You might also like

- Effect of Economic Growth and Foreign Direct Investment On Asian CountriesDocument7 pagesEffect of Economic Growth and Foreign Direct Investment On Asian Countriestran phankNo ratings yet

- Environmental Performance Versus Economic-Financial Performance: Evidence From Italian FirmsDocument11 pagesEnvironmental Performance Versus Economic-Financial Performance: Evidence From Italian FirmsCaroline HadiNo ratings yet

- Jurnal Esdal 2Document9 pagesJurnal Esdal 2Dodi SwyonoNo ratings yet

- Sustainability 12 08680Document16 pagesSustainability 12 08680abdulNo ratings yet

- The Environmental Policy Stringency in Taiwan and Its Challenges On Green Economy TransitionDocument27 pagesThe Environmental Policy Stringency in Taiwan and Its Challenges On Green Economy TransitionMuhammad Al GhifaryNo ratings yet

- Testingthe EKCHypothesisin IndonesiaDocument24 pagesTestingthe EKCHypothesisin IndonesiaAlma Aurellia AmandaNo ratings yet

- 6 9 3 PBDocument12 pages6 9 3 PBCitra DewiNo ratings yet

- Integrating Information About The Cost of Carbon Through Activity Based Costing 2012 Journal of Cleaner ProductionDocument10 pagesIntegrating Information About The Cost of Carbon Through Activity Based Costing 2012 Journal of Cleaner ProductionLilian BrodescoNo ratings yet

- Adebayo2021 Article DoCO2EmissionsEnergyConsumptioDocument17 pagesAdebayo2021 Article DoCO2EmissionsEnergyConsumptioMuhammad Syaifuddin FuadNo ratings yet

- Penelitian Carbon - LingkunganDocument27 pagesPenelitian Carbon - LingkunganNadya YuliastikaNo ratings yet

- Predominant Factors for Firms to Reduce Carbon EmissionsFrom EverandPredominant Factors for Firms to Reduce Carbon EmissionsNo ratings yet

- Sciencedomain, Saraswati2132021AJEBA65666Document9 pagesSciencedomain, Saraswati2132021AJEBA65666Senabella AristianiNo ratings yet

- The Ambivalent Role of Institutions in The CO2Document11 pagesThe Ambivalent Role of Institutions in The CO2tran phankNo ratings yet

- 1 s2.0 S0301421514003772 MainDocument9 pages1 s2.0 S0301421514003772 MainLORENZO RAFFAELE CIPRIANINo ratings yet

- Effect of Profitability On Carbon Emission Disclosure: The International Journal of Social Sciences WorldDocument14 pagesEffect of Profitability On Carbon Emission Disclosure: The International Journal of Social Sciences WorldLuthfi'ahNo ratings yet

- Carbon Emission Disclosure: Testing The Influencing FactorsDocument8 pagesCarbon Emission Disclosure: Testing The Influencing FactorsAkhmad Badrus Sholikhul MakhfudhNo ratings yet

- 49 IJEEP 12954 Rianto OkeyDocument9 pages49 IJEEP 12954 Rianto Okeyrstxm5wjfrNo ratings yet

- 1 PBDocument14 pages1 PBJosua Desmonda SimanjuntakNo ratings yet

- 1 Publication2016Document13 pages1 Publication2016Irina AlexandraNo ratings yet

- Fiscal Policy and Ecological Sustainability: A Post-Keynesian Perspective Yannis Dafermos and Maria NikolaidiDocument45 pagesFiscal Policy and Ecological Sustainability: A Post-Keynesian Perspective Yannis Dafermos and Maria NikolaidiTimni VieiraNo ratings yet

- Ekins, 1999 P. Ekins, European Environmental Taxes and Charges - Recent Experience, Issues and Trends, Ecological Economics 31 (1999), Pp. 39-62. ArticleDocument24 pagesEkins, 1999 P. Ekins, European Environmental Taxes and Charges - Recent Experience, Issues and Trends, Ecological Economics 31 (1999), Pp. 39-62. Articlew0091100No ratings yet

- The Global Green Economy A Review of Concepts Definitions MeasurementDocument23 pagesThe Global Green Economy A Review of Concepts Definitions MeasurementAdel BenatekNo ratings yet

- UK Carbon TaxDocument14 pagesUK Carbon TaxJosua Desmonda SimanjuntakNo ratings yet

- Environmental Taxation Based Integrated Modeling TDocument11 pagesEnvironmental Taxation Based Integrated Modeling TVyas NikhilNo ratings yet

- Mensah 2019Document10 pagesMensah 2019yosraNo ratings yet

- The Role of Financial Deepening and Green Technology On Carbon - ADocument6 pagesThe Role of Financial Deepening and Green Technology On Carbon - Atran phankNo ratings yet

- AJES Article 1 225Document7 pagesAJES Article 1 225Mihaela SburleaNo ratings yet

- 1 s2.0 S0301420722002495 MainDocument10 pages1 s2.0 S0301420722002495 MainLana AzimNo ratings yet

- SSRN Id2199374Document12 pagesSSRN Id2199374Ngọc Linh BùiNo ratings yet

- The Economic Costs of Indoor Air Pollution: New Results For Indonesia, The Philippines, and Timor-LesteDocument21 pagesThe Economic Costs of Indoor Air Pollution: New Results For Indonesia, The Philippines, and Timor-LesteSATRIONo ratings yet

- Literature Review of Renewable Energy Policies and Impacts: Tarek Safwat KabelDocument14 pagesLiterature Review of Renewable Energy Policies and Impacts: Tarek Safwat KabelAshokNo ratings yet

- Vivid A. Khusna, Deni Kusumawardani, 2021 - Decomposition of Carbon Dioxide (CO2) Emissions inDocument14 pagesVivid A. Khusna, Deni Kusumawardani, 2021 - Decomposition of Carbon Dioxide (CO2) Emissions intuananh9a7lhpqnNo ratings yet

- Effet Taxe Carbone EnvironnementDocument5 pagesEffet Taxe Carbone Environnementeforgues564No ratings yet

- Aydin 2023Document9 pagesAydin 2023NOUFELIE ROMUSNo ratings yet

- Alasan Pemerintah Indonesia MeratifikasiDocument23 pagesAlasan Pemerintah Indonesia MeratifikasiHamied EndriantoNo ratings yet

- Journal Pre-Proof: Energy EconomicsDocument51 pagesJournal Pre-Proof: Energy EconomicsAbdul MajeedNo ratings yet

- Assessment of Copenhagen PledgesDocument6 pagesAssessment of Copenhagen PledgesChevi RahayuNo ratings yet

- Fenvs 10 934885Document11 pagesFenvs 10 934885Iyad GuiaNo ratings yet

- 1 s2.0 S0921800922000891 MainDocument12 pages1 s2.0 S0921800922000891 MainFandy YusrilNo ratings yet

- The Impact of Renewable Energy Trade Economic Growth On CO2 Emissions in ChinaDocument21 pagesThe Impact of Renewable Energy Trade Economic Growth On CO2 Emissions in ChinaAbdur RehmanNo ratings yet

- Irfan y 2017Document25 pagesIrfan y 2017Judith Abisinia MaldonadoNo ratings yet

- Carbon FootprintDocument11 pagesCarbon FootprintAbdul HarisNo ratings yet

- Liu 2017Document26 pagesLiu 2017Alma Aurellia AmandaNo ratings yet

- Exploring The Effects of Climate-Related Financial Policies On Carbon Emissions in G20 Countries: A Panel Quantile Regression ApproachDocument25 pagesExploring The Effects of Climate-Related Financial Policies On Carbon Emissions in G20 Countries: A Panel Quantile Regression Approacharman jamshidiNo ratings yet

- How To Overcome Climate Policy ShortagesDocument8 pagesHow To Overcome Climate Policy ShortagesNemanjaNo ratings yet

- Development of Natural Gas Vehicles in ChinaDocument14 pagesDevelopment of Natural Gas Vehicles in ChinaMuhammad Imran KhanNo ratings yet

- The Relationship Between Foreign Direct Investment, Economic GrowthDocument8 pagesThe Relationship Between Foreign Direct Investment, Economic Growthtran phankNo ratings yet

- Paper 2 PDFDocument11 pagesPaper 2 PDFNancy MaribelNo ratings yet

- Journal Pre-Proof: Science of The Total EnvironmentDocument57 pagesJournal Pre-Proof: Science of The Total EnvironmentAfef HasnaouiNo ratings yet

- Are Urbanization, Industrialization and CO2 Emissions Cointegrated?Document30 pagesAre Urbanization, Industrialization and CO2 Emissions Cointegrated?doctshNo ratings yet

- The Content and Determinants of Greenhouse Gas Emissiondisclosure Evidence From Indonesian CompaniesDocument10 pagesThe Content and Determinants of Greenhouse Gas Emissiondisclosure Evidence From Indonesian CompaniesDessy Noor FaridaNo ratings yet

- Xiong 2021Document8 pagesXiong 2021NitishNo ratings yet

- 32158-Article Text-119092-1-10-20230228Document13 pages32158-Article Text-119092-1-10-20230228Caren ReasNo ratings yet

- CO2 InnoDocument11 pagesCO2 InnoAhmad BashirNo ratings yet

- Climate Change GlobalDocument20 pagesClimate Change GlobalKabir AgarwalNo ratings yet

- Public Preferences For Carbon Tax AttributesDocument12 pagesPublic Preferences For Carbon Tax AttributeslucrativenataNo ratings yet

- 10 1016@j Enpol 2019 03 007Document9 pages10 1016@j Enpol 2019 03 007rizal rachmadNo ratings yet

- The Role of Institution On FDI and Environmental Pollution Nexus - Evidence From Developing CountriesDocument12 pagesThe Role of Institution On FDI and Environmental Pollution Nexus - Evidence From Developing Countriestran phankNo ratings yet

- 10 1016@j Jclepro 2019 06 218Document13 pages10 1016@j Jclepro 2019 06 218Dr. Maryam IshaqNo ratings yet

- Main Briefing 2012Document24 pagesMain Briefing 2012Glaiza Veluz-SulitNo ratings yet

- SK Singh Lab Report 09042018Document8 pagesSK Singh Lab Report 09042018Iasam Groups'sNo ratings yet

- Grade 6 Te Pointer Term 2Document2 pagesGrade 6 Te Pointer Term 2Lucas QuiapoNo ratings yet

- APMG Agile Project Management Training Course in BangaloreDocument14 pagesAPMG Agile Project Management Training Course in BangaloreprojectingITNo ratings yet

- Tarjetas Electronicas ServoDocument2 pagesTarjetas Electronicas ServoChris HANo ratings yet

- Business Model Canvas - Editable TemplateDocument2 pagesBusiness Model Canvas - Editable TemplateVijayNo ratings yet

- The Titans and The Twelve OlympiansDocument35 pagesThe Titans and The Twelve OlympiansJariejoy Biore67% (3)

- Wireless Cellular and LTE 4G Broadband 1Document76 pagesWireless Cellular and LTE 4G Broadband 1PRANEETH DpvNo ratings yet

- Philosophy in LifeDocument1 pagePhilosophy in LifeOuelle EvansNo ratings yet

- TABLE OF SPECIFICATIONS - Grade-10 (4th Grading)Document4 pagesTABLE OF SPECIFICATIONS - Grade-10 (4th Grading)Aljon Jay Sulit SiadanNo ratings yet

- Chemistry Investigatory ProjectDocument14 pagesChemistry Investigatory ProjectKrunal VasavaNo ratings yet

- Data Collection and Rock Mass ClassificationDocument7 pagesData Collection and Rock Mass ClassificationScott FosterNo ratings yet

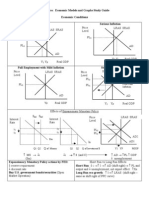

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideAznAlexT90% (21)

- KHKJHKDocument8 pagesKHKJHKMD. Naimul Isalm ShovonNo ratings yet

- Proview Datasheet - SM MDVR 401 4G - INDDocument2 pagesProview Datasheet - SM MDVR 401 4G - INDSlamat AgungNo ratings yet

- Bulletin For August 28-2010Document2 pagesBulletin For August 28-2010Twin Peaks SDA FellowshipNo ratings yet

- Applied Geography: Marco VizzariDocument11 pagesApplied Geography: Marco Vizzarialexandra mp100% (1)

- AirbusDocument176 pagesAirbusCristi VaiNo ratings yet

- Mini MBA 2020 12 Month ProgrammeDocument8 pagesMini MBA 2020 12 Month Programmelaice100% (1)

- Lesson Plan On Body Parts For EslDocument2 pagesLesson Plan On Body Parts For Eslapi-265046009No ratings yet

- 7 Problems - CompressorDocument2 pages7 Problems - CompressorBenedict TumlosNo ratings yet

- Previews IEEE 835-1994 PreDocument9 pagesPreviews IEEE 835-1994 PreKadirou BigstarNo ratings yet

- Prof Manzoor Iqbal Awan-S11-BU-BBA VII C-Comparative Management-Student Projects-23 May 11Document991 pagesProf Manzoor Iqbal Awan-S11-BU-BBA VII C-Comparative Management-Student Projects-23 May 11Manzoor Awan100% (1)

- Coordinate Geometry Class 9 Term 1Document7 pagesCoordinate Geometry Class 9 Term 1riya rajputNo ratings yet

- Noes Flex CubeDocument8 pagesNoes Flex CubeSeboeng MashilangoakoNo ratings yet

- IPC ProjectDocument15 pagesIPC ProjectAshish ChandaheNo ratings yet

- 2023 C Class Sedan AMG Order Guide en - UsDocument17 pages2023 C Class Sedan AMG Order Guide en - UsHiro Hieu NguyenNo ratings yet

- Telecommunications Regulation Handbook: InterconnectionDocument62 pagesTelecommunications Regulation Handbook: InterconnectionParam StudyNo ratings yet

- 2 Specialization in CEDocument24 pages2 Specialization in CEChrizter Jim LumaadNo ratings yet

- Nadi Astrology PDFDocument3 pagesNadi Astrology PDFabhi16No ratings yet

- Thorax Anatomy..Document21 pagesThorax Anatomy..Dungani AllanNo ratings yet