You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chapter 11 - She Part 2Document4 pagesChapter 11 - She Part 2XienaNo ratings yet

- REAPHISDocument1 pageREAPHISnmdl123No ratings yet

- Student Success Department Meeting Faculty Room: Hermione WeaslyDocument23 pagesStudent Success Department Meeting Faculty Room: Hermione Weaslynmdl123No ratings yet

- Comrehensive Exam I.: Kabata Doesn't Own by Jose Rizal. Numerous Researchers Questioned The Credibility ofDocument2 pagesComrehensive Exam I.: Kabata Doesn't Own by Jose Rizal. Numerous Researchers Questioned The Credibility ofnmdl123No ratings yet

- INTACCTDocument6 pagesINTACCTnmdl123No ratings yet

- Reaphis Discussion Board Unit 1Document1 pageReaphis Discussion Board Unit 1nmdl123No ratings yet

- Output No. 2 - PAS 1 Instruction: Write Your Answers On Long Bond PapersDocument2 pagesOutput No. 2 - PAS 1 Instruction: Write Your Answers On Long Bond Papersnmdl123No ratings yet

- 2.1. The Corporate Form of OrganizationDocument2 pages2.1. The Corporate Form of Organizationnmdl123No ratings yet

- Shareholder's Equity Shareholder's Equity: Accounting (Far Eastern University) Accounting (Far Eastern University)Document18 pagesShareholder's Equity Shareholder's Equity: Accounting (Far Eastern University) Accounting (Far Eastern University)nmdl123No ratings yet

- QuestionDocument12 pagesQuestionnmdl123No ratings yet

- Activity No. 1 - Partnership FormationDocument1 pageActivity No. 1 - Partnership Formationnmdl123No ratings yet

- 2.4. Issuance of Share CapitalDocument6 pages2.4. Issuance of Share Capitalnmdl123No ratings yet

- Discussion Board Unit 1Document1 pageDiscussion Board Unit 1nmdl123No ratings yet

- ForgivenessDocument2 pagesForgivenessnmdl123No ratings yet

- Environment and Community Awareness EducationDocument7 pagesEnvironment and Community Awareness Educationnmdl123No ratings yet

- Petstress: Reevenne Heart Ferrera, Zharena Tessa Tenefrancia, Ghysam Dave Dadulla, Adrian Leal, Mark Angelo DominiceDocument15 pagesPetstress: Reevenne Heart Ferrera, Zharena Tessa Tenefrancia, Ghysam Dave Dadulla, Adrian Leal, Mark Angelo Dominicenmdl123No ratings yet

- A Fleeting Time: Marife Bacaltos-Tarrayo (An Article Published in The Paulinian Scribe)Document2 pagesA Fleeting Time: Marife Bacaltos-Tarrayo (An Article Published in The Paulinian Scribe)nmdl123No ratings yet

- 402a - Corporate Accounting - I PDFDocument21 pages402a - Corporate Accounting - I PDFAnuranjani DhivyaNo ratings yet

- Practice For Midterm 1Document136 pagesPractice For Midterm 1ennaira 06No ratings yet

- Auditing Problems Problem 1Document8 pagesAuditing Problems Problem 1Gherome AlejoNo ratings yet

- Audit of Investments - Equity Securities Supplementary ProblemsDocument2 pagesAudit of Investments - Equity Securities Supplementary ProblemsNIMOTHI LASE0% (1)

- Cir Vs ManningDocument3 pagesCir Vs ManningEKANG100% (1)

- Analysis of Profitability:: Short Term Financial Position or Test of SolvencyDocument2 pagesAnalysis of Profitability:: Short Term Financial Position or Test of Solvencygauravbhardwaj900No ratings yet

- Trigonometry (From: Applications of Trigonometry in Real LifeDocument6 pagesTrigonometry (From: Applications of Trigonometry in Real LifeLavishGulatiNo ratings yet

- Annual Report 2014 PDFDocument94 pagesAnnual Report 2014 PDFCharles NdyabaweNo ratings yet

- Securities Listing by Laws 2053Document14 pagesSecurities Listing by Laws 2053Krishna GiriNo ratings yet

- Accounting For Corporations Chapter 13Document21 pagesAccounting For Corporations Chapter 13Rabie HarounNo ratings yet

- Ia3 M QuizzesDocument25 pagesIa3 M Quizzesbarron avenidaNo ratings yet

- Midterm Exam ADM3350 Summer 2022 PDFDocument7 pagesMidterm Exam ADM3350 Summer 2022 PDFHan ZhongNo ratings yet

- Omtex Classes: "Achieve Success Through" ONE "THE Home of Text" TIME: - 3 HoursDocument11 pagesOmtex Classes: "Achieve Success Through" ONE "THE Home of Text" TIME: - 3 HoursAMIN BUHARI ABDUL KHADERNo ratings yet

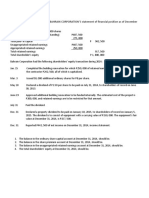

- The Shareholder's Equity Section BAHRAIN CORPORATION'S Statement of Financial Position As of December 31, 2013, Is As FollowsDocument4 pagesThe Shareholder's Equity Section BAHRAIN CORPORATION'S Statement of Financial Position As of December 31, 2013, Is As FollowsCyril John ReyesNo ratings yet

- Dividend Policy and Firm Value Assignment 2Document2 pagesDividend Policy and Firm Value Assignment 2riddhisanghviNo ratings yet

- Audit of Investments 2Document2 pagesAudit of Investments 2ShelleyNo ratings yet

- SMC Series 2LNO Preliminary Offer Terms Sheet PSE Comments - SignedDocument18 pagesSMC Series 2LNO Preliminary Offer Terms Sheet PSE Comments - SignedChristian Joseph MontellanoNo ratings yet

- 100 Qa CorpoDocument23 pages100 Qa CorpoailynvdsNo ratings yet

- 4th Assessment STUDENTDocument5 pages4th Assessment STUDENTJOHANNA TORRESNo ratings yet

- MaricoDocument13 pagesMaricoRitesh KhobragadeNo ratings yet

- Financial ManagementDocument12 pagesFinancial ManagementLevina DiazNo ratings yet

- StockDocument60 pagesStockPhan Tú AnhNo ratings yet

- Chapter 8 - QuizzDocument5 pagesChapter 8 - QuizzChloe JtrNo ratings yet

- Basics of Share Market OperationsDocument8 pagesBasics of Share Market Operationslelesachin100% (2)

- Corpo Law Dlsu..Document40 pagesCorpo Law Dlsu..Erika DiloyNo ratings yet

- Cosmo Bio Solutions PVT LTD Prime DocsDocument17 pagesCosmo Bio Solutions PVT LTD Prime DocsChandra SekaranNo ratings yet

- MATERIALDocument8 pagesMATERIALVatsal ParmarNo ratings yet

- C 7 - S - C V: Hapter Tocks Haracteristics AND AluationDocument30 pagesC 7 - S - C V: Hapter Tocks Haracteristics AND AluationMd. Shahajada Masud Anowarul HaqueNo ratings yet

- MTDrill 2Document17 pagesMTDrill 2Cedric Legaspi TagalaNo ratings yet