You might also like

- J.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnNo ratings yet

- Bonnie Road ModelDocument14 pagesBonnie Road Modelmzhao8100% (1)

- ZipCar SolutionDocument15 pagesZipCar SolutionAshwinKumarNo ratings yet

- Solution Manual For Oracle 12c SQL 3rd Edition CasteelDocument6 pagesSolution Manual For Oracle 12c SQL 3rd Edition CasteelHeatherRobertstwopa100% (35)

- Lease Vs Buy AnalysisDocument4 pagesLease Vs Buy AnalysisMuhammed Amjad IslamNo ratings yet

- McMillan 2007. Fish - Histology PDFDocument603 pagesMcMillan 2007. Fish - Histology PDFMarcela Mesa100% (1)

- Digital Systems Design and PrototypingDocument633 pagesDigital Systems Design and PrototypingAshish Shrivastava50% (2)

- VC and IPO NumericalDocument16 pagesVC and IPO Numericaluse lnctNo ratings yet

- Assignment - Operating Lease & Direct Financing LeaseDocument8 pagesAssignment - Operating Lease & Direct Financing Leaseangelian bagadiongNo ratings yet

- Qualititative Test of Lipids and Preparation of Carboxylic Acid Salt From LipidsDocument6 pagesQualititative Test of Lipids and Preparation of Carboxylic Acid Salt From LipidsNurul Farhana NasirNo ratings yet

- 03 LeasingDocument16 pages03 Leasingnotes.mcpuNo ratings yet

- 29116520Document6 pages29116520Rendy Setiadi MangunsongNo ratings yet

- ITC - Sales and DistributionDocument36 pagesITC - Sales and DistributionAbhinav KumarNo ratings yet

- Primus AutomationDocument23 pagesPrimus AutomationhimanshusangaNo ratings yet

- Crochet Pattern "Doll-Chamomile": TanaticrochetDocument9 pagesCrochet Pattern "Doll-Chamomile": TanaticrochetElene Lomidze100% (1)

- Simple Lease MethodDocument11 pagesSimple Lease MethodZeusNo ratings yet

- How Not To Analyze A LeaseDocument7 pagesHow Not To Analyze A LeaseSyed Ameer Ali ShahNo ratings yet

- Leasing ExerciseDocument6 pagesLeasing ExerciseeugeniadgzNo ratings yet

- LeasingDocument14 pagesLeasingSana SarfarazNo ratings yet

- Lease Finance - 1Document10 pagesLease Finance - 1don_mahinNo ratings yet

- Lease Question and SolutionDocument7 pagesLease Question and SolutionsajedulNo ratings yet

- Lease - LessorDocument8 pagesLease - LessorMonique ElineNo ratings yet

- Obtain A Bank Loan For 100% of The Purchase Price, or It Can Lease The Machinery. Assume That The Following Facts ApplyDocument4 pagesObtain A Bank Loan For 100% of The Purchase Price, or It Can Lease The Machinery. Assume That The Following Facts Applydahnil dicardoNo ratings yet

- IFRS NotesDocument2 pagesIFRS NotesArchana M.DNo ratings yet

- Sales Forecast Unit SalesDocument7 pagesSales Forecast Unit SalesSyed ShaheerNo ratings yet

- BUSM365 CH7 Student Version .XLSX 1Document14 pagesBUSM365 CH7 Student Version .XLSX 1Kesarapu Venkata ApparaoNo ratings yet

- Accounting-Assignment - Sales Type & Sales and LeasebackDocument8 pagesAccounting-Assignment - Sales Type & Sales and Leasebackangelian bagadiongNo ratings yet

- Example On Operating Lease and Finance LeaseDocument6 pagesExample On Operating Lease and Finance LeasekakshahNo ratings yet

- Red Chilli WorkingsDocument10 pagesRed Chilli WorkingsImran UmarNo ratings yet

- Primus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungDocument26 pagesPrimus Automation: Robert Clark Rey Mendez Nate Wills Katie YoungfmulyanaNo ratings yet

- 1714, Khitab, FS1Document4 pages1714, Khitab, FS1Ahmad KhitabNo ratings yet

- Sales Type Lease - LessorDocument19 pagesSales Type Lease - LessorRogelynCodillaNo ratings yet

- Preleased Office in Andheri East 2097Document4 pagesPreleased Office in Andheri East 2097qwikkreturnsNo ratings yet

- Question4 Solved With GraphDocument8 pagesQuestion4 Solved With GraphShafiqUr RehmanNo ratings yet

- Book 1Document4 pagesBook 1Swapan Kumar SahaNo ratings yet

- General Data: Lessee:: Input Data: Key OutputDocument10 pagesGeneral Data: Lessee:: Input Data: Key OutputShafiqUr RehmanNo ratings yet

- FINAMAA Topic 2 Additional ActivityDocument2 pagesFINAMAA Topic 2 Additional ActivityJeasmine Andrea Diane PayumoNo ratings yet

- NPV LesseeDocument6 pagesNPV Lesseekabirsharan4No ratings yet

- Adelia Marhamah. 4C Lat 42 Moonstruck CompanyDocument10 pagesAdelia Marhamah. 4C Lat 42 Moonstruck Companyanisa MuzaqiNo ratings yet

- Project Report For Home AllplianceDocument6 pagesProject Report For Home Allpliancerajesh patelNo ratings yet

- Primus Calculation Syndicate 6Document58 pagesPrimus Calculation Syndicate 6Bayu Aji PrasetyoNo ratings yet

- Pt. Cahaya Neraca Saldo Per 31 Desember 2018: Soal LatihanDocument2 pagesPt. Cahaya Neraca Saldo Per 31 Desember 2018: Soal LatihanBelindaNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Ots 24 24009366 Annexure AmlaDocument17 pagesOts 24 24009366 Annexure Amlaapi-3774915No ratings yet

- Poultry Farm For 10000 ChicksDocument7 pagesPoultry Farm For 10000 ChicksDebashish PhoneNo ratings yet

- Balance Sheet 12345Document32 pagesBalance Sheet 12345Anurag KshatriNo ratings yet

- Accounting and Financial Management-ProjectDocument8 pagesAccounting and Financial Management-ProjectMelokuhle MhlongoNo ratings yet

- TM PQsDocument10 pagesTM PQsAnooshayNo ratings yet

- Accounts Assignment Class 11 CandE 20220111131012374Document5 pagesAccounts Assignment Class 11 CandE 20220111131012374Jithu EmmanuelNo ratings yet

- Module 10-SALES TYPE LEASE - LESSORDocument8 pagesModule 10-SALES TYPE LEASE - LESSORJeanivyle CarmonaNo ratings yet

- Car WasheDocument18 pagesCar WasheABU YEROMENo ratings yet

- PM AssignmentDocument9 pagesPM AssignmentdebojyotiNo ratings yet

- Intacc2-Quiz ExamDocument10 pagesIntacc2-Quiz ExamCmNo ratings yet

- 8b Tut Questions SolutionsDocument3 pages8b Tut Questions SolutionsMk SANo ratings yet

- BRS3B Assessment Opportunity 1 2019Document11 pagesBRS3B Assessment Opportunity 1 2019221103909No ratings yet

- Session 12 - LeasingDocument7 pagesSession 12 - LeasingAlfatih 1453100% (1)

- Jawab Latihan Soal Akt Keu 2Document5 pagesJawab Latihan Soal Akt Keu 2221210061No ratings yet

- CAR LoanDocument1 pageCAR LoanRalphNo ratings yet

- Mr. M S/o R Annexure (A) To The Project Cost of Project and Means of Finance Cost of Project Amount (RS)Document9 pagesMr. M S/o R Annexure (A) To The Project Cost of Project and Means of Finance Cost of Project Amount (RS)Santhosh Kumar BattaNo ratings yet

- Week 3 SolutionDocument5 pagesWeek 3 SolutionI190006 Taimoor JanNo ratings yet

- Business Examples 2021Document12 pagesBusiness Examples 2021Faizan HyderNo ratings yet

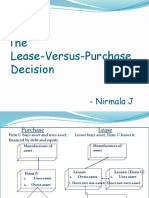

- Lease Versus PurchasingDocument10 pagesLease Versus PurchasingnirmalajNo ratings yet

- Homework Chapter 18 and 19Document7 pagesHomework Chapter 18 and 19doejohn150No ratings yet

- ExcerciseDocument10 pagesExcercisehafizulNo ratings yet

- SDM Previous Year Question Discuss The Operational Decisions of Sales Management. Explain It in The Context of Any CompanyDocument4 pagesSDM Previous Year Question Discuss The Operational Decisions of Sales Management. Explain It in The Context of Any CompanyAbhinav KumarNo ratings yet

- Solectron Case Group 8Document35 pagesSolectron Case Group 8Abhinav KumarNo ratings yet

- FPR - Studentwork Sheet.Document32 pagesFPR - Studentwork Sheet.Abhinav KumarNo ratings yet

- Intro - StudentsDocument4 pagesIntro - StudentsAbhinav KumarNo ratings yet

- Free 8 Petals DiagramDocument2 pagesFree 8 Petals DiagramAbhinav KumarNo ratings yet

- Case 2 Compress PDFDocument17 pagesCase 2 Compress PDFAbhinav KumarNo ratings yet

- TVM - Support FileDocument13 pagesTVM - Support FileAbhinav KumarNo ratings yet

- Wa0001.Document6 pagesWa0001.Abhinav KumarNo ratings yet

- NSE Smart ManualDocument334 pagesNSE Smart ManualAbhinav KumarNo ratings yet

- Portfolio Support FileDocument9 pagesPortfolio Support FileAbhinav KumarNo ratings yet

- PomnDocument5 pagesPomnAbhinav KumarNo ratings yet

- Fishbay - in MIS PresentationDocument9 pagesFishbay - in MIS PresentationAbhinav KumarNo ratings yet

- TREDS WebsiteDocument37 pagesTREDS WebsiteAbhinav KumarNo ratings yet

- Interview 1 TranscriptDocument1 pageInterview 1 TranscriptAbhinav KumarNo ratings yet

- GDP and GNPDocument1 pageGDP and GNPAbhinav KumarNo ratings yet

- TranscriptDocument3 pagesTranscriptAbhinav KumarNo ratings yet

- Olivo's Omega-11Document22 pagesOlivo's Omega-11Abhinav KumarNo ratings yet

- Social Customer Relationship Management (SCRM) - Application and TechnologyDocument9 pagesSocial Customer Relationship Management (SCRM) - Application and TechnologyThu TrangNo ratings yet

- What Is The Difference Between The Puncture and The Flashover of An Insulator - QuoraDocument3 pagesWhat Is The Difference Between The Puncture and The Flashover of An Insulator - QuorasanjuNo ratings yet

- HAL S3201 - Brochure 2011 - NopricesDocument6 pagesHAL S3201 - Brochure 2011 - NopricesOmar García MuñozNo ratings yet

- Help Utf8Document8 pagesHelp Utf8Jorge Diaz LastraNo ratings yet

- Finite Element Analysis of Suction Penetration Seepage Field of Bucket Foundation Platform With Application To Offshore Oilfield DevelopmentDocument9 pagesFinite Element Analysis of Suction Penetration Seepage Field of Bucket Foundation Platform With Application To Offshore Oilfield DevelopmentRayodcNo ratings yet

- Power FinanceDocument2 pagesPower FinancedesikanttNo ratings yet

- Sales Order Demo PolicyDocument4 pagesSales Order Demo Policysindhura2258No ratings yet

- Money and BankingDocument20 pagesMoney and BankingFAH EEMNo ratings yet

- Types of Flooring in HospitalDocument6 pagesTypes of Flooring in HospitalFiza Amim KhanNo ratings yet

- Vacancy For Ceo-Tanzania Association of Accountants-RevisedDocument2 pagesVacancy For Ceo-Tanzania Association of Accountants-RevisedOthman MichuziNo ratings yet

- Sekar KSP - Hypoglicemia Ec Tipe 2 DMDocument28 pagesSekar KSP - Hypoglicemia Ec Tipe 2 DMdianarahimmNo ratings yet

- Journal NeuroDocument15 pagesJournal Neurorwong1231No ratings yet

- Cantor Set FunctionDocument15 pagesCantor Set FunctionRenato GaloisNo ratings yet

- Fundamental of Image ProcessingDocument23 pagesFundamental of Image ProcessingSyeda Umme Ayman ShoityNo ratings yet

- Vitamins and Minerals Lecture NotesDocument9 pagesVitamins and Minerals Lecture NotesJoymae Olivares Tamayo100% (1)

- SPM Practice June 29Document7 pagesSPM Practice June 29Isabel GohNo ratings yet

- PHC Revised Plan: Roads & Buildings Dept. M.G. Road VijayawadaDocument1 pagePHC Revised Plan: Roads & Buildings Dept. M.G. Road VijayawadaTirupathi RajaNo ratings yet

- Part - I: Subjective Questions: Introduction To ChemistryDocument7 pagesPart - I: Subjective Questions: Introduction To ChemistryMohini DeviNo ratings yet

- Partners Case CCMNDocument4 pagesPartners Case CCMNapi-314349758No ratings yet

- Reading Comprehension Read The Article Below and Then Answer The Questions That FollowDocument4 pagesReading Comprehension Read The Article Below and Then Answer The Questions That Followjuan m isazaNo ratings yet

- Vmware Esx Server 3.5 Installation Guide: Devoloped By: KalamDocument24 pagesVmware Esx Server 3.5 Installation Guide: Devoloped By: KalamKarimulla KolimiNo ratings yet

- R 69 CP TDSDocument2 pagesR 69 CP TDSKripesh Kumar DubeyNo ratings yet

- Phlebotomy Essentials 5th Edition Ebook PDFDocument61 pagesPhlebotomy Essentials 5th Edition Ebook PDFeric.rodriguez669100% (42)

- FS2122-INCOMETAX-01A: BSA 1202 Atty. F. R. SorianoDocument7 pagesFS2122-INCOMETAX-01A: BSA 1202 Atty. F. R. SorianoKatring O.No ratings yet

- An Introduction To Mount EverestDocument4 pagesAn Introduction To Mount EverestJihad HasanNo ratings yet