You might also like

- Lesson 17 - Communication For Business Purposes - Writing ReportsDocument29 pagesLesson 17 - Communication For Business Purposes - Writing ReportsKenneth Gail Virrey100% (1)

- Intelligence Analysis UK NVQ (OU)Document37 pagesIntelligence Analysis UK NVQ (OU)laptopuk0% (2)

- Summarized of Valuation ReportDocument9 pagesSummarized of Valuation ReportRahel SorriNo ratings yet

- Feasibility ReportDocument4 pagesFeasibility ReportMunashe NyayaNo ratings yet

- Evaluation Report Deliverable Description: Standards For Evaluation For The UN SystemDocument6 pagesEvaluation Report Deliverable Description: Standards For Evaluation For The UN SystemPipeco SyahmieNo ratings yet

- Lecture#18: Reports & Proposals Lecture Notes What Is A Report?Document6 pagesLecture#18: Reports & Proposals Lecture Notes What Is A Report?Hazma FareedNo ratings yet

- Technical Writing Chapter-02: "Writing Comes More Easily If You Have Something To Say." - Sholem AschDocument29 pagesTechnical Writing Chapter-02: "Writing Comes More Easily If You Have Something To Say." - Sholem AschHema NairNo ratings yet

- MODULE-4 RM Vipul 2Document18 pagesMODULE-4 RM Vipul 2ritz meshNo ratings yet

- Chương 2 - KTHĐ-SVDocument57 pagesChương 2 - KTHĐ-SVNGỌC ĐỖ TRẦN BỘINo ratings yet

- Understand Appraisal 1109 PDFDocument18 pagesUnderstand Appraisal 1109 PDFrubydelacruzNo ratings yet

- Appraisal Report WritingDocument40 pagesAppraisal Report WritingLuningning Carios100% (4)

- How To Write Impactful Audit ReportDocument26 pagesHow To Write Impactful Audit ReportOpeyemi OlomolaNo ratings yet

- 1b. Writing Terms of Reference For An EvaluationDocument32 pages1b. Writing Terms of Reference For An EvaluationAle CevallosNo ratings yet

- Writing ToR For An Evaluation (2004)Document4 pagesWriting ToR For An Evaluation (2004)Tukang UsilNo ratings yet

- Audience Purpose Summaries: Framework For Success. South-Western College Publishing, 2001)Document5 pagesAudience Purpose Summaries: Framework For Success. South-Western College Publishing, 2001)Saleem RazaNo ratings yet

- Minor Project On Sbi (Data)Document2 pagesMinor Project On Sbi (Data)harshityagnik20No ratings yet

- Valuation Testing ModuleDocument58 pagesValuation Testing ModuleRafael SoroNo ratings yet

- Feasibility Report Parts and FunctionDocument12 pagesFeasibility Report Parts and FunctionAldrian Ala75% (4)

- Definition of ReportDocument41 pagesDefinition of ReportXinNo ratings yet

- OSH5005EP Safety Audit and Inspection Chapter 8Document33 pagesOSH5005EP Safety Audit and Inspection Chapter 8Eva HuiNo ratings yet

- 2Document1 page2amirophobiaNo ratings yet

- Feasibility Study ConfectioneriesDocument3 pagesFeasibility Study Confectioneriesomoetusi.okojieNo ratings yet

- SIP GuidelinesDocument15 pagesSIP GuidelinesNidhi NairNo ratings yet

- Writing The Research ReportDocument13 pagesWriting The Research ReportMichael Angelo Dela TorreNo ratings yet

- Moke 377777 OkDocument98 pagesMoke 377777 Okmekonnin tadesseNo ratings yet

- Root Cause Analysis and Critical Thought: July 19, 2012Document24 pagesRoot Cause Analysis and Critical Thought: July 19, 2012KushNo ratings yet

- Understand Appraisal 1109 PDFDocument18 pagesUnderstand Appraisal 1109 PDFwmorreNo ratings yet

- Nattaporn - BSBMKG506 Plan Market Research Learner Assessments - ReviseDocument13 pagesNattaporn - BSBMKG506 Plan Market Research Learner Assessments - ReviseOpal Ploykwhan UdonchaisirikunNo ratings yet

- Chapter ThreeDocument15 pagesChapter ThreeYasinNo ratings yet

- Active Equity Management - Compress PDFDocument435 pagesActive Equity Management - Compress PDFdnajkdfNo ratings yet

- 172-009-0-415 MKT Research Group AssignmentDocument15 pages172-009-0-415 MKT Research Group AssignmentMourin ElaNo ratings yet

- Topic 2 - Report WritingDocument7 pagesTopic 2 - Report WritingAnum Kamal100% (1)

- 11-15 TRW Assignment.Document8 pages11-15 TRW Assignment.Kamran JUTTNo ratings yet

- Evaluation Report TemplateDocument6 pagesEvaluation Report Templatenifras1234No ratings yet

- MAS Practice Standards-SumDocument4 pagesMAS Practice Standards-SumJan Mari RabenaNo ratings yet

- Mancon Outline PDFDocument5 pagesMancon Outline PDFIrra May GanotNo ratings yet

- FilesDocument77 pagesFilesbarbie robertsNo ratings yet

- Feasibility ReportDocument15 pagesFeasibility ReportSainyam JainNo ratings yet

- 8533Document12 pages8533NehaAliNo ratings yet

- ABE 502 Principles of Agro - Ind MGT - SectionBDocument28 pagesABE 502 Principles of Agro - Ind MGT - SectionBkassyNo ratings yet

- Data Analysis FindingsDocument11 pagesData Analysis FindingsMulya Fajar RahmawanNo ratings yet

- Descriptive, Normative, and Cause-Effect Evaluation Designs: Ipdet HandbookDocument47 pagesDescriptive, Normative, and Cause-Effect Evaluation Designs: Ipdet HandbookJessien KateNo ratings yet

- Reports AssignmentDocument10 pagesReports AssignmentTehreem TamannaNo ratings yet

- Chapter 6 - Reporting and Using Evaluation Information SchoolsDocument4 pagesChapter 6 - Reporting and Using Evaluation Information SchoolsrunnahakyuNo ratings yet

- Course Outline Managerial AccountingDocument4 pagesCourse Outline Managerial AccountingbsaccyinstructorNo ratings yet

- Preparing Business ReportsDocument101 pagesPreparing Business ReportsRobinson MojicaNo ratings yet

- COMM 306 Advisory Report Guidelines 2021-22 T3Document5 pagesCOMM 306 Advisory Report Guidelines 2021-22 T3Amtul AyoubNo ratings yet

- Infrastructure Blank BookDocument80 pagesInfrastructure Blank BookVinayak PadaveNo ratings yet

- Logical Framework AnalysisDocument31 pagesLogical Framework AnalysisKaelel Bilang0% (1)

- Governance and Compliance Audit - NotesDocument208 pagesGovernance and Compliance Audit - NotesDanielNo ratings yet

- Management Sciences CurriculumDocument7 pagesManagement Sciences CurriculumUmar SafdarNo ratings yet

- Topic: Business Report: Submitted byDocument25 pagesTopic: Business Report: Submitted byimrul09No ratings yet

- Appraisal Report WritingDocument6 pagesAppraisal Report WritingJen ManriqueNo ratings yet

- SAD Ch3 Aug'19Document36 pagesSAD Ch3 Aug'19Mzewakhe MzamaneNo ratings yet

- Term PaperDocument16 pagesTerm PaperMohammad TayeebNo ratings yet

- Types of Repor 01Document20 pagesTypes of Repor 01Mahmud AhmedNo ratings yet

- Writing ReportsDocument46 pagesWriting ReportsKiều AnhNo ratings yet

- Research Protocol TemplateDocument6 pagesResearch Protocol TemplateAshref BelhajNo ratings yet

- Monitoring and Evaluation Ver 2Document9 pagesMonitoring and Evaluation Ver 2Cookie MonsterNo ratings yet

- Leasing of Plant & Machinery: (2 Marks)Document32 pagesLeasing of Plant & Machinery: (2 Marks)MANNAVAN.T.NNo ratings yet

- Cost APProachDocument40 pagesCost APProachMANNAVAN.T.N100% (1)

- Cost APProachDocument40 pagesCost APProachMANNAVAN.T.NNo ratings yet

- Valuation of P&M - 240920Document24 pagesValuation of P&M - 240920MANNAVAN.T.NNo ratings yet

- Case Laws - Plant & MachineryDocument7 pagesCase Laws - Plant & MachineryMANNAVAN.T.NNo ratings yet

- PM - G - 1 - Valuation of Plant & MachineryDocument6 pagesPM - G - 1 - Valuation of Plant & MachineryMANNAVAN.T.N100% (1)

- Industrial Processes - PresentationDocument58 pagesIndustrial Processes - PresentationMANNAVAN.T.NNo ratings yet

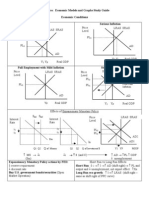

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideAznAlexT90% (21)

- Shoib CV Scaffold EngineerDocument3 pagesShoib CV Scaffold EngineerMohd Shoib100% (1)

- Parking Brake System: SectionDocument16 pagesParking Brake System: SectionEngr Ko VictorNo ratings yet

- Trials Centimeters Where The Ruler Fell Eyes Open Eyes Closed Left Hand Right Hand Left Hand Right Hand 1st 2nd 3rd 4th 5 AverageDocument4 pagesTrials Centimeters Where The Ruler Fell Eyes Open Eyes Closed Left Hand Right Hand Left Hand Right Hand 1st 2nd 3rd 4th 5 Averagerommel rentoriaNo ratings yet

- Indefinite Integration (Practice Question)Document23 pagesIndefinite Integration (Practice Question)Архи́пNo ratings yet

- Lesson 1 Poster AnalysisDocument5 pagesLesson 1 Poster AnalysisJanvi PatelNo ratings yet

- Types of Forces: Previously in This LessonDocument3 pagesTypes of Forces: Previously in This LessonRayyanNo ratings yet

- Tunnel EngineeringDocument53 pagesTunnel EngineeringshankaregowdaNo ratings yet

- CDI Format Full Specification PDFDocument1,000 pagesCDI Format Full Specification PDFmmffernandezNo ratings yet

- S7 Communication Between SIMATIC S7-1500 and SIMATIC S7-300: Step 7 V16 / Bsend / BRCVDocument45 pagesS7 Communication Between SIMATIC S7-1500 and SIMATIC S7-300: Step 7 V16 / Bsend / BRCV9226355166No ratings yet

- CNC - How To Build A - Router Part 1, 2 and 3 PDFDocument11 pagesCNC - How To Build A - Router Part 1, 2 and 3 PDFfjagorNo ratings yet

- Robert CapaDocument9 pagesRobert Capaapi-319825916No ratings yet

- Kinematics 2D (Projectile Motion) - NEET Previous Year Question With Complete SolutionDocument4 pagesKinematics 2D (Projectile Motion) - NEET Previous Year Question With Complete SolutionrevathyNo ratings yet

- Cambodia ICTDocument31 pagesCambodia ICTPhearun PayNo ratings yet

- Generating EquipmentDocument15 pagesGenerating EquipmentRajendra Lal ShresthaNo ratings yet

- Pipe Wrinkle Study-Final ReportDocument74 pagesPipe Wrinkle Study-Final Reportjafarimehdi17No ratings yet

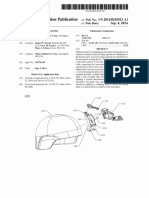

- US20140245523-Helmet Mountuing Systems - Kopia PDFDocument22 pagesUS20140245523-Helmet Mountuing Systems - Kopia PDFja2ja1No ratings yet

- Morpheus SoftDocument14 pagesMorpheus SoftTj NishaaNo ratings yet

- Philosophy in LifeDocument1 pagePhilosophy in LifeOuelle EvansNo ratings yet

- Worksheet16 Transcription To TranslationDocument3 pagesWorksheet16 Transcription To Translationliterally deadNo ratings yet

- Soda Ash MsdsDocument4 pagesSoda Ash MsdsDave ToExtremeNo ratings yet

- L&T - PBQ - 8 L Bengaluru Ring Road Project - HighwaysDocument12 pagesL&T - PBQ - 8 L Bengaluru Ring Road Project - HighwayskanagarajodishaNo ratings yet

- Escala TimpDocument8 pagesEscala TimpLucy GonzalesNo ratings yet

- CH 11 Admission, Discharge, Transfers & ReferralsDocument14 pagesCH 11 Admission, Discharge, Transfers & ReferralsNilakshi Barik Mandal100% (1)

- Teach Yourself EmbryologyDocument15 pagesTeach Yourself EmbryologySambili Tonny100% (2)

- 2016 Challenger CAT 01.pdfDocument81 pages2016 Challenger CAT 01.pdfAditya SuruNo ratings yet

- Time SchedjuleDocument1 pageTime Schedjulebass_121085477No ratings yet

- Desert Sun Arts & Entertainment Oct. 27, Nov. 3 2019Document22 pagesDesert Sun Arts & Entertainment Oct. 27, Nov. 3 2019julie makinenNo ratings yet

- Xii Physics Experiment 1Document5 pagesXii Physics Experiment 1Solomon Peter SunilNo ratings yet

- Vocational Training EmploymentDocument99 pagesVocational Training EmploymentHemant KumarNo ratings yet