You might also like

- A New Dawn for Global Value Chain Participation in the PhilippinesFrom EverandA New Dawn for Global Value Chain Participation in the PhilippinesNo ratings yet

- Merger and Acquisition. CIA 1.2docxDocument13 pagesMerger and Acquisition. CIA 1.2docxSaloni Jain 1820343No ratings yet

- Edelwess Report SunDocument5 pagesEdelwess Report SunPrajwal JainNo ratings yet

- BUY Dec. 23, 2009 TARGET: 330: Company BackgroundDocument5 pagesBUY Dec. 23, 2009 TARGET: 330: Company BackgroundnanostrNo ratings yet

- PMSGDSEP2022Document292 pagesPMSGDSEP2022Rohan ShahNo ratings yet

- ICICI Securities General Insurance Sector UpdateDocument7 pagesICICI Securities General Insurance Sector UpdateDeepak VermaNo ratings yet

- Buy Bio Con LTDDocument6 pagesBuy Bio Con LTDshashi_svtNo ratings yet

- Piramal Enterprises: Pharma: A Solid Mix of Services/products/distributionDocument18 pagesPiramal Enterprises: Pharma: A Solid Mix of Services/products/distributionIntelligent InvestingNo ratings yet

- Cipla Report - Doc Gourav Cygnus RecoveredDocument32 pagesCipla Report - Doc Gourav Cygnus RecoveredRohit BhansaliNo ratings yet

- Dabur Buy ICICIDirect 20200731 PDFDocument9 pagesDabur Buy ICICIDirect 20200731 PDFHitendra PanchalNo ratings yet

- IOL Chemical and PharmaceuticalsDocument31 pagesIOL Chemical and PharmaceuticalsamsukdNo ratings yet

- Medium Term Call - Glenmark PharmaDocument5 pagesMedium Term Call - Glenmark PharmavyasmusicNo ratings yet

- Media and Entertainment Industry BriefDocument11 pagesMedia and Entertainment Industry Briefrutveek shahNo ratings yet

- Consumer 2. Marketing Intermediaries 3. Suppliers 4. CompetitionDocument3 pagesConsumer 2. Marketing Intermediaries 3. Suppliers 4. CompetitionDeep NainwaniNo ratings yet

- October 2020 FactsheetDocument2 pagesOctober 2020 FactsheetMohit AgarwalNo ratings yet

- Supplementary GN GICDocument20 pagesSupplementary GN GICABC 123No ratings yet

- Macquarie Banking & Insurance CoverageDocument19 pagesMacquarie Banking & Insurance CoverageManipal SinghNo ratings yet

- Pharmaceutical Industry: Financial Status AnalysisDocument31 pagesPharmaceutical Industry: Financial Status AnalysisTushar GoelNo ratings yet

- Bhaskar Gowda m4Document11 pagesBhaskar Gowda m4chinmai gowda mNo ratings yet

- Piramal Enterprises: Building Scalable Differentiated Pharma BusinessDocument14 pagesPiramal Enterprises: Building Scalable Differentiated Pharma BusinessEcho WackoNo ratings yet

- Sushil Finance Initiating Coverage On Eveready Industries IndiaDocument15 pagesSushil Finance Initiating Coverage On Eveready Industries IndiamisfitmedicoNo ratings yet

- End Term Exam DCP 2021Document4 pagesEnd Term Exam DCP 2021PuneetNo ratings yet

- Nirmal Bang 26th July 2018 IPO NoteDocument13 pagesNirmal Bang 26th July 2018 IPO NoteNiruNo ratings yet

- Ambit Disruption Series Vol 9 - Life InsuranceDocument15 pagesAmbit Disruption Series Vol 9 - Life InsuranceSriram RanganathanNo ratings yet

- Company Update 6M22Document34 pagesCompany Update 6M22MichaelNo ratings yet

- Hikal LTD: Crop Protection Propels Growth But Margins MissDocument10 pagesHikal LTD: Crop Protection Propels Growth But Margins MissRakesh KumarNo ratings yet

- Abbott India LTD - Initiating Coverage - 10082020 - 10-08-2020 - 08Document11 pagesAbbott India LTD - Initiating Coverage - 10082020 - 10-08-2020 - 08Sarah AliceNo ratings yet

- ED+ Factsheet JuneDocument1 pageED+ Factsheet JunejagsNo ratings yet

- Aditya Birla Nuvo Limited: ResearchDocument9 pagesAditya Birla Nuvo Limited: ResearchravustinNo ratings yet

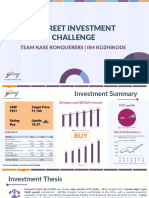

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- Biocon: CMP: INR359 On Course To Revive Earnings GrowthDocument8 pagesBiocon: CMP: INR359 On Course To Revive Earnings GrowthRomelu MartialNo ratings yet

- Not Rated: Itama RanorayaDocument18 pagesNot Rated: Itama RanorayaMuhammad Usamah ArifiantoNo ratings yet

- ACI LimitedDocument6 pagesACI Limitedtanvir616No ratings yet

- 1613233502-InvestorPresentation-February2021 Fermenta BiotechDocument34 pages1613233502-InvestorPresentation-February2021 Fermenta Biotechravi.youNo ratings yet

- PC - Cadila Co Update - May 2021 20210514005224 PDFDocument7 pagesPC - Cadila Co Update - May 2021 20210514005224 PDFAniket DhanukaNo ratings yet

- Equity Valuation Report On Square Pharmaceuticals Limited (Update)Document34 pagesEquity Valuation Report On Square Pharmaceuticals Limited (Update)maybelNo ratings yet

- Company Update FY20 AuDocument34 pagesCompany Update FY20 AuA. NurhidayatiNo ratings yet

- Dividend Policy Electrical Goods Philips, Havells, Aamron: Post Graduate Diploma in ManagementDocument5 pagesDividend Policy Electrical Goods Philips, Havells, Aamron: Post Graduate Diploma in ManagementRohan RoyNo ratings yet

- PC - PolicyBazar Sep 2021 20210921201954Document18 pagesPC - PolicyBazar Sep 2021 20210921201954NavinNo ratings yet

- ICICI Securities Tarsons Re Initiating CoverageDocument14 pagesICICI Securities Tarsons Re Initiating CoverageGaurav ChandnaNo ratings yet

- The Kotak Mahindra Group An Overview: #DiscoverkliDocument6 pagesThe Kotak Mahindra Group An Overview: #DiscoverkliNalla ThambiNo ratings yet

- Merus LabsDocument20 pagesMerus LabsJenny QuachNo ratings yet

- Diwalipicks 2020Document4 pagesDiwalipicks 2020Vimal SharmaNo ratings yet

- VB Report 2Document38 pagesVB Report 2Vandit BatlaNo ratings yet

- Aditya Birla Capital: Performance HighlightsDocument3 pagesAditya Birla Capital: Performance HighlightsdarshanmadeNo ratings yet

- Biofarma Group - KFTD February - Rakernas - Pak AyubDocument15 pagesBiofarma Group - KFTD February - Rakernas - Pak AyubMuammar AlfarouqNo ratings yet

- Studds Accessories LimitedDocument4 pagesStudds Accessories LimitedVivek SinghalNo ratings yet

- ITC Investment Thesis PDFDocument5 pagesITC Investment Thesis PDFAdarsh Poojary100% (1)

- IDBI Capital FMCG Sector UpdateDocument177 pagesIDBI Capital FMCG Sector UpdateHimani SinghalNo ratings yet

- Weekly Wrap - 24-28 July - ICICIDirectDocument11 pagesWeekly Wrap - 24-28 July - ICICIDirectAditi WareNo ratings yet

- Information Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsDocument8 pagesInformation Technology: Covid-19, Oil Price Dip To Pose Near Term HeadwindsdidwaniasNo ratings yet

- 2017 08 - Indoco - Nirmal BangDocument5 pages2017 08 - Indoco - Nirmal Bangnarayanan_rNo ratings yet

- Sun Pharma: US Specialty Progress To Re-RateDocument7 pagesSun Pharma: US Specialty Progress To Re-RateRaghvendra N DhootNo ratings yet

- Glenmark Pharmaceuticals Limited - Investor Presentation - Q3 FY24Document19 pagesGlenmark Pharmaceuticals Limited - Investor Presentation - Q3 FY24SHREYA NAIRNo ratings yet

- Heranba Industries IPO Note ICICI DirectDocument12 pagesHeranba Industries IPO Note ICICI DirectVasim MerchantNo ratings yet

- Cornell EMI Case - Campus RoundDocument20 pagesCornell EMI Case - Campus Roundkunal patilNo ratings yet

- Silo 19apr21rev.19 04 2021 - 01 00 19 - QLA6BDocument13 pagesSilo 19apr21rev.19 04 2021 - 01 00 19 - QLA6BSaladin JaysiNo ratings yet

- Dabur Revenue - Dabur India Business To See High Single-Digit Revenue Growth On A Very High Base - The Economic TimesDocument2 pagesDabur Revenue - Dabur India Business To See High Single-Digit Revenue Growth On A Very High Base - The Economic TimesstarNo ratings yet

- Sector Capsule: Oral Care in India: Key Data FindingsDocument3 pagesSector Capsule: Oral Care in India: Key Data FindingsShriniket PatilNo ratings yet

- Bharti Airtel (Bse: Bhartiartl) : Share PerformanceDocument5 pagesBharti Airtel (Bse: Bhartiartl) : Share PerformanceSrinivas NandikantiNo ratings yet

- +status Note On Npa/ Stressed Borrower (Rs.5 Crores N Above) Branch-Chennai Zone - Chennai NBG-South M/s Hallmark Living Space Private LimitedDocument2 pages+status Note On Npa/ Stressed Borrower (Rs.5 Crores N Above) Branch-Chennai Zone - Chennai NBG-South M/s Hallmark Living Space Private LimitedAbhijit TripathiNo ratings yet

- American Rubber V CIR, 1975Document12 pagesAmerican Rubber V CIR, 1975Rald RamirezNo ratings yet

- Delima, Gail Dennisse F. - Customs of The TagalogsDocument2 pagesDelima, Gail Dennisse F. - Customs of The TagalogsGail DelimaNo ratings yet

- HC Bars New Licence For Builders Using Groundwater in GurgaonDocument7 pagesHC Bars New Licence For Builders Using Groundwater in GurgaonRakeshNo ratings yet

- Evidence - 021922Document2 pagesEvidence - 021922DANICA FLORESNo ratings yet

- Nkandu Vs People 13th June 2017Document21 pagesNkandu Vs People 13th June 2017HanzelNo ratings yet

- Employment Application Form: Private & ConfidentialDocument5 pagesEmployment Application Form: Private & ConfidentialMaleni JayasankarNo ratings yet

- It deters criminals from committing serious crimes. Common sense tells us that the most frightening thing for a human being is to lose their life; therefore, the death penalty is the best deterrent when it comes (1).pdfDocument3 pagesIt deters criminals from committing serious crimes. Common sense tells us that the most frightening thing for a human being is to lose their life; therefore, the death penalty is the best deterrent when it comes (1).pdfJasmine AlbaNo ratings yet

- Topic 3 - Overview: Licensing Exam Paper 1 Topic 3Document16 pagesTopic 3 - Overview: Licensing Exam Paper 1 Topic 3anonlukeNo ratings yet

- Specialized Crime Investigation 1 With Legal Medicine: Bataan Heroes CollegeDocument10 pagesSpecialized Crime Investigation 1 With Legal Medicine: Bataan Heroes CollegePatricia Mae HerreraNo ratings yet

- What Are Some of The Most Notable Pharmaceutical Scandals in History?Document6 pagesWhat Are Some of The Most Notable Pharmaceutical Scandals in History?beneNo ratings yet

- A Critical Analysis of Arguments (Most Recent)Document3 pagesA Critical Analysis of Arguments (Most Recent)diddy_8514No ratings yet

- FECR - Sac City Man Accused of Parole Violation PDFDocument4 pagesFECR - Sac City Man Accused of Parole Violation PDFthesacnewsNo ratings yet

- Gift DeedDocument9 pagesGift DeedHarjot SinghNo ratings yet

- Chapter 04 - Consolidated Financial Statements and Outside OwnershipDocument21 pagesChapter 04 - Consolidated Financial Statements and Outside OwnershipSu EdNo ratings yet

- in India, Is There A Way I Can Buy A Vehicle in One State and Register It in AnotherDocument9 pagesin India, Is There A Way I Can Buy A Vehicle in One State and Register It in AnotherVikas JainNo ratings yet

- Punjab Rented Premises Act 2009Document13 pagesPunjab Rented Premises Act 2009humayun naseerNo ratings yet

- Ratio and Fs AnalysisDocument74 pagesRatio and Fs AnalysisRubie Corpuz SimanganNo ratings yet

- Syllabus UCC Business Law and Taxation IntegrationDocument9 pagesSyllabus UCC Business Law and Taxation IntegrationArki Torni100% (1)

- Ellen G. White's Writings - Their Role and FunctionDocument108 pagesEllen G. White's Writings - Their Role and FunctionAntonio BernardNo ratings yet

- Manila Standard Today - August 23, 2012 IssueDocument12 pagesManila Standard Today - August 23, 2012 IssueManila Standard TodayNo ratings yet

- Electronic Reservation Slip (ERS) : 4236392455 12704/falaknuma Exp Ac 2 Tier Sleeper (2A)Document2 pagesElectronic Reservation Slip (ERS) : 4236392455 12704/falaknuma Exp Ac 2 Tier Sleeper (2A)SP BabaiNo ratings yet

- Legal Aspects of NursingDocument95 pagesLegal Aspects of NursingHannah aswiniNo ratings yet

- Prophethood and Its Importance, The Life and Unique Qualities of Prophet Muhammad (Saw) CHP# 6Document28 pagesProphethood and Its Importance, The Life and Unique Qualities of Prophet Muhammad (Saw) CHP# 6Saman BaigNo ratings yet

- Tutorial III Agreement of Sale: Submitted byDocument6 pagesTutorial III Agreement of Sale: Submitted byManasi DicholkarNo ratings yet

- BSPHCL Recruitment Notification For AssistantDocument7 pagesBSPHCL Recruitment Notification For AssistantSanjana Krishna KumarNo ratings yet

- The Unbecoming of Mara DyerDocument6 pagesThe Unbecoming of Mara DyerKasshika Nigam75% (4)

- A76XX Series - Dual SIM - Application Note - V1.02Document20 pagesA76XX Series - Dual SIM - Application Note - V1.02vakif.techNo ratings yet

- Acctg 16a - Midterm Exam PDFDocument5 pagesAcctg 16a - Midterm Exam PDFMary Grace Castillo AlmonedaNo ratings yet

- Position Paper CarnappingDocument11 pagesPosition Paper CarnappingIgorot HectorNo ratings yet