You might also like

- ENTR 20083 Pricing and CostingDocument66 pagesENTR 20083 Pricing and CostingTrecy Paccial100% (1)

- Final Obe-Syllabus Teaching Multigrade ClassesDocument7 pagesFinal Obe-Syllabus Teaching Multigrade ClassesVanessa L. Vinluan83% (6)

- Course Syllabus Business FinanceDocument11 pagesCourse Syllabus Business FinanceCharmaine Shanina100% (1)

- GUEVARRA Syllabus Arts Teaching Arts in The Elementary GradesDocument7 pagesGUEVARRA Syllabus Arts Teaching Arts in The Elementary GradesVanessa L. Vinluan100% (4)

- MKTG 101 DISTRIBUTION MANAGEMENT SyllabusDocument10 pagesMKTG 101 DISTRIBUTION MANAGEMENT SyllabusrubyNo ratings yet

- Ic 11 Top4sure 'Real Feel' Timed ExamDocument52 pagesIc 11 Top4sure 'Real Feel' Timed ExamKalyani JayakrishnanNo ratings yet

- Ethics Student Activity Sheets Day 2 (For Deductive Lesson) FinalDocument5 pagesEthics Student Activity Sheets Day 2 (For Deductive Lesson) FinalChulNo ratings yet

- Syllabus in Business FinancDocument8 pagesSyllabus in Business FinancRoNnie RonNieNo ratings yet

- Topic 9 A181 - Cost Volume Profit AnalysisDocument41 pagesTopic 9 A181 - Cost Volume Profit AnalysisEngku Farah100% (1)

- Actg 10 Accounting For Governmental, Not-for-Profit Entities and Specialized IndustriesDocument3 pagesActg 10 Accounting For Governmental, Not-for-Profit Entities and Specialized IndustriesVanessa L. VinluanNo ratings yet

- Supply Chain Management AssignmentDocument26 pagesSupply Chain Management Assignmentedo100% (1)

- BBA N 103: Principles of EconomicsDocument31 pagesBBA N 103: Principles of EconomicsPritee SinghNo ratings yet

- Training Plan: Qualification: BOOKKEEPING NC IIIDocument2 pagesTraining Plan: Qualification: BOOKKEEPING NC IIIarnold mamanoNo ratings yet

- Course Syllabus Managerial AccountingDocument10 pagesCourse Syllabus Managerial AccountingCharmaine Shanina100% (1)

- Types of Business According To Activities: (WEEK 5)Document12 pagesTypes of Business According To Activities: (WEEK 5)Mark Domingo MendozaNo ratings yet

- ACC111 Managerial AccountingDocument4 pagesACC111 Managerial AccountingAnnalyn ArnaldoNo ratings yet

- Program Outcomes: Course Title: Course CodeDocument6 pagesProgram Outcomes: Course Title: Course CodeLeonalyn SantosNo ratings yet

- Master in Business Administration Mba 308 - Financial ManagementDocument5 pagesMaster in Business Administration Mba 308 - Financial ManagementJhaydiel JacutanNo ratings yet

- Types of Business According To ActivitiesDocument23 pagesTypes of Business According To ActivitiesDn AngelNo ratings yet

- ECON13B Managerial EconomicsDocument3 pagesECON13B Managerial EconomicsTin Portuzuela100% (1)

- AC 4103 OBEdized SyllabusDocument21 pagesAC 4103 OBEdized SyllabusAyame KusuragiNo ratings yet

- TOTALQM Syllabus For Term 3 SY2016-2017Document8 pagesTOTALQM Syllabus For Term 3 SY2016-2017Holly AlexanderNo ratings yet

- SECTION - GROUP No. - BUSINESS NAME - Business Plan Presentation RubricDocument2 pagesSECTION - GROUP No. - BUSINESS NAME - Business Plan Presentation RubricAllen GonzagaNo ratings yet

- Final Exam in Fundamental of Accounting, Business and Management 2 Grade 12 Name: - Date: - Section: - ScoreDocument2 pagesFinal Exam in Fundamental of Accounting, Business and Management 2 Grade 12 Name: - Date: - Section: - ScoreLeylaNo ratings yet

- Applied Economics Syllabus DeclassifiedDocument4 pagesApplied Economics Syllabus DeclassifiedAl Jay MejosNo ratings yet

- Course Outline MicroeconomicsDocument6 pagesCourse Outline MicroeconomicsMubashir Ali KhanNo ratings yet

- Obe Syllabus - Managerial EconomicsDocument10 pagesObe Syllabus - Managerial EconomicsCristeta BaysaNo ratings yet

- Week 1 - Business MathDocument5 pagesWeek 1 - Business MathHerson MadrigalNo ratings yet

- Accounting Information System Course SyllabusDocument10 pagesAccounting Information System Course Syllabusali alhussainNo ratings yet

- Adjusting Entry ProblemsDocument5 pagesAdjusting Entry ProblemsRize Takatsuki100% (1)

- Lesson 1: Lesson 5:: Asian Institute of Computer StudiesDocument28 pagesLesson 1: Lesson 5:: Asian Institute of Computer StudiesCarmelo Justin Bagunu AllauiganNo ratings yet

- SyllabusDocument3 pagesSyllabusOffice AcadNo ratings yet

- FIN222 SyllabusDocument6 pagesFIN222 Syllabusbalondojeremy100% (2)

- Bookkeeping Lesson PlanDocument4 pagesBookkeeping Lesson PlanShanin Estavillo100% (1)

- Fabm 1 Lesson 4Document3 pagesFabm 1 Lesson 4Joey Agnas67% (3)

- RUBRIC FOR OJT Practicum Weekly ReportDocument1 pageRUBRIC FOR OJT Practicum Weekly ReportFranz CantaraNo ratings yet

- Financial Management Syllabus 2021-2022Document7 pagesFinancial Management Syllabus 2021-2022Marasherlyn VergaraNo ratings yet

- Fundamental of ABM1Document4 pagesFundamental of ABM1Raul Soriano Cabanting100% (1)

- Intel College: Course Name: Business Finance and EconomicsDocument2 pagesIntel College: Course Name: Business Finance and EconomicsRocky Kaur100% (1)

- Final Rubrics For Sales PresentationDocument3 pagesFinal Rubrics For Sales PresentationNekoh Dela CernaNo ratings yet

- BUSINESS-Plan2.docx FINALDocument48 pagesBUSINESS-Plan2.docx FINALAilyn VillaruelNo ratings yet

- Production and Operations Management SyllabusDocument14 pagesProduction and Operations Management SyllabusEarl Russell S PaulicanNo ratings yet

- Entrepreneurship Report 1Document30 pagesEntrepreneurship Report 1Fretchie Anne LauroNo ratings yet

- Course Syllabus - Pom 1st Sem Ay 2019-2020Document7 pagesCourse Syllabus - Pom 1st Sem Ay 2019-2020api-194241825No ratings yet

- Business Finance FIDPDocument8 pagesBusiness Finance FIDPLizbethHazelRivera100% (1)

- Entrepreneurship 2011 ADocument4 pagesEntrepreneurship 2011 Arlcasana100% (1)

- MODULE 1 Introduction To Product ManagementDocument16 pagesMODULE 1 Introduction To Product ManagementESPINOLA MARGIENo ratings yet

- ACC 12 - Entrepreneurial Accounting Course Study GuideDocument66 pagesACC 12 - Entrepreneurial Accounting Course Study GuideHannah Jean MabunayNo ratings yet

- Entrepreneurial Management Module New6 2Document6 pagesEntrepreneurial Management Module New6 2Class LectureNo ratings yet

- Lesson Plan in Bookkeeping-Final DemoDocument4 pagesLesson Plan in Bookkeeping-Final DemoJuadjie ParbaNo ratings yet

- Updated-OBE-Syllabus MKTG 101 Professional SalesmanshipDocument7 pagesUpdated-OBE-Syllabus MKTG 101 Professional SalesmanshipAcademic OfficeNo ratings yet

- q4 Abm Fundamentals of Abm1 11 Week 3Document6 pagesq4 Abm Fundamentals of Abm1 11 Week 3Judy Ann Villanueva100% (1)

- Syllabus of Logistics ManagementDocument6 pagesSyllabus of Logistics ManagementWilliam DC RiveraNo ratings yet

- Q4 Principles of Marketing 12 - Module 5 (W2)Document18 pagesQ4 Principles of Marketing 12 - Module 5 (W2)Oreo McflurryNo ratings yet

- BMGT 323 Entrep 101 SyllabusDocument1 pageBMGT 323 Entrep 101 Syllabusmhyck100% (1)

- OBE Syllabus Market Research and Consumer Behavior San Francisco CollegeDocument4 pagesOBE Syllabus Market Research and Consumer Behavior San Francisco CollegeJerome SaavedraNo ratings yet

- Innovation Mgt-ObeDocument8 pagesInnovation Mgt-ObePlongzki TecsonNo ratings yet

- Mathematics 3 Week 4: Unified Supplementary Learning Materials Abm-Business MathematicsDocument12 pagesMathematics 3 Week 4: Unified Supplementary Learning Materials Abm-Business MathematicsRex MagdaluyoNo ratings yet

- Performance Task 2Document1 pagePerformance Task 2wivadaNo ratings yet

- Lesson 1 - Handout 1 - Fundamentals of AccountingDocument6 pagesLesson 1 - Handout 1 - Fundamentals of AccountingccgomezNo ratings yet

- FABM MID TERMS Exam PERFORMANCE TASKDocument3 pagesFABM MID TERMS Exam PERFORMANCE TASKRaymond RocoNo ratings yet

- Lesson PlanDocument3 pagesLesson PlanJasmin Caballero100% (2)

- Acco 20123 SyllabusDocument6 pagesAcco 20123 SyllabusglcpaNo ratings yet

- Case Analysis CoolMart IncDocument9 pagesCase Analysis CoolMart IncPrincessNo ratings yet

- Cost Accounting and Control Prelims RevisedDocument63 pagesCost Accounting and Control Prelims RevisedKienthvxxNo ratings yet

- Tomas Del Rosario College: City of Balanga Curricular Program: AccountancyDocument12 pagesTomas Del Rosario College: City of Balanga Curricular Program: AccountancyVanessa L. VinluanNo ratings yet

- Syllabus Assess 2Document10 pagesSyllabus Assess 2Vanessa L. VinluanNo ratings yet

- SYLLABUS CS212 Data Structure and Algorithm AnalysisDocument8 pagesSYLLABUS CS212 Data Structure and Algorithm AnalysisVanessa L. VinluanNo ratings yet

- CMO-No.19-s2008 BSNDocument1 pageCMO-No.19-s2008 BSNVanessa L. VinluanNo ratings yet

- Teaching Social Studies Syllabus FinalDocument11 pagesTeaching Social Studies Syllabus FinalVanessa L. VinluanNo ratings yet

- International Trade and AgreementsDocument1 pageInternational Trade and AgreementsVanessa L. VinluanNo ratings yet

- Tomas Del Rosario College: City of BalangaDocument5 pagesTomas Del Rosario College: City of BalangaVanessa L. VinluanNo ratings yet

- SYLLABUS CS311 Automata and Computation TheoryDocument10 pagesSYLLABUS CS311 Automata and Computation TheoryVanessa L. VinluanNo ratings yet

- Syllabus - Cs411-Multimedia System DevelopmentDocument7 pagesSyllabus - Cs411-Multimedia System DevelopmentVanessa L. VinluanNo ratings yet

- Methods of Teaching Syllabus - FinalDocument6 pagesMethods of Teaching Syllabus - FinalVanessa L. VinluanNo ratings yet

- Tomas Del Rosario College: Department: Business Administration I. Course Code: II. Course TitleDocument12 pagesTomas Del Rosario College: Department: Business Administration I. Course Code: II. Course TitleVanessa L. VinluanNo ratings yet

- Syllabus Product MGTDocument7 pagesSyllabus Product MGTVanessa L. VinluanNo ratings yet

- Facilities Management Lecture 3Document51 pagesFacilities Management Lecture 3Vanessa L. VinluanNo ratings yet

- Syllabus ENGLISH 4 Technical Writing OBE FORMATDocument5 pagesSyllabus ENGLISH 4 Technical Writing OBE FORMATVanessa L. VinluanNo ratings yet

- Syllabus - CS112-Program-Logic-FormulationDocument9 pagesSyllabus - CS112-Program-Logic-FormulationVanessa L. VinluanNo ratings yet

- Syllabus ENGLISH 4 OBE FORMATDocument6 pagesSyllabus ENGLISH 4 OBE FORMATVanessa L. VinluanNo ratings yet

- CS325 CS Elective 1 (Computer Graphics)Document4 pagesCS325 CS Elective 1 (Computer Graphics)Vanessa L. VinluanNo ratings yet

- Actg 3 Financial Accounting & Reporting, Part IDocument4 pagesActg 3 Financial Accounting & Reporting, Part IVanessa L. VinluanNo ratings yet

- Actg 2 Fundamentals of Accounting, Part IIDocument3 pagesActg 2 Fundamentals of Accounting, Part IIVanessa L. VinluanNo ratings yet

- NEW Syllabus OBE Format Readings in Phil. History Preliminaries 2021 2022Document6 pagesNEW Syllabus OBE Format Readings in Phil. History Preliminaries 2021 2022Vanessa L. VinluanNo ratings yet

- New Syllabus Facilitating Learner-CenteredDocument21 pagesNew Syllabus Facilitating Learner-CenteredVanessa L. VinluanNo ratings yet

- Actg 1 Fundamentals of Accounting, Part IDocument4 pagesActg 1 Fundamentals of Accounting, Part IVanessa L. VinluanNo ratings yet

- GUEVARRA Syllabus Math 2teaching Math in The Intermediate GradesDocument7 pagesGUEVARRA Syllabus Math 2teaching Math in The Intermediate GradesVanessa L. VinluanNo ratings yet

- Formerly Known As Sharika Enterprises Private LimitedDocument45 pagesFormerly Known As Sharika Enterprises Private LimitedKush MishraNo ratings yet

- Bankruptcy Law - AssignmentDocument6 pagesBankruptcy Law - AssignmentSophia HepheastouNo ratings yet

- Account Statement 20230530 20230629 110547Document3 pagesAccount Statement 20230530 20230629 110547DARANo ratings yet

- Assignment Foriegn Exchange Exp and RiskDocument31 pagesAssignment Foriegn Exchange Exp and RiskteddyNo ratings yet

- A Level Economics Essay-InflationDocument3 pagesA Level Economics Essay-Inflationtinomuvongashe mharazanyeNo ratings yet

- Accounts PracticalDocument22 pagesAccounts PracticalDivija MalhotraNo ratings yet

- Hospitality Financial Management Ch.4 Feasibility StudyDocument15 pagesHospitality Financial Management Ch.4 Feasibility StudyMuhammad Salihin JaafarNo ratings yet

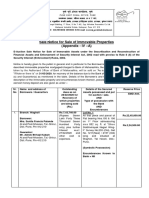

- Sale Notice For Sale of Immovable Properties (Appendix - IV - A)Document7 pagesSale Notice For Sale of Immovable Properties (Appendix - IV - A)Nikhil ShindeNo ratings yet

- Partnership LiquidationDocument3 pagesPartnership LiquidationBryaneNo ratings yet

- CARE Ratings As Sep2012Document191 pagesCARE Ratings As Sep2012Prashanth TapseNo ratings yet

- PFRS 11 - Joint ArrangementsDocument9 pagesPFRS 11 - Joint ArrangementsJona Mae Cuarto AyopNo ratings yet

- 2 - Corporate Governance PPT-02, Lecture-2,3 & 4Document37 pages2 - Corporate Governance PPT-02, Lecture-2,3 & 4PRAKHAR GUPTA100% (1)

- TAX 401 Percentage Tax Part 1Document7 pagesTAX 401 Percentage Tax Part 1Juan Miguel UngsodNo ratings yet

- Istisna Ijara Sukuk Structure FlowchartDocument2 pagesIstisna Ijara Sukuk Structure Flowchartprofbonds786100% (1)

- Tutorial Questions - Suspense and ErrorsDocument4 pagesTutorial Questions - Suspense and ErrorsDebbie DebzNo ratings yet

- Capital Structure TheoriesDocument2 pagesCapital Structure TheoriesTHEOPHILUS ATO FLETCHERNo ratings yet

- Garment Project Profile FinalDocument36 pagesGarment Project Profile Finalshivling100% (2)

- Client Information Sheet: Desire Davis ObadiaDocument5 pagesClient Information Sheet: Desire Davis ObadiaInverplay Corp0% (1)

- Diploma in IFRS (Level 1 and 2) : Your Passport To Financial Reporting ExcellenceDocument8 pagesDiploma in IFRS (Level 1 and 2) : Your Passport To Financial Reporting ExcellenceMuhammad Imran JehangirNo ratings yet

- Challan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into TheDocument1 pageChallan Form No. 32-A Treasury Copy: Challan of Cash/Transfer/Clearing Paid Into Thezafar iqbalNo ratings yet

- Preventive VigilanceDocument9 pagesPreventive VigilanceSuranjit BaralNo ratings yet

- The Global Trade and Investment EnvironmentDocument21 pagesThe Global Trade and Investment EnvironmentCarlo Niño GedoriaNo ratings yet

- Risk Management FinalDocument47 pagesRisk Management FinalManu YadavNo ratings yet

- 2.0 Marketing PlanDocument19 pages2.0 Marketing PlanflorenceviiNo ratings yet

- Sanchoy PatraDocument2 pagesSanchoy PatraSushen GainNo ratings yet

- Sec. 6. Classification of Shares. - The Shares of Stock of StockDocument9 pagesSec. 6. Classification of Shares. - The Shares of Stock of StockAnne BiagtanNo ratings yet

- GST Has Resolved The Double Taxation Dichotomy Under Previous Indirect Tax LawsDocument7 pagesGST Has Resolved The Double Taxation Dichotomy Under Previous Indirect Tax LawsSarthak TripathiNo ratings yet

- Illustrative Problems Chap7-8Document3 pagesIllustrative Problems Chap7-8Nikki GarciaNo ratings yet