You might also like

- Accel Partners VIIDocument17 pagesAccel Partners VIIfaskunjiNo ratings yet

- ARR Saas Revenue Forecast Field ServicesDocument25 pagesARR Saas Revenue Forecast Field Servicespankaj kumar100% (1)

- Assessment Task 2 - BSBADM405Document29 pagesAssessment Task 2 - BSBADM405AndresPrada0% (1)

- Assessment Task 2 - BSBADM405Document29 pagesAssessment Task 2 - BSBADM405AndresPrada0% (1)

- Uganda Implementing An IFMSDocument6 pagesUganda Implementing An IFMSkhan_sadi100% (1)

- IIBM Case Study AnswersDocument98 pagesIIBM Case Study AnswersAravind 9901366442 - 990278722422% (9)

- Anual Julio Agosto Septiembre Octubre Noviembre Diciembre Junio Enero Febrero Marzo Abril MayoDocument1 pageAnual Julio Agosto Septiembre Octubre Noviembre Diciembre Junio Enero Febrero Marzo Abril MayoMaira Alejandra LEAL NAVARRONo ratings yet

- Coffeeville: Financial ProjectionsDocument6 pagesCoffeeville: Financial ProjectionsAndresPradaNo ratings yet

- Financial Plan TemplateDocument8 pagesFinancial Plan Templatenomaden_09No ratings yet

- BSyS HojaModeloDocument1 pageBSyS HojaModelofelipevinuesaNo ratings yet

- Feed. LerhetDocument35 pagesFeed. LerhetfuadzeyniNo ratings yet

- Rojas Rosario ExcelmasteryDocument12 pagesRojas Rosario Excelmasteryapi-377244071No ratings yet

- Proyeccion FinancieraDocument1 pageProyeccion FinancieraFelixCoutiñoCorderoNo ratings yet

- Monthly budget and expenses breakdownDocument5 pagesMonthly budget and expenses breakdownAn MaNo ratings yet

- Financial PlanDocument86 pagesFinancial PlanVõ Thị Ngọc HuyềnNo ratings yet

- SITXFIN004 AssignmentDocument21 pagesSITXFIN004 AssignmentNateeNo ratings yet

- SEO-optimized title for a balance sheet document in SpanishDocument6 pagesSEO-optimized title for a balance sheet document in SpanishDaniela RodríguezNo ratings yet

- Finanzas 2022Document18 pagesFinanzas 2022JonatanFierroNo ratings yet

- Add More As You See Fit++Document1 pageAdd More As You See Fit++dendy wayNo ratings yet

- Rental Home Financial Projection TemplateDocument61 pagesRental Home Financial Projection TemplateMinh NguyenNo ratings yet

- 03-M2 Personal Finance SpreadsheetDocument20 pages03-M2 Personal Finance SpreadsheetAtlass StoreNo ratings yet

- Martinez CompanyDocument45 pagesMartinez CompanyZairi IbrahimNo ratings yet

- Proyección Financiera 2023Document4 pagesProyección Financiera 2023Esteban FierroNo ratings yet

- Plantilla Manejo Finanzas PersonalesDocument25 pagesPlantilla Manejo Finanzas PersonalesAngel Francisco Roque RamosNo ratings yet

- Sample Income StatementDocument1 pageSample Income StatementJason100% (34)

- Simple Financial Plan & Unit Economics - Lead Gen - Template - v3.0 by Future Flow - PUBLICDocument52 pagesSimple Financial Plan & Unit Economics - Lead Gen - Template - v3.0 by Future Flow - PUBLICRaúl GuerreroNo ratings yet

- How to build two successful niche sites and earn over $60,000 in two yearsDocument7 pagesHow to build two successful niche sites and earn over $60,000 in two yearsPankaj MeenaNo ratings yet

- Libro Mayor de Negocio - Herramienta (Actualizada) CODocument93 pagesLibro Mayor de Negocio - Herramienta (Actualizada) COsergloos.saloNo ratings yet

- Canizal Uriel ExcelmsteryDocument12 pagesCanizal Uriel Excelmsteryapi-377100988No ratings yet

- SteamDocument8 pagesSteamdulceNo ratings yet

- Product Marketing Budget TemplateDocument8 pagesProduct Marketing Budget TemplateHung HoangNo ratings yet

- Dropshiping PogoDocument5 pagesDropshiping PogoyassineNo ratings yet

- 1992894Document1 page1992894TAMERNo ratings yet

- Akm 233Document6 pagesAkm 233wahdah ulin nafisahNo ratings yet

- Mayorga Brayan ExcelmasteryDocument12 pagesMayorga Brayan Excelmasteryapi-377088945No ratings yet

- Mendez Emily ExcelmasteryDocument8 pagesMendez Emily Excelmasteryapi-377243899No ratings yet

- Spin Premia NegocioDocument8 pagesSpin Premia Negociorobertozenteno771No ratings yet

- 4 TiposDocument4 pages4 TiposCarlos BernadacNo ratings yet

- Liquidación Promedio para Obtener Ibl Pensional (Últimos 10 Años Ó El Tiempo Que Le Hiciere Falta)Document14 pagesLiquidación Promedio para Obtener Ibl Pensional (Últimos 10 Años Ó El Tiempo Que Le Hiciere Falta)alvaraco uribeNo ratings yet

- Cash Flow Statement Year 1-3 with Key MetricsDocument4 pagesCash Flow Statement Year 1-3 with Key MetricsHải Linh NguyễnNo ratings yet

- SEO-Optimized Title for Real Estate Income and Expense ReportDocument7 pagesSEO-Optimized Title for Real Estate Income and Expense ReportᎬᏞᏉᎥᏁ TrinidadNo ratings yet

- Trade and Other Receivables p2Document51 pagesTrade and Other Receivables p2Camille G.No ratings yet

- Budget Summary Report1Document4 pagesBudget Summary Report1MarvvvNo ratings yet

- Calculating your monthly cash flowDocument5 pagesCalculating your monthly cash flowKSXNo ratings yet

- Mónica - Valenzuela - Control 7Document9 pagesMónica - Valenzuela - Control 7Mónica ValenzuelaNo ratings yet

- Backbar Liquor Inventory Spreadsheet TemplateDocument1,672 pagesBackbar Liquor Inventory Spreadsheet Templatenakitare makanaNo ratings yet

- Consolidated financial recordsDocument4 pagesConsolidated financial recordsJulia AnandaNo ratings yet

- Financial Plan For Meet Green: Locally Grown Produce, Chemical-And Preservative-Free GroceriesDocument6 pagesFinancial Plan For Meet Green: Locally Grown Produce, Chemical-And Preservative-Free Groceriesramsha nishatNo ratings yet

- HolaKola HW Model ProvideDocument4 pagesHolaKola HW Model ProvideslmedcalfeNo ratings yet

- Magana Jose Excel MasteryDocument12 pagesMagana Jose Excel Masteryapi-377101001No ratings yet

- Executive SummaryDocument6 pagesExecutive SummaryGio Densel GarciaNo ratings yet

- Shopify Financial Worksheet Template: More Instructions On Cash Flow Management HereDocument6 pagesShopify Financial Worksheet Template: More Instructions On Cash Flow Management HereOLOMOSEDARA IFEOLUWANo ratings yet

- Vital Marketing Budget TemplateDocument45 pagesVital Marketing Budget TemplateShafaat KabirNo ratings yet

- Rif - Bancos - Ing - EgreDocument132 pagesRif - Bancos - Ing - EgreFABIANNo ratings yet

- Cash Flow Forecast ToolDocument11 pagesCash Flow Forecast Toolnessa catarmanNo ratings yet

- Jaxworks PaybackAnalysis1Document1 pageJaxworks PaybackAnalysis1Jo Ann RangelNo ratings yet

- Vital Marketing Budget TemplateDocument45 pagesVital Marketing Budget TemplateDiego Andres Rozo NeptaNo ratings yet

- Blank Cash Flow Template ExcelDocument5 pagesBlank Cash Flow Template ExcelPro ResourcesNo ratings yet

- Gastos Sueldos Local Compra O Renta Materia Prima Maquinaria Y Equip. Transporte Publicidad Material ServiciosDocument1 pageGastos Sueldos Local Compra O Renta Materia Prima Maquinaria Y Equip. Transporte Publicidad Material ServiciosRogeliovaldezNo ratings yet

- 5.3 Estado de Flujo CorregidoDocument3 pages5.3 Estado de Flujo CorregidoBrenda GonzálezNo ratings yet

- Blue Text Cells (Blue Text)Document7 pagesBlue Text Cells (Blue Text)joshua goNo ratings yet

- Reporte de Ingresos y Egresos (Recuperado)Document2 pagesReporte de Ingresos y Egresos (Recuperado)WAGNER CGNo ratings yet

- Complete Trading Journal For ShareDocument3 pagesComplete Trading Journal For ShareHaslina Mohd SallehNo ratings yet

- Project cash flow analysis and investment returnsDocument4 pagesProject cash flow analysis and investment returnsvanesaNo ratings yet

- Perform Keyword ResearchDocument2 pagesPerform Keyword ResearchAngie Fer.No ratings yet

- Do Employees Blame You For Increased Healthcare CostsDocument3 pagesDo Employees Blame You For Increased Healthcare CostsAngie Fer.No ratings yet

- You Understand ACA, But Your Employees Don't (Infographic) : New Affordable Care Act-Compliant Healthcare PlanDocument3 pagesYou Understand ACA, But Your Employees Don't (Infographic) : New Affordable Care Act-Compliant Healthcare PlanAngie Fer.No ratings yet

- Plagiarism Checker ToolDocument2 pagesPlagiarism Checker ToolAngie Fer.No ratings yet

- What Is Content and Why Is It Important For SEODocument2 pagesWhat Is Content and Why Is It Important For SEOAngie Fer.No ratings yet

- How Vacations Benefit Our WorkDocument2 pagesHow Vacations Benefit Our WorkAngie Fer.No ratings yet

- Best Tools To Avoid PlagiarismDocument2 pagesBest Tools To Avoid PlagiarismAngie Fer.No ratings yet

- Need For Online Information Technology Assignment HelpDocument1 pageNeed For Online Information Technology Assignment HelpAngie Fer.No ratings yet

- Human ResourcesDocument2 pagesHuman ResourcesAngie Fer.No ratings yet

- Need For Online It Management Assignment Help ServiceDocument2 pagesNeed For Online It Management Assignment Help ServiceAngie Fer.No ratings yet

- Indirect CostsDocument2 pagesIndirect CostsAngie Fer.No ratings yet

- What Are The Legislative and Regulatory Expectations in Respect of Your Project in AustraliaDocument1 pageWhat Are The Legislative and Regulatory Expectations in Respect of Your Project in AustraliaAngie Fer.No ratings yet

- Order Online Operating System Assignment Help Service NowDocument1 pageOrder Online Operating System Assignment Help Service NowAngie Fer.No ratings yet

- It Management Assignment HelpDocument2 pagesIt Management Assignment HelpAngie Fer.No ratings yet

- BSBFIM601 - Assessment Task 1Document3 pagesBSBFIM601 - Assessment Task 1Angie Fer.No ratings yet

- Information Technology Assignment HelpDocument2 pagesInformation Technology Assignment HelpAngie Fer.No ratings yet

- BSBFIM601 - Assessment Task 1Document13 pagesBSBFIM601 - Assessment Task 1Angie Fer.No ratings yet

- BSBFIM601 Assessment 1 18522Document12 pagesBSBFIM601 Assessment 1 18522Angie Fer.No ratings yet

- Student checklist for business tech and spreadsheets rolesDocument2 pagesStudent checklist for business tech and spreadsheets rolesAngie Fer.No ratings yet

- What Are The Legislative and Regulatory Expectations in Respect of Your Project in AustraliaDocument1 pageWhat Are The Legislative and Regulatory Expectations in Respect of Your Project in AustraliaAngie Fer.No ratings yet

- BSBFIM601 - Assessment Task 1Document13 pagesBSBFIM601 - Assessment Task 1Angie Fer.No ratings yet

- BSBFIM601 Assessment 1 18522Document12 pagesBSBFIM601 Assessment 1 18522Angie Fer.No ratings yet

- Advanced Diploma of Leadership & Management: Part ADocument10 pagesAdvanced Diploma of Leadership & Management: Part AAngie Fer.No ratings yet

- Student checklist for business tech and spreadsheets rolesDocument2 pagesStudent checklist for business tech and spreadsheets rolesAngie Fer.No ratings yet

- BSBFIM601 - Assessment Task 1Document3 pagesBSBFIM601 - Assessment Task 1Angie Fer.No ratings yet

- A. 1Document15 pagesA. 1Angie Fer.No ratings yet

- 1 Org - ChangeDocument50 pages1 Org - ChangeAngie Fer.No ratings yet

- PRTC 1stPB - 05.22 Sol FARDocument7 pagesPRTC 1stPB - 05.22 Sol FARCiatto SpotifyNo ratings yet

- Birch Gold Information KitDocument20 pagesBirch Gold Information KitRexrgisNo ratings yet

- Virtual CFO Services for StartupsDocument15 pagesVirtual CFO Services for StartupsKarun GuptaNo ratings yet

- Bibliography (1) 3 Mcvedited EeDocument4 pagesBibliography (1) 3 Mcvedited EeAmal TP PushpanNo ratings yet

- Used Car Dealers Convicted - The AFC & DSC ConspiracyDocument2 pagesUsed Car Dealers Convicted - The AFC & DSC ConspiracyzacallfordNo ratings yet

- 7110 w15 Ms 22 PDFDocument9 pages7110 w15 Ms 22 PDFRachel RAMSAMYNo ratings yet

- S.Aniker (Apbf2022.35Document28 pagesS.Aniker (Apbf2022.35aniketsuradkar22.imperialNo ratings yet

- Major and Minor Programmes 2022-23Document11 pagesMajor and Minor Programmes 2022-23Kelly lamNo ratings yet

- Midnight Jurnal EntryDocument11 pagesMidnight Jurnal EntryAndharu WisnuNo ratings yet

- The Importance of Information Technology Implementation in Facing Industrial Revolution 4.0: Case Study of Banking IndustryDocument5 pagesThe Importance of Information Technology Implementation in Facing Industrial Revolution 4.0: Case Study of Banking IndustryEditor IJTSRDNo ratings yet

- Dynacon Systems Ar 2017 5323650317Document101 pagesDynacon Systems Ar 2017 5323650317murali_pmp1766No ratings yet

- QuizDocument5 pagesQuizJuvy Jane DuarteNo ratings yet

- Ac20 Quiz 1 - DGCDocument10 pagesAc20 Quiz 1 - DGCMaricar PinedaNo ratings yet

- Annual Report MERK 2012Document108 pagesAnnual Report MERK 2012StefanyNo ratings yet

- Forms of Business OrganizationDocument26 pagesForms of Business Organizationtrustme77No ratings yet

- Exercise Financial Statements Without AdjustmentsDocument3 pagesExercise Financial Statements Without AdjustmentsShahrillNo ratings yet

- D12999R64581 PDFDocument8 pagesD12999R64581 PDFNoor Liza AliNo ratings yet

- Financial ServicesDocument10 pagesFinancial ServicesDinesh Sugumaran100% (4)

- Characteristic Features of Financial InstrumentsDocument17 pagesCharacteristic Features of Financial Instrumentsmanoranjanpatra93% (15)

- Flash Memory Inc Student Spreadsheet SupplementDocument5 pagesFlash Memory Inc Student Spreadsheet Supplementjamn1979No ratings yet

- FAR 6.2MC - Noncurrent Liabilities (Part 1) Notes and Loans PayableDocument4 pagesFAR 6.2MC - Noncurrent Liabilities (Part 1) Notes and Loans Payablekateangel ellesoNo ratings yet

- Demat Services Project ReportDocument35 pagesDemat Services Project Reportjyoti raghuvanshi100% (2)

- Nedbank Case StudyDocument14 pagesNedbank Case Studyambuj joshiNo ratings yet

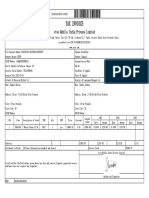

- Tax Invoice: Vivo Mobile India Private LimitedDocument1 pageTax Invoice: Vivo Mobile India Private LimitedRaghav SharmaNo ratings yet

- Amalda Aulia 1810533004 Int - AccountingDocument11 pagesAmalda Aulia 1810533004 Int - AccountingAmalda AuliaNo ratings yet

- Ibm Cognos ProspectingDocument3 pagesIbm Cognos ProspectingtasvirkhaliliNo ratings yet

- DocumentDocument1 pageDocumentVanessa GuardadoNo ratings yet