You might also like

- Law On Partnership and Corporation by Hector de LeonDocument113 pagesLaw On Partnership and Corporation by Hector de LeonShiela Marie Vics75% (12)

- Income Taxation CHAPTER 4-NOTESDocument12 pagesIncome Taxation CHAPTER 4-NOTESMarkNo ratings yet

- Tax Remedies of The GovernmentDocument16 pagesTax Remedies of The GovernmentrmsenyoritaNo ratings yet

- Chapter 3-Income TaxDocument42 pagesChapter 3-Income TaxRochelle ChuaNo ratings yet

- Chapter 3taxDocument21 pagesChapter 3taxJustine AbreaNo ratings yet

- Chapter 04Document36 pagesChapter 04Rein ConcepcionNo ratings yet

- Cia15 Study Guide 4 Bac 103 Taxation Income Taxation SfernandoDocument23 pagesCia15 Study Guide 4 Bac 103 Taxation Income Taxation Sfernando5555-899341No ratings yet

- Bsa2 - TaxDocument40 pagesBsa2 - TaxLyca Nichol IbanNo ratings yet

- Income Taxation SchemesDocument2 pagesIncome Taxation SchemesLeonard Cañamo100% (4)

- Chapter 4Document25 pagesChapter 4crackheads philippinesNo ratings yet

- Accounting Periods and MethodsDocument51 pagesAccounting Periods and MethodsKenzel lawasNo ratings yet

- Lesson 5 Accounting PeriodDocument42 pagesLesson 5 Accounting PeriodCASTRO, HANNAH CAMILLE E.No ratings yet

- Tax RemediesDocument37 pagesTax RemediesMisshtaCNo ratings yet

- Income Tax Report - TOPIC 4&5Document65 pagesIncome Tax Report - TOPIC 4&5Jenny RanilloNo ratings yet

- Tax RemediesDocument56 pagesTax RemediesElaiza RegaladoNo ratings yet

- PDF 20221213 214318 0000 PDFDocument117 pagesPDF 20221213 214318 0000 PDFNCTDREAM 07No ratings yet

- Assessment ReturnDocument10 pagesAssessment ReturnTriila manillaNo ratings yet

- Tax Finals Summative s01Document4 pagesTax Finals Summative s01Von Andrei Medina100% (1)

- TAXATION SCHEMES EXPLAINEDDocument7 pagesTAXATION SCHEMES EXPLAINEDLeonard CañamoNo ratings yet

- Article About Provisional TaxDocument6 pagesArticle About Provisional Taxduanedejager01No ratings yet

- The Source of Canadian Tax Law:: Federal and Provincial Income Taxes Are Imposed On Only Three Basic Types of EntitiesDocument3 pagesThe Source of Canadian Tax Law:: Federal and Provincial Income Taxes Are Imposed On Only Three Basic Types of EntitiessarahNo ratings yet

- Accounting Periods and Methods of AccountingDocument11 pagesAccounting Periods and Methods of Accountingmhilet_chiNo ratings yet

- Accounting PeriodsDocument3 pagesAccounting PeriodsAna Mae CatubesNo ratings yet

- Chapter 4 TaxDocument3 pagesChapter 4 TaxSAFLOR, Edlyn Mae A.No ratings yet

- Income Tax Schemes, Accounting Periods, Methods, and ReportingDocument30 pagesIncome Tax Schemes, Accounting Periods, Methods, and ReportingamiNo ratings yet

- Tax AdministrationDocument5 pagesTax AdministrationAbdullahi AbdikadirNo ratings yet

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Document44 pagesPresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNo ratings yet

- CHAPTER 4 - IncomeTaxDocument7 pagesCHAPTER 4 - IncomeTaxVicente, Liza Mae C.No ratings yet

- CPA Reviewer: Introduction to Income TaxationDocument10 pagesCPA Reviewer: Introduction to Income TaxationmaeNo ratings yet

- Tax 1 Unit 1. Chapter 4Document5 pagesTax 1 Unit 1. Chapter 4angelika dijamcoNo ratings yet

- Taxation 1 Transcript (Part 5 Syllabus)Document8 pagesTaxation 1 Transcript (Part 5 Syllabus)cristiepearlNo ratings yet

- TAX 1 ReviewerDocument10 pagesTAX 1 ReviewerAngelaNo ratings yet

- Companies Income Tax and Other Taxes As at Feb 2023Document10 pagesCompanies Income Tax and Other Taxes As at Feb 2023BaneNo ratings yet

- Income Tax Schemes and Accounting MethodsDocument28 pagesIncome Tax Schemes and Accounting MethodsCJ GranadaNo ratings yet

- Filing Tax ReturnsDocument10 pagesFiling Tax ReturnsSamNo ratings yet

- Income TaxationDocument6 pagesIncome TaxationJahz Aira GamboaNo ratings yet

- Taxation: Basic ConceptsDocument10 pagesTaxation: Basic ConceptsVineet RajNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- IT NotesDocument58 pagesIT NotesIshitaNo ratings yet

- FABM2 Module 09 (Q2-W3-5)Document9 pagesFABM2 Module 09 (Q2-W3-5)Christian Zebua50% (4)

- Siena College of Taytay Inc. Taxation 1 - Income Taxation College of Business and AccountancyDocument2 pagesSiena College of Taytay Inc. Taxation 1 - Income Taxation College of Business and AccountancyDonnan OreaNo ratings yet

- Income Tax Schemes, Accounting Periods, Accounting Methods, and ReportingDocument4 pagesIncome Tax Schemes, Accounting Periods, Accounting Methods, and ReportingColeen BiocalesNo ratings yet

- Taxation 1 NotesDocument27 pagesTaxation 1 NotesKate CalansinginNo ratings yet

- Dimaampao NotesDocument68 pagesDimaampao Notesgeorgeannarayco100% (2)

- 3 Income Tax ConceptsDocument37 pages3 Income Tax ConceptsRommel Espinocilla Jr.No ratings yet

- C BAC7 MODULE 3 Tax RemediesDocument9 pagesC BAC7 MODULE 3 Tax RemediesJOSHUA M. ESCOTONo ratings yet

- Filing Requirementsestimated Returns and PaymentsDocument8 pagesFiling Requirementsestimated Returns and Paymentsbest tax filerNo ratings yet

- Methods of Accounting: AX Ccounting Eriods AND EthodsDocument11 pagesMethods of Accounting: AX Ccounting Eriods AND EthodsAiron BendañaNo ratings yet

- What Is IncomeDocument6 pagesWhat Is Incomenaman guptaNo ratings yet

- Assessment ProcedureDocument7 pagesAssessment Procedurebabajan_4No ratings yet

- Nmba FM 03: Tax Planning and Management Unit IDocument19 pagesNmba FM 03: Tax Planning and Management Unit IParul GargNo ratings yet

- 5.1-Module 5Document3 pages5.1-Module 5Arpita ArtaniNo ratings yet

- Tax Amnesty - Said. Redeem. Relieved: PictureDocument4 pagesTax Amnesty - Said. Redeem. Relieved: PictureANGELINA ANGELINANo ratings yet

- Income Tax Schemes, Accounting Periods, Accounting Methods, and ReportingDocument6 pagesIncome Tax Schemes, Accounting Periods, Accounting Methods, and ReportingAilene MendozaNo ratings yet

- Income Tax Schemes, Accounting Periods, Accounting Methods and ReportingDocument32 pagesIncome Tax Schemes, Accounting Periods, Accounting Methods and ReportingSassy GirlNo ratings yet

- Income Taxation RulesDocument5 pagesIncome Taxation RulesJacqueline SyNo ratings yet

- Business Taxation Unit 1Document23 pagesBusiness Taxation Unit 1Akash GoreNo ratings yet

- Income Tax in GeneralDocument6 pagesIncome Tax in GeneralMatt Marqueses PanganibanNo ratings yet

- TAXNDocument22 pagesTAXNMonica MonicaNo ratings yet

- Bookkeeping and recording rulesDocument2 pagesBookkeeping and recording rulesCecilia AngelineNo ratings yet

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- Partnership - An OverviewDocument12 pagesPartnership - An OverviewRochelle ChuaNo ratings yet

- Chapter 2 - Income TaxDocument30 pagesChapter 2 - Income TaxRochelle ChuaNo ratings yet

- Chapter 1-Income TaxDocument56 pagesChapter 1-Income TaxRochelle ChuaNo ratings yet

- Advanced Grammar and CompositionDocument22 pagesAdvanced Grammar and CompositionRochelle Chua100% (1)

- Agency: Classification of Agents On The Basis of Authority On The Basis of Nature of WorkDocument8 pagesAgency: Classification of Agents On The Basis of Authority On The Basis of Nature of WorkATBNo ratings yet

- Provisions, Contingent Liabilities and Contingent Assets: Problem 1: True or FalseDocument6 pagesProvisions, Contingent Liabilities and Contingent Assets: Problem 1: True or FalseKim HanbinNo ratings yet

- Chapter 9 Assigned Question SOLUTIONSDocument31 pagesChapter 9 Assigned Question SOLUTIONSDang ThanhNo ratings yet

- Week 3 ModuleDocument14 pagesWeek 3 ModuleSofia Biangca M. BalderasNo ratings yet

- Industrial Disputes ResolutionDocument9 pagesIndustrial Disputes ResolutionNitinNo ratings yet

- Airline Business Plan Air LeoDocument64 pagesAirline Business Plan Air LeokgmakNo ratings yet

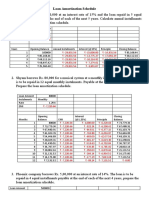

- Solution Time Value of Money 5 Loan Amortization Schedule and PV of Perpetual Annuity and PV Growing Annuity 3PVyvICyHiDocument5 pagesSolution Time Value of Money 5 Loan Amortization Schedule and PV of Perpetual Annuity and PV Growing Annuity 3PVyvICyHiShareshth JainNo ratings yet

- Output Determination: Contributed by Prabhakant Tiwari Under The Guidance of SAP GURU INDIADocument9 pagesOutput Determination: Contributed by Prabhakant Tiwari Under The Guidance of SAP GURU INDIASeren SökmenNo ratings yet

- How To Use This Template: Delete This Slide Before Submitting Your AssignmentDocument11 pagesHow To Use This Template: Delete This Slide Before Submitting Your AssignmentAnnah AnnNo ratings yet

- Substantive Procedures: 1) Trade RecievablesDocument3 pagesSubstantive Procedures: 1) Trade RecievablesMeghaNo ratings yet

- Cir VS Transitions OpticalDocument2 pagesCir VS Transitions OpticalDaLe AparejadoNo ratings yet

- Barclays Case Study.Document2 pagesBarclays Case Study.ReemaNo ratings yet

- Understanding Mergers and Acquisitions (M&A) Introduction: Mergers and Acquisitions (M&A) Are Complex Financial Transactions That InvolveDocument2 pagesUnderstanding Mergers and Acquisitions (M&A) Introduction: Mergers and Acquisitions (M&A) Are Complex Financial Transactions That InvolveSebastian StolkinerNo ratings yet

- Privatization and Management Office v. Court of Tax AppealsDocument7 pagesPrivatization and Management Office v. Court of Tax AppealsBeltran KathNo ratings yet

- Lorelle CarenderiaDocument22 pagesLorelle CarenderiaShiela may AdlawonNo ratings yet

- Child Nutrition Procurement 2022Document91 pagesChild Nutrition Procurement 2022Jesse VillarrealNo ratings yet

- 1.10 International Organization NewDocument14 pages1.10 International Organization NewArbind YadavNo ratings yet

- Week 1 - Introduction, Ethical and Legal IssuesDocument3 pagesWeek 1 - Introduction, Ethical and Legal IssuesTaneisha McLeanNo ratings yet

- Doles Vs AngelesDocument2 pagesDoles Vs Angelesfermo ii ramosNo ratings yet

- E-Commerce Website Using MERN StackDocument5 pagesE-Commerce Website Using MERN StackIJRASETPublicationsNo ratings yet

- Chapter 2 The Concept of Audit Syllabus 2023Document88 pagesChapter 2 The Concept of Audit Syllabus 2023nguyenanleybNo ratings yet

- MPU3222 - Course Introduction Briefing For Student (Sem 1 - 2022-2023) (I)Document24 pagesMPU3222 - Course Introduction Briefing For Student (Sem 1 - 2022-2023) (I)trickyhunter9999No ratings yet

- Sap Fi Budget Balance ReportsDocument58 pagesSap Fi Budget Balance ReportsPallavi ChawlaNo ratings yet

- Selling Groceries Through The Cloud in A Tier II City in IndiaDocument12 pagesSelling Groceries Through The Cloud in A Tier II City in IndiaFathima HeeraNo ratings yet

- Semi Formal ExamplesDocument3 pagesSemi Formal ExamplesDjshh oiNo ratings yet

- On September 1 2011 The Account Balances of Rand Equipment PDFDocument1 pageOn September 1 2011 The Account Balances of Rand Equipment PDFM Bilal SaleemNo ratings yet

- Ez Mill: Low-Cost Portable Hammer Mill Helps Small FarmersDocument37 pagesEz Mill: Low-Cost Portable Hammer Mill Helps Small FarmersANIME CHANNo ratings yet

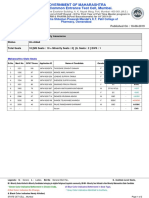

- Maharashtra Pharmacy Seat Allotment for CAP Round IIIDocument2 pagesMaharashtra Pharmacy Seat Allotment for CAP Round IIIPharmacy Admission ExpertNo ratings yet

- Nomco Charter 2022Document3 pagesNomco Charter 2022abcNo ratings yet

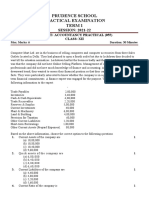

- Prudence School Accountancy Practical ExamDocument2 pagesPrudence School Accountancy Practical Examicarus fallsNo ratings yet