You might also like

- The Professional and Ethical Duties of the Accountant. ACCA. Paper P2. Students notes.: ACCA studies, #2From EverandThe Professional and Ethical Duties of the Accountant. ACCA. Paper P2. Students notes.: ACCA studies, #2Rating: 4 out of 5 stars4/5 (2)

- At.1304 - Code of EthicsDocument29 pagesAt.1304 - Code of EthicsSheila Mae PlanciaNo ratings yet

- The Code of Professional EthicsDocument50 pagesThe Code of Professional EthicsMicaela MarimlaNo ratings yet

- Lecturer 2 (Ii) - Professional EthicsDocument41 pagesLecturer 2 (Ii) - Professional EthicskhooNo ratings yet

- AT.1304 - Code of EthicsDocument28 pagesAT.1304 - Code of EthicsUzumaki NarutoNo ratings yet

- Code of Ethics For AccountantsDocument49 pagesCode of Ethics For AccountantsAlly CapacioNo ratings yet

- Code of Ethics For Professional AccountantsDocument17 pagesCode of Ethics For Professional AccountantsJay Mark AbellarNo ratings yet

- Audit Chapter 14Document4 pagesAudit Chapter 14Areej AzharNo ratings yet

- Code of Professional EthicsDocument42 pagesCode of Professional EthicsMariella CatacutanNo ratings yet

- Code of Ethics - EditedDocument76 pagesCode of Ethics - EditedAaron Mañacap100% (1)

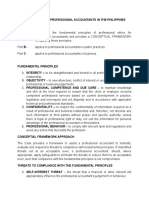

- Code of Ethics For Professional Accountants in The PhilippinesDocument4 pagesCode of Ethics For Professional Accountants in The PhilippinesAlex Ong0% (1)

- Ethics and AcceptanceDocument41 pagesEthics and AcceptanceTaimur ShahidNo ratings yet

- Auditing Ethics: Lecture # 2 Fundamental PrinciplesDocument3 pagesAuditing Ethics: Lecture # 2 Fundamental PrinciplessiddiqueicmaNo ratings yet

- WV&PE Lesson 3Document14 pagesWV&PE Lesson 3Daniel S. GonzalesNo ratings yet

- Professional Ethics in AuditingDocument4 pagesProfessional Ethics in AuditingWaseem Basha SkNo ratings yet

- Lecture Notes - Code of EthicsDocument5 pagesLecture Notes - Code of EthicsHalim Matuan MaamorNo ratings yet

- Auditing TheoryDocument3 pagesAuditing TheoryJereza Joy LastreNo ratings yet

- Chapter 4 - Lesson Outline - StudentDocument28 pagesChapter 4 - Lesson Outline - StudentKim Heok ChuaNo ratings yet

- Code of Ethics for AccountantsDocument78 pagesCode of Ethics for AccountantsNeriza PonceNo ratings yet

- Code of Ethics: For Professional AccountantsDocument130 pagesCode of Ethics: For Professional AccountantsSalvador BrionesNo ratings yet

- Code of Ethics 5th Year Acc. ReviewDocument10 pagesCode of Ethics 5th Year Acc. ReviewCykee Hanna Quizo LumongsodNo ratings yet

- Quiz 1Document13 pagesQuiz 1수지No ratings yet

- 08 JournalDocument6 pages08 Journalits me keiNo ratings yet

- 4 Quality ControlDocument10 pages4 Quality ControlMoffat MakambaNo ratings yet

- Code of Etichs of Professional AccountantsDocument40 pagesCode of Etichs of Professional AccountantsYamateNo ratings yet

- Auditing I CH 2Document36 pagesAuditing I CH 2Hussien AdemNo ratings yet

- Code of Ethics Reviewer - CompressDocument44 pagesCode of Ethics Reviewer - CompressGlance Piscasio CruzNo ratings yet

- De - Guzman - Module 12Document8 pagesDe - Guzman - Module 12Ma Ruby II SantosNo ratings yet

- Key Concepts in AccountingDocument9 pagesKey Concepts in AccountingSunday OcheNo ratings yet

- 23 Code of Ethics For Professional Accountants: An Ethical Practice Is The Bedrock of An Accountant's SuccessDocument46 pages23 Code of Ethics For Professional Accountants: An Ethical Practice Is The Bedrock of An Accountant's SuccesstrishaNo ratings yet

- Code of Ethics For Professional Accountants in The PhilippinesDocument3 pagesCode of Ethics For Professional Accountants in The Philippinesmac mercadoNo ratings yet

- Code of Professional Ethics: The Accountancy Act of 2004Document51 pagesCode of Professional Ethics: The Accountancy Act of 2004Just SomeoneNo ratings yet

- Code of Ethics Summary - P 1 & 2Document9 pagesCode of Ethics Summary - P 1 & 2RafayAliNo ratings yet

- The Code of Professional EthicsDocument33 pagesThe Code of Professional EthicsLaezelie PalajeNo ratings yet

- Pervezvikiyo - 3498 - 17836 - 2 - Ethics, Threats & Safeguards (Nov 1, 2021)Document11 pagesPervezvikiyo - 3498 - 17836 - 2 - Ethics, Threats & Safeguards (Nov 1, 2021)Sadia AbidNo ratings yet

- Chapter 17 ReportingDocument11 pagesChapter 17 ReportingJanine MosatallaNo ratings yet

- Code of EthicsDocument37 pagesCode of EthicsDawn Rei Dangkiw100% (1)

- Opaud Midterm PDFDocument8 pagesOpaud Midterm PDFThea LicupNo ratings yet

- CODE OF ETHICS GUIDEDocument24 pagesCODE OF ETHICS GUIDEMojiNo ratings yet

- Dac 204 Lecture 2Document27 pagesDac 204 Lecture 2raina mattNo ratings yet

- MAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)Document18 pagesMAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)vintmyoNo ratings yet

- Code of EthicsDocument5 pagesCode of EthicsZeus GamoNo ratings yet

- Accounting Ethics: Lect. Victor-Octavian Müller, PH.DDocument7 pagesAccounting Ethics: Lect. Victor-Octavian Müller, PH.DavalentinNo ratings yet

- 4.1 MIA By-Law (On Professional Conducts and Ethics)Document84 pages4.1 MIA By-Law (On Professional Conducts and Ethics)Yaya-Nadia AhmadNo ratings yet

- PROFESSIONAL ACCOUNTANTS CODE OF ETHICSDocument31 pagesPROFESSIONAL ACCOUNTANTS CODE OF ETHICSAJ BlazaNo ratings yet

- Introduction To Audit and Assurance ServicesDocument61 pagesIntroduction To Audit and Assurance ServicesMAAN SHIN ANGNo ratings yet

- AUDIT Journal 8Document12 pagesAUDIT Journal 8Daena NicodemusNo ratings yet

- Intro to Audit & Assurance Lecture 1Document63 pagesIntro to Audit & Assurance Lecture 1Kogilavani a/p ApadoreNo ratings yet

- Understanding Threats and Safeguards in AccountancyDocument20 pagesUnderstanding Threats and Safeguards in AccountancyKezNo ratings yet

- AuditingDocument12 pagesAuditingMY GODNo ratings yet

- W2 Professional Ethics Revised 29 Mac 2021Document33 pagesW2 Professional Ethics Revised 29 Mac 2021YalliniNo ratings yet

- Test Bank For Auditing A Practical Approach 3rd Canadian Edition by Robyn MoroneyDocument35 pagesTest Bank For Auditing A Practical Approach 3rd Canadian Edition by Robyn MoroneyNitin100% (1)

- CODE OF ETHICS For Professional Accountants in TheDocument61 pagesCODE OF ETHICS For Professional Accountants in TheDiana Rose BassigNo ratings yet

- Auditing Client Acceptance ProcedureDocument11 pagesAuditing Client Acceptance Proceduretaohid khanNo ratings yet

- The Code of Ethics For Professional Accountants in The PhilippinesDocument4 pagesThe Code of Ethics For Professional Accountants in The PhilippinesKimberly LimNo ratings yet

- Code of Ethics for CPAs in the PhilippinesDocument24 pagesCode of Ethics for CPAs in the PhilippinesQueenie QuisidoNo ratings yet

- Code of Ethics QuestionsDocument11 pagesCode of Ethics QuestionsAiAiNo ratings yet

- Code of Ethics For Professional AccountantDocument14 pagesCode of Ethics For Professional AccountantClarise Satentes AquinoNo ratings yet

- Slides - Lecture 2 - st versionDocument17 pagesSlides - Lecture 2 - st versionNguyễn Thu UyênNo ratings yet

- 08 Code of Ethics For CPAs in The PhilippinesDocument12 pages08 Code of Ethics For CPAs in The PhilippinesBack Up StorageNo ratings yet

- Chapter 12 - Audit Reports and Communication: Rick Hayes, Hans Gortemaker and Philip WallageDocument42 pagesChapter 12 - Audit Reports and Communication: Rick Hayes, Hans Gortemaker and Philip WallageMichael AnthonyNo ratings yet

- Chapter 1Document52 pagesChapter 1Michael AnthonyNo ratings yet

- Chapter 9Document44 pagesChapter 9Michael AnthonyNo ratings yet

- Chapter 10 - Audit Documentation and Working Papers (Appendix)Document17 pagesChapter 10 - Audit Documentation and Working Papers (Appendix)Michael AnthonyNo ratings yet

- Analytical Procedures Chapter SummaryDocument49 pagesAnalytical Procedures Chapter SummaryMichael AnthonyNo ratings yet

- Chapter 12 - Audit Reports and Communication: Rick Hayes, Hans Gortemaker and Philip WallageDocument42 pagesChapter 12 - Audit Reports and Communication: Rick Hayes, Hans Gortemaker and Philip WallageMichael AnthonyNo ratings yet

- Chapter 1Document52 pagesChapter 1Michael AnthonyNo ratings yet

- Chapter 2Document51 pagesChapter 2Michael AnthonyNo ratings yet

- Chapter 9Document44 pagesChapter 9Michael AnthonyNo ratings yet

- Review QuestionDocument7 pagesReview QuestionMichael AnthonyNo ratings yet

- Chapter 2Document51 pagesChapter 2Michael AnthonyNo ratings yet

- Chapter 5 - Client Acceptance: Rick Hayes, Hans Gortemaker and Philip WallageDocument33 pagesChapter 5 - Client Acceptance: Rick Hayes, Hans Gortemaker and Philip WallageMichael AnthonyNo ratings yet

- Review QuestionDocument7 pagesReview QuestionMichael AnthonyNo ratings yet

- Chapter 1Document52 pagesChapter 1Michael AnthonyNo ratings yet

- Case StudyDocument2 pagesCase StudyСветлана Дирко100% (1)

- AsdDocument2 pagesAsdRenz GuiangNo ratings yet

- CEO Board Report TemplateDocument3 pagesCEO Board Report TemplateMayur Patel100% (1)

- Sgsy Paper: June 2021Document7 pagesSgsy Paper: June 2021ima doucheNo ratings yet

- 8 SIM336 Evaluating StrategyDocument30 pages8 SIM336 Evaluating StrategyigotoschoolbybusNo ratings yet

- Faisel Curriculum VitaeDocument2 pagesFaisel Curriculum VitaeFaisel Ahmed BundyNo ratings yet

- Analytical School JurisprudenceDocument7 pagesAnalytical School JurisprudenceRavi ShenkerNo ratings yet

- Widows and The Matrimonial Home The GapDocument17 pagesWidows and The Matrimonial Home The GapDiana Wangamati100% (1)

- Leading Changes at Simmons Case StudyDocument9 pagesLeading Changes at Simmons Case StudyJanki SolankiNo ratings yet

- Crim Law 1 Case DigestDocument69 pagesCrim Law 1 Case DigestPatricia Jade LimNo ratings yet

- Criterion and Norm-Referenced (Kemuel)Document9 pagesCriterion and Norm-Referenced (Kemuel)Luffy D NatsuNo ratings yet

- Unfair CompetitionDocument8 pagesUnfair CompetitionnandhuNo ratings yet

- 2 - Strategist or TacticianDocument2 pages2 - Strategist or Tacticiangvillacres1627No ratings yet

- Visual Arts Lesson on Variety Using Elements of ArtDocument4 pagesVisual Arts Lesson on Variety Using Elements of ArtIrenejoy RamirezNo ratings yet

- 210311081143rays New Curriculum VitaeDocument3 pages210311081143rays New Curriculum VitaeHamis Rabiam MagundaNo ratings yet

- Anti-fouling certificate for KARADENIZ POWERSHIP ASIMDocument2 pagesAnti-fouling certificate for KARADENIZ POWERSHIP ASIMVirtual ExtrovertNo ratings yet

- Proposal For The Gardens Mardan (Detailed Supervision)Document22 pagesProposal For The Gardens Mardan (Detailed Supervision)Umer KhanNo ratings yet

- International Trade Law Notes - 2Document203 pagesInternational Trade Law Notes - 2Munyaradzi DokoteraNo ratings yet

- Bulletlist - The Marketing ProcessDocument4 pagesBulletlist - The Marketing ProcessSs ArNo ratings yet

- Contextualized School Child Protection and Anti-Bullying PolicyDocument46 pagesContextualized School Child Protection and Anti-Bullying Policykarim100% (2)

- Expectancy Theory (Victor Vroom's)Document8 pagesExpectancy Theory (Victor Vroom's)Pavan Kumar IrrinkiNo ratings yet

- Police Patrol Organization and FunctionsDocument14 pagesPolice Patrol Organization and FunctionsfendyNo ratings yet

- The Use of Mean Kinetic TemperatureDocument13 pagesThe Use of Mean Kinetic TemperatureMykola Kurilo50% (2)

- GAIL CSR Project Boosts Girls Education in UttarakhandDocument34 pagesGAIL CSR Project Boosts Girls Education in UttarakhandKarthik RNo ratings yet

- Joan Batayo ProfileDocument2 pagesJoan Batayo ProfileJong PerrarenNo ratings yet

- EOHSMS-04-F05 EHS Talk & Briefing RecordDocument1 pageEOHSMS-04-F05 EHS Talk & Briefing RecordLisa SwansonNo ratings yet

- Creativity Ted Talks 1Document4 pagesCreativity Ted Talks 1api-528608734No ratings yet

- Extension of Time Standard LettersDocument41 pagesExtension of Time Standard LettersFrancis Aw Soon Lee96% (46)

- Naca and The Naca6409Document1 pageNaca and The Naca6409Kevin ChanNo ratings yet

- Compiled Tasks ICTICT606Document4 pagesCompiled Tasks ICTICT606Ankit AroraNo ratings yet