You might also like

- Industrial Estate Snapshot: Q3 2014 Greater Jakarta, IndonesiaDocument1 pageIndustrial Estate Snapshot: Q3 2014 Greater Jakarta, IndonesiaCookiesNo ratings yet

- Jakarta Ind 1q16Document2 pagesJakarta Ind 1q16JarjitUpinIpinJarjitNo ratings yet

- 2019 Q3 CushWake Jakarta IndustrialDocument2 pages2019 Q3 CushWake Jakarta IndustrialCookiesNo ratings yet

- Mumbai Office Marketbeat 3Q 2014Document2 pagesMumbai Office Marketbeat 3Q 2014khansahil.1331No ratings yet

- 2019 Q1 CushWake Jakarta IndustrialDocument2 pages2019 Q1 CushWake Jakarta IndustrialCookiesNo ratings yet

- Bengaluru Retail 4q16Document2 pagesBengaluru Retail 4q16Surya ReddyNo ratings yet

- PropIndex JAS'23 - FinalDocument72 pagesPropIndex JAS'23 - Finalabhishek.bhadraNo ratings yet

- FOCUS - Indofood Sukses Makmur: Saved by The GreenDocument10 pagesFOCUS - Indofood Sukses Makmur: Saved by The GreenriskaNo ratings yet

- 2019 Q2 CushWake Jakarta IndustrialDocument2 pages2019 Q2 CushWake Jakarta IndustrialCookiesNo ratings yet

- CHP Col ResearchDocument10 pagesCHP Col ResearchJun GomezNo ratings yet

- CgreDocument5 pagesCgreAnonymous Feglbx5No ratings yet

- Philadelphia Americas MarketBeat Industrial Q32019 PDFDocument2 pagesPhiladelphia Americas MarketBeat Industrial Q32019 PDFAnonymous yMYxjXNo ratings yet

- Qb23q3 en Ch2Document5 pagesQb23q3 en Ch2milvibesupplyNo ratings yet

- Semen Indonesia (Persero) : Slower Sales Volume Reflected On Bottom LineDocument8 pagesSemen Indonesia (Persero) : Slower Sales Volume Reflected On Bottom LineRendy SentosaNo ratings yet

- Investor DigestDocument7 pagesInvestor DigestVerin IchiharaNo ratings yet

- Garware Wall RopesDocument15 pagesGarware Wall RopesbolinjkarvinitNo ratings yet

- Retail Industry Retail Industry Retail IndustryDocument8 pagesRetail Industry Retail Industry Retail IndustryTanmay PokaleNo ratings yet

- Icici Manufacture in India Fund - Investor PDFDocument30 pagesIcici Manufacture in India Fund - Investor PDFkashifbeg786No ratings yet

- Havells India Ltd. - INDSECDocument12 pagesHavells India Ltd. - INDSECResearch ReportsNo ratings yet

- Mumbai Off 3q15Document3 pagesMumbai Off 3q15Pushkar JadhavNo ratings yet

- 2018 Q4 CushWake Jakarta IndustrialDocument2 pages2018 Q4 CushWake Jakarta IndustrialCookiesNo ratings yet

- MIMAROPA 2019 ARES With CoverDocument26 pagesMIMAROPA 2019 ARES With Coverlynda_christineNo ratings yet

- Mumbai Office Marketbeat 1Q 2014Document2 pagesMumbai Office Marketbeat 1Q 2014khansahil.1331No ratings yet

- 2019 Q4 Jakarta Office Market Report ColliersDocument4 pages2019 Q4 Jakarta Office Market Report Colliersluthfi anshariNo ratings yet

- Mumbai Office Marketbeat 2Q 2014Document2 pagesMumbai Office Marketbeat 2Q 2014khansahil.1331No ratings yet

- PropIndex JFM24Document72 pagesPropIndex JFM24prem kumarNo ratings yet

- Industrial Real Estate (Singapore) : Industry OutlookDocument13 pagesIndustrial Real Estate (Singapore) : Industry OutlookElaine YeapNo ratings yet

- Infra-Road Q3FY23 Earnings Preview - 05012023 - 06-01-2023 - 11Document7 pagesInfra-Road Q3FY23 Earnings Preview - 05012023 - 06-01-2023 - 11Karthi KeyanNo ratings yet

- Supreme Industries LTD Hold: Retail Equity ResearchDocument5 pagesSupreme Industries LTD Hold: Retail Equity ResearchanjugaduNo ratings yet

- Mumbai Office Marketbeat 4Q 2014Document2 pagesMumbai Office Marketbeat 4Q 2014khansahil.1331No ratings yet

- Cargills Ceylon: Date: 6 February 2019Document71 pagesCargills Ceylon: Date: 6 February 2019Janitha Dissanayake100% (1)

- Monthly Bulletin July 2023 EnglishDocument13 pagesMonthly Bulletin July 2023 EnglishNirmal MenonNo ratings yet

- Baltimore Americas MarketBeat Industrial Q22019 PDFDocument2 pagesBaltimore Americas MarketBeat Industrial Q22019 PDFAnonymous 6zS940JNo ratings yet

- Cushman & Wakefield Global Cities Retail GuideDocument9 pagesCushman & Wakefield Global Cities Retail GuideGreen StoneNo ratings yet

- 40 Bangladesh CiplaDocument9 pages40 Bangladesh CiplaPartho MukherjeeNo ratings yet

- Nielsen - A Weakening of Consumer Purchase or ShiftingDocument42 pagesNielsen - A Weakening of Consumer Purchase or ShiftingTotok SediyantoroNo ratings yet

- Semen Indonesia (Persero) : Enabling Future GrowthDocument10 pagesSemen Indonesia (Persero) : Enabling Future GrowthSugeng YuliantoNo ratings yet

- ICICI Prudential Life - 2QFY20 - HDFC Sec-201910231337147517634Document15 pagesICICI Prudential Life - 2QFY20 - HDFC Sec-201910231337147517634sandeeptirukotiNo ratings yet

- GAIL LTD - Q4FY11 Result UpdateDocument3 pagesGAIL LTD - Q4FY11 Result UpdateSeema GusainNo ratings yet

- Ecowrap - 20190830 - Q1fy20 GDP at 25 Quarters LowDocument2 pagesEcowrap - 20190830 - Q1fy20 GDP at 25 Quarters LowSanjoySahaNo ratings yet

- Executive Summary-2020 State of LogisticsDocument10 pagesExecutive Summary-2020 State of LogisticspharssNo ratings yet

- AK Stockmart - ACC - Oct 22, 2010Document4 pagesAK Stockmart - ACC - Oct 22, 2010bharshanNo ratings yet

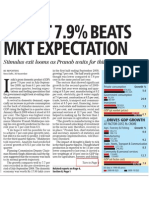

- GDP at 7.9%Document1 pageGDP at 7.9%soumyaranjan_d3393No ratings yet

- Jarir AlRajhi Capital 2023.8Document3 pagesJarir AlRajhi Capital 2023.8robynxjNo ratings yet

- Stock Pointer: Alok Industries LTDDocument20 pagesStock Pointer: Alok Industries LTDGirish RaskarNo ratings yet

- Gatere: Delhi NCR Office MarketDocument13 pagesGatere: Delhi NCR Office MarketPrateek MathurNo ratings yet

- Escorts: Expectation of Significant Recovery Due To A Better Monsoon BuyDocument7 pagesEscorts: Expectation of Significant Recovery Due To A Better Monsoon BuynnsriniNo ratings yet

- Wipro Q4FY09 Result UpdateDocument4 pagesWipro Q4FY09 Result UpdateHardikNo ratings yet

- 2020 11 18 PH e Meg PDFDocument8 pages2020 11 18 PH e Meg PDFJNo ratings yet

- Greenville Americas Alliance MarketBeat Industrial Q22017Document2 pagesGreenville Americas Alliance MarketBeat Industrial Q22017Anonymous Feglbx5No ratings yet

- Q1FY23 - Result Update: Future Growth IntactDocument10 pagesQ1FY23 - Result Update: Future Growth IntactResearch ReportsNo ratings yet

- Ciptadana Company Update ROTI 5 Mar 2024 - Not RatedDocument7 pagesCiptadana Company Update ROTI 5 Mar 2024 - Not RatedCandra AdyastaNo ratings yet

- 2023 Korea Logistics Market Outlook (En) Rev3Document4 pages2023 Korea Logistics Market Outlook (En) Rev3dexterNo ratings yet

- Ciptadana Sekuritas ASRI - Growing Recurring IncomeDocument6 pagesCiptadana Sekuritas ASRI - Growing Recurring Incomebudi handokoNo ratings yet

- 1Q18 Earnings Drop 49.9% Y/y On Lower Revenues, Below COL ForecastDocument6 pages1Q18 Earnings Drop 49.9% Y/y On Lower Revenues, Below COL ForecastMark Angelo BustosNo ratings yet

- Nawaz Sharif Era 2013 - 2017: Presented By: Alysaad HassanDocument11 pagesNawaz Sharif Era 2013 - 2017: Presented By: Alysaad Hassanace rogerNo ratings yet

- Tata Elxsi Limited: Result UpdateDocument6 pagesTata Elxsi Limited: Result UpdateinvestfortestNo ratings yet

- National Bank of Ethiopia 2017-18 Annual ReportDocument106 pagesNational Bank of Ethiopia 2017-18 Annual Reportsamuel seifu100% (1)

- Competition Law and Economic Regulation in Southern Africa: Addressing Market Power in Southern AfricaFrom EverandCompetition Law and Economic Regulation in Southern Africa: Addressing Market Power in Southern AfricaNo ratings yet

- Bangladesh Quarterly Economic Update: September 2014From EverandBangladesh Quarterly Economic Update: September 2014No ratings yet

- 2020 Q3 CushWake Jakarta IndustrialDocument2 pages2020 Q3 CushWake Jakarta IndustrialCookiesNo ratings yet

- 2020 Q2 CushWake Jakarta IndustrialDocument2 pages2020 Q2 CushWake Jakarta IndustrialCookiesNo ratings yet

- 2018 Q4 CushWake Jakarta IndustrialDocument2 pages2018 Q4 CushWake Jakarta IndustrialCookiesNo ratings yet

- Greater Jakarta: Industrial Q1 2020Document2 pagesGreater Jakarta: Industrial Q1 2020CookiesNo ratings yet

- 2020 Q3 CushWake Jakarta IndustrialDocument2 pages2020 Q3 CushWake Jakarta IndustrialCookiesNo ratings yet

- 2020 Q2 CushWake Jakarta IndustrialDocument2 pages2020 Q2 CushWake Jakarta IndustrialCookiesNo ratings yet

- Greater Jakarta: Industrial Q4 2019Document2 pagesGreater Jakarta: Industrial Q4 2019CookiesNo ratings yet

- 2019 Q2 CushWake Jakarta IndustrialDocument2 pages2019 Q2 CushWake Jakarta IndustrialCookiesNo ratings yet

- Sample Complaint Against California Insurance Company For Bad FaithDocument3 pagesSample Complaint Against California Insurance Company For Bad FaithStan Burman80% (5)

- Fin AcctgDocument9 pagesFin AcctgCarl Angelo0% (1)

- Disruptive TechnologyDocument3 pagesDisruptive TechnologyNeetu GoyalNo ratings yet

- Accounts ProjectDocument5 pagesAccounts ProjectJyotirup SamalNo ratings yet

- AML Presentation & KYC Ver 1.9Document58 pagesAML Presentation & KYC Ver 1.9nehal10100% (1)

- Chapter 2 Service Operations Management-BediDocument17 pagesChapter 2 Service Operations Management-BediSanket ShetyeNo ratings yet

- PhilipsVsMatsushit Case AnalysisDocument7 pagesPhilipsVsMatsushit Case AnalysisGaurav RanjanNo ratings yet

- Problem 5-19Document5 pagesProblem 5-19Phuong ThaoNo ratings yet

- Chiefdissertation 161006221902 PDFDocument59 pagesChiefdissertation 161006221902 PDFManoj Kumar100% (1)

- Population Growth and DevelopmentDocument22 pagesPopulation Growth and DevelopmentKathrine CadalsoNo ratings yet

- Solutions Test Bank For Principles of Managerial Finance 15th Edition by ZutterDocument30 pagesSolutions Test Bank For Principles of Managerial Finance 15th Edition by Zuttergood goodNo ratings yet

- ALUMNI MEET 2023-24 SampleDocument16 pagesALUMNI MEET 2023-24 SampleTamil SelvanNo ratings yet

- Report CEM483 FinalisedDocument53 pagesReport CEM483 FinalisedMohamad HazimNo ratings yet

- Homework On Inventories Problem 1 (Borrowing Cost ConceptsDocument3 pagesHomework On Inventories Problem 1 (Borrowing Cost ConceptsJazehl Joy ValdezNo ratings yet

- CPP PPT Gr-13 FinalDocument21 pagesCPP PPT Gr-13 FinalChetan SonawaneNo ratings yet

- Lone Pine CafeDocument4 pagesLone Pine CafeRahul TiwariNo ratings yet

- A Popular HR Chief Burned To Death: People Management Dynamics atDocument8 pagesA Popular HR Chief Burned To Death: People Management Dynamics at20PGPIB064AKSHAR PANDYA100% (2)

- SAPTP-4058 - CNH Brand Vendor Consignment Process - SAP Estimate v0.4Document13 pagesSAPTP-4058 - CNH Brand Vendor Consignment Process - SAP Estimate v0.4Chandra MathiNo ratings yet

- Intitulé Du Module: Business English Durée de La Formation: 30 Hours Déroulé J1Document5 pagesIntitulé Du Module: Business English Durée de La Formation: 30 Hours Déroulé J1benzidaNo ratings yet

- Logistic OptimizationDocument34 pagesLogistic OptimizationYudie Andre SiswantoNo ratings yet

- Parate EksekusiDocument15 pagesParate EksekusiWanda WandaNo ratings yet

- Bed2110 2124 Mathematics For Economist I Reg SuppDocument4 pagesBed2110 2124 Mathematics For Economist I Reg SuppQelvoh JoxNo ratings yet

- 1 - Finance Short NotesDocument12 pages1 - Finance Short NotesSudhanshu PatelNo ratings yet

- Od 123557026424340000Document1 pageOd 123557026424340000Sahil HasanNo ratings yet

- Royal Enfield Project 36 Organisation StudyDocument45 pagesRoyal Enfield Project 36 Organisation StudyVijay AravindNo ratings yet

- Dokumen PDFDocument21 pagesDokumen PDFMark AlcazarNo ratings yet

- Investor Presentation MARCH 2011: A Global Leader in Integrated Clean Air Solutions For IndustryDocument33 pagesInvestor Presentation MARCH 2011: A Global Leader in Integrated Clean Air Solutions For IndustrymynameisvinnNo ratings yet

- Finance Lecturers by Course and Size UNSWDocument2 pagesFinance Lecturers by Course and Size UNSWhello248No ratings yet

- Ifs GMP Checklist Pac enDocument9 pagesIfs GMP Checklist Pac enCevdet BEŞENNo ratings yet

- Customer Persona and Value PropositionDocument24 pagesCustomer Persona and Value PropositionVishnu KompellaNo ratings yet