You might also like

- Calculate inventory valuation and ending value for two productsDocument2 pagesCalculate inventory valuation and ending value for two productsNguyễn PhươngNo ratings yet

- Group 7 Tutorial AnswersDocument27 pagesGroup 7 Tutorial AnswersKwang Yi Juin0% (1)

- Financial and Managerial Accounting 15Th Edition Warren Solutions Manual Full Chapter PDFDocument67 pagesFinancial and Managerial Accounting 15Th Edition Warren Solutions Manual Full Chapter PDFclitusarielbeehax100% (12)

- BT Ke Toan Quan TriDocument39 pagesBT Ke Toan Quan TriTram NguyenNo ratings yet

- Inventories Comprehensive ExerciseDocument4 pagesInventories Comprehensive ExerciseBryan FloresNo ratings yet

- NSU ACT202 #Group ProjectDocument21 pagesNSU ACT202 #Group ProjectArisha Faisal 1931944630No ratings yet

- Exercises Chapter 3Document13 pagesExercises Chapter 3mohsen bukNo ratings yet

- Manufacturing Cost Problems: Chapter 1 Set B SolutionsDocument3 pagesManufacturing Cost Problems: Chapter 1 Set B SolutionsPak CareerNo ratings yet

- Corporate Financial Accounting 14th Edition Warren Solutions Manual DownloadDocument48 pagesCorporate Financial Accounting 14th Edition Warren Solutions Manual DownloadRobert Gee100% (26)

- Chapter 10 Lab Review WorksheetDocument2 pagesChapter 10 Lab Review WorksheetKyle AndersNo ratings yet

- Rubino Anna Bu20145 Budget Project s3-23Document10 pagesRubino Anna Bu20145 Budget Project s3-23api-701459983No ratings yet

- COST ACCOUNTING - Sample ExerciseDocument3 pagesCOST ACCOUNTING - Sample ExerciseLorenzo PanchoNo ratings yet

- Tugas 1 Akuntansi Manajemen - Darma Guna (2019104432)Document14 pagesTugas 1 Akuntansi Manajemen - Darma Guna (2019104432)Darma GunaNo ratings yet

- Topic 1 - Assignment 1 CostDocument4 pagesTopic 1 - Assignment 1 CostAnna Cabrera0% (1)

- Bismillah Final Excel AlksDocument24 pagesBismillah Final Excel AlksRohis RahmahNo ratings yet

- Sample Final Exam With SolutionDocument17 pagesSample Final Exam With SolutionYevhenii VdovenkoNo ratings yet

- Task AccountingDocument13 pagesTask AccountingYordan LawijayaNo ratings yet

- Problem 4-47 Application of Overhead Rate Service IndustryDocument26 pagesProblem 4-47 Application of Overhead Rate Service IndustryIkram100% (1)

- B7AF107 J16 August 2020 Paper 1-5Document5 pagesB7AF107 J16 August 2020 Paper 1-5dayahNo ratings yet

- Individual assignment (Fall 2023)2.docx2Document10 pagesIndividual assignment (Fall 2023)2.docx2RealGenius (Carl)No ratings yet

- Panta budget schedules for production, materials, laborDocument10 pagesPanta budget schedules for production, materials, laborFiles OrganizedNo ratings yet

- Maximizing sales revenue through price adjustmentsDocument13 pagesMaximizing sales revenue through price adjustmentsxxxNo ratings yet

- Chapter 2 Sol 31-39Document8 pagesChapter 2 Sol 31-39Something ChicNo ratings yet

- Managerial Accounting-Solutions To Ch09Document16 pagesManagerial Accounting-Solutions To Ch09Mohammed Hassan100% (1)

- Orca Share Media1646571581803 6906221771846243726Document12 pagesOrca Share Media1646571581803 6906221771846243726LACONSAY, Nathalie B.No ratings yet

- Budget AssignmentDocument6 pagesBudget AssignmentGurveer Karen, and the PriceNo ratings yet

- Tutorial Questions CVPDocument6 pagesTutorial Questions CVPChristopher LoisulieNo ratings yet

- Solution - Worksheet 7 (Budgeting)Document2 pagesSolution - Worksheet 7 (Budgeting)La MarNo ratings yet

- Number Four Solution AdjustmentDocument8 pagesNumber Four Solution AdjustmentKisitu MosesNo ratings yet

- Tutorial ContDocument25 pagesTutorial ContJJ Rivera75% (4)

- Prelim Exam-Boticario D. (SBA)Document5 pagesPrelim Exam-Boticario D. (SBA)Dominic E. BoticarioNo ratings yet

- MASTER BUDGETDocument17 pagesMASTER BUDGETlov3m3No ratings yet

- Finch Excel ReportDocument15 pagesFinch Excel ReportshuvorajbhattaNo ratings yet

- LGT5105 Exercise 3 SolutionDocument2 pagesLGT5105 Exercise 3 SolutionHẰNG NGUYỄN THANHNo ratings yet

- Solución de Problemas Planteados PresupuestosDocument13 pagesSolución de Problemas Planteados PresupuestosAndre AliagaNo ratings yet

- Key To Corrections - LEVEL 2 MODULE 7Document9 pagesKey To Corrections - LEVEL 2 MODULE 7UFO CatcherNo ratings yet

- Jacobh Excel3Document8 pagesJacobh Excel3api-664413574No ratings yet

- Introduction To Accounting and Finance Unit Code Aaf005-1 Main Exam Semester 3 2020/21Document7 pagesIntroduction To Accounting and Finance Unit Code Aaf005-1 Main Exam Semester 3 2020/21Chulbul PandeyNo ratings yet

- (A) Jorge Company CVP Income Statement (Estimated) For The Year Ending December 31, 2014Document4 pages(A) Jorge Company CVP Income Statement (Estimated) For The Year Ending December 31, 2014Kim QuyênNo ratings yet

- Addition Exercises - Chapter 1 To 3Document4 pagesAddition Exercises - Chapter 1 To 3Raymond GuillartesNo ratings yet

- Cash 5,000 Accounts Receivable 1,500 Raw Materials Inventory 258 Finished Goods Inventory 1,462Document17 pagesCash 5,000 Accounts Receivable 1,500 Raw Materials Inventory 258 Finished Goods Inventory 1,462Lan Tran HoangNo ratings yet

- Chapter 7 Problems PDFDocument18 pagesChapter 7 Problems PDFArham Sheikh100% (1)

- Advanced Financial Accounting & Reporting Cost ConceptsDocument6 pagesAdvanced Financial Accounting & Reporting Cost ConceptsMarynelle Labrador SevillaNo ratings yet

- Ca (Bsaf - Bba.mba)Document5 pagesCa (Bsaf - Bba.mba)kashif aliNo ratings yet

- Projected Sales and Finished Goods Inventory RequirementsDocument5 pagesProjected Sales and Finished Goods Inventory RequirementsKath JornalNo ratings yet

- Quest 13Document2 pagesQuest 13kaji cruzNo ratings yet

- Managerial Accounting 9th Edition Crosson Solutions ManualDocument39 pagesManagerial Accounting 9th Edition Crosson Solutions ManualKennethSparkskqgmrNo ratings yet

- Individual assignment (Fall 2023)2Document11 pagesIndividual assignment (Fall 2023)2RealGenius (Carl)No ratings yet

- Exam 2Document3 pagesExam 2tamene woldeNo ratings yet

- Tutorial - Topic 1 SolutionDocument4 pagesTutorial - Topic 1 SolutionFrancescoNo ratings yet

- Calculation of Issue Price and Percentage for BondsDocument119 pagesCalculation of Issue Price and Percentage for Bondssai krishnaNo ratings yet

- Chap 4 Job CostingDocument9 pagesChap 4 Job CostingWadiah AkbarNo ratings yet

- RevisionDocument16 pagesRevisionKaycee C. San DiegoNo ratings yet

- Topic 5: Short Term Decision Making Answer To Exercise 1: BKAM3023 Management Accounting IIDocument3 pagesTopic 5: Short Term Decision Making Answer To Exercise 1: BKAM3023 Management Accounting IIdini sofiaNo ratings yet

- Management AccountingDocument6 pagesManagement AccountingJohn Allen Cruz Caballa100% (2)

- Mac Session 15Document12 pagesMac Session 15Dhairya GuptaNo ratings yet

- Question Paper 2022Document4 pagesQuestion Paper 2022vanshikagoyal7600No ratings yet

- AFAR 14D Cost Accounting (Job Order, Process Costing, JIT Backflush, Activity Based Costing, Joint and ByProducts, Standard Costing)Document9 pagesAFAR 14D Cost Accounting (Job Order, Process Costing, JIT Backflush, Activity Based Costing, Joint and ByProducts, Standard Costing)Jeepee John100% (1)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- ch.20 Acc HW PDFDocument2 pagesch.20 Acc HW PDFyizhou FengNo ratings yet

- ch.18 Acc HWDocument2 pagesch.18 Acc HWyizhou FengNo ratings yet

- Ch.17 HW Acc PDFDocument2 pagesCh.17 HW Acc PDFyizhou FengNo ratings yet

- Ch.19 Acc HW PDFDocument2 pagesCh.19 Acc HW PDFyizhou FengNo ratings yet

- Ch.21 Acc HW PDFDocument4 pagesCh.21 Acc HW PDFyizhou FengNo ratings yet

- DigitalDocket B202337253 N6204 69281Document9 pagesDigitalDocket B202337253 N6204 69281tyagictwNo ratings yet

- Vat Form 100Document10 pagesVat Form 100Shoaib4804174No ratings yet

- Auditing SAP GRCDocument45 pagesAuditing SAP GRCsaty_temp286475% (4)

- El Paso Hispanic Chamber of Commerce Grant Application PackageDocument8 pagesEl Paso Hispanic Chamber of Commerce Grant Application PackageDavidNo ratings yet

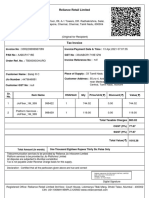

- Reliance Retail Limited: Sr. No. Item Name Hsn/Sac Qty Price/Unit Discount ValueDocument3 pagesReliance Retail Limited: Sr. No. Item Name Hsn/Sac Qty Price/Unit Discount ValuemukeshNo ratings yet

- Fixed Deposit Receipt FormatDocument9 pagesFixed Deposit Receipt Formatशुभ चिंतकNo ratings yet

- Accounting Entries in OracleDocument31 pagesAccounting Entries in OracleConrad RodricksNo ratings yet

- APTC form-40-A-GPFDocument2 pagesAPTC form-40-A-GPFvijay_dilse100% (1)

- Oracle Process Manufacturing (OPM) Setup Document Oracle Process Manufacturing (OPM) Setup Document Raju Chinthapatla Raju ChinthapatlaDocument19 pagesOracle Process Manufacturing (OPM) Setup Document Oracle Process Manufacturing (OPM) Setup Document Raju Chinthapatla Raju Chinthapatlahaitham ibrahem mohmedNo ratings yet

- Rmo 07-06Document9 pagesRmo 07-06Printet08No ratings yet

- DEMS SPZ Audit ReportDocument9 pagesDEMS SPZ Audit ReportSubhas MishraNo ratings yet

- GRC MM P2PDocument9 pagesGRC MM P2PVijay Kumar DasNo ratings yet

- Credit Card Advantage Release Notes ArticleDocument10 pagesCredit Card Advantage Release Notes ArticleiamagoodboyNo ratings yet

- Lecture Chapter 6 Introduction To The Value Added TaxDocument16 pagesLecture Chapter 6 Introduction To The Value Added TaxChristian PelimcoNo ratings yet

- 2Document29 pages2shankari24381No ratings yet

- Enloe Field Trip GuidelinesDocument2 pagesEnloe Field Trip GuidelinesSarita ShawNo ratings yet

- Reliance Retail Limited: Total Amount (In Words) One Thousand Eighteen Rupees Thirty Six Paisa OnlyDocument3 pagesReliance Retail Limited: Total Amount (In Words) One Thousand Eighteen Rupees Thirty Six Paisa OnlyBalaNo ratings yet

- LAN-Based Inventory Management for JumpStart Auto SpaDocument7 pagesLAN-Based Inventory Management for JumpStart Auto SpaArchie GuillenaNo ratings yet

- Qbo 2018 TBDocument20 pagesQbo 2018 TBWilson CarlosNo ratings yet

- International Transfer AgreementDocument6 pagesInternational Transfer AgreementDidier ChristelNo ratings yet

- Job Description: Polaris Power Engineering Silliman Avenue Extension Dumaguete CityDocument2 pagesJob Description: Polaris Power Engineering Silliman Avenue Extension Dumaguete CityWilliam Andrew Gutiera BulaqueñaNo ratings yet

- TAX Invoice Summary for Dubai Tour PackagesDocument2 pagesTAX Invoice Summary for Dubai Tour PackagesZeyadNo ratings yet

- TACNDocument6 pagesTACNNhi Nguyễn ThảoNo ratings yet

- Drop Shipment AccountingDocument28 pagesDrop Shipment AccountingIbbu Mohd0% (1)

- Aron PDFDocument41 pagesAron PDFÃrõñ HãbtãmüNo ratings yet

- Digitec - Sales Receipt - 81894093Document1 pageDigitec - Sales Receipt - 81894093smokin tigernenteNo ratings yet

- How to create a return PO and process a vendor return in SAPDocument35 pagesHow to create a return PO and process a vendor return in SAPSunil BonalaNo ratings yet

- FABM1 4th Quarter Summative ExamDocument4 pagesFABM1 4th Quarter Summative ExamRizaphel J SalemNo ratings yet

- Materials ManagementDocument347 pagesMaterials Managementhare001671% (7)

- Accounts Officer Training ReportDocument7 pagesAccounts Officer Training ReportsrmurralitharanNo ratings yet