You might also like

- Voyage EstimationDocument10 pagesVoyage EstimationMohamed Salah El DinNo ratings yet

- Financial Analysis (Detail)Document68 pagesFinancial Analysis (Detail)Paulo NascimentoNo ratings yet

- Dry Cargo CharteringDocument6 pagesDry Cargo Charteringrahul yo yoNo ratings yet

- PvsystDocument44 pagesPvsystSgfvv100% (1)

- Fuzzy Topsis CalculationDocument12 pagesFuzzy Topsis CalculationLuis Enrique LavayenNo ratings yet

- Sbi Car LoanDocument10 pagesSbi Car LoanShweta Yashwant Chalke100% (2)

- Bimco Standard Statement of Facts PDFDocument2 pagesBimco Standard Statement of Facts PDFAzlan AzlanNo ratings yet

- Vessel Laytime CalculationDocument20 pagesVessel Laytime CalculationSaikumar SelaNo ratings yet

- BPI Investment Corporation vs. Court of Appeals, 377 SCRA 117, February 15, 2002Document2 pagesBPI Investment Corporation vs. Court of Appeals, 377 SCRA 117, February 15, 2002Robinson MojicaNo ratings yet

- RMFI Software v1.00Document39 pagesRMFI Software v1.00RENJiiiNo ratings yet

- Introduction To M&A With Piramal Abbott DealDocument22 pagesIntroduction To M&A With Piramal Abbott DealSachidanand Singh100% (2)

- Comparing Projects with Unequal Lives Using Replacement Chain Method and Equivalent Annual AnnuityDocument3 pagesComparing Projects with Unequal Lives Using Replacement Chain Method and Equivalent Annual AnnuitydzazeenNo ratings yet

- SEB Commodities Monthly May 2010Document22 pagesSEB Commodities Monthly May 2010SEB GroupNo ratings yet

- Gerald CorcoranDocument9 pagesGerald CorcoranMarketsWikiNo ratings yet

- Research Speak - 16-04-2010Document12 pagesResearch Speak - 16-04-2010A_KinshukNo ratings yet

- Comunicado SSUINGLSDocument1 pageComunicado SSUINGLSMultiplan RINo ratings yet

- Mwo 121010Document10 pagesMwo 121010richardck50No ratings yet

- SEB Report: Commodity Prices To Rise in Fourth QuarterDocument20 pagesSEB Report: Commodity Prices To Rise in Fourth QuarterSEB GroupNo ratings yet

- Lanvyl TubesDocument5 pagesLanvyl TubesIshmeet SinghNo ratings yet

- Sharespost Groupon Research ReportDocument60 pagesSharespost Groupon Research ReportTechCrunchNo ratings yet

- Chemical Supply ChainDocument11 pagesChemical Supply ChainLogiChemNo ratings yet

- Global Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandsDocument16 pagesGlobal Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandslukeniaNo ratings yet

- Banking Review - Q4FY10Document26 pagesBanking Review - Q4FY10vishi.segalNo ratings yet

- Update On IDFC Arbitrage FundDocument6 pagesUpdate On IDFC Arbitrage FundGNo ratings yet

- Pakistan Fertilizer Sector Update Highlights Valuations and Growth OutlookDocument3 pagesPakistan Fertilizer Sector Update Highlights Valuations and Growth OutlookOnail AbbasNo ratings yet

- 2014 Comparing SARIMA and Holt Winter Model For Indian Automobile SectorDocument4 pages2014 Comparing SARIMA and Holt Winter Model For Indian Automobile SectorShiv PrasadNo ratings yet

- Financial Technologies (India)Document8 pagesFinancial Technologies (India)venkatesanvpmNo ratings yet

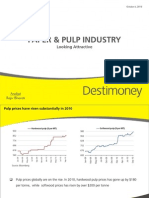

- Paper & Pulp Industry-Looking AttractiveDocument14 pagesPaper & Pulp Industry-Looking AttractiverabharatNo ratings yet

- Job Losses Since December 2007Document1 pageJob Losses Since December 2007EricFruitsNo ratings yet

- CH 7 Diminishing MusharakaDocument32 pagesCH 7 Diminishing Musharakasaadullah98.sk.skNo ratings yet

- FMG Global H1-10 AJ Version2Document10 pagesFMG Global H1-10 AJ Version2henrik_kahmNo ratings yet

- Unemployment DataDocument2 pagesUnemployment Datakettle1No ratings yet

- JPM Global Equity Multi-FactorDocument2 pagesJPM Global Equity Multi-FactorHari ChandanaNo ratings yet

- Lecture 2 Case Study McDonald's Dim Sum Bonds "Lovin' It"Document4 pagesLecture 2 Case Study McDonald's Dim Sum Bonds "Lovin' It"Simal ShaikhNo ratings yet

- Highlights: S&P/ TSX Global Gold I Ndex Gold DXY I Ndex GoldDocument19 pagesHighlights: S&P/ TSX Global Gold I Ndex Gold DXY I Ndex GoldkaiselkNo ratings yet

- Russia 2010 Worth A Tactical Look: An Investor's Guide To The Risks and Opportunities in 2010Document21 pagesRussia 2010 Worth A Tactical Look: An Investor's Guide To The Risks and Opportunities in 2010jamesdb1No ratings yet

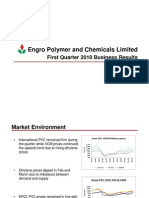

- 1Q 2010 Business ResultsDocument11 pages1Q 2010 Business ResultsmagicsohailNo ratings yet

- Lecture 1 2019Document58 pagesLecture 1 2019yitong zhangNo ratings yet

- RBI Annual Policy 2011-12 ReviewDocument2 pagesRBI Annual Policy 2011-12 ReviewclevinnashNo ratings yet

- New Microsoft Office Power Point PresentationDocument31 pagesNew Microsoft Office Power Point PresentationReshma GuptaNo ratings yet

- Presentation To Macquarie Corporate Day in Singapore & Hong KongDocument54 pagesPresentation To Macquarie Corporate Day in Singapore & Hong KongnigelburkeNo ratings yet

- What Is Really Killing The Irish EconomyDocument1 pageWhat Is Really Killing The Irish EconomyLuis Riestra Delgado100% (1)

- Short and Medium Term OutlookDocument6 pagesShort and Medium Term OutlookTushar LanjekarNo ratings yet

- Thematic - Power Sector - 2009-08-26 - Rainfall and Hydro PowerDocument5 pagesThematic - Power Sector - 2009-08-26 - Rainfall and Hydro PowerMehul MukatiNo ratings yet

- Kemajuan Fizikal SG Sat 050709Document1 pageKemajuan Fizikal SG Sat 050709wghazNo ratings yet

- Baltics RevisitedDocument12 pagesBaltics RevisitedideanoiseNo ratings yet

- 34 Birla Corp Buy For A Price Target of Rs430Document2 pages34 Birla Corp Buy For A Price Target of Rs430mamtakariraNo ratings yet

- Paper 5 Condition Assessment of Surge ArresterDocument33 pagesPaper 5 Condition Assessment of Surge ArrestertotochakrabortyNo ratings yet

- AS-AD Applications and Data InterpretationDocument2 pagesAS-AD Applications and Data Interpretationalanoud AlmheiriNo ratings yet

- ANDHRA BANK: STRONG CREDIT GROWTH OUTLOOK AND SUPERIOR ASSET QUALITY TO DRIVE EARNINGSDocument30 pagesANDHRA BANK: STRONG CREDIT GROWTH OUTLOOK AND SUPERIOR ASSET QUALITY TO DRIVE EARNINGSca.deepaktiwariNo ratings yet

- CIMB Islamic Sukuk Fund: Fund Objective Investment VolatilityDocument2 pagesCIMB Islamic Sukuk Fund: Fund Objective Investment VolatilityMaria haneffNo ratings yet

- "Planning Your Financial Future": Mangala Boyagoda 26 October 2010Document71 pages"Planning Your Financial Future": Mangala Boyagoda 26 October 2010Inde Pendent LkNo ratings yet

- SR&ED Work Schedule Associated R&D Dec 10 08Document4 pagesSR&ED Work Schedule Associated R&D Dec 10 08metroroadNo ratings yet

- Challenges & Opportunities in The Automotive Leasing IndustryDocument25 pagesChallenges & Opportunities in The Automotive Leasing Industrylévai_gáborNo ratings yet

- J.C. Parets, CMTDocument25 pagesJ.C. Parets, CMTPunit TewaniNo ratings yet

- CME - Comparing E-Minis and ETFs - Sep2012 PDFDocument8 pagesCME - Comparing E-Minis and ETFs - Sep2012 PDFbearsqNo ratings yet

- TheArgentineEconomy IAE - Marzo 2011Document43 pagesTheArgentineEconomy IAE - Marzo 2011norbertoNo ratings yet

- The Capability Crunch: The Battle For ResourcesDocument24 pagesThe Capability Crunch: The Battle For Resourceswael zantourNo ratings yet

- The Week That Just Passed March 12, 2010Document4 pagesThe Week That Just Passed March 12, 2010WallstreetableNo ratings yet

- Why Choose The IASDocument6 pagesWhy Choose The IASPeter UrbaniNo ratings yet

- Fertilizer - FFC - Urea Price Hike Clarifies Margin Outlook - KASBDocument3 pagesFertilizer - FFC - Urea Price Hike Clarifies Margin Outlook - KASBmuddasir1980No ratings yet

- Derivatives in IndiaDocument21 pagesDerivatives in IndiaShajupaulNo ratings yet

- SSRNDocument7 pagesSSRNjoystocks777No ratings yet

- UTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)Document29 pagesUTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)Rinku MishraNo ratings yet

- Lecture SlidesDocument51 pagesLecture SlidesAshish MalhotraNo ratings yet

- 23 Aug 09 25 Sep 09 12 Oct 09 23 Oct 09 18 Jan 10 5 Aug 09 1 Feb 10Document2 pages23 Aug 09 25 Sep 09 12 Oct 09 23 Oct 09 18 Jan 10 5 Aug 09 1 Feb 10brut_fora_drinkNo ratings yet

- 3 QTD MCO and Cumulative Outflow AnalysisDocument1 page3 QTD MCO and Cumulative Outflow AnalysisAlberto EstanesNo ratings yet

- Get The Power of Equity and Debt With Sbi Dual Advantage Fund - Series XxiiDocument4 pagesGet The Power of Equity and Debt With Sbi Dual Advantage Fund - Series Xxiiarghya000No ratings yet

- Solr and Lucene Search RevolutionDocument27 pagesSolr and Lucene Search RevolutionErvin MillerNo ratings yet

- Market Port PythonDocument1 pageMarket Port PythonLuis Enrique LavayenNo ratings yet

- DCC Final QuestionsDocument2 pagesDCC Final QuestionsLuis Enrique LavayenNo ratings yet

- GlassDocument4 pagesGlassLuis Enrique LavayenNo ratings yet

- Weeklyreport 05 02 2021Document5 pagesWeeklyreport 05 02 2021Luis Enrique LavayenNo ratings yet

- MINUSMADocument6 pagesMINUSMALuis Enrique LavayenNo ratings yet

- Dot 12117 DS1Document124 pagesDot 12117 DS1Luis Enrique LavayenNo ratings yet

- ICM 300 Assignment 2021Document2 pagesICM 300 Assignment 2021Luis Enrique LavayenNo ratings yet

- D2-42-HSVA Report CE CS NR Rev02 SubmittedDocument39 pagesD2-42-HSVA Report CE CS NR Rev02 Submittedrammech85No ratings yet

- Points of View: 2. Dry Cargo Chartering 3. Dry Cargo S&P 4. TankersDocument4 pagesPoints of View: 2. Dry Cargo Chartering 3. Dry Cargo S&P 4. TankersLuis Enrique LavayenNo ratings yet

- 7.adam KentDocument38 pages7.adam KentLuis Enrique LavayenNo ratings yet

- MIL-HDBK 881 Work Breakdown Structure Handbook Update: Neil F. Albert MCR, LLCDocument19 pagesMIL-HDBK 881 Work Breakdown Structure Handbook Update: Neil F. Albert MCR, LLCLuis Enrique LavayenNo ratings yet

- Ship Name: Date: SPEED (MPH) Rotation DISTANCE/miles: Cargo DiscriptionDocument1 pageShip Name: Date: SPEED (MPH) Rotation DISTANCE/miles: Cargo DiscriptionShivani KarkeraNo ratings yet

- Shipping Intelligence Network TimeseriesDocument10 pagesShipping Intelligence Network TimeseriesLuis Enrique LavayenNo ratings yet

- Shipping Intelligence Network TimeseriesDocument17 pagesShipping Intelligence Network TimeseriesLuis Enrique LavayenNo ratings yet

- Ode 45Document6 pagesOde 45Gustavo SalgeNo ratings yet

- Shipping Intelligence Network TimeseriesDocument6 pagesShipping Intelligence Network TimeseriesLuis Enrique LavayenNo ratings yet

- Shipping Intelligence Network TimeseriesDocument6 pagesShipping Intelligence Network TimeseriesLuis Enrique LavayenNo ratings yet

- IACS Interpretations of the International Convention on Load LinesDocument130 pagesIACS Interpretations of the International Convention on Load Linesjohn9812No ratings yet

- Personal History - P 11 Form 3Document6 pagesPersonal History - P 11 Form 3Zafire PYNo ratings yet

- Shipping Intelligence Network TimeseriesDocument4 pagesShipping Intelligence Network TimeseriesLuis Enrique LavayenNo ratings yet

- Fendering For Tugs: Mike Harrison, Trelleborg Marine Systems, UKDocument5 pagesFendering For Tugs: Mike Harrison, Trelleborg Marine Systems, UKRizal RachmanNo ratings yet

- Uk Co2 PDFDocument46 pagesUk Co2 PDFrajishrrrNo ratings yet

- The Current State of The Accounting ProfessionDocument2 pagesThe Current State of The Accounting ProfessionYuliana ArceNo ratings yet

- Fina 385class NotesDocument119 pagesFina 385class NotesNazimBenNo ratings yet

- Optional Riders Provide Critical Illness and Disability CoverageDocument2 pagesOptional Riders Provide Critical Illness and Disability Coverageemaraty khNo ratings yet

- Matia C.VDocument4 pagesMatia C.VKayiza AndrewNo ratings yet

- GST ScannerDocument48 pagesGST ScannerdonNo ratings yet

- Tax p2 - Taxes and Fringe BenefitsDocument25 pagesTax p2 - Taxes and Fringe BenefitsMa. Elene MagdaraogNo ratings yet

- John Neff 22 Sep 2020 1116Document5 pagesJohn Neff 22 Sep 2020 1116Debashish Priyanka SinhaNo ratings yet

- GE - Authorization FormDocument2 pagesGE - Authorization FormYiki TanNo ratings yet

- APC Individual Assignment - CIC160097Document10 pagesAPC Individual Assignment - CIC160097Siti Nor Azliza AliNo ratings yet

- Project InsuranceDocument13 pagesProject InsuranceRohan Raj MishraNo ratings yet

- BSP Circulars 2020-2000Document64 pagesBSP Circulars 2020-2000Miguel BenitezNo ratings yet

- Lesson 2 - Activity FSA2Document4 pagesLesson 2 - Activity FSA2jeffrey galanzaNo ratings yet

- Exploring Muslim Entrepreneurs Knowledge and Usage of Islamic FinancingDocument26 pagesExploring Muslim Entrepreneurs Knowledge and Usage of Islamic FinancingBadiu'zzaman Fahami100% (1)

- BBusCom2015 24 Oct 2014Document1 pageBBusCom2015 24 Oct 2014gerald_junNo ratings yet

- Ecovis CAG GuideDocument68 pagesEcovis CAG GuidemahletNo ratings yet

- Monetary Policy and The Federal Reserve: Current Policy and ConditionsDocument25 pagesMonetary Policy and The Federal Reserve: Current Policy and ConditionsJithinNo ratings yet

- Larsen & Toubro Limited, ConstructionDocument3 pagesLarsen & Toubro Limited, ConstructionandrewgeorgecherianNo ratings yet

- Reinsurance Industry Results 15Document14 pagesReinsurance Industry Results 15Philip SandaNo ratings yet

- HOOPP - General BookletDocument20 pagesHOOPP - General BookletJohn Michael GabuleNo ratings yet

- Chapter 4 SolutionsDocument80 pagesChapter 4 SolutionssurpluslemonNo ratings yet

- Wealth Creation and Employability Soft Skills For Youth 2 HandoutDocument15 pagesWealth Creation and Employability Soft Skills For Youth 2 HandoutSam ONiNo ratings yet

- Earnings Call q2 16-17Document10 pagesEarnings Call q2 16-17Neetesh DohareNo ratings yet

- Tax Invoice: Vivo Mobile India Private LimitedDocument1 pageTax Invoice: Vivo Mobile India Private LimitedRaghav SharmaNo ratings yet

- Midterm Exam Answer Sheet Course 8110Document8 pagesMidterm Exam Answer Sheet Course 8110kajalNo ratings yet

- New Global Vision Collage 22Document28 pagesNew Global Vision Collage 22Man TKNo ratings yet

- Income TaxDocument3 pagesIncome TaxMsAvalonNo ratings yet