You might also like

- Income Taxation of Individuals: Citizens: Resident Non-Residents CitizensDocument2 pagesIncome Taxation of Individuals: Citizens: Resident Non-Residents CitizenshellomynameisNo ratings yet

- 2016 Tax Aid Classification of TaxpayersDocument4 pages2016 Tax Aid Classification of TaxpayersDewm DewmNo ratings yet

- Income Tax TableDocument14 pagesIncome Tax TableDanielle Sophia GardunoNo ratings yet

- 6 11 18 Tax Summary in The Philippines EditedDocument117 pages6 11 18 Tax Summary in The Philippines EditedBianca PalomaNo ratings yet

- Income Tax On IndividualsDocument7 pagesIncome Tax On IndividualsThe man with a Square stacheNo ratings yet

- Taxation 1 NotesDocument15 pagesTaxation 1 NotesTricia SandovalNo ratings yet

- Personal Income Taxation 1Document29 pagesPersonal Income Taxation 1Rovic OrdonioNo ratings yet

- Tax Code: Partnerships' Are Partnerships Formed by Persons For TheDocument10 pagesTax Code: Partnerships' Are Partnerships Formed by Persons For Thegabriel omliNo ratings yet

- Individual Income TaxDocument9 pagesIndividual Income TaxCharmaine RosalesNo ratings yet

- Income Tax On Individuals PDFDocument20 pagesIncome Tax On Individuals PDFKaren Joy MagsayoNo ratings yet

- Bar TaxDocument29 pagesBar TaxMaisie ZabalaNo ratings yet

- Income Tax On Individuals - Ust PDFDocument15 pagesIncome Tax On Individuals - Ust PDFKana Lou Cassandra Besana100% (1)

- Individual Taxpayers Handouts and ProblemsDocument15 pagesIndividual Taxpayers Handouts and ProblemsLovely De CastroNo ratings yet

- Taxation Chapter Explains Individual Income Tax RatesDocument31 pagesTaxation Chapter Explains Individual Income Tax RatesDerick Ocampo FulgencioNo ratings yet

- Person - Orporation: Income TaxDocument223 pagesPerson - Orporation: Income TaxMich FelloneNo ratings yet

- Income Tax Guide for IndividualsDocument141 pagesIncome Tax Guide for Individualsrav dano100% (2)

- Classification of TaxpayerDocument2 pagesClassification of TaxpayerEduard Morelos100% (1)

- SEC. 23. General Principles of Income Taxation in The Philippines. - Except WhenDocument11 pagesSEC. 23. General Principles of Income Taxation in The Philippines. - Except WhenMiguel BerguNo ratings yet

- Differences between schedular and global tax systemsDocument18 pagesDifferences between schedular and global tax systemsElaine Yap100% (1)

- TAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S ADocument12 pagesTAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S AVaughn TheoNo ratings yet

- TSN By: Adil, Flores, Orquina, Dura-Butaslac, Tan, Besin From The Lecture of Atty. AbrantesDocument31 pagesTSN By: Adil, Flores, Orquina, Dura-Butaslac, Tan, Besin From The Lecture of Atty. AbrantesEmma PaglalaNo ratings yet

- Tax ChartsDocument33 pagesTax ChartsDavid TanNo ratings yet

- TaxInd P1Document25 pagesTaxInd P1Rael RaelNo ratings yet

- Person - Orporation: Income TaxDocument138 pagesPerson - Orporation: Income TaxMich FelloneNo ratings yet

- Tax 601Document11 pagesTax 601C.J. Clarisse FranciscoNo ratings yet

- Tax Rates and Classifications for Individual Filipino TaxpayersDocument3 pagesTax Rates and Classifications for Individual Filipino TaxpayersOdessa De JesusNo ratings yet

- PDF Taxation 1 NotesDocument24 pagesPDF Taxation 1 NotesLeuNo ratings yet

- Chapter 2 InctaxDocument14 pagesChapter 2 InctaxLiRose SmithNo ratings yet

- Classification of TaxpayerDocument2 pagesClassification of Taxpayerhannahmousa83% (24)

- Income TaxationDocument21 pagesIncome TaxationUbalda AbuboNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- Income Tax Rules for IndividualsDocument7 pagesIncome Tax Rules for IndividualsEmperiumNo ratings yet

- 2nd Semester Income Taxation Module 5 Classification of TaxpayersDocument5 pages2nd Semester Income Taxation Module 5 Classification of TaxpayersMaryrose SumulongNo ratings yet

- Taxation of IndividualsDocument6 pagesTaxation of IndividualsLyca V100% (1)

- Classification of Individual TaxpayersDocument18 pagesClassification of Individual TaxpayersChristine Bernadette PagalNo ratings yet

- Unit III A. IndividualsDocument31 pagesUnit III A. IndividualsBea BernardoNo ratings yet

- Unit III A. IndividualsDocument32 pagesUnit III A. IndividualsJay GoNo ratings yet

- Tax CompiledDocument379 pagesTax Compiledlayla scotNo ratings yet

- TAX Notes AdditionalDocument18 pagesTAX Notes AdditionalJoben Vernan CuencaNo ratings yet

- Income Taxation: Income Tax For IndividualsDocument8 pagesIncome Taxation: Income Tax For IndividualsJohnnoff Bagacina0% (1)

- Taxation Income TaxationDocument73 pagesTaxation Income TaxationB-an Javelosa0% (1)

- PreFi Tax PDFDocument21 pagesPreFi Tax PDFJoesil Dianne SempronNo ratings yet

- Income Taxation Midterm ReviewerDocument16 pagesIncome Taxation Midterm ReviewerRAMIREZ, MARVIN L.No ratings yet

- Quickie PreFi Tax PDFDocument12 pagesQuickie PreFi Tax PDFJoesil Dianne Sempron100% (1)

- Income Tax Reviewer GuideDocument6 pagesIncome Tax Reviewer GuideAnne KimNo ratings yet

- Income Taxation - Key Concepts and PrinciplesDocument20 pagesIncome Taxation - Key Concepts and PrinciplesArt MelancholiaNo ratings yet

- Types of Individual Taxpayers Citizens Revenue Regulations No. 1-79Document8 pagesTypes of Individual Taxpayers Citizens Revenue Regulations No. 1-79James Evan I. ObnamiaNo ratings yet

- HO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Document5 pagesHO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Erine ContranoNo ratings yet

- IBAÑEZ Present Income Tax SystemDocument74 pagesIBAÑEZ Present Income Tax SystemJasmine Montero-GaribayNo ratings yet

- Tax Reviewer by MoiDocument4 pagesTax Reviewer by MoiKenny BesarioNo ratings yet

- Tax601 Individual Itx Lecture Notes 122Document12 pagesTax601 Individual Itx Lecture Notes 122Justine JaymaNo ratings yet

- Income Tax Prelims.Document13 pagesIncome Tax Prelims.Amber Lavarias BernabeNo ratings yet

- Over But Not OverDocument2 pagesOver But Not OverSherrizah Ferrer MaribbayNo ratings yet

- Produced The Income)Document4 pagesProduced The Income)bluesNo ratings yet

- Assignment No. 4Document7 pagesAssignment No. 4HannahPauleneDimaanoNo ratings yet

- University of St. Lasalle: Student HandoutsDocument13 pagesUniversity of St. Lasalle: Student HandoutsMae EscanillanNo ratings yet

- Canadian International Taxation: Income Tax Rules for ResidentsFrom EverandCanadian International Taxation: Income Tax Rules for ResidentsNo ratings yet

- TRIGGER WARNING: Graphic Description of DeathDocument5 pagesTRIGGER WARNING: Graphic Description of DeathJul A.No ratings yet

- 77 Cruz v. Sun HolidaysDocument2 pages77 Cruz v. Sun HolidaysJul A.No ratings yet

- 70 Home Insurance Co. v. American Steamship AgenciesDocument2 pages70 Home Insurance Co. v. American Steamship AgenciesJul A.No ratings yet

- 80 Asia Lighterage and Shipping V CADocument2 pages80 Asia Lighterage and Shipping V CAAnn Julienne AristozaNo ratings yet

- 78 Schmitz Transport - Brokerage Corporation V Transport VentureDocument3 pages78 Schmitz Transport - Brokerage Corporation V Transport VentureJul A.No ratings yet

- 72 BASCOS v. CADocument3 pages72 BASCOS v. CAJul A.No ratings yet

- Caravan Travel's negligence disputeDocument3 pagesCaravan Travel's negligence disputeJul A.No ratings yet

- III. Common Carriers - A.1. Definitions, Essential Elements, B. LiberalDocument3 pagesIII. Common Carriers - A.1. Definitions, Essential Elements, B. LiberalJul A.No ratings yet

- Kabit System - An Arrangement Whereby A Person Who Has Been Granted ADocument2 pagesKabit System - An Arrangement Whereby A Person Who Has Been Granted AJul A.No ratings yet

- 59 Baliwag Transit Inc V CA and MartinezDocument3 pages59 Baliwag Transit Inc V CA and MartinezJul A.No ratings yet

- LARA V. VALENCIADocument3 pagesLARA V. VALENCIAJul A.No ratings yet

- 62 PCI Leasing v. UCPB InsuranceDocument2 pages62 PCI Leasing v. UCPB InsuranceJul A.No ratings yet

- Cabil Was Grossly Negligent.: Respondents Are CA, WWCF, and Several of The Injured PassengersDocument3 pagesCabil Was Grossly Negligent.: Respondents Are CA, WWCF, and Several of The Injured PassengersJul A.No ratings yet

- 73 Planters Products, Inc. v. CADocument5 pages73 Planters Products, Inc. v. CAJul A.No ratings yet

- 56 Lita Enterprises, Inc. v. Second Civil Cases Division, 129 SCRA 79Document2 pages56 Lita Enterprises, Inc. v. Second Civil Cases Division, 129 SCRA 79Jul A.No ratings yet

- 58 Santos V SibugDocument3 pages58 Santos V SibugJul A.No ratings yet

- RTC ruling ignores cross-claimDocument2 pagesRTC ruling ignores cross-claimJul A.No ratings yet

- 58 Santos V SibugDocument3 pages58 Santos V SibugJul A.No ratings yet

- 55 Batangas Transportation v. OrlanesDocument3 pages55 Batangas Transportation v. OrlanesJul A.No ratings yet

- 57 Teja v. IACDocument2 pages57 Teja v. IACJul A.No ratings yet

- 54 SAN PABLO v. PANTRANCODocument3 pages54 SAN PABLO v. PANTRANCOJul A.No ratings yet

- 52 Cogeo-Cubao Operator - Driver Association v. Court of AppealsDocument3 pages52 Cogeo-Cubao Operator - Driver Association v. Court of AppealsJul A.100% (1)

- ERC jurisdiction over Meralco refund caseDocument2 pagesERC jurisdiction over Meralco refund caseJul A.No ratings yet

- 47 Gerochi v. Department of EnergyDocument3 pages47 Gerochi v. Department of EnergyJul A.100% (1)

- 51 Raymundo v. Luneta MotorDocument2 pages51 Raymundo v. Luneta MotorJul A.No ratings yet

- G.R. No. 88404 - October 18, 1990 - Melencio-Herrera, J.: (48) PLDT v. NTC, SupraDocument4 pagesG.R. No. 88404 - October 18, 1990 - Melencio-Herrera, J.: (48) PLDT v. NTC, SupraJul A.No ratings yet

- 50 Taxicab Operators of Metro Manila v. Board of TransportationDocument2 pages50 Taxicab Operators of Metro Manila v. Board of TransportationJul A.No ratings yet

- 53 1-UTAK v. COMELECDocument4 pages53 1-UTAK v. COMELECJul A.No ratings yet

- 53 1-UTAK v. COMELECDocument4 pages53 1-UTAK v. COMELECJul A.No ratings yet

- 54 MERALCO v. ERB (NOT in Revised Syllabus)Document3 pages54 MERALCO v. ERB (NOT in Revised Syllabus)Jul A.No ratings yet

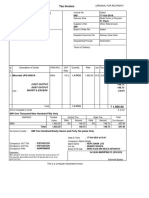

- Tax InvoiceDocument1 pageTax InvoiceSuraj KumarNo ratings yet

- TAX-801 (Sources of Income)Document2 pagesTAX-801 (Sources of Income)lyndon delfinNo ratings yet

- Tax SyllabusDocument3 pagesTax SyllabusTalhakgsNo ratings yet

- 2015 ITAD - BIR - Ruling - No. - 335 1520210622 12 19ad6s6Document4 pages2015 ITAD - BIR - Ruling - No. - 335 1520210622 12 19ad6s6rian.lee.b.tiangcoNo ratings yet

- Wagner's Law and the Evolution of Public SpendingDocument13 pagesWagner's Law and the Evolution of Public Spendingilove2shopNo ratings yet

- HIRVJIAYDocument1 pageHIRVJIAYArtish PadaiyaNo ratings yet

- Central Region July 2020 Salary Statement for Education WorkerDocument1 pageCentral Region July 2020 Salary Statement for Education WorkerJONAS BAAHNo ratings yet

- PIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityDocument1 pagePIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityPeter Osundwa KitekiNo ratings yet

- Corporate Income Tax: Section A - Multiple Choice QuestionsDocument36 pagesCorporate Income Tax: Section A - Multiple Choice QuestionsWanda NguyenNo ratings yet

- CBDT Clarifies Doubts On Account of New TCS Provisions - Taxguru - inDocument2 pagesCBDT Clarifies Doubts On Account of New TCS Provisions - Taxguru - inVivek AgarwalNo ratings yet

- UPS BillDocument2 pagesUPS Billmack100% (1)

- Paper F6 Revision ProformasDocument12 pagesPaper F6 Revision ProformasShristee ReetunNo ratings yet

- 2550m April 2019 - LGSLDocument3 pages2550m April 2019 - LGSLexergyNo ratings yet

- Computation Details: Ali Hassan M. Lucman Jr. Hermeno A. PalamineDocument1 pageComputation Details: Ali Hassan M. Lucman Jr. Hermeno A. PalamineKobi SaibenNo ratings yet

- Income Deemed To Arise in IndiaDocument7 pagesIncome Deemed To Arise in IndiaDebaNo ratings yet

- Job Aid For Form 1701-OfflineDocument20 pagesJob Aid For Form 1701-OfflineRozen Jake Domingo ValenaNo ratings yet

- Calamba Steel Center Inc Vs CIR GR151857Document17 pagesCalamba Steel Center Inc Vs CIR GR151857AnonymousNo ratings yet

- Myob - Chart of AccountsDocument4 pagesMyob - Chart of AccountsAr RaziNo ratings yet

- Assessment of Tax Collection Problems On Business (A Case Study On Sokoru Woreda)Document39 pagesAssessment of Tax Collection Problems On Business (A Case Study On Sokoru Woreda)NigatuNo ratings yet

- 06 VAT Compliance-RequirementsDocument2 pages06 VAT Compliance-RequirementsJaneLayugCabacungan100% (1)

- Fiscal Policy: Expansionary Fiscal Policy When The Government Spend More Then It Receives in Order ToDocument2 pagesFiscal Policy: Expansionary Fiscal Policy When The Government Spend More Then It Receives in Order TominhaxxNo ratings yet

- Hcm trg uk_py_master dataDocument4 pagesHcm trg uk_py_master dataAditya DeshpandeNo ratings yet

- Kepco Philippines v. CIR tax refund denialDocument4 pagesKepco Philippines v. CIR tax refund denialamareia yapNo ratings yet

- Idt - GSTDocument35 pagesIdt - GSTArush KothariNo ratings yet

- EY Young Tax Professional Wins AwardDocument5 pagesEY Young Tax Professional Wins AwardXiaxun OngNo ratings yet

- Analisis Perpajakan Terhadap Bentuk Usaha Tetap Berbasis Layanan AplikasiDocument23 pagesAnalisis Perpajakan Terhadap Bentuk Usaha Tetap Berbasis Layanan AplikasiNidha NianNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House PropertyPraveen EkkaNo ratings yet

- Expansionary & Contractionary Fiscal PolicyDocument4 pagesExpansionary & Contractionary Fiscal PolicyShwetabh SrivastavaNo ratings yet

- Tax 4Document33 pagesTax 4Thái Minh ChâuNo ratings yet

- Chapter 1 - Fundamental Principles: TAXATION - The Process by Which The Sovereign, Through Its Law-Making BodyDocument11 pagesChapter 1 - Fundamental Principles: TAXATION - The Process by Which The Sovereign, Through Its Law-Making BodyLiRose SmithNo ratings yet