1 pageCircular Economy HUL TechtonicSam DhuriNo ratings yet

- Bajaj Atom Pitch NMIMSDocument1 pageBajaj Atom Pitch NMIMSSam DhuriNo ratings yet

- Quikr: Unlocking The Value of Used Goods MarketDocument3 pagesQuikr: Unlocking The Value of Used Goods MarketSam DhuriNo ratings yet

- Script-Consumer LawDocument4 pagesScript-Consumer LawSam DhuriNo ratings yet

- AC Report PDFDocument20 pagesAC Report PDFSam DhuriNo ratings yet

- TAB Report - Group7Document10 pagesTAB Report - Group7Sam DhuriNo ratings yet

- Prodect Commercialisation PlanDocument1 pageProdect Commercialisation PlanSam DhuriNo ratings yet

- Fasten Case AnalysisDocument3 pagesFasten Case AnalysisSam DhuriNo ratings yet

- Consumer LawDocument25 pagesConsumer LawSam DhuriNo ratings yet

- Marketing ManagementDocument7 pagesMarketing ManagementSam DhuriNo ratings yet

- Hacienda Luisita vs. Presidential Agrarian Reform CouncilDocument74 pagesHacienda Luisita vs. Presidential Agrarian Reform CouncilJoyce VillanuevaNo ratings yet

- CE 111 Finals AnswerDocument20 pagesCE 111 Finals AnswerJulie BajadoNo ratings yet

- Final Programme of High Level International ConferenceDocument16 pagesFinal Programme of High Level International ConferencekranosgrNo ratings yet

- ContourDocument15 pagesContourkaran ahariNo ratings yet

- 6.1 Monthly Report - March 2023 - Perway Emergency Slope StabilityDocument22 pages6.1 Monthly Report - March 2023 - Perway Emergency Slope StabilityJeanri RustNo ratings yet

- Modal AnalysisDocument21 pagesModal AnalysisemreNo ratings yet

- Katalog STAG Akcesoria ENDocument32 pagesKatalog STAG Akcesoria ENBELLO SAIFULLAHINo ratings yet

- FW-V20 NivomerDocument8 pagesFW-V20 NivomersxasxNo ratings yet

- Libel CasesDocument21 pagesLibel Casesgp_ph86No ratings yet

- Manila Mining Corporation v. AmorDocument2 pagesManila Mining Corporation v. AmorFaye Cience Bohol100% (1)

- Service ManualDocument142 pagesService ManualPrashanthNo ratings yet

- S Setting Value, C Check Value) OT Outside Tolerance (X Is Set)Document3 pagesS Setting Value, C Check Value) OT Outside Tolerance (X Is Set)Agus WijayadiNo ratings yet

- Definition of EncumbranceDocument3 pagesDefinition of EncumbranceamvronaNo ratings yet

- SzlendakGryniewicz-FEMmodel Diaphragmactioneffectsv 0 95Document9 pagesSzlendakGryniewicz-FEMmodel Diaphragmactioneffectsv 0 95Ivan BurtovoyNo ratings yet

- Geography Sba GuideDocument3 pagesGeography Sba GuideKareem WignallNo ratings yet

- Quick Sizer Guide For SAPDocument76 pagesQuick Sizer Guide For SAPpkv001No ratings yet

- WOMEN EMPOWERMENT MCQs UNIT - IIDocument13 pagesWOMEN EMPOWERMENT MCQs UNIT - IIRohit Choudhary 2100% (12)

- Sentinel Event Notification and Management Policy Final20227484Document19 pagesSentinel Event Notification and Management Policy Final20227484ahamedsahibNo ratings yet

- An Overview of IEEE Software Engineering Standards and Knowledge ProductsDocument46 pagesAn Overview of IEEE Software Engineering Standards and Knowledge ProductsNava GrahazNo ratings yet

- SM-800.11 TypeM Plus ValvesDocument13 pagesSM-800.11 TypeM Plus ValvesAdel AhmedNo ratings yet

- DBU Final First YearDocument2 pagesDBU Final First YeargagimarkenNo ratings yet

- 30 Theories of RetailDocument30 pages30 Theories of RetailDrparul Khanna0% (1)

- Paramount Insurance Corp VsDocument2 pagesParamount Insurance Corp VsJL A H-DimaculanganNo ratings yet

- 7 Check Points by Sourcing Warrior 1Document12 pages7 Check Points by Sourcing Warrior 1Chrystom joyeNo ratings yet

- Creative Accounting Full EditDocument11 pagesCreative Accounting Full EditHabib MohdNo ratings yet

- Automotive Tire Information System Market - Global Industry Analysis, Size, Share, Growth, Trends, and Forecast - Facts and TrendsDocument3 pagesAutomotive Tire Information System Market - Global Industry Analysis, Size, Share, Growth, Trends, and Forecast - Facts and Trendssurendra choudharyNo ratings yet

- The Girl From Ipanema PDFDocument2 pagesThe Girl From Ipanema PDFCRM LUIS DUNCKER LAVALLENo ratings yet

- Ministry of Higher Education and HighwaysDocument5 pagesMinistry of Higher Education and HighwaysIreshani JayatungaNo ratings yet

- LinkedIn Guys Profile ChecklistDocument17 pagesLinkedIn Guys Profile ChecklistYasir Khan RasheediNo ratings yet