You might also like

- Rice Retailer Company Final PaperDocument81 pagesRice Retailer Company Final PaperJoemar Furigay86% (110)

- Essay On MortgagesDocument2 pagesEssay On MortgagesViorel Mihai Mitrana100% (1)

- Contracts: Appropriation of Payments.Document8 pagesContracts: Appropriation of Payments.DigvijayNo ratings yet

- Bankruptcy Act BangladeshDocument16 pagesBankruptcy Act BangladeshMarjia Heemi57% (7)

- Secured Borrowing and A Sale of ReceivablesDocument1 pageSecured Borrowing and A Sale of Receivableswarsidi100% (1)

- Effects of Changes in ForEx RatesDocument40 pagesEffects of Changes in ForEx RatesEnrique Paolo Mendoza80% (5)

- Enforcement of JudgmentDocument3 pagesEnforcement of Judgmental moore100% (1)

- Ethics Box Any Ethical Obligation After DischargeDocument7 pagesEthics Box Any Ethical Obligation After DischargeHijratul SevenNo ratings yet

- Group6 - Islamic Law - If20 - ZulfadhliDocument25 pagesGroup6 - Islamic Law - If20 - ZulfadhliKepala AcikNo ratings yet

- Clog On Redemption by IpleaderDocument4 pagesClog On Redemption by IpleadersaurabhNo ratings yet

- Application of PaymentDocument13 pagesApplication of Paymentulticon0% (2)

- Cancellation of 4ward ContractDocument8 pagesCancellation of 4ward ContractManu K AnujanNo ratings yet

- Extinguishment of ObligationsDocument24 pagesExtinguishment of ObligationsChristine RenolaNo ratings yet

- Banking Module 2Document8 pagesBanking Module 2edhaNo ratings yet

- Objectives of Insolvency LawDocument13 pagesObjectives of Insolvency LawKaran VermaNo ratings yet

- Once A Mortgage Always A MortgageDocument6 pagesOnce A Mortgage Always A MortgageSudarshani SumanasenaNo ratings yet

- Limitation Bars The Remedy, It Does Not Extinguish The RightDocument11 pagesLimitation Bars The Remedy, It Does Not Extinguish The RightPankhuri AroraNo ratings yet

- Oblicon PDFDocument61 pagesOblicon PDFKatherine Heigl MadrigalNo ratings yet

- Jai (A) Explain THREE Remedies Available To A Mortgage To Enforce His SecurityDocument6 pagesJai (A) Explain THREE Remedies Available To A Mortgage To Enforce His SecurityRyan RamkirathNo ratings yet

- Oblicon Articles 1252-1261Document5 pagesOblicon Articles 1252-1261kumiko sakamoto100% (1)

- Group 3 Banker's Rights, Lien, Appropriation, Combination and Set-OffDocument12 pagesGroup 3 Banker's Rights, Lien, Appropriation, Combination and Set-OffthhiongomungaiNo ratings yet

- Execution of Forward Contracts in Foreign Exchange MarketsDocument7 pagesExecution of Forward Contracts in Foreign Exchange Marketsmohanbaskar87No ratings yet

- Acceleration Clauses in Foreclosure Actions: New RulesDocument6 pagesAcceleration Clauses in Foreclosure Actions: New Rulesbob doleNo ratings yet

- Foreclosure in Housing Finance and Legal DocumentationDocument35 pagesForeclosure in Housing Finance and Legal DocumentationUsman AkramNo ratings yet

- Vii. Who Pays For Expenses For Making Payment ART. 1247 Debtor Pays For Extrajudicial ExpensesDocument19 pagesVii. Who Pays For Expenses For Making Payment ART. 1247 Debtor Pays For Extrajudicial ExpensesDianne RosalesNo ratings yet

- Q - Commercial Law Exam Last Minute TipsDocument10 pagesQ - Commercial Law Exam Last Minute TipsChare MarcialNo ratings yet

- Pledge of SharesDocument8 pagesPledge of Sharesshubhamgupta04101994No ratings yet

- Chapter 2 Notes and MortgagesDocument24 pagesChapter 2 Notes and Mortgagesnazmul islamNo ratings yet

- 11 - Chapter 3 PDFDocument38 pages11 - Chapter 3 PDFAbhishek Kumar100% (1)

- Contracts AssignmentDocument21 pagesContracts AssignmentNAVEENNo ratings yet

- Defaults & Foreclosures QUESTIONSDocument11 pagesDefaults & Foreclosures QUESTIONSPrince EG DltgNo ratings yet

- Arts 1252-1261 PAYMENT 4 Special FormsDocument5 pagesArts 1252-1261 PAYMENT 4 Special FormsKareen BaucanNo ratings yet

- BAM 026 Group 2 Comprehensive PaperDocument8 pagesBAM 026 Group 2 Comprehensive PaperMary Lyn DatuinNo ratings yet

- TOPADocument15 pagesTOPAAiyushiNo ratings yet

- Once A Mortgage, Always A MortgageDocument2 pagesOnce A Mortgage, Always A MortgageAtishay JainNo ratings yet

- E Zobel Inc VS CADocument6 pagesE Zobel Inc VS CAAerwin AbesamisNo ratings yet

- Credit Transaction QuizDocument5 pagesCredit Transaction QuizMelrick LuceroNo ratings yet

- Business Law Module MidtermDocument8 pagesBusiness Law Module MidtermZero OneNo ratings yet

- Tpa IntroductionDocument12 pagesTpa Introductionbrijen singh thakurNo ratings yet

- Application of Payments, Consignation, Cession, Tender of PaymentDocument10 pagesApplication of Payments, Consignation, Cession, Tender of PaymentJulius MilaNo ratings yet

- Various Types of Charges: What Is A Charge & What Is Its PurposeDocument12 pagesVarious Types of Charges: What Is A Charge & What Is Its PurposevinodkulkarniNo ratings yet

- 2012 - Tpa ProjectDocument14 pages2012 - Tpa ProjectIshika kanyalNo ratings yet

- UntitledDocument5 pagesUntitledRj NelsonNo ratings yet

- Assignment TopicDocument8 pagesAssignment Topicumaima aliNo ratings yet

- Continuing Guarantee AnsDocument5 pagesContinuing Guarantee AnsSwarna LathaNo ratings yet

- Oblicon Articles 1249 - 1258Document29 pagesOblicon Articles 1249 - 1258vicmanlawrenzeNo ratings yet

- COMPENSATION - SalubreDocument23 pagesCOMPENSATION - SalubreRichie SalubreNo ratings yet

- Law On Obligations and ContractsDocument19 pagesLaw On Obligations and ContractsAlex JudillaNo ratings yet

- DEPOSIT V MutuumDocument3 pagesDEPOSIT V MutuumNichole LanuzaNo ratings yet

- Mortgage Redemption StatementsDocument4 pagesMortgage Redemption StatementsThe Lone GunmanNo ratings yet

- Civil Law Review Ii MidtermsDocument8 pagesCivil Law Review Ii MidtermsKatherine Jane UnayNo ratings yet

- Common Latin Legal Terms in Loan Agreements and SuretiesDocument3 pagesCommon Latin Legal Terms in Loan Agreements and Suretieshislordship100% (4)

- ObliconDocument2 pagesObliconAngela SerranoNo ratings yet

- Agbayani: There Are Certain Notes Containing Acceleration Provisions. These Provisions (1) Make ItDocument2 pagesAgbayani: There Are Certain Notes Containing Acceleration Provisions. These Provisions (1) Make ItShazna SendicoNo ratings yet

- Cred Trans DoctrinesDocument6 pagesCred Trans DoctrinesAshaselenaNo ratings yet

- Assignment #6Document3 pagesAssignment #6Lenmariel GallegoNo ratings yet

- Extinguishment of ObligationsDocument6 pagesExtinguishment of ObligationsRic Bienne Marc AndresNo ratings yet

- Al HawalahDocument3 pagesAl HawalahZulaikha Meseri100% (1)

- B Lien Banking LawDocument9 pagesB Lien Banking LawxyzNo ratings yet

- Once A Mortgage Always A MortgagesDocument6 pagesOnce A Mortgage Always A MortgagesAnonymous 2Q60K5kNo ratings yet

- Author: Mushtak Parker - Arab News Publication Date: Mon, 2010-07-05 01:54Document4 pagesAuthor: Mushtak Parker - Arab News Publication Date: Mon, 2010-07-05 01:54Putri PurwandariNo ratings yet

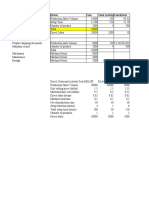

- Indirect Labor Cost Driver Cost Total Activitycost/DriverDocument3 pagesIndirect Labor Cost Driver Cost Total Activitycost/DriverPutri PurwandariNo ratings yet

- Study Case SolutionDocument3 pagesStudy Case SolutionPutri PurwandariNo ratings yet

- Lembar Jawaban Elimination Stage 2017Document5 pagesLembar Jawaban Elimination Stage 2017Putri PurwandariNo ratings yet

- Assessment Report On Asset ManagementDocument29 pagesAssessment Report On Asset ManagementMuhammad ArifNo ratings yet

- 2 Introduction To Sales Management PDFDocument34 pages2 Introduction To Sales Management PDFParul Agarwal100% (1)

- Armin Ravoof (TVS Motors)Document18 pagesArmin Ravoof (TVS Motors)armeena falakNo ratings yet

- Sabina Nepal CVDocument5 pagesSabina Nepal CVRakesh PradhanNo ratings yet

- Comprehensive Accounting Cycle Problem PDFDocument11 pagesComprehensive Accounting Cycle Problem PDFDin Rose Gonzales100% (1)

- HREDRD ANNUAL WORK AND FINANCIAL PLAN - Updated 2023Document8 pagesHREDRD ANNUAL WORK AND FINANCIAL PLAN - Updated 2023Martin Lenin SantosNo ratings yet

- General Electric Executive Summary: By: William Quinn MBA 510 - Financial Accounting August 10, 2009Document5 pagesGeneral Electric Executive Summary: By: William Quinn MBA 510 - Financial Accounting August 10, 2009bquinn08No ratings yet

- EduMple Learning Slide DeckDocument14 pagesEduMple Learning Slide Deckarun kumarNo ratings yet

- Industrial Relation Chapter 2Document14 pagesIndustrial Relation Chapter 2Ahmad Izzat Hamzah100% (1)

- Entrepreneurship: Managing Your Personal FinancesDocument38 pagesEntrepreneurship: Managing Your Personal FinancesRamon BrionesNo ratings yet

- NPNPNPDocument13 pagesNPNPNPTeuku M. Zachari AlamsyahNo ratings yet

- Mod 02Document19 pagesMod 02gingeNo ratings yet

- SalamDocument12 pagesSalamqurathNo ratings yet

- 56464bos45796cp4u1 PDFDocument119 pages56464bos45796cp4u1 PDFVinay kumarNo ratings yet

- Purchase Order: (PR No. 1000001452)Document4 pagesPurchase Order: (PR No. 1000001452)Prudence dela CruzNo ratings yet

- Investor Protection Guidelines by Sebi NewDocument17 pagesInvestor Protection Guidelines by Sebi Newnikudi92No ratings yet

- Mahdi Kafi CVDocument2 pagesMahdi Kafi CVSubhanjanDasNo ratings yet

- Small Business: Distribution and LocationDocument40 pagesSmall Business: Distribution and LocationMahmoud AbdullahNo ratings yet

- 4 Pillars of Corporate Gov.Document3 pages4 Pillars of Corporate Gov.Anita Khan76% (17)

- Kusina Ni NanayDocument16 pagesKusina Ni NanayGlades Cacho100% (1)

- CH 08Document20 pagesCH 08Amaurrie ArpilledaNo ratings yet

- NovartisDocument14 pagesNovartisRahul KumarNo ratings yet

- Business Mumbai Mba Pharma Curriculum PDFDocument4 pagesBusiness Mumbai Mba Pharma Curriculum PDFTech WizardNo ratings yet

- Quiz-Ch1-Introduction Retailing CompletedDocument3 pagesQuiz-Ch1-Introduction Retailing CompletedR.A.A.V M.DNo ratings yet

- Case IbmDocument3 pagesCase IbmEVA SALVATIERRA LOPEZNo ratings yet

- Quality Engineer Skills Competencies 1671770511Document8 pagesQuality Engineer Skills Competencies 1671770511AlfiNo ratings yet

- Entrepreneurship - 2015-2021 SolutionsDocument66 pagesEntrepreneurship - 2015-2021 SolutionsJay MaximumNo ratings yet

- Wcms 864222Document176 pagesWcms 864222Scooby DoNo ratings yet