You might also like

- BM414 Financial Decision Making 40Document15 pagesBM414 Financial Decision Making 40MD. SHAKIL100% (1)

- Chapter Thirteen SolutionsDocument18 pagesChapter Thirteen Solutionsapi-3705855No ratings yet

- Tax SecretsDocument3 pagesTax Secretshrpufnstuf100% (10)

- Questions & Answers: 2 SalariesDocument26 pagesQuestions & Answers: 2 SalariesSabyasachi Ghosh67% (3)

- MP2 FAQ April15Document3 pagesMP2 FAQ April15rieann09No ratings yet

- Cat Module 1 Answer KeysDocument27 pagesCat Module 1 Answer KeysLexden MendozaNo ratings yet

- Lecture 1 and Lecture 2 Quiz Answer Section: Ramon Magsaysay Memorial CollegesDocument6 pagesLecture 1 and Lecture 2 Quiz Answer Section: Ramon Magsaysay Memorial Collegesbelinda dagohoyNo ratings yet

- Obn - Gwox - Issue 34 (March 2021)Document1 pageObn - Gwox - Issue 34 (March 2021)Nate TobikNo ratings yet

- Instructions For Form 1099-B: Future DevelopmentsDocument12 pagesInstructions For Form 1099-B: Future DevelopmentsScott Homuth100% (1)

- FINA 4221 Corporate Finance Problem Set 1Document2 pagesFINA 4221 Corporate Finance Problem Set 1mahirahmed510% (1)

- Annual Compensation and Business TaxesDocument21 pagesAnnual Compensation and Business TaxesRyDNo ratings yet

- f6vnm 2007 Dec ADocument6 pagesf6vnm 2007 Dec APhạm Hùng DũngNo ratings yet

- M12 Tax ActivityDocument6 pagesM12 Tax ActivityJanna RodriguezNo ratings yet

- Fabm2 Q2 W4 5Document8 pagesFabm2 Q2 W4 5maeesotoNo ratings yet

- CAF 06 - TaxationDocument7 pagesCAF 06 - TaxationKhurram ShahzadNo ratings yet

- SSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077Document29 pagesSSF Not Listed-Monthly Salary Sheet With TDS Calculation 2076-2077samNo ratings yet

- PSBA REFRESHER TAXATION QUIZDocument10 pagesPSBA REFRESHER TAXATION QUIZEdnalyn CruzNo ratings yet

- Dit Sem V SolnDocument10 pagesDit Sem V Solnmaaz11052020No ratings yet

- I. Sources of Fund A. EquityDocument20 pagesI. Sources of Fund A. EquityJoshell Roz RamasNo ratings yet

- FABM 2 Module 9 Income Tax DueDocument11 pagesFABM 2 Module 9 Income Tax DueJOHN PAUL LAGAO100% (1)

- Problems On Individual Taxation AY 2020-21 StudentsDocument9 pagesProblems On Individual Taxation AY 2020-21 StudentsAminul Islam RubelNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- Islamic Banking - Profit Calculation On Deposits Home AssignmentDocument1 pageIslamic Banking - Profit Calculation On Deposits Home AssignmentSyed Qasim GhaniNo ratings yet

- TM PQsDocument9 pagesTM PQsAnooshayNo ratings yet

- BUS 142 - Exercises CH 11Document10 pagesBUS 142 - Exercises CH 11Jess IcaNo ratings yet

- Calculating PAYE (Pay As You Earn) : Please Read Page 10 - 11 of The Student ManualDocument3 pagesCalculating PAYE (Pay As You Earn) : Please Read Page 10 - 11 of The Student Manualjadeaa54345No ratings yet

- Review Questions For Final Exam ACC210Document13 pagesReview Questions For Final Exam ACC210AaaNo ratings yet

- DBH Finance PLC.: Current Month (BDT) Cumulative (BDT) ParticularsDocument1 pageDBH Finance PLC.: Current Month (BDT) Cumulative (BDT) ParticularsHossainmoajjemNo ratings yet

- Lagrimas, Sarah Nicole S. - PC&OL PART 2Document3 pagesLagrimas, Sarah Nicole S. - PC&OL PART 2Sarah Nicole S. LagrimasNo ratings yet

- Intermediate Accounting 3: PROBLEM 1-11Document3 pagesIntermediate Accounting 3: PROBLEM 1-11Gemmalyn JulatonNo ratings yet

- Assignment 4 - SolutionsDocument2 pagesAssignment 4 - SolutionsstoryNo ratings yet

- Calculating Present Value of Restructured NoteDocument5 pagesCalculating Present Value of Restructured NoteClarisse AnnNo ratings yet

- MMW - Activity 7Document2 pagesMMW - Activity 7Hazel TanongNo ratings yet

- Tutanes, Ma. Angelita 3BAM5ADocument2 pagesTutanes, Ma. Angelita 3BAM5AMaxGel De VeraNo ratings yet

- Income From Salaries: Rs. Rs. Rs. SCH - NoDocument3 pagesIncome From Salaries: Rs. Rs. Rs. SCH - NoBilalNo ratings yet

- Questions & Answers - Salary IncomeDocument14 pagesQuestions & Answers - Salary IncomeKiran BendeNo ratings yet

- Accrued Liability Asnwer KeyDocument4 pagesAccrued Liability Asnwer KeyNecitas Cortez PanuganNo ratings yet

- Tax On CompensationDocument26 pagesTax On Compensationtyrone inocenteNo ratings yet

- Eva StatisticsDocument3 pagesEva StatisticsBaron Mumo MuiaNo ratings yet

- Latihan Soal Chapter 21 - Yoga Cipta Nugraha - 1181002067 - Sesi 12Document7 pagesLatihan Soal Chapter 21 - Yoga Cipta Nugraha - 1181002067 - Sesi 12Yoga Cipta NugrahaNo ratings yet

- M 14 IPCC Taxation Guideline AnswersDocument14 pagesM 14 IPCC Taxation Guideline Answerssantosh barkiNo ratings yet

- Alinaz Spa and Beauty7374Document10 pagesAlinaz Spa and Beauty7374Mallik DCNo ratings yet

- NVC FinanceDocument4 pagesNVC FinanceĐặng Hồng NhungNo ratings yet

- Self Employed Tax ContributionDocument4 pagesSelf Employed Tax ContributionLe-Noi AndersonNo ratings yet

- (Answers) R1 20200924153547prl3 - Final - ExamDocument21 pages(Answers) R1 20200924153547prl3 - Final - ExamArslan HafeezNo ratings yet

- Income Statement For The Year Ended, December, 31, 2016: Pt. ZaliaDocument4 pagesIncome Statement For The Year Ended, December, 31, 2016: Pt. ZaliaNofi Nurlaila0% (1)

- Appendix D Accounting For Deferred Income TaxesDocument2 pagesAppendix D Accounting For Deferred Income TaxesLan Hương Trần ThịNo ratings yet

- Template 2 Task 3 Calculation Worksheet - BSBFIM601Document17 pagesTemplate 2 Task 3 Calculation Worksheet - BSBFIM601Writing Experts0% (1)

- Prelim Topic 1 2ansDocument6 pagesPrelim Topic 1 2ansKenneth Forro TorresNo ratings yet

- Salary IllustrationDocument10 pagesSalary IllustrationSarvar Pathan100% (1)

- Impusto A La Renta 2022 P. N. V Cat.Document18 pagesImpusto A La Renta 2022 P. N. V Cat.STEFANIA ANGGIE ALVAREZ SILESNo ratings yet

- 2021 - FM Past Paper SolutionDocument3 pages2021 - FM Past Paper SolutionInox HassanNo ratings yet

- DO IT Salary Income With SolutionDocument3 pagesDO IT Salary Income With SolutionAnsary LabibNo ratings yet

- Government Grant ActivitiesDocument5 pagesGovernment Grant Activitiesjoong wanNo ratings yet

- Cash Management: Sale of EquipmentDocument4 pagesCash Management: Sale of EquipmentjohnNo ratings yet

- Manny Company: Required: Compute For The Balances of The Following On December 31, 2X14Document4 pagesManny Company: Required: Compute For The Balances of The Following On December 31, 2X14MauiNo ratings yet

- Government Rank and File Employee Summary of Compensation and Benefits in 2020Document4 pagesGovernment Rank and File Employee Summary of Compensation and Benefits in 2020kate bautistaNo ratings yet

- Year 2021 2022 2023 2024 2025 Opening Balance Projected Cash Flow StatementDocument1 pageYear 2021 2022 2023 2024 2025 Opening Balance Projected Cash Flow StatementLailanie NuñezNo ratings yet

- Ca Ipcc Taxation Guideline Answer For May 2016 ExamDocument8 pagesCa Ipcc Taxation Guideline Answer For May 2016 Examileshrathod0No ratings yet

- 2015 Annual Accomplishment ReportDocument8 pages2015 Annual Accomplishment ReportAngelica Aquino GasmenNo ratings yet

- Casibang OEDocument2 pagesCasibang OEKrung KrungNo ratings yet

- Sample FsDocument3 pagesSample FsLocel Maquiran LamosteNo ratings yet

- Paper 4Document16 pagesPaper 4Kali KhannaNo ratings yet

- MT Test Review-Taxation 1-Win 2024Document4 pagesMT Test Review-Taxation 1-Win 2024Mariola AlkuNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Truth in Lending NotesDocument2 pagesTruth in Lending NotesRyDNo ratings yet

- Philippine Competition Act NotesDocument5 pagesPhilippine Competition Act NotesRyDNo ratings yet

- Truth in Lending Portfolio RequirementDocument1 pageTruth in Lending Portfolio RequirementRyDNo ratings yet

- DPA Portfolio RequirementDocument1 pageDPA Portfolio RequirementRyDNo ratings yet

- AMLA NotesDocument5 pagesAMLA NotesRyDNo ratings yet

- Bank Secrecy Law NotesDocument3 pagesBank Secrecy Law NotesRyDNo ratings yet

- Bank Secrecy Law Portfolio RequirementDocument1 pageBank Secrecy Law Portfolio RequirementRyDNo ratings yet

- Truth in Lending Portfolio RequirementDocument1 pageTruth in Lending Portfolio RequirementRyDNo ratings yet

- 01 PdicDocument51 pages01 PdicRyDNo ratings yet

- Bouncing Checks Portfolio RequirementDocument1 pageBouncing Checks Portfolio RequirementRyDNo ratings yet

- HOW TO CALCULATE THE NUMBER OF BASKETS A WEAVER CAN FINISH IN A WEEK USING FRACTIONS, DECIMALS AND PERCENTAGESDocument9 pagesHOW TO CALCULATE THE NUMBER OF BASKETS A WEAVER CAN FINISH IN A WEEK USING FRACTIONS, DECIMALS AND PERCENTAGESRyDNo ratings yet

- PDIC NotesDocument5 pagesPDIC NotesRyDNo ratings yet

- Quizzer On Withholding of Monthly Tax Compensation IncomeDocument10 pagesQuizzer On Withholding of Monthly Tax Compensation IncomeRyDNo ratings yet

- PDIC Portfolio RequirementDocument1 pagePDIC Portfolio RequirementRyDNo ratings yet

- Illustrative Problem On Adjusted Bank MethodDocument15 pagesIllustrative Problem On Adjusted Bank MethodRyDNo ratings yet

- Withholding Tax On Monthly Compensation IncomeDocument11 pagesWithholding Tax On Monthly Compensation IncomeRyDNo ratings yet

- Notes in Judicial Department (Philippine Constitution)Document19 pagesNotes in Judicial Department (Philippine Constitution)RyD100% (1)

- Discussion On FractionsDocument9 pagesDiscussion On FractionsRyDNo ratings yet

- VAT BackgroundDocument6 pagesVAT BackgroundRyDNo ratings yet

- How to determine VATDocument5 pagesHow to determine VATRyDNo ratings yet

- Withholding Tax On Annual Compensation IncomeDocument7 pagesWithholding Tax On Annual Compensation IncomeRyDNo ratings yet

- Notes in Executive Department (Philippine Constitution)Document14 pagesNotes in Executive Department (Philippine Constitution)RyDNo ratings yet

- Compensation IncomeDocument21 pagesCompensation IncomeRyDNo ratings yet

- Three Powers of TaxationDocument24 pagesThree Powers of TaxationRyDNo ratings yet

- Notes in Writ of Habeas Data (Philippine Law)Document5 pagesNotes in Writ of Habeas Data (Philippine Law)RyDNo ratings yet

- Legislative Dept Powers & LimitsDocument20 pagesLegislative Dept Powers & LimitsRyDNo ratings yet

- Notes in Writ of Amparo (Philippine Law)Document13 pagesNotes in Writ of Amparo (Philippine Law)RyDNo ratings yet

- Anti Money Laundering Act (Philippine Law)Document11 pagesAnti Money Laundering Act (Philippine Law)RyDNo ratings yet

- Accounting Textbook Solutions - 50Document19 pagesAccounting Textbook Solutions - 50acc-expertNo ratings yet

- Bab 3 (Inggris)Document21 pagesBab 3 (Inggris)Nadira Fadhila HudaNo ratings yet

- APTC form-40-A-GPFDocument2 pagesAPTC form-40-A-GPFvijay_dilse100% (1)

- Shabnam Ahuja - JanDocument2 pagesShabnam Ahuja - JanLove LoveNo ratings yet

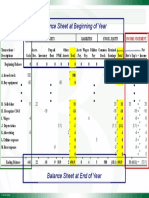

- Balance Sheet at Beginning of Year: Cash FlowDocument1 pageBalance Sheet at Beginning of Year: Cash FlowluisNo ratings yet

- Team Energy Corporation Vs CIRDocument3 pagesTeam Energy Corporation Vs CIRMark Gilverton Buenconsejo Ignacio67% (3)

- Financial Management Strategy-MBA-731: Work-SheetDocument8 pagesFinancial Management Strategy-MBA-731: Work-SheetEyuael SolomonNo ratings yet

- McqsDocument2 pagesMcqsMuhammad AhmedNo ratings yet

- Ratio-rate-speed-G 7Document2 pagesRatio-rate-speed-G 7tripti aggarwalNo ratings yet

- Chapter 18 Part 1Document61 pagesChapter 18 Part 1Hannah KatNo ratings yet

- Incremental Analysis: Summary of Questions by Objectives and Bloom'S Taxonomy True-False StatementsDocument43 pagesIncremental Analysis: Summary of Questions by Objectives and Bloom'S Taxonomy True-False StatementsMarcus MonocayNo ratings yet

- Labor Exercise - Cost AccountingDocument3 pagesLabor Exercise - Cost AccountingKolins ChakmaNo ratings yet

- Irem Vol IiDocument67 pagesIrem Vol IiVeera ChaitanyaNo ratings yet

- Problems in TAX Collection in PakistanDocument20 pagesProblems in TAX Collection in PakistanAmjad HussainNo ratings yet

- Corporate Reporting Paper 3.1march 2023Document28 pagesCorporate Reporting Paper 3.1march 2023JAMAN SOUTH MUNICIPAL HEALTH DIRECTORATENo ratings yet

- Accounting For Manufacturing OperationsDocument49 pagesAccounting For Manufacturing Operationsgab mNo ratings yet

- Reviewer-IN-FAR - Lecture Notes Financial Accounting and Reporting 1-10 Reviewer-IN-FAR - Lecture Notes Financial Accounting and Reporting 1-10Document4 pagesReviewer-IN-FAR - Lecture Notes Financial Accounting and Reporting 1-10 Reviewer-IN-FAR - Lecture Notes Financial Accounting and Reporting 1-10Jocelyn TejerosNo ratings yet

- Debt Restructuring SummaryDocument5 pagesDebt Restructuring SummaryLady PilaNo ratings yet

- Multiple Choice - Problems Part 1: A. Percentage TaxDocument8 pagesMultiple Choice - Problems Part 1: A. Percentage TaxheyheyNo ratings yet

- Bba 407 - Management AccountingDocument10 pagesBba 407 - Management AccountingSimanta KalitaNo ratings yet

- Akuntansi 1Document1 pageAkuntansi 1Bintang FitriNo ratings yet

- Korbel Foundation College Inc.: (Messenger)Document2 pagesKorbel Foundation College Inc.: (Messenger)Jeanmay CalseñaNo ratings yet

- Cost AccountingDocument122 pagesCost Accountingkaran kNo ratings yet

- Lesson 1 Working Capital MGTDocument6 pagesLesson 1 Working Capital MGTklipordNo ratings yet

- Final Exam Preparation Auditing II: Condition Yang Terjadi Dan Mempengaruhi Akun-Akun Sebelum TanggalDocument5 pagesFinal Exam Preparation Auditing II: Condition Yang Terjadi Dan Mempengaruhi Akun-Akun Sebelum TanggalAlvira FajriNo ratings yet