You might also like

- Lease Finance - 1Document10 pagesLease Finance - 1don_mahinNo ratings yet

- Leasing - Student SupportDocument12 pagesLeasing - Student SupportAbhinav KumarNo ratings yet

- BUSM365 CH7 Student Version .XLSX 1Document14 pagesBUSM365 CH7 Student Version .XLSX 1Kesarapu Venkata ApparaoNo ratings yet

- Seatwork 12/1/21 cash flow analysisDocument7 pagesSeatwork 12/1/21 cash flow analysisRhea SodelaNo ratings yet

- Kainat Mazhar FM Lab NewDocument16 pagesKainat Mazhar FM Lab Newi234579No ratings yet

- Chapter 5 Answers to Problems and Financial AnalysisDocument11 pagesChapter 5 Answers to Problems and Financial AnalysisEvan AzizNo ratings yet

- Chapter 14 LEASINGDocument17 pagesChapter 14 LEASINGKaran KashyapNo ratings yet

- Primus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungDocument26 pagesPrimus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungfmulyanaNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Lease - LessorDocument8 pagesLease - LessorMonique ElineNo ratings yet

- Finance lease calculation and journal entriesDocument8 pagesFinance lease calculation and journal entriesAdilla KhulaidahNo ratings yet

- Practice Set 9 BondsDocument11 pagesPractice Set 9 BondsVivek JainNo ratings yet

- Calculating finance lease accounting entriesDocument7 pagesCalculating finance lease accounting entriessajedulNo ratings yet

- Primus AutomationDocument23 pagesPrimus AutomationhimanshusangaNo ratings yet

- IA - Receivables Addtl ConceptsDocument3 pagesIA - Receivables Addtl ConceptsDiana AcostaNo ratings yet

- Intermediate Accounting 2 Final ExamDocument35 pagesIntermediate Accounting 2 Final ExamJEFFERSON CUTE97% (32)

- Chapter 18 LabDocument6 pagesChapter 18 LabTran Kim Tram PhanNo ratings yet

- Statement of CashflowDocument9 pagesStatement of CashflowOwen Lustre50% (2)

- 03 LeasingDocument16 pages03 Leasingnotes.mcpuNo ratings yet

- Leasing ExerciseDocument6 pagesLeasing ExerciseeugeniadgzNo ratings yet

- Accounting LesseeDocument7 pagesAccounting Lesseeangelian bagadiongNo ratings yet

- Week 3 SolutionDocument5 pagesWeek 3 SolutionI190006 Taimoor JanNo ratings yet

- Project ADVANCE FINANCIAL MANAGEMENTDocument11 pagesProject ADVANCE FINANCIAL MANAGEMENTBilal KhalidNo ratings yet

- Assigment 4 Tutor Financial Accounting II - Audry Martarini Putri - 210169622Document8 pagesAssigment 4 Tutor Financial Accounting II - Audry Martarini Putri - 210169622Oshin MenNo ratings yet

- poa_2012_Jan_p.2.q.1_1Document4 pagespoa_2012_Jan_p.2.q.1_1RealGenius (Carl)No ratings yet

- Term Loan and Lease Financing Worked-Out ProblemsDocument13 pagesTerm Loan and Lease Financing Worked-Out ProblemsSoo CealNo ratings yet

- Intacc2-Quiz ExamDocument5 pagesIntacc2-Quiz ExamCmNo ratings yet

- Making Capital Investment DecisionsDocument48 pagesMaking Capital Investment DecisionsJerico ClarosNo ratings yet

- Final Exam SFM (Reppi, Michelle Gladys)Document7 pagesFinal Exam SFM (Reppi, Michelle Gladys)Bervie RondonuwuNo ratings yet

- Ch08 - Principles of Capital InvestmentDocument7 pagesCh08 - Principles of Capital InvestmentStevin GeorgeNo ratings yet

- SPREADSHEET APPLICATIONS - PEA 2021-2022 SESSION - Case StudiesDocument8 pagesSPREADSHEET APPLICATIONS - PEA 2021-2022 SESSION - Case StudiesOladapo Oluwakayode AbiodunNo ratings yet

- August 20 - Notes PayableDocument4 pagesAugust 20 - Notes PayableRodolfo Jr. LasquiteNo ratings yet

- Bai Tap Ias36Document25 pagesBai Tap Ias36Thiện PhátNo ratings yet

- 2022 Sem 1 ACC10007 Lecture IllustrationsDocument8 pages2022 Sem 1 ACC10007 Lecture IllustrationsJordanNo ratings yet

- Intacc2-Quiz ExamDocument10 pagesIntacc2-Quiz ExamCmNo ratings yet

- RMC No. 11-2024 - Annex A - Illustrations and Accounting EntriesDocument3 pagesRMC No. 11-2024 - Annex A - Illustrations and Accounting EntriesAnostasia NemusNo ratings yet

- LBO TITLEDocument16 pagesLBO TITLEsingh0001No ratings yet

- Calculate loan EMI and outstanding balance over timeDocument3 pagesCalculate loan EMI and outstanding balance over timeShirish BaisaneNo ratings yet

- IA-2 FINAL EXAM ANSWER KEYDocument4 pagesIA-2 FINAL EXAM ANSWER KEYCarlos arnaldo lavadoNo ratings yet

- INTERMEDIATE TECHNICAL CERTIFICATE EXAMINATION JUNE 2022Document12 pagesINTERMEDIATE TECHNICAL CERTIFICATE EXAMINATION JUNE 2022serge folegweNo ratings yet

- BRS3B Assessment Opportunity 1 2019Document11 pagesBRS3B Assessment Opportunity 1 2019221103909No ratings yet

- Intac QuizDocument4 pagesIntac QuizPamela Joy AlvarezNo ratings yet

- Description: Tags: 668appgDocument2 pagesDescription: Tags: 668appganon-829526No ratings yet

- ACCT 202 Pre-Quiz Number 2 Spring 2018Document6 pagesACCT 202 Pre-Quiz Number 2 Spring 2018Lexzy Chant LopezNo ratings yet

- PDF PDFDocument7 pagesPDF PDFMikey MadRatNo ratings yet

- Chu de 3 Nhom 6 Hay PDFDocument10 pagesChu de 3 Nhom 6 Hay PDFNhư NhưNo ratings yet

- Finance and Operating Lease Exercise (Solution)Document10 pagesFinance and Operating Lease Exercise (Solution)Emnet AbNo ratings yet

- Psaf Revision Day 3 May 2023Document8 pagesPsaf Revision Day 3 May 2023Esther AkpanNo ratings yet

- BF405 May 2019 PDFDocument5 pagesBF405 May 2019 PDFhuku memeNo ratings yet

- Adelia Marhamah. 4C Lat 42 Moonstruck CompanyDocument10 pagesAdelia Marhamah. 4C Lat 42 Moonstruck Companyanisa MuzaqiNo ratings yet

- Notes ReceivablesDocument2 pagesNotes ReceivablesNo NotreallyNo ratings yet

- Income Statement and Balance Sheet AnalysisDocument18 pagesIncome Statement and Balance Sheet AnalysisKailash KumarNo ratings yet

- Test 4 Bervie R (1) 5Document2 pagesTest 4 Bervie R (1) 5Bervie RondonuwuNo ratings yet

- Rent Vs Buy Calculator - AssetyogiDocument1 pageRent Vs Buy Calculator - AssetyogiRanjit MishraNo ratings yet

- Principles of Accounting 5th Edition Smart Solutions ManualDocument9 pagesPrinciples of Accounting 5th Edition Smart Solutions Manualspaidvulcano8wlriz100% (19)

- Spartan Inc - German MotorsDocument4 pagesSpartan Inc - German MotorsFavian Maraville YadisaputraNo ratings yet

- PricewaterhouseCoopers' Guide to the New Tax RulesFrom EverandPricewaterhouseCoopers' Guide to the New Tax RulesNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- What Every Real Estate Investor Needs to Know About Cash Flow...And 36 Other Key FInancial MeasuresFrom EverandWhat Every Real Estate Investor Needs to Know About Cash Flow...And 36 Other Key FInancial MeasuresRating: 4.5 out of 5 stars4.5/5 (9)

- Using The Activecelldemo Macro: 5 #Value! 11 #Value!Document16 pagesUsing The Activecelldemo Macro: 5 #Value! 11 #Value!Syed Ameer Ali ShahNo ratings yet

- fm3 Chapter36Document11 pagesfm3 Chapter36Syed Ameer Ali ShahNo ratings yet

- Using Transpose: A B C D E F G 1 2 3 4Document24 pagesUsing Transpose: A B C D E F G 1 2 3 4Syed Ameer Ali ShahNo ratings yet

- fm3 Chapter41Document34 pagesfm3 Chapter41Syed Ameer Ali ShahNo ratings yet

- fm3 Chapter35Document21 pagesfm3 Chapter35Syed Ameer Ali ShahNo ratings yet

- Using Excel'S Rand FunctionDocument239 pagesUsing Excel'S Rand FunctionSyed Ameer Ali ShahNo ratings yet

- The Immunization Problem: Illustrated For The 30-Year BondDocument18 pagesThe Immunization Problem: Illustrated For The 30-Year BondSyed Ameer Ali ShahNo ratings yet

- fm3 Chapter27Document79 pagesfm3 Chapter27Syed Ameer Ali ShahNo ratings yet

- Excel'S NPV FunctionDocument41 pagesExcel'S NPV FunctionSyed Ameer Ali ShahNo ratings yet

- Black-Scholes Option-Pricing Formula: Data Table: Comparing The Black-Scholes To The Intrinsic ValueDocument47 pagesBlack-Scholes Option-Pricing Formula: Data Table: Comparing The Black-Scholes To The Intrinsic ValueSyed Ameer Ali ShahNo ratings yet

- Fm3 - Chapter26, Mcculloch Term StructuresDocument3 pagesFm3 - Chapter26, Mcculloch Term StructuresSyed Ameer Ali ShahNo ratings yet

- Matrices in Excel: Matrix A (A Row Vector) Matrix B (Square 3 X 3 Matrix) Matrix C (Column Vector)Document14 pagesMatrices in Excel: Matrix A (A Row Vector) Matrix B (Square 3 X 3 Matrix) Matrix C (Column Vector)Syed Ameer Ali ShahNo ratings yet

- Black-Scholes Option Pricing Formula Applied To General Pills PutDocument25 pagesBlack-Scholes Option Pricing Formula Applied To General Pills PutSyed Ameer Ali ShahNo ratings yet

- The Option To Expand: Black-Scholes Option Pricing FormulaDocument29 pagesThe Option To Expand: Black-Scholes Option Pricing FormulaSyed Ameer Ali ShahNo ratings yet

- Session20 DataFile BarrierDocument22 pagesSession20 DataFile BarriermohitNo ratings yet

- Underlying Assets and Path-Independent Versus Path-Dependent PayoffsDocument39 pagesUnderlying Assets and Path-Independent Versus Path-Dependent PayoffsSyed Ameer Ali ShahNo ratings yet

- Expected Return On A One-Year Bond With An Adjustment For Default ProbabilityDocument83 pagesExpected Return On A One-Year Bond With An Adjustment For Default ProbabilitySyed Ameer Ali ShahNo ratings yet

- Fm3 - Chapter13 (Portfolio Optimization)Document46 pagesFm3 - Chapter13 (Portfolio Optimization)Syed Ameer Ali ShahNo ratings yet

- Session20 DataFile AsianDocument15 pagesSession20 DataFile AsianJosé Carlos GBNo ratings yet

- Black-Scholes Greeks This Spreadsheet Uses The Merton Model For A Continuously Dividend-Paying StockDocument44 pagesBlack-Scholes Greeks This Spreadsheet Uses The Merton Model For A Continuously Dividend-Paying StockSyed Ameer Ali ShahNo ratings yet

- The Unit Circle: For The Quarter Circle and The Pi Experiment, See The Graph BelowDocument36 pagesThe Unit Circle: For The Quarter Circle and The Pi Experiment, See The Graph BelowSyed Ameer Ali ShahNo ratings yet

- The Event Study Time Line: Estimation Window Event WindowDocument194 pagesThe Event Study Time Line: Estimation Window Event WindowSyed Ameer Ali ShahNo ratings yet

- Basic Duration Calculation: Year C T C / Price (1+YTM) C T C / Price (1+YTM)Document13 pagesBasic Duration Calculation: Year C T C / Price (1+YTM) C T C / Price (1+YTM)Syed Ameer Ali ShahNo ratings yet

- Calculating The Efficient FrontierDocument31 pagesCalculating The Efficient FrontierSyed Ameer Ali ShahNo ratings yet

- Probability of End-Year Portfolio ValueDocument130 pagesProbability of End-Year Portfolio ValueSyed Ameer Ali ShahNo ratings yet

- Binomial Option Pricing in A One-Period Model: Stock Price Bond PriceDocument36 pagesBinomial Option Pricing in A One-Period Model: Stock Price Bond PriceSyed Ameer Ali ShahNo ratings yet

- Annual Stock Price and Return Data For Six StocksDocument37 pagesAnnual Stock Price and Return Data For Six StocksSyed Ameer Ali ShahNo ratings yet

- Call Option Payoff Patterns: Time 0 Time TDocument23 pagesCall Option Payoff Patterns: Time 0 Time TSyed Ameer Ali ShahNo ratings yet

- Portfolio Optimization Allowing Short Sales: Variance-Covariance Matrix MeansDocument21 pagesPortfolio Optimization Allowing Short Sales: Variance-Covariance Matrix MeansSyed Ameer Ali ShahNo ratings yet

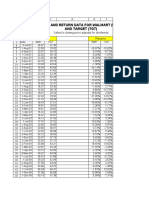

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- Prisoner of ZendaDocument27 pagesPrisoner of ZendaSauban AhmedNo ratings yet

- PHSS Control Strategy White PaperDocument13 pagesPHSS Control Strategy White PaperAkuWilliams100% (1)

- USA2Document2 pagesUSA2Helena TrầnNo ratings yet

- Achievement Gaps Mindset Belonging FeedbackDocument4 pagesAchievement Gaps Mindset Belonging FeedbackResearchteam2014No ratings yet

- Yes O Action Plan FinalDocument4 pagesYes O Action Plan FinalRHENAN BACOLOD100% (1)

- NAME: - Grade Level: 12 Q:2 - Lesson: 1Document2 pagesNAME: - Grade Level: 12 Q:2 - Lesson: 1neschee leeNo ratings yet

- Krishna Grameena BankDocument101 pagesKrishna Grameena BankSuresh Babu ReddyNo ratings yet

- Estmt - 2024 01 05Document8 pagesEstmt - 2024 01 05alejandro860510No ratings yet

- GSCR Report China KoreaDocument313 pagesGSCR Report China KoreaD.j. DXNo ratings yet

- History and Political Science: Solution: Practice Activity Sheet 3Document9 pagesHistory and Political Science: Solution: Practice Activity Sheet 3Faiz KhanNo ratings yet

- Confidentiality Agreement GuideDocument11 pagesConfidentiality Agreement GuideSeema WadkarNo ratings yet

- Letter From Canute FranksonDocument2 pagesLetter From Canute FranksonAbraham Lincoln Brigade ArchiveNo ratings yet

- Tracking DepEd Division Funds for Disaster MonitoringDocument2 pagesTracking DepEd Division Funds for Disaster MonitoringMamad Tomara BatingoloNo ratings yet

- Báo cáo cuối kì môn thực hành an ninh mạngDocument5 pagesBáo cáo cuối kì môn thực hành an ninh mạngDương Thành ĐạtNo ratings yet

- Local Power of Eminent DomainDocument13 pagesLocal Power of Eminent DomainLab LeeNo ratings yet

- Seismic Vulnerability of Structures in Sikkim During 2011 EarthquakeDocument20 pagesSeismic Vulnerability of Structures in Sikkim During 2011 EarthquakeManpreet SinghNo ratings yet

- Strategic Management Journal Article Breaks Down Strategizing vs EconomizingDocument20 pagesStrategic Management Journal Article Breaks Down Strategizing vs EconomizingVinícius RodriguesNo ratings yet

- Micro and Macro Environment of NestleDocument2 pagesMicro and Macro Environment of Nestlewaheedahmedarain56% (18)

- Study On Comparative Analysis of Icici Bank and HDFC Bank Mutual Fund SchemesDocument8 pagesStudy On Comparative Analysis of Icici Bank and HDFC Bank Mutual Fund SchemesRaja DasNo ratings yet

- Fallacies EssayDocument1 pageFallacies EssayrahimNo ratings yet

- The Impact of Innovative Digital Marketing Strategy On Small Firm PerformanceDocument43 pagesThe Impact of Innovative Digital Marketing Strategy On Small Firm PerformanceFavour ChukwuelesieNo ratings yet

- Business PlanDocument12 pagesBusiness PlanSaqib FayyazNo ratings yet

- Minutes Feb 28 2022Document5 pagesMinutes Feb 28 2022Raquel dg.BulaongNo ratings yet

- Imagine by John LennonDocument3 pagesImagine by John Lennonmichelle12wong4000No ratings yet

- CIMA's Background as Malaysia's Third Largest Cement ManufacturerDocument47 pagesCIMA's Background as Malaysia's Third Largest Cement ManufacturerApom LenggangNo ratings yet

- SociologyDocument3 pagesSociologyMuxammil ArshNo ratings yet

- History of The Alphabet Sejarah AbjadDocument29 pagesHistory of The Alphabet Sejarah AbjadEmian MangaNo ratings yet

- UP v. Calleja - G.R. No. 96189 - July 14, 1992 - DIGESTDocument4 pagesUP v. Calleja - G.R. No. 96189 - July 14, 1992 - DIGESTFe A. Bartolome0% (1)

- Computation of Basic and Diluted Eps Charles Austin of The PDFDocument1 pageComputation of Basic and Diluted Eps Charles Austin of The PDFAnbu jaromiaNo ratings yet

- Microeconomics 20th Edition Mcconnell Test BankDocument25 pagesMicroeconomics 20th Edition Mcconnell Test BankMeganAguilarkpjrz100% (56)