You might also like

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Ajp Dan Neraca LajurDocument5 pagesAjp Dan Neraca LajurMa chezzNo ratings yet

- How to Double your Wealth Every 10 Years (Without Really Trying)From EverandHow to Double your Wealth Every 10 Years (Without Really Trying)Rating: 3 out of 5 stars3/5 (1)

- Sayed Muhammad Khatami 1801003010035 Prak PajakDocument3 pagesSayed Muhammad Khatami 1801003010035 Prak PajakNB乛 SigenkNo ratings yet

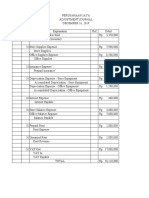

- PT Cahaya-Pjdm (Anugrah Syahrani)Document15 pagesPT Cahaya-Pjdm (Anugrah Syahrani)Ara SyahraniNo ratings yet

- 1E - 24 - Radiah AriyaniDocument4 pages1E - 24 - Radiah AriyaniRadiah AriyaniNo ratings yet

- Description Commersial Loss (Profit)Document3 pagesDescription Commersial Loss (Profit)fitri anggra eniNo ratings yet

- Neraca Lajur - Kertas KerjaDocument6 pagesNeraca Lajur - Kertas KerjaAdmin Anak PanahNo ratings yet

- B. Kertas Kerja Konsolidasi 3 Bagian Per 31 Des 2018: Laba Neto (Dari Atas)Document5 pagesB. Kertas Kerja Konsolidasi 3 Bagian Per 31 Des 2018: Laba Neto (Dari Atas)Wasitoh Rizki HidayatiNo ratings yet

- Tugas Akuntansi (Lois Riris Nababan - 2036010019)Document13 pagesTugas Akuntansi (Lois Riris Nababan - 2036010019)Lois NababanNo ratings yet

- Neraca LajurDocument2 pagesNeraca LajurBulan julpi suwelly100% (1)

- Kumala Wardani X.akDocument6 pagesKumala Wardani X.akDakun PonorogoNo ratings yet

- Contoh Cash FlowDocument9 pagesContoh Cash FlowIrma Felicia WidjajaNo ratings yet

- Akuntansi (Haspisah KLS 11 Akl2)Document6 pagesAkuntansi (Haspisah KLS 11 Akl2)sansihkNo ratings yet

- Jawaban Soal Simulasi No 2Document15 pagesJawaban Soal Simulasi No 2Muhammad Fadel LaminaNo ratings yet

- Pembahasan Plant AssetDocument5 pagesPembahasan Plant AssetIsan KamilNo ratings yet

- Cashflow 03Document14 pagesCashflow 03Mon RoeNo ratings yet

- Analisis KreditDocument14 pagesAnalisis KreditIndah NkNo ratings yet

- Pajak LatihanDocument2 pagesPajak LatihanRandy PermanaNo ratings yet

- Ud Wirastri Siklus AkuntansiDocument39 pagesUd Wirastri Siklus AkuntansiPutri EkawatiNo ratings yet

- CV Sandoro IrwandaDocument12 pagesCV Sandoro IrwandaMuhammad IrwandaNo ratings yet

- Acc No Account Name Trial Balance Adjustment Entries Debit Credit DebitDocument14 pagesAcc No Account Name Trial Balance Adjustment Entries Debit Credit Debitelza jiuniNo ratings yet

- Akl 2 Consolidation-Change in Ownership InterestDocument6 pagesAkl 2 Consolidation-Change in Ownership InterestVenna LestariNo ratings yet

- Trial Balance January 2009: JL - Hr.Subrantas No.26 PekanbaruDocument1 pageTrial Balance January 2009: JL - Hr.Subrantas No.26 PekanbaruHabib NasrudinNo ratings yet

- Budget Plan Periode 2021 - 2023Document3 pagesBudget Plan Periode 2021 - 2023Ichi OchaNo ratings yet

- Trial Balance (PD JAYA MOTOR)Document1 pageTrial Balance (PD JAYA MOTOR)Arum AnnisaNo ratings yet

- Laporan Laba-Rugi PT Mondar Mandir TAHUN 2013: Jumlah PendapatanDocument6 pagesLaporan Laba-Rugi PT Mondar Mandir TAHUN 2013: Jumlah PendapatanFahrizal RivaldinataNo ratings yet

- Worksheet Adi JayaDocument4 pagesWorksheet Adi JayaMarda LenaNo ratings yet

- CV Maju WorksheetDocument6 pagesCV Maju WorksheetWijaya Mahathir AlbatawyNo ratings yet

- Kunci Jawaban Pra UasDocument7 pagesKunci Jawaban Pra UasKiki Saskia Marta BelaNo ratings yet

- Master Tenancy 2020Document5 pagesMaster Tenancy 2020Muhammad nasrullahNo ratings yet

- Bab Iii: 3.1 Kebutuhan Investasi 3.1.1 Modal Tetap (MT)Document4 pagesBab Iii: 3.1 Kebutuhan Investasi 3.1.1 Modal Tetap (MT)Carry NihonNo ratings yet

- Contoh Chas FlowDocument2 pagesContoh Chas FlowRubi MazNo ratings yet

- Trial Balance Ud Wirastri Setelah JP KBM 6 (GT - Latifah XII Akl 2) PDFDocument1 pageTrial Balance Ud Wirastri Setelah JP KBM 6 (GT - Latifah XII Akl 2) PDFGusti LatifahNo ratings yet

- Bengkel Alani PuratonaDocument32 pagesBengkel Alani PuratonaFierda Eka PratiwiNo ratings yet

- Laporan PenyesuaianDocument15 pagesLaporan PenyesuaianNuzrul Fani NursiamNo ratings yet

- PA PT. Lambada & PT. AbadiDocument27 pagesPA PT. Lambada & PT. AbadiSetia NiniNo ratings yet

- Cashflow Keripik SingkongDocument8 pagesCashflow Keripik SingkongAnnisa NovrizalNo ratings yet

- Worksheet Akuntansi DahliaDocument4 pagesWorksheet Akuntansi DahliaDahliaNo ratings yet

- Pak NotoDocument9 pagesPak NotopanjiNo ratings yet

- Analisis Finansial Kelompok 2Document11 pagesAnalisis Finansial Kelompok 2Nazli Wulantri BinabaNo ratings yet

- SPD Cat 4 Unit, Carry Out To WSDocument4 pagesSPD Cat 4 Unit, Carry Out To WSArdiansyah SHNo ratings yet

- SPD Na 40 Pancaran Infinity, 1 Unit, Carry Out VesselDocument4 pagesSPD Na 40 Pancaran Infinity, 1 Unit, Carry Out VesselArdiansyah SHNo ratings yet

- SPD Swadaya Met 42Document4 pagesSPD Swadaya Met 42Ardiansyah SHNo ratings yet

- SPD RH 2023 2unit, Carry Out To WsDocument4 pagesSPD RH 2023 2unit, Carry Out To WsArdiansyah SHNo ratings yet

- SPD VTR 454 Kota Rukun, CARRY OUT TO WSDocument4 pagesSPD VTR 454 Kota Rukun, CARRY OUT TO WSArdiansyah SHNo ratings yet

- Siklus Akuntansi Pada PT Adi JayaDocument11 pagesSiklus Akuntansi Pada PT Adi Jayafitrianura04No ratings yet

- Neraca Saldo DR CR: Pt. Abc Worksheet Untuk Periode Yang Berakhir 31 DESEMBER 2020Document13 pagesNeraca Saldo DR CR: Pt. Abc Worksheet Untuk Periode Yang Berakhir 31 DESEMBER 2020Ardila JuliantiNo ratings yet

- Tugas Pert 15 PA IKelas BDocument12 pagesTugas Pert 15 PA IKelas BRinaldy SabilfinaNo ratings yet

- Balance Sheet As of December 2010: Jalan Soekarno Hatta KM 12, Bandung Jawa BaratDocument2 pagesBalance Sheet As of December 2010: Jalan Soekarno Hatta KM 12, Bandung Jawa Baratupik palupiNo ratings yet

- Finna Fitria Chopandi - TM 10 - Ucp 3Document8 pagesFinna Fitria Chopandi - TM 10 - Ucp 3Finna Fitria ChNo ratings yet

- Latihan 10Document7 pagesLatihan 10Trifenna Edna Widya Perdani0% (1)

- Contoh Working Balance SheetDocument4 pagesContoh Working Balance SheetMichaelNo ratings yet

- Pajak BusyamsiahDocument12 pagesPajak BusyamsiahIcha Almeera0% (3)

- Rahma ConsutingDocument6 pagesRahma ConsutingEko Firdausta TariganNo ratings yet

- ULANGANDocument5 pagesULANGANRama Nur Anggrit PratamaNo ratings yet

- Spesifikasi Barang: Bidang: Kegiatan: Pengadaan Alat Rumah Tangga Lainnya (Home Use) SKPD: Sumber Dana: APBD 2019Document6 pagesSpesifikasi Barang: Bidang: Kegiatan: Pengadaan Alat Rumah Tangga Lainnya (Home Use) SKPD: Sumber Dana: APBD 2019Juan ReppiNo ratings yet

- UD BUANA Trial BalanceDocument1 pageUD BUANA Trial Balancerasaz deviNo ratings yet

- Direktur Utama: Komisaris Dan HRDocument12 pagesDirektur Utama: Komisaris Dan HRCindy Nella DewiNo ratings yet

- Mura Inc Adjusting Entries December 31, 2016 Account Title Ref Debit CreditDocument4 pagesMura Inc Adjusting Entries December 31, 2016 Account Title Ref Debit CreditFadhilahNo ratings yet

- Bibliometric Analysis: Accounting Research MethodologyDocument5 pagesBibliometric Analysis: Accounting Research MethodologyFadhilah IstiqomahNo ratings yet

- Week 14 - Data AnalysisDocument7 pagesWeek 14 - Data AnalysisFadhilah IstiqomahNo ratings yet

- Assignment Week 1Document2 pagesAssignment Week 1Fadhilah IstiqomahNo ratings yet

- 2b. Zakat Harta TunaiDocument26 pages2b. Zakat Harta TunaiFadhilah IstiqomahNo ratings yet

- Assignment Week 2Document1 pageAssignment Week 2Fadhilah IstiqomahNo ratings yet

- Railway Hand Book On Internal ChecksDocument308 pagesRailway Hand Book On Internal ChecksHiraBallabh82% (34)

- 08L0767 Fy18-19 Kyc Aml CFT Fatca CRSDocument13 pages08L0767 Fy18-19 Kyc Aml CFT Fatca CRSabhi646son5124No ratings yet

- 2023 Signal Mountain Comparision Fire Study FinalDocument30 pages2023 Signal Mountain Comparision Fire Study FinalWTVC100% (1)

- Role of Merchant Banking in Portfolio Management and Issue Management'Document85 pagesRole of Merchant Banking in Portfolio Management and Issue Management'Rinkesh SutharNo ratings yet

- Retail Store Manager Resume SampleDocument8 pagesRetail Store Manager Resume Sampleafdmjphtj100% (1)

- Hyper CompetitionDocument27 pagesHyper Competitiondilip15043No ratings yet

- Ae It11 Test Oct Assessment CriteriaDocument5 pagesAe It11 Test Oct Assessment CriteriaAna Paula CristóvãoNo ratings yet

- Activiteiten Formulier - 5. Acquire Professional CompetencesDocument2 pagesActiviteiten Formulier - 5. Acquire Professional CompetencesRaiane InácioNo ratings yet

- Cambridge Assessment International Education: Economics 0455/22 March 2019Document12 pagesCambridge Assessment International Education: Economics 0455/22 March 2019AhmedNo ratings yet

- Process Audit Vda 63Document9 pagesProcess Audit Vda 63hanifkadekarNo ratings yet

- Project Closure at Post Project Review Template (Hnrae)Document4 pagesProject Closure at Post Project Review Template (Hnrae)3212 Borlagdatan, Johnrae B.No ratings yet

- Business PlanDocument34 pagesBusiness PlanAli Mudenyo MwinyiNo ratings yet

- Unveiling The Starbucks-Spotify CollaborationDocument12 pagesUnveiling The Starbucks-Spotify Collaborationcollinsmacharia99No ratings yet

- Part - A: Generic Information: Application For Registration As GST Dealer (See Rule 7 (A) )Document5 pagesPart - A: Generic Information: Application For Registration As GST Dealer (See Rule 7 (A) )rajnikant kukretiNo ratings yet

- Form 30Document1 pageForm 30Mohammad AkilNo ratings yet

- Mini Project - NANO LEARNINGDocument50 pagesMini Project - NANO LEARNINGAnkit ChourasiaNo ratings yet

- How Do You Promate Our Traditional Games To OthersDocument1 pageHow Do You Promate Our Traditional Games To Othersjade3208No ratings yet

- 3.1 Specialist Domination (Niche Selection)Document9 pages3.1 Specialist Domination (Niche Selection)Lynx OP GamingNo ratings yet

- Coffee CabanaDocument10 pagesCoffee CabanaAbhay Kumar SinghNo ratings yet

- PESTEL - Consolidated VersionDocument9 pagesPESTEL - Consolidated Versiontanmaya_purohitNo ratings yet

- Intro 3Document14 pagesIntro 3Zack ZhangNo ratings yet

- Country Financing Roadmap For The SDGS: Saint Lucia: Insight Report December 2021Document43 pagesCountry Financing Roadmap For The SDGS: Saint Lucia: Insight Report December 2021Christopher WyattNo ratings yet

- Alejandro Fernandez 2Document2 pagesAlejandro Fernandez 2afdez100No ratings yet

- Material Safety Data Sheet - Reach' 1907/2006: Cas Number Product Name Content Symbols R PhrasesDocument4 pagesMaterial Safety Data Sheet - Reach' 1907/2006: Cas Number Product Name Content Symbols R PhrasesnghiaNo ratings yet

- Business Case Study Report ENT300Document16 pagesBusiness Case Study Report ENT300rozanah abu100% (2)

- Community Relations CHAPTER ONEDocument20 pagesCommunity Relations CHAPTER ONEAdewuyi Alani RidwanNo ratings yet

- STCQCAA Class Reps Assembly 2018Document42 pagesSTCQCAA Class Reps Assembly 2018STCQC Alumnae AssociationNo ratings yet

- Ypvpgwl15ypvpgwl15-Study Material-202005110828pm028364-Science 1-1Document5 pagesYpvpgwl15ypvpgwl15-Study Material-202005110828pm028364-Science 1-1AnantNo ratings yet

- Raja Metal Catalog October 2022-3Document32 pagesRaja Metal Catalog October 2022-3Tanvir Ahmed Khan0% (1)

- The Effect of Benefits Offered and Customer Experience On Re-Use Intention of Mobile Banking Through Customer Satisfaction and TrustDocument19 pagesThe Effect of Benefits Offered and Customer Experience On Re-Use Intention of Mobile Banking Through Customer Satisfaction and TrustViaNo ratings yet

- The Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseFrom EverandThe Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseNo ratings yet

- Contract Law for Serious Entrepreneurs: Know What the Attorneys KnowFrom EverandContract Law for Serious Entrepreneurs: Know What the Attorneys KnowRating: 1 out of 5 stars1/5 (1)

- A Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsFrom EverandA Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsNo ratings yet

- Learn the Essentials of Business Law in 15 DaysFrom EverandLearn the Essentials of Business Law in 15 DaysRating: 4 out of 5 stars4/5 (13)

- Law of Contract Made Simple for LaymenFrom EverandLaw of Contract Made Simple for LaymenRating: 4.5 out of 5 stars4.5/5 (9)

- Legal Forms for Everyone: Leases, Home Sales, Avoiding Probate, Living Wills, Trusts, Divorce, Copyrights, and Much MoreFrom EverandLegal Forms for Everyone: Leases, Home Sales, Avoiding Probate, Living Wills, Trusts, Divorce, Copyrights, and Much MoreRating: 3.5 out of 5 stars3.5/5 (2)

- The Perfect Stage Crew: The Complete Technical Guide for High School, College, and Community TheaterFrom EverandThe Perfect Stage Crew: The Complete Technical Guide for High School, College, and Community TheaterNo ratings yet

- Contracts: The Essential Business Desk ReferenceFrom EverandContracts: The Essential Business Desk ReferenceRating: 4 out of 5 stars4/5 (15)

- How to Win Your Case In Traffic Court Without a LawyerFrom EverandHow to Win Your Case In Traffic Court Without a LawyerRating: 4 out of 5 stars4/5 (5)

- Legal Guide to Social Media, Second Edition: Rights and Risks for Businesses, Entrepreneurs, and InfluencersFrom EverandLegal Guide to Social Media, Second Edition: Rights and Risks for Businesses, Entrepreneurs, and InfluencersRating: 5 out of 5 stars5/5 (1)

- Fundamentals of Theatrical Design: A Guide to the Basics of Scenic, Costume, and Lighting DesignFrom EverandFundamentals of Theatrical Design: A Guide to the Basics of Scenic, Costume, and Lighting DesignRating: 3.5 out of 5 stars3.5/5 (3)

- How to Win Your Case in Small Claims Court Without a LawyerFrom EverandHow to Win Your Case in Small Claims Court Without a LawyerRating: 5 out of 5 stars5/5 (1)

- Digital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetFrom EverandDigital Technical Theater Simplified: High Tech Lighting, Audio, Video and More on a Low BudgetNo ratings yet

- Crash Course Business Agreements and ContractsFrom EverandCrash Course Business Agreements and ContractsRating: 3 out of 5 stars3/5 (3)

- What Are You Laughing At?: How to Write Humor for Screenplays, Stories, and MoreFrom EverandWhat Are You Laughing At?: How to Write Humor for Screenplays, Stories, and MoreRating: 4 out of 5 stars4/5 (2)