You might also like

- Template - Annual Partner Plan 2023 - DefDocument37 pagesTemplate - Annual Partner Plan 2023 - DefYasir SaeedNo ratings yet

- 50 of 2021's Best-Selling Pharmaceuticals - Drug DiscoveryDocument8 pages50 of 2021's Best-Selling Pharmaceuticals - Drug DiscoveryBonnie DebbarmaNo ratings yet

- COVID19-EOI-Procurement-Public Briefing-31082020Document20 pagesCOVID19-EOI-Procurement-Public Briefing-31082020Antonio MoncayoNo ratings yet

- Pakistan Covid Patient AssumptionDocument3 pagesPakistan Covid Patient AssumptionAbdullahNo ratings yet

- ARM AR2021 FINAL-singlesDocument40 pagesARM AR2021 FINAL-singlesYefinadya MfNo ratings yet

- Presentation 1Document19 pagesPresentation 1Mohammad ZargarNo ratings yet

- Biologic Drugs: Black Is The New OrangeDocument194 pagesBiologic Drugs: Black Is The New OrangeTom ChoiNo ratings yet

- Phm234a S005Document18 pagesPhm234a S005Hafiiz OsmanNo ratings yet

- Bus 620 Warrirors PresentationDocument27 pagesBus 620 Warrirors PresentationArju LubnaNo ratings yet

- Optimizing Costs in Pharmaceutical Business and ServicesDocument27 pagesOptimizing Costs in Pharmaceutical Business and ServicesnellcoindopharmaNo ratings yet

- California Workers' Compensation Trends and COVID-19 ImpactDocument26 pagesCalifornia Workers' Compensation Trends and COVID-19 ImpactStanley WangNo ratings yet

- Substance Use Disorder Best Practices 09232019Document44 pagesSubstance Use Disorder Best Practices 09232019anishthNo ratings yet

- Therapeutic Monoclonal Antibodies Approved by FDA in 2020Document2 pagesTherapeutic Monoclonal Antibodies Approved by FDA in 2020asclepiuspdfsNo ratings yet

- Business Plan Analysis - 08 1: SFHN/SJ&G Oxalepsy (Oxcarbazipine300 & 600 MG)Document63 pagesBusiness Plan Analysis - 08 1: SFHN/SJ&G Oxalepsy (Oxcarbazipine300 & 600 MG)Muhammad SalmanNo ratings yet

- Dermatologicals in Singapore: Euromonitor International November 2020Document9 pagesDermatologicals in Singapore: Euromonitor International November 2020Phua Wei TingNo ratings yet

- Diagnostic & Medical Laboratories in The US Industry ReportDocument44 pagesDiagnostic & Medical Laboratories in The US Industry Reportsalmapratyush100% (1)

- The Biopharmaceutical Anomaly: FeatureDocument8 pagesThe Biopharmaceutical Anomaly: FeatureTakaNo ratings yet

- PRICE SURVEY - Vaccines Pricing Audit IndonesiaDocument10 pagesPRICE SURVEY - Vaccines Pricing Audit IndonesiaNur Farahiyah AmalinaNo ratings yet

- Ophthalmic Drugs: Indications and Market LandscapeDocument14 pagesOphthalmic Drugs: Indications and Market LandscapeToàn Nguyễn PhúcNo ratings yet

- CBD Medicinal Cannabis Market 2026Document17 pagesCBD Medicinal Cannabis Market 2026paramorobbenNo ratings yet

- IQ4I Research & Consultancy Published A New Report On Nuclear Medicine/Radiopharmaceuticals Global Market - Forecast To 2027Document10 pagesIQ4I Research & Consultancy Published A New Report On Nuclear Medicine/Radiopharmaceuticals Global Market - Forecast To 2027VinayNo ratings yet

- Food and BeveragesDocument24 pagesFood and BeveragesAnk KeshriNo ratings yet

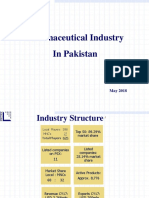

- Pharmaceutical Industry in Pakistan: Industry Structure, Growth Dynamics, and Future OutlookDocument10 pagesPharmaceutical Industry in Pakistan: Industry Structure, Growth Dynamics, and Future OutlookZia ul IslamNo ratings yet

- Macleods Pharmaceuticals - WIPDocument3 pagesMacleods Pharmaceuticals - WIPMinakshi XP23010No ratings yet

- Ipg 2016 Investor Day PresentationDocument122 pagesIpg 2016 Investor Day PresentationyaacovNo ratings yet

- Role of Nano-Biotech in Global Pharma Industry: DR - Pawan SaharanDocument18 pagesRole of Nano-Biotech in Global Pharma Industry: DR - Pawan SaharanGinu GeorgeNo ratings yet

- HC Radnet (RDNT)Document37 pagesHC Radnet (RDNT)Qwerty UiopNo ratings yet

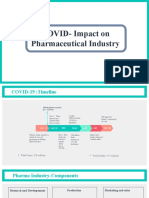

- COVID-Impact On Pharmaceutical IndustryDocument12 pagesCOVID-Impact On Pharmaceutical IndustryAyush GuptaNo ratings yet

- Q1 2023 Results AnnouncementDocument47 pagesQ1 2023 Results AnnouncementVass GergelyNo ratings yet

- $MRIC $VYGR Value Impact AnalysisDocument4 pages$MRIC $VYGR Value Impact AnalysisbiggercapitalNo ratings yet

- Top Companies and Drugs by Sales in 2019: Market WatchDocument1 pageTop Companies and Drugs by Sales in 2019: Market WatchDawit BirhanuNo ratings yet

- SECTOR STUDY-Pharmaceutical APRIL 2020 Kanwal - 1589554722Document13 pagesSECTOR STUDY-Pharmaceutical APRIL 2020 Kanwal - 1589554722Zia ul IslamNo ratings yet

- VACCINES COVID-19 INVIGORATES A STAGNANT INDUSTRYresDocument22 pagesVACCINES COVID-19 INVIGORATES A STAGNANT INDUSTRYresiyad.alsabiNo ratings yet

- Recent M & A in PharmaDocument9 pagesRecent M & A in PharmaSoumya KhanduriNo ratings yet

- Situation Report No.: Tested Confirmed Recovered Dead IsolatedDocument13 pagesSituation Report No.: Tested Confirmed Recovered Dead IsolatedDinar HassanNo ratings yet

- Johnson & Johnson (NYSE: JNJ) Buy Pitch: October 25th, 2017Document18 pagesJohnson & Johnson (NYSE: JNJ) Buy Pitch: October 25th, 2017Rohan JohnNo ratings yet

- Top 10 Global Pharma in 2022Document4 pagesTop 10 Global Pharma in 2022Ade DjatniksNo ratings yet

- 340B ProgramDocument68 pages340B Programapi-26219976No ratings yet

- Global In-Vitro Diagnostics Market - FeasibilityDocument35 pagesGlobal In-Vitro Diagnostics Market - Feasibilitypushpanjali singhNo ratings yet

- IQ4I Research & Consultancy Published A New Report On "Nuclear Medicine/ Radiopharmaceuticals Global Market - Forecast To 2024"Document7 pagesIQ4I Research & Consultancy Published A New Report On "Nuclear Medicine/ Radiopharmaceuticals Global Market - Forecast To 2024"VinayNo ratings yet

- Flagyl Marketing PlanDocument50 pagesFlagyl Marketing Planstring70575% (4)

- Global Lactoferrin Market - Analysis by Application, Function, Distribution Channel, by Region, by Country (2021 Edition) : Market Insights and Forecast With Impact of COVID-19 (2021-2026)Document18 pagesGlobal Lactoferrin Market - Analysis by Application, Function, Distribution Channel, by Region, by Country (2021 Edition) : Market Insights and Forecast With Impact of COVID-19 (2021-2026)Azoth AnalyticsNo ratings yet

- Materi Sesi 2Document44 pagesMateri Sesi 2vincent jawaNo ratings yet

- Use of Medication Global ReportDocument51 pagesUse of Medication Global Reporthassan shahidNo ratings yet

- Pharma Industry Demand and Supply AnalysisDocument19 pagesPharma Industry Demand and Supply AnalysisYatendra VarmaNo ratings yet

- CBDX Han Medical Cannabis Wellness UCITS ETF USDDocument3 pagesCBDX Han Medical Cannabis Wellness UCITS ETF USDpee-jayNo ratings yet

- 744Document16 pages744Ruxandra DanuletNo ratings yet

- Consumer Sector - Best in ClassDocument30 pagesConsumer Sector - Best in ClassEry IrmansyahNo ratings yet

- Galenica Annual Report 2020Document160 pagesGalenica Annual Report 2020giyevec213No ratings yet

- NS Kebijakan POR Jaktim 2019Document42 pagesNS Kebijakan POR Jaktim 2019yesiNo ratings yet

- Analgesics in IndiaDocument10 pagesAnalgesics in IndiaLionel MessiNo ratings yet

- HowHealthtechisshapingtheindustry May2021Document6 pagesHowHealthtechisshapingtheindustry May2021Vansh AggarwalNo ratings yet

- Not Rated: Itama RanorayaDocument18 pagesNot Rated: Itama RanorayaMuhammad Usamah ArifiantoNo ratings yet

- Solving Pharmas Quality Unit Identity CrisisDocument3 pagesSolving Pharmas Quality Unit Identity CrisisAYMEN GOODKidNo ratings yet

- Dead Recovered Confirmed Tested Isolated: Situation Report NoDocument10 pagesDead Recovered Confirmed Tested Isolated: Situation Report NoAbu UsamaNo ratings yet

- Photocure ASA Results For 2nd Quarter 2021: August 11, 2021Document25 pagesPhotocure ASA Results For 2nd Quarter 2021: August 11, 2021TorfinnKDKNo ratings yet

- ArcView Group Executive Summary: The State of Legal Marijuana Markets 5th EditionDocument24 pagesArcView Group Executive Summary: The State of Legal Marijuana Markets 5th EditionMonterey Bud100% (1)

- Beginning SAP R - 3 Implementation at Geneva PharmaceuticalsDocument40 pagesBeginning SAP R - 3 Implementation at Geneva PharmaceuticalsVivekNo ratings yet

- J.P. Morgan 2022 Conference ReviewDocument204 pagesJ.P. Morgan 2022 Conference ReviewAndres Quintero Gomez100% (2)

- The Race to Manufacture COVID-19 Vaccines: Emerging Vaccine TechnologiesFrom EverandThe Race to Manufacture COVID-19 Vaccines: Emerging Vaccine TechnologiesNo ratings yet

- Tratuzumab Patent US20060275305A1Document61 pagesTratuzumab Patent US20060275305A1SHINDY ARIESTA DEWIADJIENo ratings yet

- Tratuzumab Patent US20060275305A1Document61 pagesTratuzumab Patent US20060275305A1SHINDY ARIESTA DEWIADJIENo ratings yet

- Pipeline Biologics2020 s41587-021-00814-wDocument9 pagesPipeline Biologics2020 s41587-021-00814-wSHINDY ARIESTA DEWIADJIENo ratings yet

- Biosimilar Bioterapetik Kmab-12-01-1743517Document15 pagesBiosimilar Bioterapetik Kmab-12-01-1743517SHINDY ARIESTA DEWIADJIENo ratings yet

- Antibiotics - Small Molecule - Not - B - Developed d41586-020-02884-3Document3 pagesAntibiotics - Small Molecule - Not - B - Developed d41586-020-02884-3SHINDY ARIESTA DEWIADJIENo ratings yet

- NTP MOP 6th Ed Module 7 Treatment of TB in Special Situations 10.20.20Document56 pagesNTP MOP 6th Ed Module 7 Treatment of TB in Special Situations 10.20.20gbNo ratings yet

- 01 Intro To TCCC For All Combatants 140602Document53 pages01 Intro To TCCC For All Combatants 140602Bruno100% (1)

- CFCSDocument77 pagesCFCSNurul NadiahNo ratings yet

- Ebola Virus: Sorveto, Dayle Daniel GDocument10 pagesEbola Virus: Sorveto, Dayle Daniel GDayledaniel SorvetoNo ratings yet

- Presentation - Uric AcidDocument31 pagesPresentation - Uric AcidTc Khoon100% (1)

- PG Addmision 2021Document3 pagesPG Addmision 2021Harpreet KaurNo ratings yet

- Adrenocorticosteroids & Adrenocortical AntagonistsDocument20 pagesAdrenocorticosteroids & Adrenocortical Antagonistsapi-3859918No ratings yet

- Long-Term Surgery Graves Disease 20 YearsDocument3 pagesLong-Term Surgery Graves Disease 20 YearsTambunta TariganNo ratings yet

- Dr. Ali Khamis - CVDocument2 pagesDr. Ali Khamis - CVAli KhamisNo ratings yet

- RCT - Masters - 2022Document24 pagesRCT - Masters - 2022Kanwal KhanNo ratings yet

- Nhis 2Document36 pagesNhis 2Saravanakumar RajaramNo ratings yet

- Color Atlas of Small Animal Necropsy 1Document81 pagesColor Atlas of Small Animal Necropsy 1Sai KrupaNo ratings yet

- Goto 2019Document6 pagesGoto 2019Marmox Lab.No ratings yet

- Beneficios de La Relacion y Embarazo Revision 2012Document11 pagesBeneficios de La Relacion y Embarazo Revision 2012ogarcía_pattoNo ratings yet

- CS HTNDocument16 pagesCS HTNAngela Carrillo Triano67% (3)

- MARIE CRISELLE CASIMJuly 26 2023-Letter of AuthorizationDocument1 pageMARIE CRISELLE CASIMJuly 26 2023-Letter of Authorizationjqm printingNo ratings yet

- ESA2013 Abstract BookDocument300 pagesESA2013 Abstract BookAyyaz HussainNo ratings yet

- Q3 Health 8 Module 6 PDFDocument13 pagesQ3 Health 8 Module 6 PDFkateNo ratings yet

- Pearson - Vue - 200 QUESTIONS PDFDocument40 pagesPearson - Vue - 200 QUESTIONS PDFDr-Jahanzaib Gondal100% (2)

- Nursing Care Plan GastroenteritisDocument3 pagesNursing Care Plan GastroenteritisChryst Louise SaavedraNo ratings yet

- Pricelist SKINTIFIC Jakarta X Beauty II 14 - 17 Dec 2023Document1 pagePricelist SKINTIFIC Jakarta X Beauty II 14 - 17 Dec 2023ZakiyahNo ratings yet

- Association Between Polymorphisms in CXCR2 Gene and PreeclampsiaDocument8 pagesAssociation Between Polymorphisms in CXCR2 Gene and PreeclampsiaalyneNo ratings yet

- Ashhad's Step 2 CK UW Notes PDFDocument166 pagesAshhad's Step 2 CK UW Notes PDFabNo ratings yet

- DD by Laboratory MedicineDocument1,122 pagesDD by Laboratory MedicineBiancaPancu100% (1)

- Juvenile Idiopathic Arthritis TypesDocument1 pageJuvenile Idiopathic Arthritis TypesDinesh ReddyNo ratings yet

- Defic I Enc I A MultipleDocument16 pagesDefic I Enc I A MultipleEnrique GonzalvusNo ratings yet

- W2-11 Neurological Issues in Women - LectureDocument47 pagesW2-11 Neurological Issues in Women - LectureNanjit SharmaNo ratings yet

- Acute Chest Syndrome (ACS) CCGDocument11 pagesAcute Chest Syndrome (ACS) CCGJessa MaeNo ratings yet

- Hybrid Hyrax Distalizer JO PDFDocument7 pagesHybrid Hyrax Distalizer JO PDFCaTy ZamNo ratings yet

- Abbrivation of Medical TrminologyDocument1,215 pagesAbbrivation of Medical Trminologyapi-271694220No ratings yet