You might also like

- Shift Report: Availability Performance Rate Quality Products RateDocument6 pagesShift Report: Availability Performance Rate Quality Products RatehwhhadiNo ratings yet

- Ia Chapter 11-12Document4 pagesIa Chapter 11-12Marinella LosaNo ratings yet

- Top 10 Warehouse ManagementDocument48 pagesTop 10 Warehouse ManagementmmarizNo ratings yet

- Orca Share Media1547030319812Document523 pagesOrca Share Media1547030319812Maureen Joy Andrada80% (10)

- Current Liabilities Quiz No. 1 (September 10, 2020)Document5 pagesCurrent Liabilities Quiz No. 1 (September 10, 2020)Carlo De VeraNo ratings yet

- 09 Chapter # 9 - InventoriesDocument29 pages09 Chapter # 9 - InventoriesNiña Yna Franchesca PantallaNo ratings yet

- Part 10Document5 pagesPart 10chimchimcoliNo ratings yet

- Question 1: SolutionDocument15 pagesQuestion 1: Solutiondebate ddNo ratings yet

- InventoriesDocument64 pagesInventoriesMarjorie PalmaNo ratings yet

- Prelim Review Docx 427399963 Prelim ReviewDocument42 pagesPrelim Review Docx 427399963 Prelim ReviewMarjorie PalmaNo ratings yet

- Problems On Gross Profit Method and ManufacturingDocument5 pagesProblems On Gross Profit Method and Manufacturingcriszel4sobejanaNo ratings yet

- Problem 1: University of San Jose-Recoletos Auditing ProblemsDocument9 pagesProblem 1: University of San Jose-Recoletos Auditing ProblemsPaul Doroin100% (1)

- Problem 10-1 Problem 10-2Document13 pagesProblem 10-1 Problem 10-2Yen YenNo ratings yet

- ACCTG102 MidtermQ2 InventoriesDocument10 pagesACCTG102 MidtermQ2 InventoriesDayan DudosNo ratings yet

- Cost of CapitalDocument10 pagesCost of CapitalCharmaine ChuNo ratings yet

- ACCTG102 - PrelimSW4 Accounts Receivable Part 1 Answer KeyDocument2 pagesACCTG102 - PrelimSW4 Accounts Receivable Part 1 Answer KeyJessica Albaracin100% (1)

- Ingredients Quantity Unit Cost/Unit ExtDocument5 pagesIngredients Quantity Unit Cost/Unit Extdebate ddNo ratings yet

- Problems - Inventory Estimation: Retail Inventory MethodDocument13 pagesProblems - Inventory Estimation: Retail Inventory MethodKez MaxNo ratings yet

- May 2020 - AP Drill 3 (Investments and Inventories) - Answer KeyDocument7 pagesMay 2020 - AP Drill 3 (Investments and Inventories) - Answer KeyROMAR A. PIGANo ratings yet

- Quarantine Company, A Manufacturer of Small Tools, Provided The Following Information For The Year Ended December 31, 2019Document9 pagesQuarantine Company, A Manufacturer of Small Tools, Provided The Following Information For The Year Ended December 31, 2019Ann louNo ratings yet

- InventoriesDocument64 pagesInventoriesJoey WassigNo ratings yet

- This Study Resource Was: B. Cost of Designing Products For Specific CustomersDocument6 pagesThis Study Resource Was: B. Cost of Designing Products For Specific CustomersSha RaNo ratings yet

- Financial Accounting P 1 Quiz 3 KeyDocument6 pagesFinancial Accounting P 1 Quiz 3 KeyJei CincoNo ratings yet

- Chapter 12: Leverage and Capital StructureDocument26 pagesChapter 12: Leverage and Capital Structuredebate ddNo ratings yet

- Case 7 SolutionsDocument3 pagesCase 7 SolutionsMichale Jacomilla50% (2)

- Financial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CDocument15 pagesFinancial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CAngelo PayawalNo ratings yet

- (02D) Inventories Assignment 02 ANSWER KEYDocument9 pages(02D) Inventories Assignment 02 ANSWER KEYGabriel Adrian ObungenNo ratings yet

- Content: Practice Exams: Chapter Six and Seven (Notes Receivable) Practice ProblemsDocument10 pagesContent: Practice Exams: Chapter Six and Seven (Notes Receivable) Practice ProblemsTrina Mae GarciaNo ratings yet

- Module 4.2 Activity-Based Costing ProblemsDocument5 pagesModule 4.2 Activity-Based Costing ProblemsDanica Ramos100% (1)

- This Study Resource WasDocument9 pagesThis Study Resource WasMarjorie PalmaNo ratings yet

- Problem No.1: D. P147,000 C. P349,000 C. P639,000Document6 pagesProblem No.1: D. P147,000 C. P349,000 C. P639,000debate ddNo ratings yet

- SDocument15 pagesSdebate ddNo ratings yet

- Write Down of Inventory To Net Realizable Value3Document4 pagesWrite Down of Inventory To Net Realizable Value3CJ alandy100% (1)

- Sample Barangay BudgetDocument17 pagesSample Barangay Budgetnilo bia100% (4)

- RamosDocument2 pagesRamosAustine FloresNo ratings yet

- Proof of Cash Cebu CompanyDocument6 pagesProof of Cash Cebu CompanyCJ alandyNo ratings yet

- Problem 12-2 To 6Document3 pagesProblem 12-2 To 6MYCO PONCE PAQUENo ratings yet

- Chapter 12 FinalDocument19 pagesChapter 12 FinalMichael Hu100% (1)

- CashDocument7 pagesCashhellohello100% (1)

- Cash Shortage Computation: SolutionDocument4 pagesCash Shortage Computation: SolutionCJ alandyNo ratings yet

- Chapter 4 AnswersDocument6 pagesChapter 4 AnswersDomingo PaguioNo ratings yet

- Activity Sheets in Precalculus Quarter 2, Week 1& 2Document7 pagesActivity Sheets in Precalculus Quarter 2, Week 1& 2debate ddNo ratings yet

- Cpa P1Document27 pagesCpa P1Chrisia67% (3)

- Capstone Project-Grainger and Bosch: Digital Marketing CampaignDocument25 pagesCapstone Project-Grainger and Bosch: Digital Marketing Campaignk.saikumar100% (1)

- Actg 431 Quiz Week 7 Practical Accounting I (Part II) Inventories QuizDocument4 pagesActg 431 Quiz Week 7 Practical Accounting I (Part II) Inventories QuizMarilou Arcillas PanisalesNo ratings yet

- Sarmiento, Shayne Angela - Exercises-Inventories P-1Document4 pagesSarmiento, Shayne Angela - Exercises-Inventories P-1SHAYNE ANGELA SARMIENTONo ratings yet

- p2 Guerrero ch15Document30 pagesp2 Guerrero ch15Clarissa Teodoro100% (1)

- Examination About Investment 2Document2 pagesExamination About Investment 2BLACKPINKLisaRoseJisooJennieNo ratings yet

- Nissan FinalDocument4 pagesNissan FinalPrince Jayanmar BerbaNo ratings yet

- Walleye Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageWalleye Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Bleak Company Requirement A Debit Credit Requirement BDocument2 pagesBleak Company Requirement A Debit Credit Requirement BAnonn100% (1)

- Auditing Report CASE11Document18 pagesAuditing Report CASE11Coke Aidenry Saludo0% (1)

- HO 11 - Inventory EstimationDocument4 pagesHO 11 - Inventory EstimationMakoy BixenmanNo ratings yet

- Seatwork 2B ASSIGNDocument5 pagesSeatwork 2B ASSIGNYzzabel Denise L. Tolentino100% (1)

- Audit of Invest. in Equity and Debt SecuritiesDocument23 pagesAudit of Invest. in Equity and Debt SecuritiesJoseph SalidoNo ratings yet

- P 1Document8 pagesP 1Ken Mosende TakizawaNo ratings yet

- The Following Data Pertain To Lincoln Corporation On December 31Document8 pagesThe Following Data Pertain To Lincoln Corporation On December 31Eiuol Nhoj Arraeugse100% (3)

- DocDocument6 pagesDocBanana QNo ratings yet

- Audit Problem Inventories AnswerDocument6 pagesAudit Problem Inventories AnswerJames PaulNo ratings yet

- Ia 2Document2 pagesIa 2Nadine SofiaNo ratings yet

- Audit Prob Cash AnsDocument7 pagesAudit Prob Cash AnsNoreen BinagNo ratings yet

- Chapter 26 - Inventory Cost Flow: Question 26-1Document11 pagesChapter 26 - Inventory Cost Flow: Question 26-1Cyrus IsanaNo ratings yet

- This Study Resource Was Shared Via: Solution 23-2 Answer DDocument5 pagesThis Study Resource Was Shared Via: Solution 23-2 Answer DDummy GoogleNo ratings yet

- This Study Resource Was: Return It After Use. Thank You and GODBLESS!Document6 pagesThis Study Resource Was: Return It After Use. Thank You and GODBLESS!Stephanie LeeNo ratings yet

- Lecture Notes On Inventories - 000Document8 pagesLecture Notes On Inventories - 000judel ArielNo ratings yet

- CasDocument29 pagesCasJunneth Pearl Homoc0% (1)

- Ae 103 QuizDocument17 pagesAe 103 Quizlolli lollipopNo ratings yet

- ACt1104 Final Quiz No. 1wit AnsDocument7 pagesACt1104 Final Quiz No. 1wit AnsDyenNo ratings yet

- This Study Resource Was: F-ACADL-01Document8 pagesThis Study Resource Was: F-ACADL-01Marjorie PalmaNo ratings yet

- Examination About Investment 7Document3 pagesExamination About Investment 7BLACKPINKLisaRoseJisooJennieNo ratings yet

- CHEER UP Chapter 13 Gross Profit MethodDocument7 pagesCHEER UP Chapter 13 Gross Profit MethodaprilNo ratings yet

- Joint & by ProductsDocument10 pagesJoint & by Productsharry severino0% (1)

- Intermediate Accounting Chapter 17 and 18Document9 pagesIntermediate Accounting Chapter 17 and 18avilastephjaneNo ratings yet

- 79 157 1 SM PDFDocument34 pages79 157 1 SM PDFGena Aquino-ArcayeraNo ratings yet

- This Study Resource Was: Page 1 of 5Document5 pagesThis Study Resource Was: Page 1 of 5debate ddNo ratings yet

- Hapter 6: International Trade and InvestmentDocument40 pagesHapter 6: International Trade and Investmentdebate ddNo ratings yet

- This Study Resource WasDocument9 pagesThis Study Resource Wasdebate ddNo ratings yet

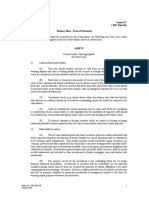

- "Annex K" (SRC Rule 68) Balance Sheet - Form of StatementDocument9 pages"Annex K" (SRC Rule 68) Balance Sheet - Form of StatementBelle MadrigalNo ratings yet

- Module21 Version2010 02 PDFDocument55 pagesModule21 Version2010 02 PDFChristine Joy OriginalNo ratings yet

- This Study Resource Was: Law On Obligations and ContractsDocument7 pagesThis Study Resource Was: Law On Obligations and Contractsdebate ddNo ratings yet

- Coa C2015-002Document71 pagesCoa C2015-002Pearl AudeNo ratings yet

- COMMISSION ON AUDIT CIRCULAR NO. 81-155 February 23, 1981Document7 pagesCOMMISSION ON AUDIT CIRCULAR NO. 81-155 February 23, 1981debate ddNo ratings yet

- 2020 Statistical Annex Table 1Document4 pages2020 Statistical Annex Table 1The Studio ChromaNo ratings yet

- Coa C2015-002Document71 pagesCoa C2015-002Pearl AudeNo ratings yet

- Precalculus Activity Sheets Q2 w3&4Document2 pagesPrecalculus Activity Sheets Q2 w3&4debate ddNo ratings yet

- SDocument8 pagesSdebate ddNo ratings yet

- Precalculus Activity Sheets Q2 w5&6Document4 pagesPrecalculus Activity Sheets Q2 w5&6debate ddNo ratings yet

- PD1445 PDFDocument37 pagesPD1445 PDFDswdCoaNo ratings yet

- Precalculus Activity Sheets Q2 w7 & 8Document4 pagesPrecalculus Activity Sheets Q2 w7 & 8debate ddNo ratings yet

- Worksheet1 3Document10 pagesWorksheet1 3debate ddNo ratings yet

- AnswersDocument12 pagesAnswersdebate ddNo ratings yet

- DocxDocument1 pageDocxEvelynNo ratings yet

- Quiz 1: Answer: DDocument7 pagesQuiz 1: Answer: DYazan MelhimNo ratings yet

- NUS Engineering SEP Brochure Final PageViewDocument6 pagesNUS Engineering SEP Brochure Final PageViewGlenden KhewNo ratings yet

- 8 General Foods v. NACOCODocument3 pages8 General Foods v. NACOCOShaula FlorestaNo ratings yet

- State of Afghan Cities 2015 Volume - 1Document156 pagesState of Afghan Cities 2015 Volume - 1United Nations Human Settlements Programme (UN-HABITAT)No ratings yet

- Actividad 19 Evidencia 7 Taller "Talking About Logistics, Workshop"Document5 pagesActividad 19 Evidencia 7 Taller "Talking About Logistics, Workshop"claudia gomezNo ratings yet

- Elimination Questions Elimination QuestionsDocument4 pagesElimination Questions Elimination QuestionsasffghjkNo ratings yet

- Management 8th Edition Kinicki Solutions Manual 1Document66 pagesManagement 8th Edition Kinicki Solutions Manual 1rodney100% (52)

- CH 05Document37 pagesCH 05Janna KarapetyanNo ratings yet

- CSE4003 - Cyber Security: Digital Assignment IDocument15 pagesCSE4003 - Cyber Security: Digital Assignment IjustadityabistNo ratings yet

- Chapter 4-Product and Service Design NewDocument104 pagesChapter 4-Product and Service Design Newsp914132No ratings yet

- DIVYA VISHWAKARMA Construction IndustryDocument87 pagesDIVYA VISHWAKARMA Construction IndustryNITISH CHANDRA PANDEYNo ratings yet

- A Case Study Analysis of The Montreal (CANADA) Chapter of The Hells Angels Outlaw Motorcycle Club (HAMC) (1995-2010) : Applying The Crime Business Analysis Matrix (CBAM)Document22 pagesA Case Study Analysis of The Montreal (CANADA) Chapter of The Hells Angels Outlaw Motorcycle Club (HAMC) (1995-2010) : Applying The Crime Business Analysis Matrix (CBAM)Ryan29No ratings yet

- Tenant Verification Form PDFDocument2 pagesTenant Verification Form PDFmohit kumarNo ratings yet

- MG8591 Principles of Management 2,13 MARKS Converted 1Document90 pagesMG8591 Principles of Management 2,13 MARKS Converted 14723 Nilamani M100% (1)

- Borehole Pump Works 3 & 6Document36 pagesBorehole Pump Works 3 & 6abrhamNo ratings yet

- Strategic Analysis and ChoiceDocument13 pagesStrategic Analysis and ChoiceAbhitak MoradabadNo ratings yet

- Money Indian Currency Is Rupees and Paise. Let Us Look at Some Currency Notes and Coins That We UseDocument6 pagesMoney Indian Currency Is Rupees and Paise. Let Us Look at Some Currency Notes and Coins That We UseDhivya APNo ratings yet

- Habtamu SerteDocument17 pagesHabtamu SerteAklilu GirmaNo ratings yet

- Golden Rules For AccountingDocument4 pagesGolden Rules For AccountingRoshani ChaudhariNo ratings yet

- 大萧条:历史与经验Document54 pages大萧条:历史与经验吴宙航No ratings yet

- Listening Test Unit 6Document2 pagesListening Test Unit 6Xuân Bách0% (1)

- Understanding The Leadership Spectrum - Developing The SkillsDocument46 pagesUnderstanding The Leadership Spectrum - Developing The SkillsSam PoliasNo ratings yet

- Indicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesDocument1 pageIndicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesJul A.No ratings yet

- GiftDocument6 pagesGiftalive2flirtNo ratings yet

- G11 1ST SemDocument2 pagesG11 1ST SemKrichel Mikhaela CorroNo ratings yet

- Wiley CFA Test Bank 180527 (20 Preguntas)Document12 pagesWiley CFA Test Bank 180527 (20 Preguntas)rafav10No ratings yet

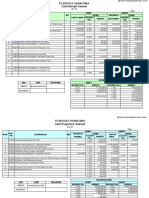

- Amarylis Putri - KERTAS KERJA JURNAL - Sent2Document6 pagesAmarylis Putri - KERTAS KERJA JURNAL - Sent2SatriaArdya10No ratings yet