You might also like

- Shariah Court Procedure and Evidence: Prepared By: Atty Nadjer D. PinataraDocument16 pagesShariah Court Procedure and Evidence: Prepared By: Atty Nadjer D. PinataraDatu ArumpacNo ratings yet

- Al Qadi Al-Nu'Man - Farhad Daftary - 01-12-10 - FinalDocument3 pagesAl Qadi Al-Nu'Man - Farhad Daftary - 01-12-10 - FinalKomail RajaniNo ratings yet

- Translation of 9th Namat of Nasir Tusi S CommentaryDocument50 pagesTranslation of 9th Namat of Nasir Tusi S Commentarywww.alhassanain.org.englishNo ratings yet

- Type of ZakatDocument7 pagesType of ZakatMuhd Zulhusni MusaNo ratings yet

- Essential Duas For Muslims GR 1-7Document98 pagesEssential Duas For Muslims GR 1-7Salmaan JoomaNo ratings yet

- VERY Rewarding Nafl Salaahs We Can Pray Everyday EVERY RamadanDocument6 pagesVERY Rewarding Nafl Salaahs We Can Pray Everyday EVERY Ramadanzakir2012100% (1)

- The Four Imams - Muhammad Abu Zahra PDFDocument466 pagesThe Four Imams - Muhammad Abu Zahra PDFAhmedNazeerMohammed75% (12)

- Zakat Calculation: Based on Fiqh-uz-Zakat by Yusuf al-QaradawiFrom EverandZakat Calculation: Based on Fiqh-uz-Zakat by Yusuf al-QaradawiRating: 3.5 out of 5 stars3.5/5 (3)

- AL-KAFI VOLUME 5 (English) PDFDocument696 pagesAL-KAFI VOLUME 5 (English) PDFDhulfikarETayyar100% (2)

- Differences of The ImamsDocument61 pagesDifferences of The ImamsWaqar100% (7)

- Fiqh of Zakat: Mufti Faraz Adam Amanah AdvisorsDocument49 pagesFiqh of Zakat: Mufti Faraz Adam Amanah AdvisorsRendiNurcahyoNo ratings yet

- Brief Guidelines On Zakat 23Document2 pagesBrief Guidelines On Zakat 23mimunaaneNo ratings yet

- Chapter On ZakatDocument19 pagesChapter On Zakatimranhaq23No ratings yet

- Zakat Ch01Document19 pagesZakat Ch01KhalidNo ratings yet

- CH 4 Zakat and Tax PlanningDocument48 pagesCH 4 Zakat and Tax Planningabdihakimmohamed628No ratings yet

- Islamic Banking - Ipacc J - Chapter 6Document6 pagesIslamic Banking - Ipacc J - Chapter 6sadwi fitriNo ratings yet

- 62198bos50436 cp9Document90 pages62198bos50436 cp9GabbarNo ratings yet

- Understanding & Calculating Zakah: 1stethical Charitable Trust'SguidetoDocument9 pagesUnderstanding & Calculating Zakah: 1stethical Charitable Trust'SguidetoidamielNo ratings yet

- 67847bos54415 cp9Document90 pages67847bos54415 cp9Gopika CANo ratings yet

- Types of ZakahDocument17 pagesTypes of ZakahAishah SisNo ratings yet

- Analisis Investasi Tambang - 3 - 4Document52 pagesAnalisis Investasi Tambang - 3 - 4samuel sedikNo ratings yet

- Zakat Accounting 2Document199 pagesZakat Accounting 2asna_No ratings yet

- AFM QB 2024 - FinalDocument621 pagesAFM QB 2024 - Final74ef8465d65d1bNo ratings yet

- Week 10 - Zakat For Companies - 2018Document12 pagesWeek 10 - Zakat For Companies - 2018Raihana BaharomNo ratings yet

- Hedging at Its Most Basic: Ian LevyDocument3 pagesHedging at Its Most Basic: Ian Levyivanuska90100% (1)

- Rina Septiyani - 19021040Document4 pagesRina Septiyani - 19021040리나박No ratings yet

- Hedging at Its Most BasicDocument4 pagesHedging at Its Most BasicHenry NCNo ratings yet

- UntitledDocument268 pagesUntitledkalyanNo ratings yet

- Week 9 - Zakat On Companies - Method2018Document8 pagesWeek 9 - Zakat On Companies - Method2018Raihana BaharomNo ratings yet

- Chapter 3 Foreign Exchange Exposure & Risk ManagementDocument50 pagesChapter 3 Foreign Exchange Exposure & Risk Managementvaibhavrs22.pumbaNo ratings yet

- Appendix: Explanations To Be Used in Conjunction With The Spreadsheet On Zakat CalculatorDocument25 pagesAppendix: Explanations To Be Used in Conjunction With The Spreadsheet On Zakat CalculatorAmeen SyedNo ratings yet

- Lecture 1 & 2 - Accounting & Financial Statements - MD Sazzad HossainDocument26 pagesLecture 1 & 2 - Accounting & Financial Statements - MD Sazzad HossainMd. Sazzad HossainNo ratings yet

- Zakat CalculatorDocument3 pagesZakat Calculatorapi-3759337No ratings yet

- Time Value of Moneytks19Document63 pagesTime Value of Moneytks19Udita GopalkrishnaNo ratings yet

- Cash and Liquidity Management: February 2011Document44 pagesCash and Liquidity Management: February 2011Bulls Bears FinancialsNo ratings yet

- ZAKAT ACCOUNTING ON RIKAZtDocument24 pagesZAKAT ACCOUNTING ON RIKAZtLarasma Mutiara PutriNo ratings yet

- Trade and Cash Discount NotesDocument3 pagesTrade and Cash Discount NotesAyushNo ratings yet

- ARTICLES365Document2 pagesARTICLES365aimatova208.4No ratings yet

- AU PA03 02 CU!BANGET BUSINESS Finance PDFDocument9 pagesAU PA03 02 CU!BANGET BUSINESS Finance PDFMichelle OliviaNo ratings yet

- Future PricingDocument14 pagesFuture PricingashutoshNo ratings yet

- Accounting RemedialDocument40 pagesAccounting Remedialwhyme_bNo ratings yet

- Missed Zakat: Your Guide To Understanding and CalculatingDocument20 pagesMissed Zakat: Your Guide To Understanding and CalculatingHnia UsmanNo ratings yet

- Unit 4 Preparation of Trial Balance andDocument21 pagesUnit 4 Preparation of Trial Balance andAnand V RNo ratings yet

- U2 Conversion of SE To DESDocument3 pagesU2 Conversion of SE To DESneyadanNo ratings yet

- Chapter 1 Cash and Cash Equivalents Students Copy 2Document23 pagesChapter 1 Cash and Cash Equivalents Students Copy 2Shyra RiveraNo ratings yet

- Week 4-5 Tutorial Solutions UpdatedDocument7 pagesWeek 4-5 Tutorial Solutions UpdatedAshley ChandNo ratings yet

- Petty Cash & 3 Column Cash BookDocument22 pagesPetty Cash & 3 Column Cash BookAbisellyNo ratings yet

- Cash&Cash EquivalentDocument16 pagesCash&Cash EquivalentJessicaNo ratings yet

- Chapter 8 - Futures CurrencyDocument16 pagesChapter 8 - Futures CurrencyYa YaNo ratings yet

- Working Capital Management: An Insight ToDocument20 pagesWorking Capital Management: An Insight Toaditi_awasthi_1No ratings yet

- Financial AccountingDocument6 pagesFinancial AccountingHAROON EDITZNo ratings yet

- Tally - AssignmentDocument6 pagesTally - AssignmentAash RedmiNo ratings yet

- Penerimaan Kas (General Cashier)Document8 pagesPenerimaan Kas (General Cashier)Dewa PradnyanaNo ratings yet

- Zakah Pamphlet With CalculatorDocument22 pagesZakah Pamphlet With CalculatorHaider AliNo ratings yet

- Wa0010Document6 pagesWa0010Ardhystha AulyaNo ratings yet

- CashBook and Petty CashBookDocument22 pagesCashBook and Petty CashBookNabiha KhanNo ratings yet

- Cash Management: Preprared & Presented BYDocument25 pagesCash Management: Preprared & Presented BYVenkata PrashanthNo ratings yet

- Lecture4 DepositsDocument24 pagesLecture4 DepositsRy NielNo ratings yet

- Salon Cantik (Finished)Document48 pagesSalon Cantik (Finished)Sarah NoveritaNo ratings yet

- Jusa Zakaat Calculation TableDocument8 pagesJusa Zakaat Calculation Tablemariyathai_1No ratings yet

- Z00330010220164013Installment SalesDocument19 pagesZ00330010220164013Installment SalesLinna GuinarsoNo ratings yet

- (KELOMPOK 4) Latihan Soal Cash FlowDocument5 pages(KELOMPOK 4) Latihan Soal Cash FlowꧾꧾNo ratings yet

- Chapter 1 Cash and Cash EquivalentsDocument23 pagesChapter 1 Cash and Cash EquivalentsZeo AlcantaraNo ratings yet

- Zakat Calculator Ver 2005Document5 pagesZakat Calculator Ver 2005u1umarNo ratings yet

- Piecemeal Sybcom Sem3Document100 pagesPiecemeal Sybcom Sem3Poonam Sunil Lalwani LalwaniNo ratings yet

- MRK - Fall 2022 - MGT101Document6 pagesMRK - Fall 2022 - MGT101HAROON EDITZNo ratings yet

- Zakat FormDocument6 pagesZakat Formmdalt9180No ratings yet

- ShorttermdepositgmsDocument3 pagesShorttermdepositgmsSnehashree SahooNo ratings yet

- Week 14 - Data AnalysisDocument7 pagesWeek 14 - Data AnalysisFadhilah IstiqomahNo ratings yet

- Week 14 - Data AnalysisDocument7 pagesWeek 14 - Data AnalysisFadhilah IstiqomahNo ratings yet

- Bibliometric Analysis: Accounting Research MethodologyDocument5 pagesBibliometric Analysis: Accounting Research MethodologyFadhilah IstiqomahNo ratings yet

- Bibliometric Analysis: Accounting Research MethodologyDocument5 pagesBibliometric Analysis: Accounting Research MethodologyFadhilah IstiqomahNo ratings yet

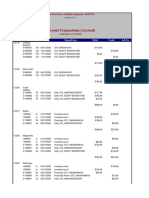

- Account Transactions (Accrual) : ID# SRC Date Memo/Payee Debit Credit Job NoDocument3 pagesAccount Transactions (Accrual) : ID# SRC Date Memo/Payee Debit Credit Job NoFadhilah IstiqomahNo ratings yet

- Week 6 AssignmentDocument9 pagesWeek 6 AssignmentFadhilah IstiqomahNo ratings yet

- Assignment Week 1Document2 pagesAssignment Week 1Fadhilah IstiqomahNo ratings yet

- Assignment Week 3Document1 pageAssignment Week 3Fadhilah IstiqomahNo ratings yet

- Assignment Week 2Document1 pageAssignment Week 2Fadhilah IstiqomahNo ratings yet

- Assignment Week 1Document1 pageAssignment Week 1Fadhilah IstiqomahNo ratings yet

- The Legal Status of Following A MadhabDocument132 pagesThe Legal Status of Following A MadhabE-IQRA.INFONo ratings yet

- Implementasi (Studi Kasus Pada KSPPS BMT Fastabiq Jepara) : Syariah Compliance Pada Akad Murabahah Dan IjarahDocument10 pagesImplementasi (Studi Kasus Pada KSPPS BMT Fastabiq Jepara) : Syariah Compliance Pada Akad Murabahah Dan IjarahAri ArdiansyahNo ratings yet

- Indian Institute of Legal StudiesDocument13 pagesIndian Institute of Legal Studiessehnaz NaazNo ratings yet

- Hajj and Umrah Pocket GuideDocument2 pagesHajj and Umrah Pocket Guideanwar.buchooNo ratings yet

- Hagiography in Biographies of Al Awzai and Sufyan Al ThawriDocument14 pagesHagiography in Biographies of Al Awzai and Sufyan Al ThawrighouseNo ratings yet

- Identity in The Margins - Unpublished Hanafi Commentaries On The Mukhtasar of Ahmad B. Muhammad Al-QuduriDocument28 pagesIdentity in The Margins - Unpublished Hanafi Commentaries On The Mukhtasar of Ahmad B. Muhammad Al-QuduriAbul HasanNo ratings yet

- MurtadDocument149 pagesMurtadSyeda Asiya0% (1)

- What Is AkhbariatDocument7 pagesWhat Is AkhbariatDr. Izzat HusainNo ratings yet

- Post Divorce Maintenance MAATA For MusliDocument10 pagesPost Divorce Maintenance MAATA For MusliMUHAMMAD ADAM LUQMAN MOHAMMAD ISMAILNo ratings yet

- Press - Selected Pilgrims Cover NumbersDocument10 pagesPress - Selected Pilgrims Cover NumbersMdmNo ratings yet

- Living Apart TogetherDocument100 pagesLiving Apart Togetherpythias returnsNo ratings yet

- Icd Thomson Reuters Islamic Finance Development Report 2017Document120 pagesIcd Thomson Reuters Islamic Finance Development Report 2017Victoria MaciasNo ratings yet

- Are Menstruating Women Permitted To Recite or Touch The Qur'AnDocument2 pagesAre Menstruating Women Permitted To Recite or Touch The Qur'AnSajid HolyNo ratings yet

- (Q5) Maslahah MursalahDocument8 pages(Q5) Maslahah MursalahALINA WONG WAN LINGNo ratings yet

- Naafey Ulema SADocument57 pagesNaafey Ulema SAAtif KaramatNo ratings yet

- Bihar Ul Anwar PDFDocument2 pagesBihar Ul Anwar PDFArsalan Haider100% (2)

- Tawheed Vol1 Basis of Islam and Its Essential PillarsDocument31 pagesTawheed Vol1 Basis of Islam and Its Essential PillarsWahidNo ratings yet

- Full Night Prayer ScheduleDocument34 pagesFull Night Prayer ScheduleumhafeezaNo ratings yet

- Human Rights ConstitutionDocument70 pagesHuman Rights ConstitutionJurisNo ratings yet

- What Is Sood, Interest, Ar-Riba? Muhammad Anwar AbbasiDocument35 pagesWhat Is Sood, Interest, Ar-Riba? Muhammad Anwar AbbasiRana Mazhar100% (2)

- Archipelagic DoctrineDocument4 pagesArchipelagic Doctrineapple gryn acederaNo ratings yet

- Developing Modern Islamic Financial System Via IjtihadDocument18 pagesDeveloping Modern Islamic Financial System Via IjtihadabdulhameednaseerNo ratings yet