You might also like

- New Materi#4 Risk Management ProcessDocument17 pagesNew Materi#4 Risk Management ProcessKavin Biridho Al-HaqNo ratings yet

- Quality Assurance MappingDocument1 pageQuality Assurance MappingArtoToroNo ratings yet

- 2019 FCM Cookbook 2019 May 09 PDFDocument18 pages2019 FCM Cookbook 2019 May 09 PDFJames HurstNo ratings yet

- 10 Firstgroup Annual Report 2023 Risk ManagementDocument9 pages10 Firstgroup Annual Report 2023 Risk ManagementSHERIEFNo ratings yet

- Section 3: Appendix: 1. Audit Checklist: Risk Management ProcessDocument3 pagesSection 3: Appendix: 1. Audit Checklist: Risk Management Processpgupta101No ratings yet

- Fig5 Risk Control CategoriesDocument1 pageFig5 Risk Control CategoriesAmit RajoriaNo ratings yet

- KPMG Risk Management Survey 2011 1 PDFDocument36 pagesKPMG Risk Management Survey 2011 1 PDFVansh Agarwal100% (1)

- Enterprise Risk ManagementDocument6 pagesEnterprise Risk ManagementcoleenNo ratings yet

- ISO31000:2009 and Principles For Managing RiskDocument2 pagesISO31000:2009 and Principles For Managing RiskPatrick Ow100% (2)

- APMM Risk ManagementDocument4 pagesAPMM Risk ManagementsunnyNo ratings yet

- Construction Risk Management ProcessDocument77 pagesConstruction Risk Management ProcessJebat DerhakaNo ratings yet

- Three Lines of Defense FullDocument1 pageThree Lines of Defense FullPremNo ratings yet

- Subject Area No. 22: Risk Assessment & ManagementDocument5 pagesSubject Area No. 22: Risk Assessment & ManagementHarman SandhuNo ratings yet

- Communicating Information Security Risk Simply and Effectively, Part 1Document7 pagesCommunicating Information Security Risk Simply and Effectively, Part 1sashiNo ratings yet

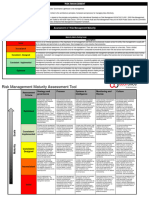

- Risk Management Maturity and Toolkit September 2015Document2 pagesRisk Management Maturity and Toolkit September 2015muratandac3357No ratings yet

- GROUP 2 Risk AssessmentDocument62 pagesGROUP 2 Risk AssessmentAimee UdarbeNo ratings yet

- FRM 1 - PDFDocument19 pagesFRM 1 - PDFIsaacNo ratings yet

- Management Society (Rims) Dalam AnalisisDocument9 pagesManagement Society (Rims) Dalam AnalisisandrianioktafNo ratings yet

- Risk Assessments111 PDFDocument14 pagesRisk Assessments111 PDFMeina ShengNo ratings yet

- Presentations 2021 11Document14 pagesPresentations 2021 11huykhiemNo ratings yet

- Risk Management ReportDocument9 pagesRisk Management Reportkhaoula lahciniNo ratings yet

- Dbs Annual Report 2022 Risk ManagementDocument9 pagesDbs Annual Report 2022 Risk ManagementGouravAgarwalNo ratings yet

- Annex II - Reference Maturity Model For Risk Management (Ii) Summary MatrixDocument2 pagesAnnex II - Reference Maturity Model For Risk Management (Ii) Summary MatrixisolongNo ratings yet

- Reducing Subjectivity Qualitative Risk Assessments 2014Document13 pagesReducing Subjectivity Qualitative Risk Assessments 2014AbhiNo ratings yet

- Risk ManagementDocument3 pagesRisk ManagementMonica GunnacaoNo ratings yet

- Risk Management PolicyDocument2 pagesRisk Management PolicyAkhilesh MehtaNo ratings yet

- Guidance Risk AnalysisDocument23 pagesGuidance Risk AnalysisandreaNo ratings yet

- Ecuador Risk ManagementDocument13 pagesEcuador Risk ManagementzakeoecNo ratings yet

- Managing Risk On Future Building Projects: Case Study Alex TimocDocument10 pagesManaging Risk On Future Building Projects: Case Study Alex TimocAlex TimocNo ratings yet

- (IIA UK) - Position Statement - RIsk Based Internal AuditingDocument4 pages(IIA UK) - Position Statement - RIsk Based Internal Auditingsfakhrurrozi44No ratings yet

- How Risky Is Your: Risk Assessment?Document3 pagesHow Risky Is Your: Risk Assessment?AleAle100% (1)

- Risk Assessment and Risk Treatment - BroadleafDocument10 pagesRisk Assessment and Risk Treatment - BroadleafpriyankaNo ratings yet

- GERMIC Risk ManagementDocument14 pagesGERMIC Risk ManagementCiana SacdalanNo ratings yet

- Measuring Risk Management Maturity at Maninjau Hydropower PlantDocument9 pagesMeasuring Risk Management Maturity at Maninjau Hydropower Plantfauzan datasheetNo ratings yet

- 2019 Risk Management Framework V6 2019.11.29 FINALDocument15 pages2019 Risk Management Framework V6 2019.11.29 FINALJhan Edwards Pasiolan RectoNo ratings yet

- Draft Prudential Practice Guide: CPG 220 - Risk ManagementDocument20 pagesDraft Prudential Practice Guide: CPG 220 - Risk ManagementLord KrusaderNo ratings yet

- Official - Erm Report Main Content - Group 4Document23 pagesOfficial - Erm Report Main Content - Group 4Callum LightNo ratings yet

- Analyze Risks Management Plan Module 8Document1 pageAnalyze Risks Management Plan Module 8Jaira Mae DiazNo ratings yet

- ERM Summary: Established Risk ManagementDocument4 pagesERM Summary: Established Risk ManagementCISA PwCNo ratings yet

- CISM 15e Domain 2Document114 pagesCISM 15e Domain 2neeldxtNo ratings yet

- KWSP2 - Taklimat Di Intan 300610Document21 pagesKWSP2 - Taklimat Di Intan 300610rml1804No ratings yet

- Enterprise Risk Management FrameworkDocument2 pagesEnterprise Risk Management FrameworkalkalkiaNo ratings yet

- Enterprise Risk Management FrameworkDocument2 pagesEnterprise Risk Management FrameworkShrawan Jha100% (2)

- Analyzing Construction Project Risks with Post-Mortem ReviewsDocument9 pagesAnalyzing Construction Project Risks with Post-Mortem ReviewsMatthieu PotesNo ratings yet

- Get Certified As An ISO 31000 Risk Manager To Advance Your SkillsDocument2 pagesGet Certified As An ISO 31000 Risk Manager To Advance Your SkillsGSDC CouncilNo ratings yet

- Risk Management ProcessDocument5 pagesRisk Management Processatiq100% (1)

- Identifying and Managing Our Risks: Risk SummaryDocument2 pagesIdentifying and Managing Our Risks: Risk SummaryAmu Mohan MohanNo ratings yet

- Risk Management - Procurement - Toolkit - 0Document16 pagesRisk Management - Procurement - Toolkit - 0H ZNo ratings yet

- Event Risk Management Plan TemplateDocument1 pageEvent Risk Management Plan TemplateMohammed OsmanNo ratings yet

- Msa_qsp_01_risk Assessment and Mitigation PlanDocument11 pagesMsa_qsp_01_risk Assessment and Mitigation PlanVasudevan GovindarajNo ratings yet

- HSE Risk ManagementDocument9 pagesHSE Risk ManagementSamuelFarfanNo ratings yet

- Working at Heights Risk AssessmentDocument7 pagesWorking at Heights Risk Assessmentshaibaz chafekarNo ratings yet

- Nist CSWP 04162018Document7 pagesNist CSWP 04162018Paul Ryan BalonNo ratings yet

- RMC InfoSheet21 ENDocument1 pageRMC InfoSheet21 ENjdyxg7tzmvNo ratings yet

- Three Lines of Defense To Enhance Technology Risk Management MaturityDocument6 pagesThree Lines of Defense To Enhance Technology Risk Management Maturitypadmapriya deenadayalanNo ratings yet

- Risk Managment Matrice 3x3 enDocument17 pagesRisk Managment Matrice 3x3 enKavitha G3No ratings yet

- 13 - Risk Program Maturity AssessmentDocument2 pages13 - Risk Program Maturity AssessmentSuleyman S. GulcanNo ratings yet

- Risk-Based Management of Rotating EquipmentDocument8 pagesRisk-Based Management of Rotating EquipmentalNo ratings yet

- Managing Risk Within A Decision Analysis FrameworkDocument9 pagesManaging Risk Within A Decision Analysis FrameworkSaileshNo ratings yet

- 01 IntroDocument21 pages01 Introwiwid permamaNo ratings yet

- National ML TF Risk Assessment PDFDocument60 pagesNational ML TF Risk Assessment PDFAna GsNo ratings yet

- 2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next EnronDocument7 pages2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next Enronwiwid permamaNo ratings yet

- Kalender Masehi 2021 PDFDocument12 pagesKalender Masehi 2021 PDFBudiNo ratings yet

- 2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next EnronDocument7 pages2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next Enronwiwid permamaNo ratings yet

- Sanction GuidelinesDocument115 pagesSanction GuidelinesShawnDurraniNo ratings yet

- 07 General Anti Fraud Controls Entity LevelDocument17 pages07 General Anti Fraud Controls Entity Levelwiwid permamaNo ratings yet

- 5a 7a Dan TannebaumDocument46 pages5a 7a Dan Tannebaumaras54No ratings yet

- 2.5 Practial Guides - Common Ethic Code ProvisionsDocument2 pages2.5 Practial Guides - Common Ethic Code Provisionswiwid permamaNo ratings yet

- 2.7 Practical Guides - The PLUS Decision Making ModelDocument2 pages2.7 Practical Guides - The PLUS Decision Making Modelwiwid permamaNo ratings yet

- 2.4 Practical Guides - Code Construction and ContentDocument1 page2.4 Practical Guides - Code Construction and Contentwiwid permamaNo ratings yet

- 2.2 Practical Guides - Definitions of ValuesDocument10 pages2.2 Practical Guides - Definitions of Valueswiwid permamaNo ratings yet

- 2.6 Practical Guides - Ten Writing Tips For Creating An Effective Code of ConductsDocument3 pages2.6 Practical Guides - Ten Writing Tips For Creating An Effective Code of Conductswiwid permamaNo ratings yet

- 2.4 Practical Guides - Code Construction and ContentDocument1 page2.4 Practical Guides - Code Construction and Contentwiwid permamaNo ratings yet

- 2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next EnronDocument7 pages2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next Enronwiwid permamaNo ratings yet

- 2.3 Practical Guides - Why Have A Code of ConductDocument1 page2.3 Practical Guides - Why Have A Code of Conductwiwid permamaNo ratings yet

- ETHICS GLOSSARY TERMSDocument7 pagesETHICS GLOSSARY TERMSwiwid permamaNo ratings yet

- 2.2 Practical Guides - Definitions of ValuesDocument10 pages2.2 Practical Guides - Definitions of Valueswiwid permamaNo ratings yet

- 2.5 Practial Guides - Common Ethic Code ProvisionsDocument2 pages2.5 Practial Guides - Common Ethic Code Provisionswiwid permamaNo ratings yet

- ETHICS GLOSSARY TERMSDocument7 pagesETHICS GLOSSARY TERMSwiwid permamaNo ratings yet

- 2.2 Practical Guides - Definitions of ValuesDocument10 pages2.2 Practical Guides - Definitions of Valueswiwid permamaNo ratings yet

- Fraud Risk Management: © 2018 Association of Certified Fraud Examiners, IncDocument43 pagesFraud Risk Management: © 2018 Association of Certified Fraud Examiners, Incwiwid permamaNo ratings yet

- 2.3 Practical Guides - Why Have A Code of ConductDocument1 page2.3 Practical Guides - Why Have A Code of Conductwiwid permamaNo ratings yet

- 2.6 Practical Guides - Ten Writing Tips For Creating An Effective Code of ConductsDocument3 pages2.6 Practical Guides - Ten Writing Tips For Creating An Effective Code of Conductswiwid permamaNo ratings yet

- 5.2 The Fairness Approach - How To Use The Justice or Fairness TestDocument2 pages5.2 The Fairness Approach - How To Use The Justice or Fairness Testwiwid permamaNo ratings yet

- 2.7 Practical Guides - The PLUS Decision Making ModelDocument2 pages2.7 Practical Guides - The PLUS Decision Making Modelwiwid permamaNo ratings yet

- 2.4 Practical Guides - Code Construction and ContentDocument1 page2.4 Practical Guides - Code Construction and Contentwiwid permamaNo ratings yet

- 2.3 Practical Guides - Why Have A Code of ConductDocument1 page2.3 Practical Guides - Why Have A Code of Conductwiwid permamaNo ratings yet

- 2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next EnronDocument7 pages2.8 Practical Guides - Ten Things You Can Do To Avoid Being The Next Enronwiwid permamaNo ratings yet

- Human Resource Information System (SunFish HR SaaS)Document13 pagesHuman Resource Information System (SunFish HR SaaS)sndpalur krgNo ratings yet

- Case Study Legal Forms of BusinessDocument5 pagesCase Study Legal Forms of BusinessRica BañaresNo ratings yet

- Functional Area of Management-2Document79 pagesFunctional Area of Management-2Ketan VibgyorNo ratings yet

- Bip 2149-2008Document272 pagesBip 2149-2008ali rabieeNo ratings yet

- Slomins Home Heating Oil ServiceDocument2 pagesSlomins Home Heating Oil ServiceRohin Cookie SharmaNo ratings yet

- Tinywow - Unit 1 Assignment 2 Exploring Businesses - 6114684Document54 pagesTinywow - Unit 1 Assignment 2 Exploring Businesses - 6114684ali MuradNo ratings yet

- Hea Ignitor ManualDocument124 pagesHea Ignitor ManualYogesh PandeyNo ratings yet

- 4 Financial Management ND2020Document4 pages4 Financial Management ND2020Srikrishna DharNo ratings yet

- Sherefa Husein PaperDocument35 pagesSherefa Husein Paperkassahun mesele100% (1)

- Full Download Advanced Accounting 6th Edition Jeter Test BankDocument35 pagesFull Download Advanced Accounting 6th Edition Jeter Test Bankjacksongubmor100% (40)

- Case Study Columbus InstrumentsDocument8 pagesCase Study Columbus Instrumentsramji100% (6)

- CP Shipping Desk 2018Document18 pagesCP Shipping Desk 2018Farid OMARINo ratings yet

- Seamless Marketo - Google Analytics Integration: Cheat SheetDocument7 pagesSeamless Marketo - Google Analytics Integration: Cheat SheetWill ChouNo ratings yet

- Introduction of OngcDocument11 pagesIntroduction of OngcPIYUSH RAWAT100% (2)

- Business Ethics Q4 Mod4 Introduction To The Notion of Social Enterprise-V3Document29 pagesBusiness Ethics Q4 Mod4 Introduction To The Notion of Social Enterprise-V3Charmian100% (1)

- Customer Satisfaction and Brand Loyalty in Big BasketDocument73 pagesCustomer Satisfaction and Brand Loyalty in Big BasketUpadhayayAnkurNo ratings yet

- Autocratic Leadership Style of Henry Ford 1.1. DefinitionDocument3 pagesAutocratic Leadership Style of Henry Ford 1.1. DefinitionThảo Ngọc100% (2)

- Conventional Milling Machine Into CNC MachineDocument18 pagesConventional Milling Machine Into CNC MachineEverAngelNo ratings yet

- OpenSAP Genai1 Unit 02 Introgenai PresentationDocument12 pagesOpenSAP Genai1 Unit 02 Introgenai Presentationjpdbtptrial123No ratings yet

- Licence Conditions and Codes of PracticeDocument80 pagesLicence Conditions and Codes of PracticeEric GarciaNo ratings yet

- Acct 2251 Enlarged Review Qs Final ExamW07Document9 pagesAcct 2251 Enlarged Review Qs Final ExamW07hatanolove100% (1)

- Data Science 101: An Introduction to Fundamentals, Use Cases, and the Data Science ProcessDocument23 pagesData Science 101: An Introduction to Fundamentals, Use Cases, and the Data Science ProcessVijay BhemalNo ratings yet

- Solarwinds Technical Reference: Polled Object Identifiers For Orion NPM, Orion Nta, and Orion Ip Sla ManagerDocument16 pagesSolarwinds Technical Reference: Polled Object Identifiers For Orion NPM, Orion Nta, and Orion Ip Sla ManagerAngelo JacosalemNo ratings yet

- Sample Questions MBADocument8 pagesSample Questions MBAMike McclainNo ratings yet

- Financial Reporting Council Guidance On Audit Committees: AppendixDocument14 pagesFinancial Reporting Council Guidance On Audit Committees: AppendixnmamNo ratings yet

- Saudi Aramco Port and Terminal Booklet 2020 PDFDocument384 pagesSaudi Aramco Port and Terminal Booklet 2020 PDFmersail100% (1)

- PWC Sharing Economy Report 2015 PDFDocument30 pagesPWC Sharing Economy Report 2015 PDFIván R. MinuttiNo ratings yet

- Lesson 4Document21 pagesLesson 4Đoàn Ngọc DũngNo ratings yet

- Get Download All Report - 27ADMPJ5260G1ZG - 2023 - 2024Document26 pagesGet Download All Report - 27ADMPJ5260G1ZG - 2023 - 2024ajay.patelNo ratings yet

- New Tablet Menu Project CharterDocument3 pagesNew Tablet Menu Project CharterBasit Ali QureshiNo ratings yet