You might also like

- Sensitivity AnalysisDocument4 pagesSensitivity AnalysisMei Yi YeoNo ratings yet

- Hospital Supply Inc. - SolutionsDocument5 pagesHospital Supply Inc. - SolutionsMEERA JOSHY 192743633% (3)

- Jawaban Relevant CostDocument18 pagesJawaban Relevant CostReviandi RamadhanNo ratings yet

- Assgnment 2 (f5) 10341Document11 pagesAssgnment 2 (f5) 10341Minhaj AlbeezNo ratings yet

- Break-Even Point and Cost-Volume-Profit Analysis: QuestionsDocument34 pagesBreak-Even Point and Cost-Volume-Profit Analysis: QuestionsGuinevereNo ratings yet

- 4.basics of Marginal Costing-SN FoundationDocument22 pages4.basics of Marginal Costing-SN FoundationHasim SaiyedNo ratings yet

- Fin. Anal RafaelDocument6 pagesFin. Anal RafaelMarjonNo ratings yet

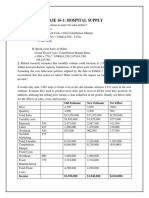

- Case 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Document6 pagesCase 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Lalit SapkaleNo ratings yet

- Latihan Akt MGT Lanjutan - Ppak Untar Genap 21-22 HTDocument18 pagesLatihan Akt MGT Lanjutan - Ppak Untar Genap 21-22 HTCalvin HadikusumaNo ratings yet

- MA and FMA Full Specimen Exam AnswersDocument14 pagesMA and FMA Full Specimen Exam AnswersLanre OdubanjoNo ratings yet

- Unit Four Tactical Decision MakingDocument21 pagesUnit Four Tactical Decision MakingDzukanji SimfukweNo ratings yet

- Week 67 and 9 Absorption Costing Vs Marginal Costing Costing MethodDocument31 pagesWeek 67 and 9 Absorption Costing Vs Marginal Costing Costing MethodMai LyNo ratings yet

- FIM PL IV Solution Dec 2019Document8 pagesFIM PL IV Solution Dec 2019Hanif Khan SrkNo ratings yet

- Variance AnalysisDocument10 pagesVariance AnalysisPalesaNo ratings yet

- Case 16-1 (Alfi & Yessy)Document4 pagesCase 16-1 (Alfi & Yessy)Ana KristianaNo ratings yet

- Variable Cost Tools: As A DecisionDocument17 pagesVariable Cost Tools: As A DecisionTusif Islam RomelNo ratings yet

- Costing TC9AD17Document10 pagesCosting TC9AD17kalowekamoNo ratings yet

- CMA May 2017 SSDocument11 pagesCMA May 2017 SSGoremushandu MungarevaniNo ratings yet

- Hospital Supply: Alternative Choice Decisions Differential CostingDocument13 pagesHospital Supply: Alternative Choice Decisions Differential Costingksandeep25No ratings yet

- Lecture 9 Managerial BIS 2022Document9 pagesLecture 9 Managerial BIS 2022nada ahmedNo ratings yet

- Managerial Accounting 14Th Edition Warren Solutions Manual Full Chapter PDFDocument67 pagesManagerial Accounting 14Th Edition Warren Solutions Manual Full Chapter PDFykydxnjk4100% (11)

- Decision MakingDocument28 pagesDecision MakingJem ColebraNo ratings yet

- Problem 8-41 1Document3 pagesProblem 8-41 1Jey JNo ratings yet

- The Model Consists of Three Elements: The Objective Function, Decision Variables and Business ConstraintsDocument18 pagesThe Model Consists of Three Elements: The Objective Function, Decision Variables and Business Constraintshomedefault 369No ratings yet

- Question 1-1-1Document14 pagesQuestion 1-1-1Aqsa AnumNo ratings yet

- Akuntansi Ratna FixxxDocument17 pagesAkuntansi Ratna Fixxxaditya muhammadNo ratings yet

- MA and FMA Full Specimen Exam Answers - 2Document14 pagesMA and FMA Full Specimen Exam Answers - 2zunndraaNo ratings yet

- Tutorial 7 (Week 9) - Managerial Accounting Concepts and Principles - Cost-Volume-Profit AnalysisDocument7 pagesTutorial 7 (Week 9) - Managerial Accounting Concepts and Principles - Cost-Volume-Profit AnalysisVincent TanNo ratings yet

- CostingDocument4 pagesCostingDatz HuynhNo ratings yet

- CH (7) Incremental Analysis (Decision Making)Document11 pagesCH (7) Incremental Analysis (Decision Making)Khaled Abo YousefNo ratings yet

- Ma2 Examreport Aug19 Sept20Document6 pagesMa2 Examreport Aug19 Sept20tashiNo ratings yet

- Cost Classification: Total Product/ ServiceDocument21 pagesCost Classification: Total Product/ ServiceThureinNo ratings yet

- Chapter 6 Lecture Slides 9eDocument44 pagesChapter 6 Lecture Slides 9ecolinmac8892No ratings yet

- Marginal Costing NotesDocument7 pagesMarginal Costing NotesJul 480weshNo ratings yet

- Exercise 2Document3 pagesExercise 2Kathy LaiNo ratings yet

- 4 Cvpbe PROB EXDocument5 pages4 Cvpbe PROB EXjulia4razoNo ratings yet

- Cost Accounting Level 3/series 4 2008 (3017)Document17 pagesCost Accounting Level 3/series 4 2008 (3017)Hein Linn Kyaw100% (1)

- CH 13Document24 pagesCH 13antonio-dublines-372150% (2)

- Hospital Supplies Inc: Presented By: Sushmita Gahlot - Bhumika AggarwalDocument14 pagesHospital Supplies Inc: Presented By: Sushmita Gahlot - Bhumika AggarwalSushmita GahlotNo ratings yet

- Study Unit 5.1Document26 pagesStudy Unit 5.1Valerie Verity MarondedzeNo ratings yet

- CH 05Document3 pagesCH 05Gus JooNo ratings yet

- Soultions - Chapter 3Document8 pagesSoultions - Chapter 3Naudia L. TurnbullNo ratings yet

- CH 13Document35 pagesCH 13billybuttonNo ratings yet

- BACC207 ASS 1 2019 Semester2Document3 pagesBACC207 ASS 1 2019 Semester2Tawanda Tatenda HerbertNo ratings yet

- Name: Student No.: Exercises For Decision MakingDocument7 pagesName: Student No.: Exercises For Decision MakingShohnura FayzulloevaNo ratings yet

- Suggested Solution To CVP TutorialDocument5 pagesSuggested Solution To CVP TutorialLiyendra FernandoNo ratings yet

- Chapter 4Document8 pagesChapter 4Châu Ánh ViNo ratings yet

- Acc 301 Week 5Document9 pagesAcc 301 Week 5Accounting GuyNo ratings yet

- Diva Rianitha Manurung R43A - 468825: E13-13 Structuring A Make-or-Buy ProblemDocument4 pagesDiva Rianitha Manurung R43A - 468825: E13-13 Structuring A Make-or-Buy ProblemDhiva Rianitha ManurungNo ratings yet

- ABC Practice Question 2 With SolutionDocument5 pagesABC Practice Question 2 With SolutionBennie KingNo ratings yet

- Chapter 8 MowenDocument25 pagesChapter 8 MowenRosamae PialaneNo ratings yet

- Chapter 7 Practice QuestionsDocument12 pagesChapter 7 Practice QuestionsZethu JoeNo ratings yet

- Taller Costeo VariablesDocument10 pagesTaller Costeo VariablesKaroll Joseph Sanchez AlmaralesNo ratings yet

- Lecture 1. Basic Costing CVPDocument14 pagesLecture 1. Basic Costing CVPTân NguyênNo ratings yet

- Advanced Management AccountingDocument14 pagesAdvanced Management AccountingZain ul AbidinNo ratings yet

- Inventory Costing & Capacity AnalysisDocument18 pagesInventory Costing & Capacity AnalysisReshu BediaNo ratings yet

- Cost-Volume-Profit Analysis (Week 7)Document8 pagesCost-Volume-Profit Analysis (Week 7)Ihuoma Onwubu ChikaNo ratings yet

- At Wid SolDocument4 pagesAt Wid SolglamfactorsalonspaNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Topic 2.2.1 Additional NotesDocument6 pagesTopic 2.2.1 Additional NotesMei Yi YeoNo ratings yet

- Topic 1.1.1 Additional NotesDocument6 pagesTopic 1.1.1 Additional NotesMei Yi YeoNo ratings yet

- Topic 1.1.1 Additional NotesDocument6 pagesTopic 1.1.1 Additional NotesMei Yi YeoNo ratings yet

- Interger and Goal ProgrammingDocument10 pagesInterger and Goal ProgrammingSyurga Fathonah100% (1)

- 1.1.1 Textbook and Addition AnswersDocument6 pages1.1.1 Textbook and Addition AnswersMei Yi YeoNo ratings yet

- 1.4.4A Limited Companies NotesDocument27 pages1.4.4A Limited Companies NotesMei Yi YeoNo ratings yet

- A Level Accounting (9706) IAS Booklet v1 0Document58 pagesA Level Accounting (9706) IAS Booklet v1 0Mei Yi YeoNo ratings yet

- 1.1.1 Textbook and Addition AnswersDocument6 pages1.1.1 Textbook and Addition AnswersMei Yi YeoNo ratings yet

- A Level Accounting (9706) IAS Booklet v1 0Document58 pagesA Level Accounting (9706) IAS Booklet v1 0Mei Yi YeoNo ratings yet

- 1.4.4A Limited Companies NotesDocument27 pages1.4.4A Limited Companies NotesMei Yi YeoNo ratings yet

- A Level Accounting (9706) IAS Booklet v1 0Document58 pagesA Level Accounting (9706) IAS Booklet v1 0Mei Yi YeoNo ratings yet

- 1.4.4A Limited Companies NotesDocument27 pages1.4.4A Limited Companies NotesMei Yi YeoNo ratings yet

- 1.1.1 Textbook and Addition AnswersDocument6 pages1.1.1 Textbook and Addition AnswersMei Yi YeoNo ratings yet

- Making The Trend Your FriendDocument4 pagesMaking The Trend Your FriendACasey101No ratings yet

- Scrambled MerchandisingDocument12 pagesScrambled MerchandisingNisha ChauhanNo ratings yet

- Financial Markets and InstitutionsDocument5 pagesFinancial Markets and InstitutionsEng Abdikarim WalhadNo ratings yet

- Explaining The Process of STP & 3P's of Marketing Perspective To Jockey IndustryDocument3 pagesExplaining The Process of STP & 3P's of Marketing Perspective To Jockey IndustrySoumadeep GuharayNo ratings yet

- Business Plan of Poultry FarmDocument4 pagesBusiness Plan of Poultry FarmDiip_Ahsan_791186% (49)

- CaseDocument4 pagesCaseRaghuveer ChandraNo ratings yet

- Chapter 17 Notes-Concepts, Homework Problems With AnswersDocument45 pagesChapter 17 Notes-Concepts, Homework Problems With Answersanilegna990% (2)

- Bonifacio Street, Davao City Bonifacio Street, Davao CityDocument1 pageBonifacio Street, Davao City Bonifacio Street, Davao CityGlee Cris S. UrbiztondoNo ratings yet

- Strategic Management Assignment: Marketing SimulationDocument13 pagesStrategic Management Assignment: Marketing SimulationMohit KumarNo ratings yet

- Marketing DynamicsDocument15 pagesMarketing DynamicsMuhammad Sajid SaeedNo ratings yet

- Facebook Ads StrategyDocument2 pagesFacebook Ads Strategyannas_ahm100% (2)

- Marketing Research Assignment: By: Neeraj DaniDocument5 pagesMarketing Research Assignment: By: Neeraj DaniNeeraj DaniNo ratings yet

- Marketing Report On Idea Cellular Ltd.Document26 pagesMarketing Report On Idea Cellular Ltd.amin pattani82% (11)

- Slip PDFDocument1 pageSlip PDFPrachi BhosaleNo ratings yet

- Chapter No.3 Research Methodology 3.1 IntroductionDocument15 pagesChapter No.3 Research Methodology 3.1 Introductionpooja shandilyaNo ratings yet

- Congress Research PowerpointDocument12 pagesCongress Research PowerpointElle SanchezNo ratings yet

- Game Theory and Competitive StrategyDocument95 pagesGame Theory and Competitive StrategyirfantoniNo ratings yet

- Capitalism and Socialism ReportDocument17 pagesCapitalism and Socialism ReportRaisen Esperanza100% (1)

- Unit I-Mefa Final NotesDocument24 pagesUnit I-Mefa Final NotesMuskan TambiNo ratings yet

- Analisis Market Segmentation Targeting Dan Positio PDFDocument16 pagesAnalisis Market Segmentation Targeting Dan Positio PDFdavidkurniawanNo ratings yet

- Lecture 6 1567834793996Document52 pagesLecture 6 1567834793996Jay ShuklaNo ratings yet

- Revealedpreferencetheory 161122184928Document11 pagesRevealedpreferencetheory 161122184928BoNo ratings yet

- Section VI: NRV Vs Fair Value: ExampleDocument5 pagesSection VI: NRV Vs Fair Value: ExamplebinuNo ratings yet

- Unit I SDMDocument76 pagesUnit I SDMChirag JainNo ratings yet

- Chap008 Location Planning & AnalysisDocument23 pagesChap008 Location Planning & Analysisnatasha_sethi_3No ratings yet

- 2015 SRC Rules Table of ContentsDocument13 pages2015 SRC Rules Table of ContentsErika delos SantosNo ratings yet

- Depository SystemDocument36 pagesDepository SystemRabia PearlNo ratings yet

- Transfer PricingDocument98 pagesTransfer PricingMAHESH JAINNo ratings yet

- Sol Man - Pas 2 InventoriesDocument3 pagesSol Man - Pas 2 InventoriesDaniella Mae ElipNo ratings yet

- Assignment 1Document5 pagesAssignment 1sabaNo ratings yet